Australia

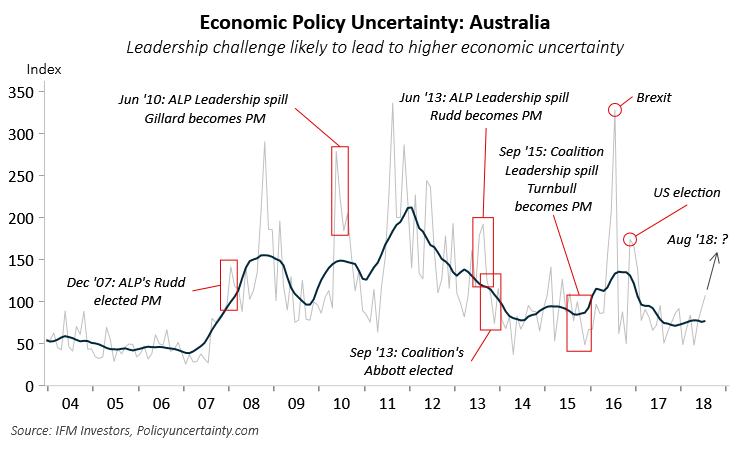

Australia – Economic Policy Uncertainty

Sydney & Melbourne – Auction Clearances

![]()

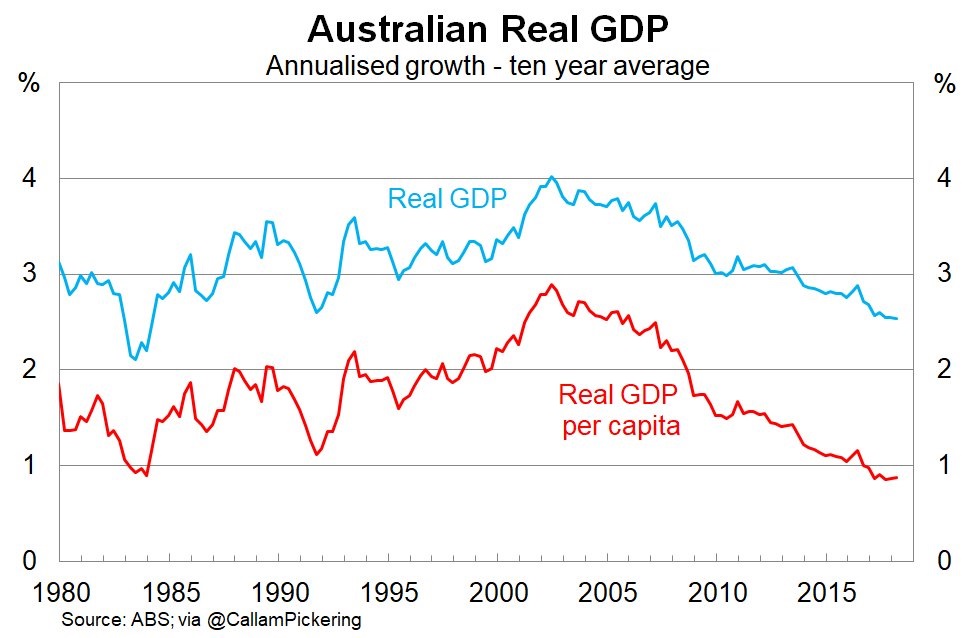

Australian GDP

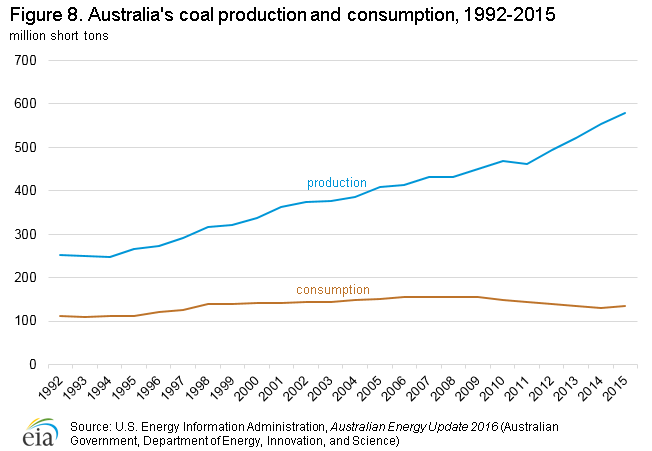

Coal Production & Consumption

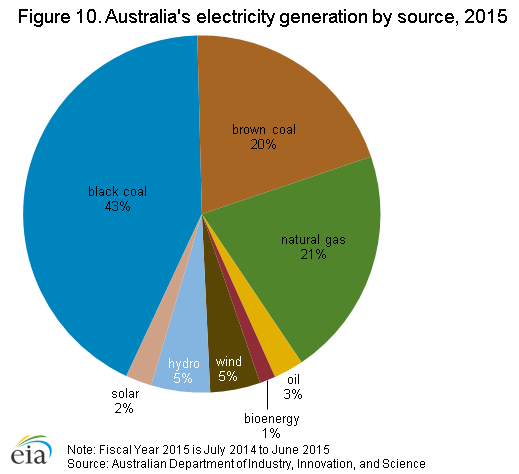

