DXY was solid again Friday night. EUR fell and CNY firmed:

EUR positioning is stable meaning there is a lot of room for it to fall as ECB hawkishness is forced backwards:

Advertisement

AUD was mostly up against DMs:

And EMs:

The market went even shorter AUD last week. This is the main reason why I am not bearish AUD short term. It looks way oversold:

Advertisement

Gold firmed:

Oil is off to the races:

Advertisement

Base metals were firm:

Big miners OK:

EM stocks flamed out:

Advertisement

EM junk stalled:

Treasuries were bought:

But not as much as bunds:

Advertisement

Italy is a problem again:

Stocks were stable:

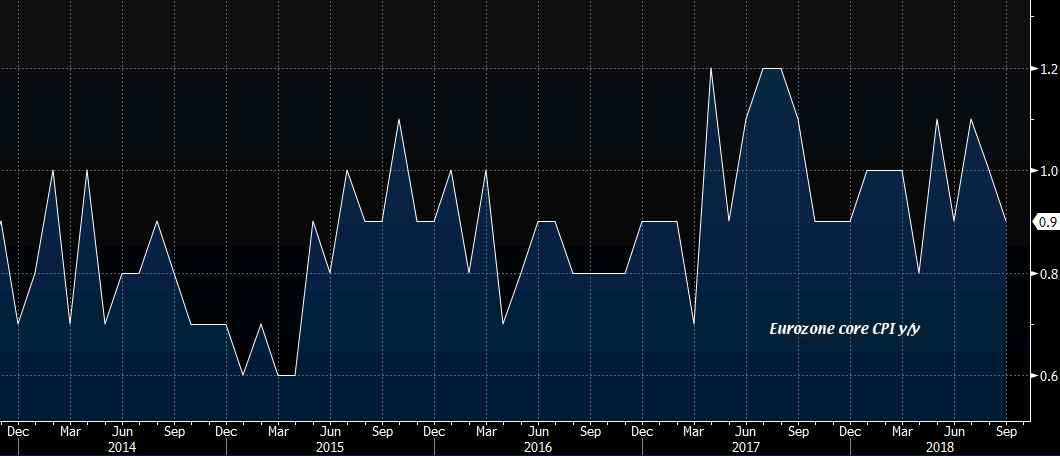

The big news on the night was weak European inflation with core at 0.9%:

Advertisement

The ECB has got Buckley’s chance of hiking. Adding EUR woes was Italy’s proposed budget deficit of 2.4% which blew up European rules. The clash is set for October 15 when Brussels will reject it.

A weak EUR automatically means a strong DXY which ought to weigh on EMs and commodities for the remainder of the year.

Advertisement

Macquarie’s excellent Viktor Shvets is still worried:

