Is it a moose? Or a mounty? No, it’s an Aussie house price leading indicator:

With house prices falling, Australia is entering unknown territory.

Nervousness is gripping the nation. The housing finance data that came out on Friday will only add to that nervousness. A 3.8 per cent fall in lending for housing in just one month? That is huge.

But we don’t need to go forward with eyes closed. Just across the Pacific is a country we can learn from.

Canada’s housing market is a lot like Australia’s. Like us, Canada had no major fall in house prices during the Global Financial Crisis. Like in Australia, official interest rates fell, making borrowing very cheap. House prices soared and household debt went with them.

The epicentres of the boom were Toronto, Canada’s biggest city, and Vancouver, on the Pacific Coast. Their enormous house price boom continued until 2017. Then, while Australia was still appreciating, Toronto suddenly stopped.

…“‘The frenzy is over’: Toronto’s housing bubble finally pops,” screamed the headlines.

What happened next is the surprise. The fall promptly stopped. Toronto stabilised and then prices kept going up.

I don’t want to say that will happen in Australia too. I can’t predict the future. But a lot of people are claiming they can predict the future just because they predicted the falls so far.

This was written by Jason Murphy, a former Treasury economist turned blogger and rerun on News.com. He appears too have been reading too much Guy Debelle:

Probabilistic statements dominate a lot of talk in financial markets, Debelle said, but be careful with those that masquerade as certainties.

“Beware the lure of incredible certitude,” the RBA official said, quoting a line from American economist Charles Manski.

“Try to avoid presenting point predictions and estimates without conveying any sense of the uncertainty around them. This is hard because, as Manski notes, ‘the public, impatient for solutions to its pressing concerns, rewards those who offer simple analyses leading to unequivocal policy recommendations’.”

Does the RBA make forecasts? Yes. Is it the only one allowed? Do the rest of us just stick our heads in the sand?

Forecasting is obviously tricky. But attacking it when prices go against your preferred outcome is pretty stupid. You have to engage with the underlying fundamentals and extrapolate as best as possible on that basis. Change when they change. For Aussie house prices that includes assessing all of the current variables in pricing:

- macroprudentials two and three;

- Hayne impacts;

- out-of-cycle mortgage rate hikes;

- oversupply and strong immigration but possible cuts;

- election and negative gearing reform;

- withdrawing Chinese investors.

Let’s assess each.

MP2 is the interest-only shock. On this front there has been good progress as banks chew through reset ahead of schedule:

The total is now down from a peak of $583bn in March 2017 to $461bn five quarters later. Given banks have issued $95bn in new interest-only loans in that time we’ve seen as much as $200bn reset in outstanding interest-only loans already. The total refinancing task out to 2021 is roughly $450bn so the banks have gotten materially ahead of the curve. Nonetheless, the shock will will roll on at a diminished pace so it remains a price negative.

MP3 is APRA’s new high-leverage restrictions which are still developing as bank data reporting improves. These are, if anything, going to get tighter once the data is in. I can’t see APRA backing off what is an obviously ponzi segment of the market in today’s post-Hayne environment so that’s more tightening to come.

The Hayne Royal Commission fallout, which we might parse as management paralysis and uncertainty, will run until the mid-2019. The final report is out in February but then we’ll have the federal election to content with. Labor will be harder on the banks than the Coalition. How the corrupt RBA and Treasury’s efforts to restore criminal banking will play out is unknowable. There is also the implications of massive class actions if Hayne findings are criminal enough. It’s probably fair to say that there is at least another year of uncertainty yet for bank managers.

The recent spate of bank reports shows that there is no let up in the need for more out-of-cycle rate hikes as BBSW spreads remain wide:

Just today NAB is hiking again and more will come next year as pressure on NIMs persists.

The oversupply issue is also intact:

And, if anything, is getting worse as unsold inventory piles up:

New builds will begin to fall away soon which will help. But that will present a new problem in falling building activity and jobs.

As for immigration, who knows what is coming? The Coalition is bonkers if it doesn’t cut it back. I think Labor will also be forced to eventually but that will take years of falling wages first. So, for now, it is a support but is a risk.

The coming election will stall economic activity and is going to converge with a consumer under increasing pressure as house prices keep falling. So by May next year I expect to see domestic demand falling precipitously and unemployment rising. Obviously this will make house price falls worse:

Then there is the now certain negative gearing reforms which most observers agree are worth -10% to prices (some of which might be underway in advance).

Chinese investors are gone and will keep fleeing as Cold War 2.0 forces China to curtail capital outflows:

They are not coming back. This is particularly a problem for massively inflated prestige values.

So, what could stop the falls given this array of shocks?

Will yield do it? Hardly. For historically low yields to be remotely tempting amid falling prices they will need to double in Sydney and Melbourne and given sluggish rental growth that means prices halving first! The truth is, the investor-concentration in Australian property long ago turned it into a capital gains-led market. Such markets are either rising or falling. They do not stand still.

Will pent-up demand do it? Not without a trigger.

Will immigration do it? I don’t think so. As the economy slows and jobs dry up more people will live together and the oversupply linger despite demand growth.

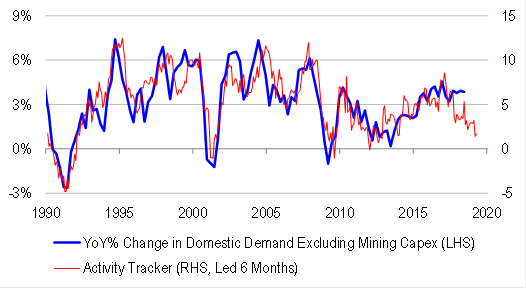

Will economic strength do it? Nope. The Botox Boom has peaked and is falling away as fiscal spending plateaus plus private investment slows and the consumer buckles. Here’s the Credit Suisse leading activity tracker which speaks for itself:

That leaves us with stimulus. Fiscally, we could see some renewed FHB grant but, remarkably, there are already generous incentives in the market so any impact would be muted. There will be election tax cuts but not enough and not until next financial year. Monetarily, the RBA could step in with two rate cuts. But the banks will keep half and then the central bank’s cupboard will be bare. I reckon this is coming mid-2019 as the economy stalls and will work to stabilise prices for a little while.

But even this won’t last long given the age of the business cycle. What will the property market do when the next external shock arrives, there is no big Chinese stimulus, commodities crash, immigration halves, the stock market halves, unemployment launches and the RBA has no rate cuts left? This will also come the usual pro-cyclical shocks of bank credit tightening.

Or you can refer to the distant wisdom of a Canadian moose.