Electricity Generation

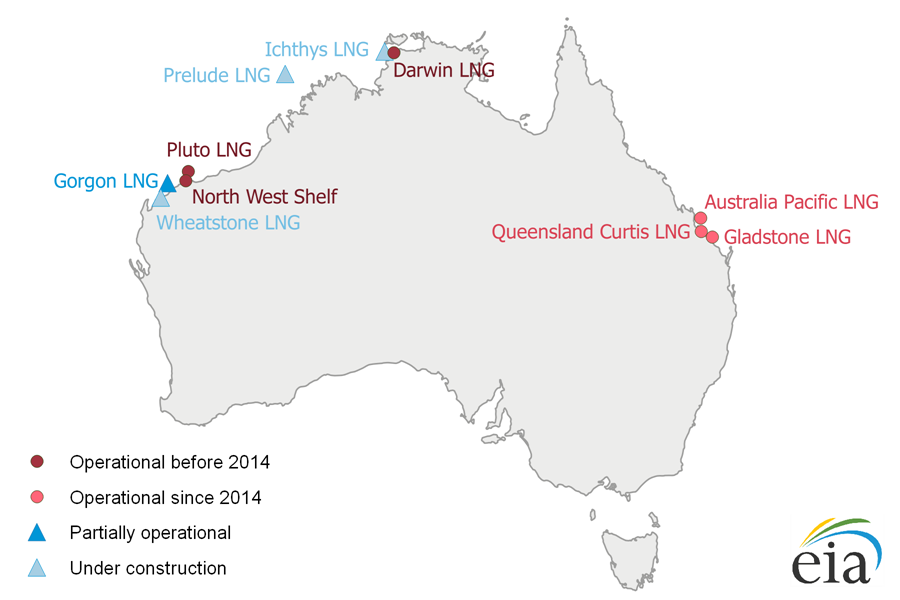

Major LNG Plants

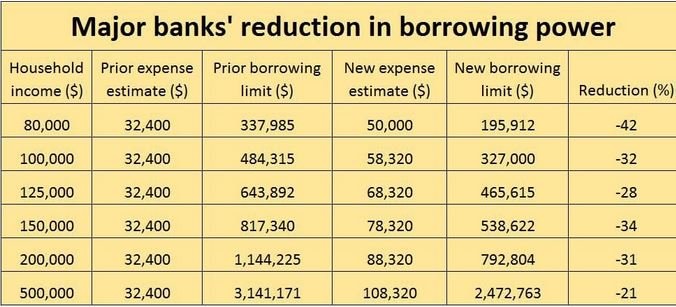