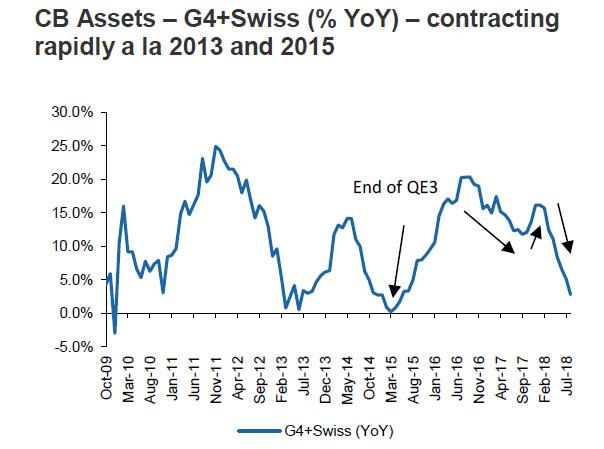

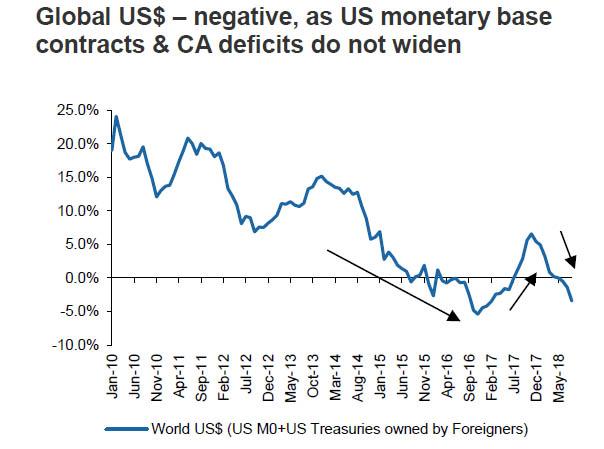

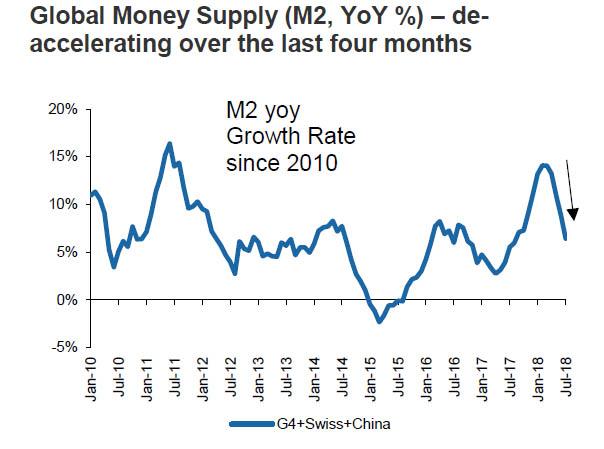

All measures of liquidity continue to tighten…

All of our measures of liquidity have continued to weaken over the last two months. This applies to public sector liquidity, which has now declined to ~3% (vs 16%+ growth in ‘16 and ‘17)…

… US$ liquidity is negative (vs growth of ~5%- 6% in ‘17) and money supply (down to 4-5% vs double-digit growth in late ‘17).

G5+China M2 has fallen over the last four months by over US$2 trillion. At the same time, CBs are gradually pushing up the cost of capital.

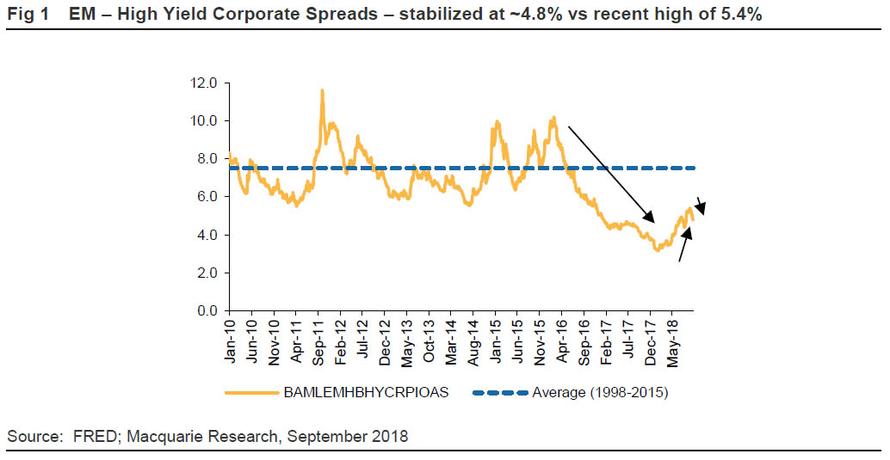

While investors have already witnessed several tremors (VIX volatility in Feb’18, massive explosion of basis points and TED and US Libor in Mar-Apr’18, DXY acceleration and attack on the most vulnerable of EMs in Jul-Sep’18), the degree of dislocation has thus far been contained. For example, EM FX volatility rates have recently again eased and the same applies to EM high-yield corporate debt…

