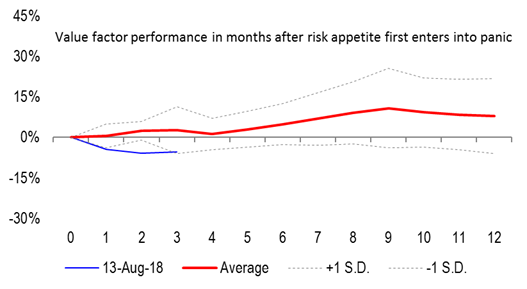

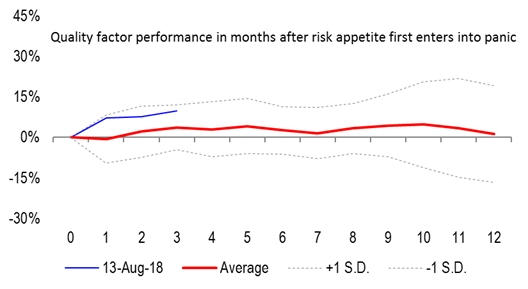

Some nice charts from Damien Bey as Credit Suisse give us context:

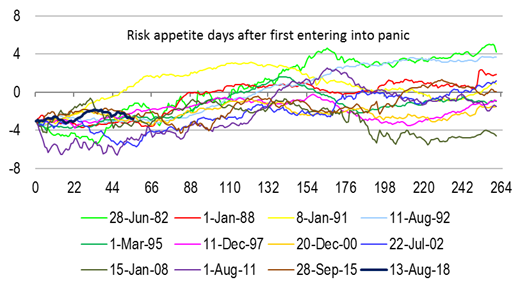

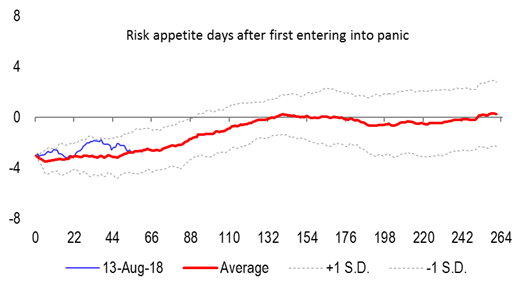

Credit Suisse’s proprietary measure of risk appetite very briefly entered panic in mid-August 2018. It has since staged a modest recovery to less negative levels.

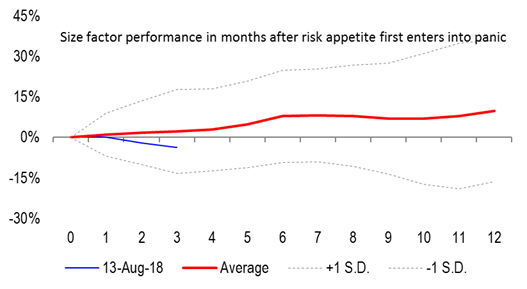

2. Past cycles show that after risk appetite enters panic, small caps tend to outperform in the following year, followed by value and momentum once recovery gains traction. In contrast, quality tends to offer fairly mundane performance.

3. This time could be a little different. Unusually, up to October, quality has been performing quite strongly, while value has been badly undershooting. The performance dispersion is almost statistically significant, even for this early stage of a risk appetite “recovery”.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.