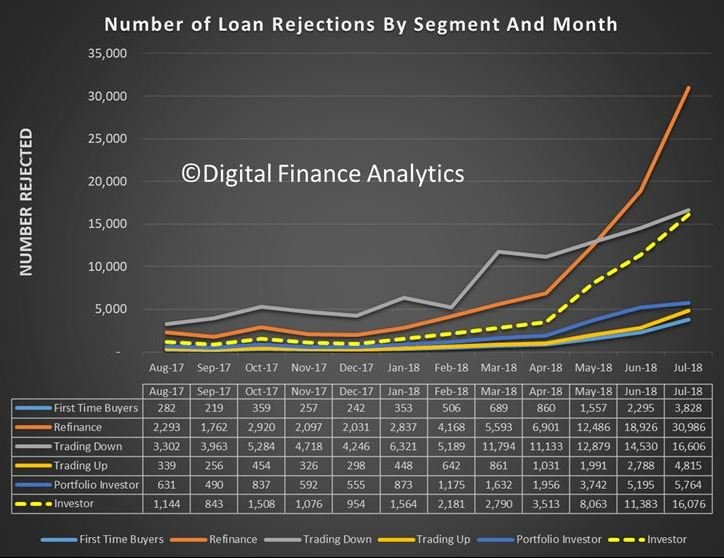

Implications of Tightening Lending Standards

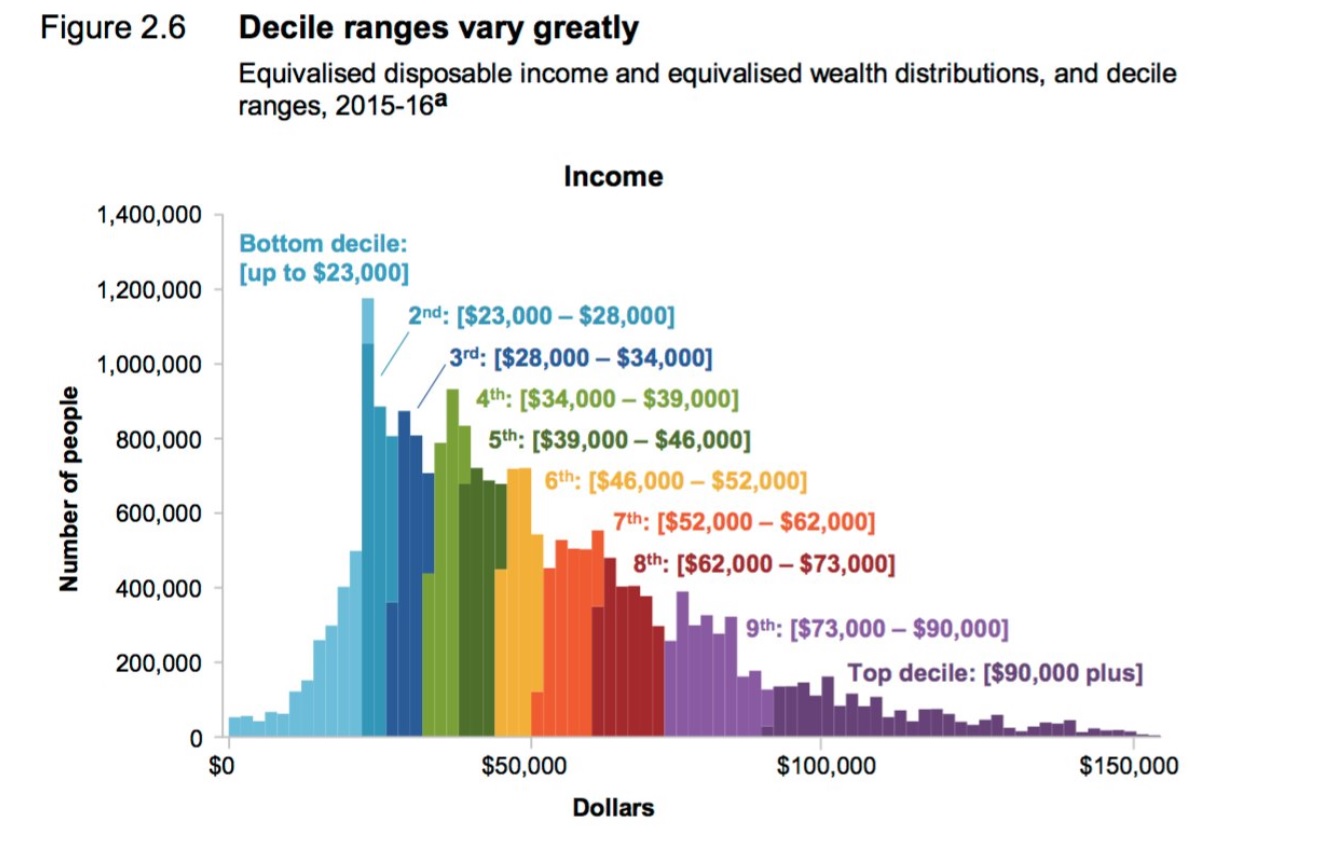

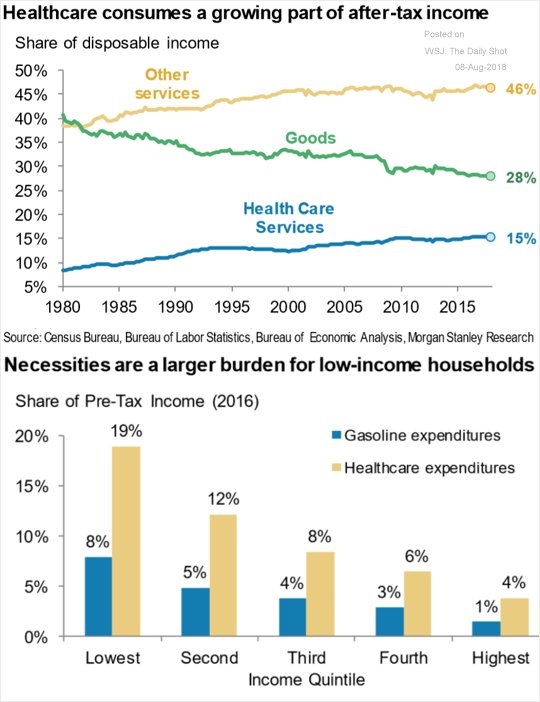