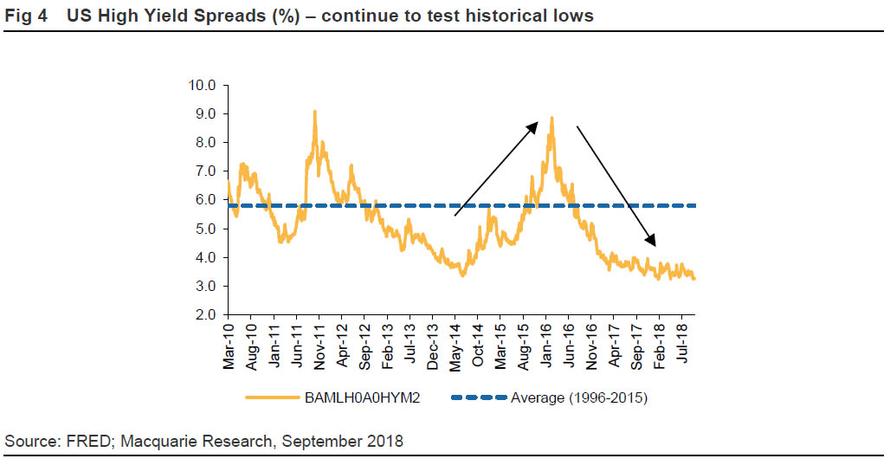

… while both OIS Libor and TED spreads remain relatively placid, and the US high-yield market continues to enjoy some of the lowest ever spreads (~3.2%). It applies even for CCC & below debt (~6.6%).

… but complacency keeps returning as inflation remains subdued.

Although one could highlight some specific measures (e.g. IMF rescue of Argentina or tightening in Turkey), we believe that returns to complacency are primarily due to a deeply held view that CBs would never allow any meaningful break-out of volatilities, and would step-in with either liquidity supports and/or end of tightening while as long as the US domestic economy is strong, the risk appetite is expected to prevail. If we dig deeper, investors seem to agree with us that overleveraging, lack of clearance of past excesses & disruption are generating such strong headwinds, that break-out of excessive wage inflation is unlikely, even as markets tighten. This in turn, limits the degree of damage to margins or rise in the cost of capital, except for the most marginal of cases.

We worry about the next six months; but 2019-20 might not be bad

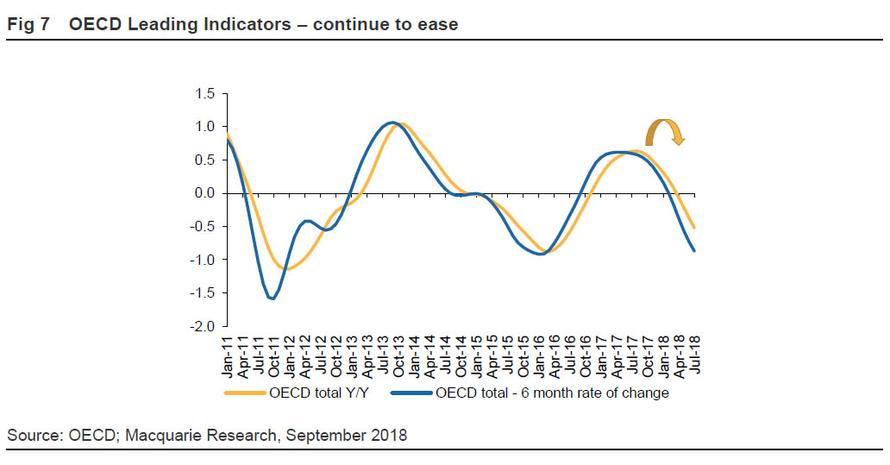

Our concern remains one of accumulation of policy failures, as CBs and investors understate the degree of linkages between asset classes. For example as 30Y mortgages touch 4.7%, there are already signs of tightening. Similarly rising short-term rates are bound to impact car loans & credit cards, while more vulnerable EMs could infect stronger EMs, causing a more robust contraction at the time when OECD leading indicators are already easing.

The role of the Fed and China is particularly important. It seems that the Fed is only focusing on domestic strength, while ignoring global tightening. As long as it continues to view the world through one-dimensional lenses, the non-US world runs a risk of significant contraction, which in turn would return to haunt US. Similarly, while recent actions have stabilized China’s credit impulse, it does not yet represent a substantive policy shift. While most investors worry about ’19-20, we remain far more concerned what would happen over the next six months. Either the Fed stops and China stimulates, or accidents happen. EMs still look very vulnerable; but ‘19-20 might not be bad years, as either normality returns or Fed pulls back. Systemic failure is not an option.

A good summation. But Chinese stimulus is already flowing. And there is one outcome that Shvets does not canvas, further US fiscal stimulus, specifically Trump’s infrastructure plan which would support both growth and further Fed tightening:

Advertisement

The context is febrile with the US mid-terms only six weeks away. But beyond that we still think Trump will look to further growth measures to remedy the fiscal cliff. That would mean 2019 develops as a counter-intuitively good year, with both trade war parties stimulating.

Then 2020 shapes as a bust as the Fed is forced to hike beyond current expectations…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.