Global stocks roar, Australian dollar whimpers

DXY is breaking out. EUR is weak and CNY the meat in the sandwich:

The rising DXY sat on any AUD rebound but it rose against other DMs:

Was mixed against EMs:

Gold flamed out:

Oil firmed:

Base metals sagged:

Big miners snapped back:

As did EM stocks:

And junk:

Treasuries were sold a little:

Bunds too:

Italy soothed:

And global stocks roared back on good earnings:

Westpac has the wrap:

Market Wrap

Global market sentiment: US equities bounced back overnight, the S&P500 up 2.0% currently. The US dollar and bond yields are also higher.

Interest rates: The US 10yr treasury yield rose from 3.10% to 3.14%, the 2yr yield from 2.83% to 2.86%. Fed fund futures yields continued to price the chance of another rate hike in December at 75%.

FX: The US dollar index is up 0.3% on the day, and is at a two-month high. EUR initially rose to 1.1432 following the ECB statement but fell to 1.1360 following the press conference and US data. USD/JPY rose from 112.00 to 112.65. AUD performed well, rising from 0.7060 to 0.7100, perhaps helped by the improved equities sentiment. NZD ranged between 0.6510 and 0.6544. AUD/NZD ground higher from 1.0840 to 1.0865.

Economic Wrap

US durable goods orders rose a stronger than expected 0.8% in September, following an upwardly revised 4.6% gain in the previous month. The detail was not as upbeat though; excluding volatile aircraft and defence items orders fell 0.1% while shipments, a close proxy for business investment were unchanged in the month versus expectations for a 0.4% gain. The US merchandise trade deficit continues to deteriorate, hitting a record $76bn in September. The lukewarm detail in the durable goods report and the wider trade deficit prompted some last minute trimming of Q3 GDP growth forecasts, due Friday; the closely watched Atlanta Fed Nowcast was cut to 3.6% from 3.8%. Pending home sales rose 0.5% in September, their first gain in three months, defying the trend in other housing data lately that show the industry losing momentum.

Fed VC Clarida said further gradual tightening will be appropriate, and could move beyond neutral if the economy and employment continued to improve in 2019.

ECB policy was unchanged as expected. The deposit rate will remain at -0.40% at “least through the summer of 2019”, asset purchases of EUR15bn per month will cease at the end of Dec. 2018, and reinvestment will continue for as long as necessary. Draghi expertly maintained the positive, “broadly balanced” tone from September whilst acknowledging greater uncertainties in the global economy and recently soft incoming Eurozone economic data. Whilst focusing on the positive developments in employment and wage growth, Draghi also stated that the December update of ECB staff projections would be important. Their forward guidance would persist as would the re-investing of their APP with all aspects of their policy being data dependent.

Germany’s October IFO business survey missed expectations (headline 102.8, exp. 103.2, prior 103.8). The pullback from September had little impact on markets since it was reflecting the recent softness in both ZEW and PMI surveys.

Event Risk

Australia: The 2017/18 National Accounts are released. They will provide additional information and may contain revisions to GDP growth.

Euro Area: ECB President Draghi speaks at a National Bank of Belgium event.

US: Q3 GDP is expected to rise by a 3.3% annualised pace. Westpac is forecasting 3.4% as the consumer trend continues to be robust while investment is boosted by new structures. Fedspeak involves Mester at a Money Marketeers event in NY.

The key to the rising USD overnight was that Draghi also said:

Regarding non-standard monetary policy measures, we will continue to make net purchases under the asset purchase programme (APP) at the new monthly pace of 15 billion euros until the end of December 2018. We anticipate that, subject to incoming data confirming our medium-term inflation outlook, we will then end net purchases. We intend to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of our net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Incoming information, while somewhat weaker than expected, remains overall consistent with an ongoing broad-based expansion of the euro area economy and gradually rising inflation pressures. The underlying strength of the economy continues to support our confidence that the sustained convergence of inflation to our aim will proceed and will be maintained even after a gradual winding-down of our net asset purchases. At the same time, uncertainties relating to protectionism, vulnerabilities in emerging markets and financial market volatility remain prominent. Significant monetary policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term. This support will continue to be provided by the net asset purchases until the end of the year, by the sizeable stock of acquired assets and the associated reinvestments, and by our enhanced forward guidance on the key ECB interest rates. In any event, the Governing Council stands ready to adjust all of its instruments as appropriate to ensure that inflation continues to move towards the Governing Council’s inflation aim in a sustained manner.

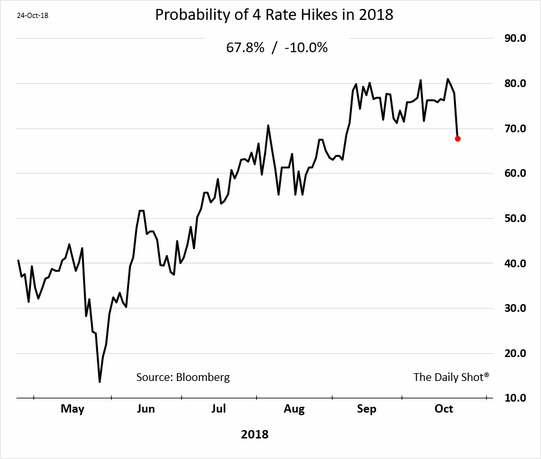

Hardly bullhawk scary stuff. The rising USD is some calm for markets given it will aid the Fed. The stock rout has already bashed tightening expectations lower:

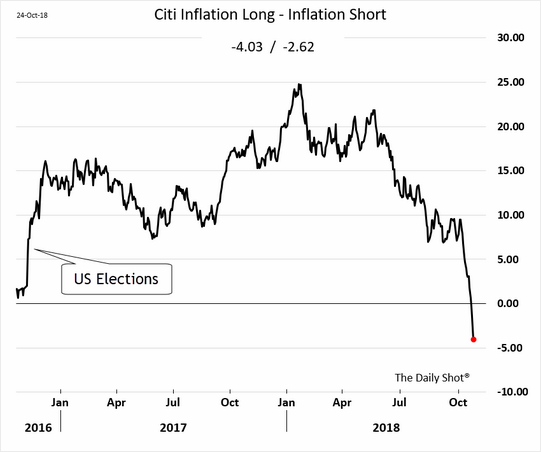

Stocks are pricing for a return of lowflation:

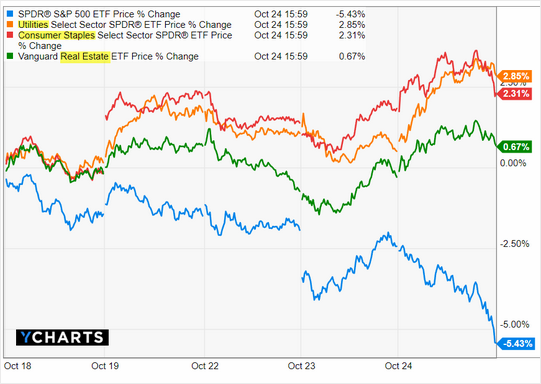

With staples and defensives outperforming:

Fundamentals and earnings are still decent. I am not of the view that US inflation will rocket despite good wages growth. We know it’s late cycle but still don’t know how late so the portfolio is positioned for both growth (via tech) and slowing (via staples) in a barbell structure. We’re holding high cash balances and the AUD hedge is still working, as is the local bond holding which is going to get a further boost as housing comes apart.

Addendum

Amazon and Alphabet hit the market after hours and, although quite reasonable, missed a few metrics so futures are down again and volatility continues!