Disposable Income by Decile

Loan Rejections

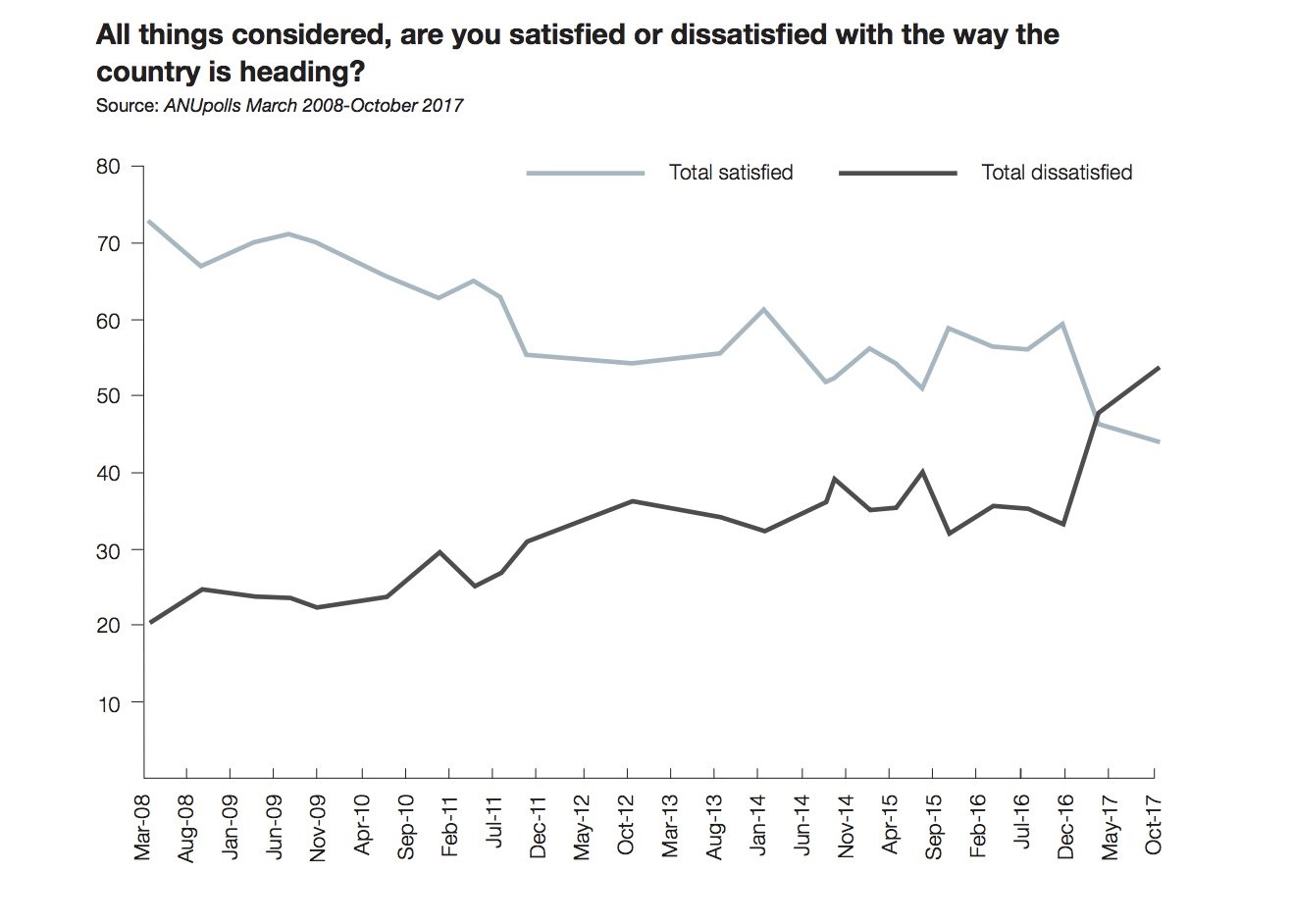

Public Satisfaction with the National Direction

