Amid all the scaremongering from our Property Council Prime Minister, Scott Morrison, along with property industry vested interests, Bill Shorten is standing firm on Labor’s negative gearing and capital gains tax (CGT) policy, vowing to make homes more affordable. From The AFR:

Bill Shorten says Labor will forge ahead with curbing negative gearing and capital gains tax exemptions if it wins the election because housing is still unaffordable for most…

“A lot of first-home buyers can’t enter the market. Come with us to any auction on a Saturday. Plenty of people …are still priced out of the market,” he said.

“If you don’t think housing affordability is a problem, talk to a young couple or talk to people who rent.”

The reality is that if policy makers actually want affordable housing, this means that dwelling values must fall relative to income. This necessarily means falling prices.

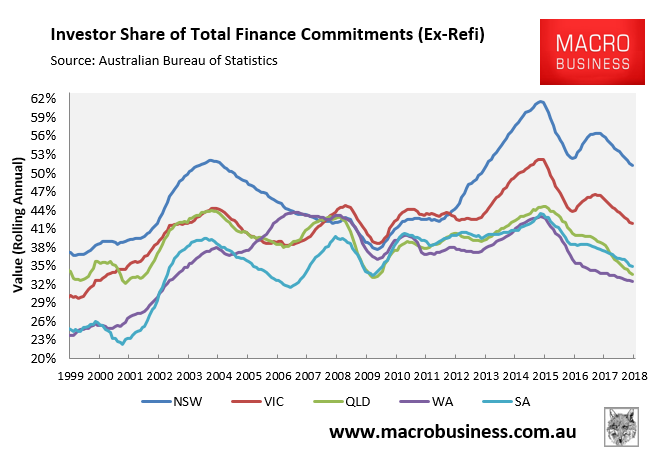

We need (and may see) investor shares of mortgage finance to halve for a healthy real demand driven market. Negative gearing reform should go ahead to achieve it.

The biggest risk to Labor’s policy is not the Coalition’s or the property lobby’s scaremongering, which is expected, but rather that which might come from the RBA and Treasury, as they have shown with the banking royal commission:

The Reserve Bank of Australia and Treasury have privately cautioned the Morrison government that any regulatory response to the financial services Royal Commission must be careful to avoid putting the brakes on lending to home buyers and business.

These institutions are no longer managing the economy, but rather managing the bubble. Hence, expect them to throw Labor’s sensible negative gearing and CGT policy to the wolves in a bid to keep the bubble alive.