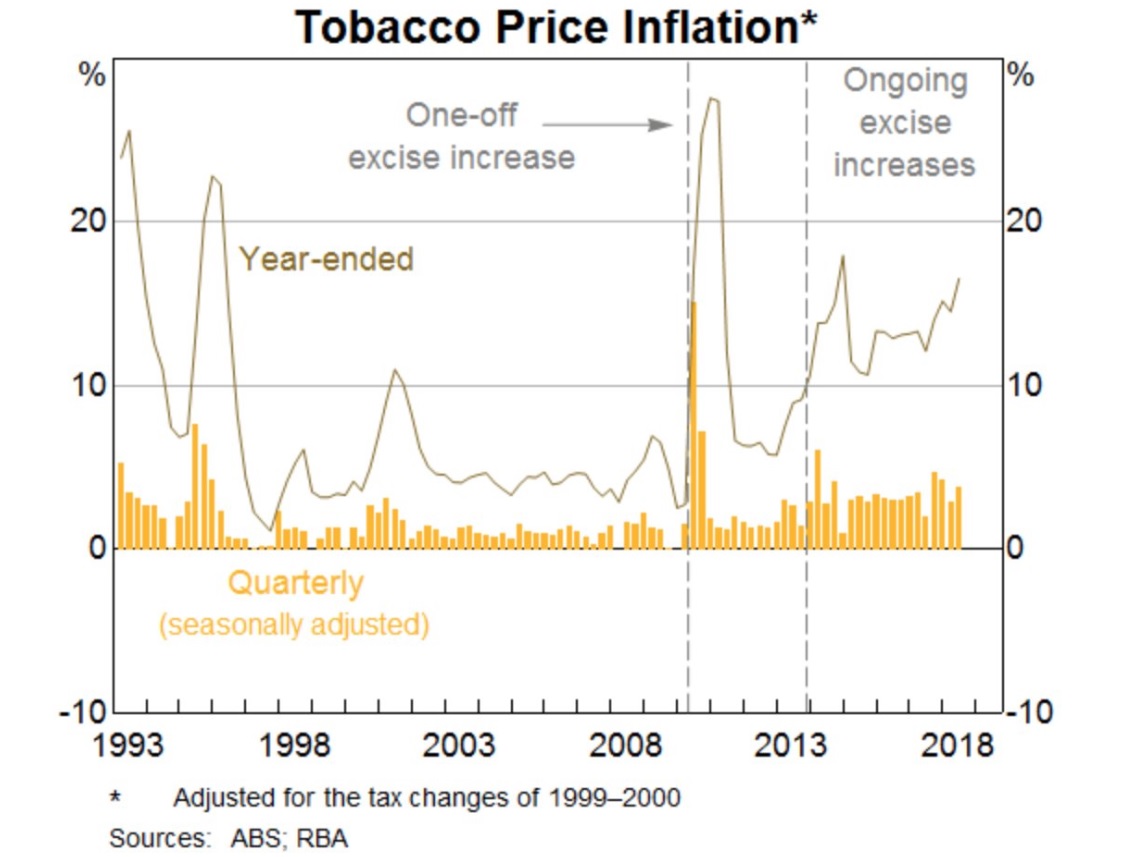

Tobacco Price Inflation

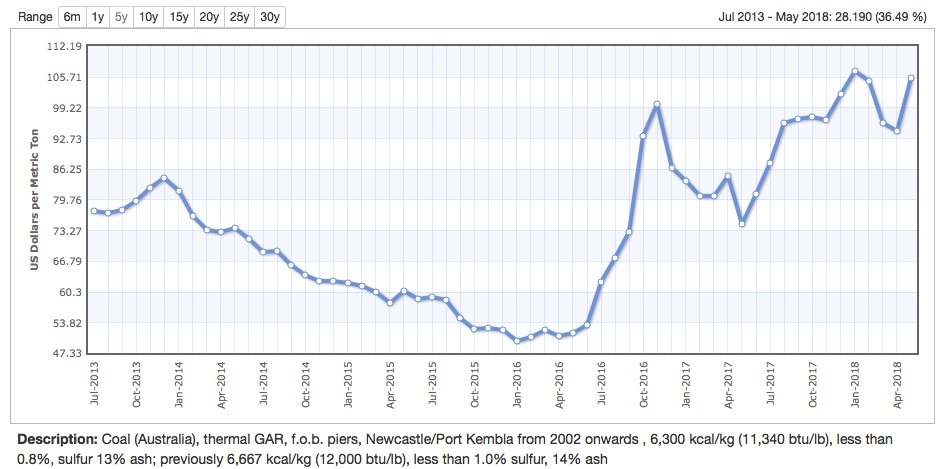

Australian Thermal Coal Price

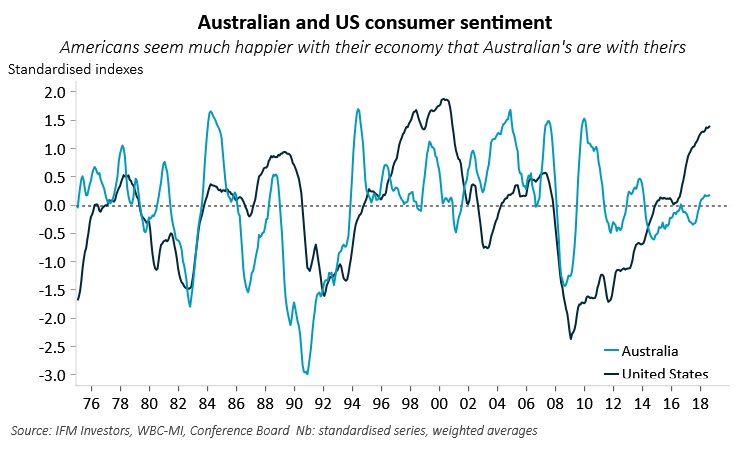

Australian & United States Consumer sentiment

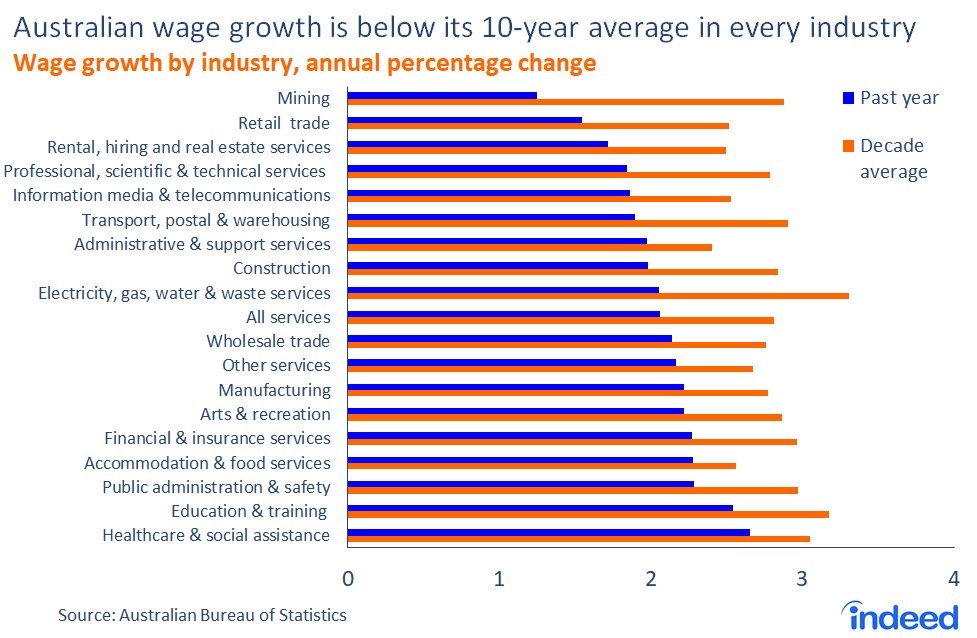

Australian Wage Growth by Industry

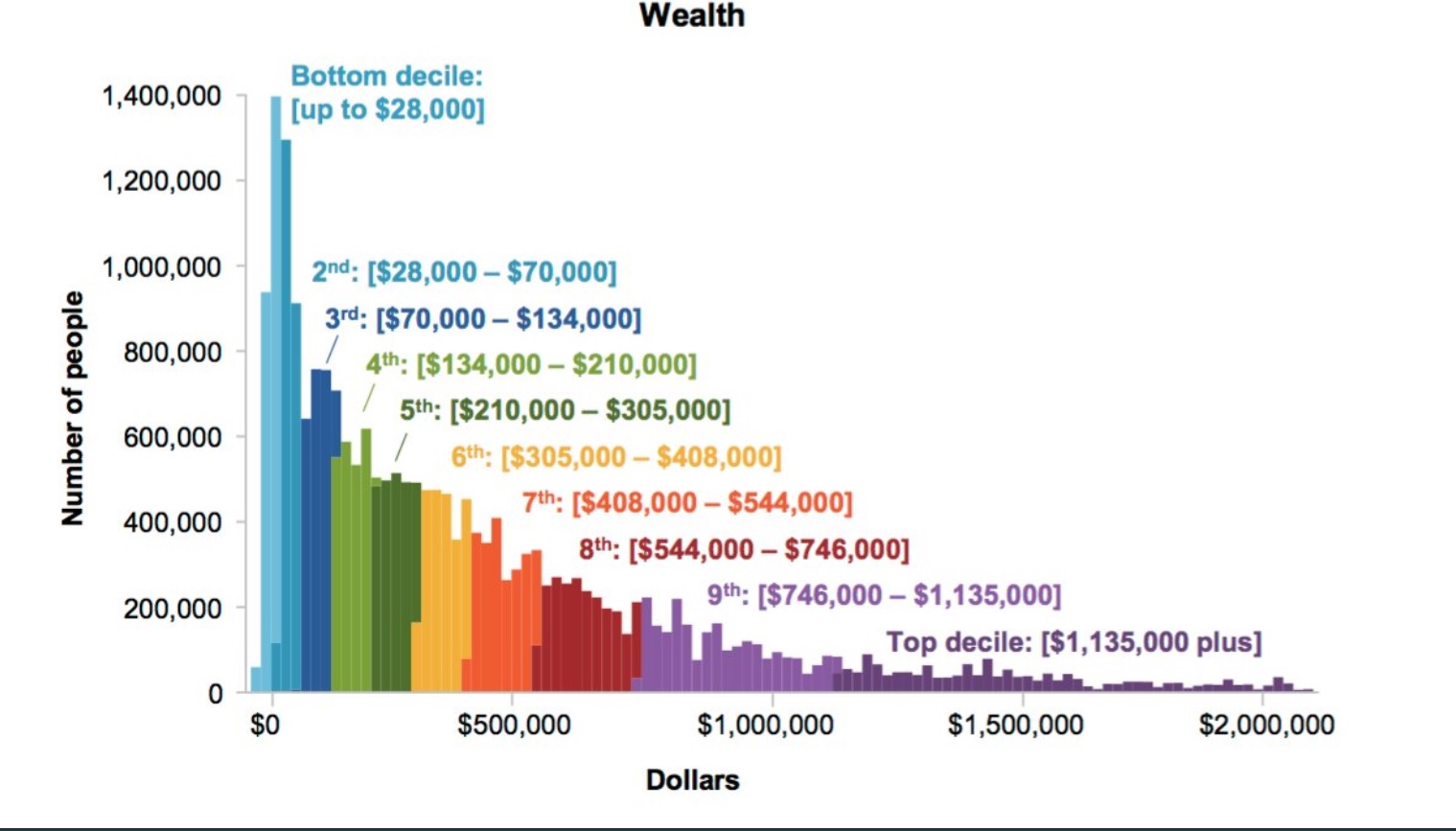

Net Wealth by Decile

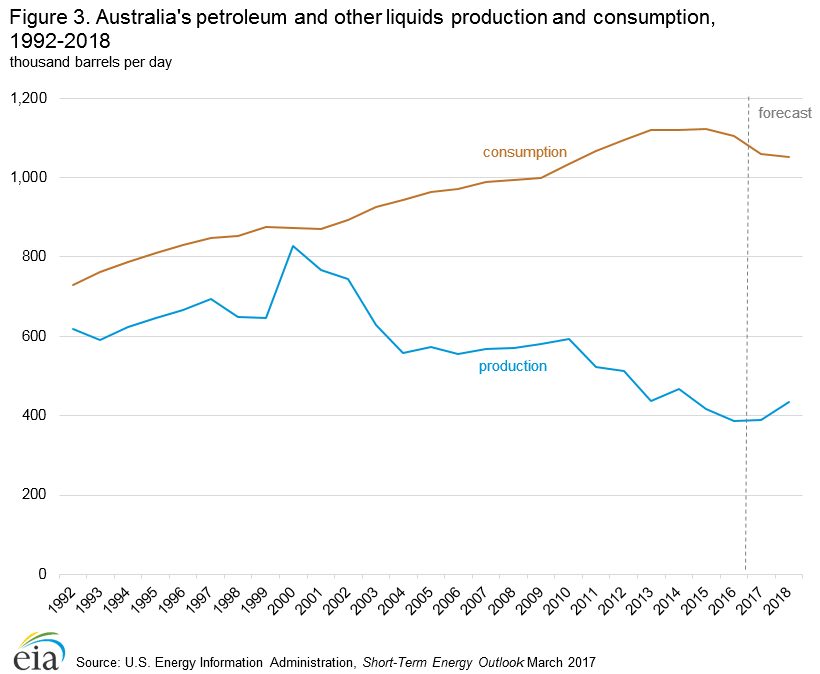

Petroleum Production & Consumption

United States & Americas

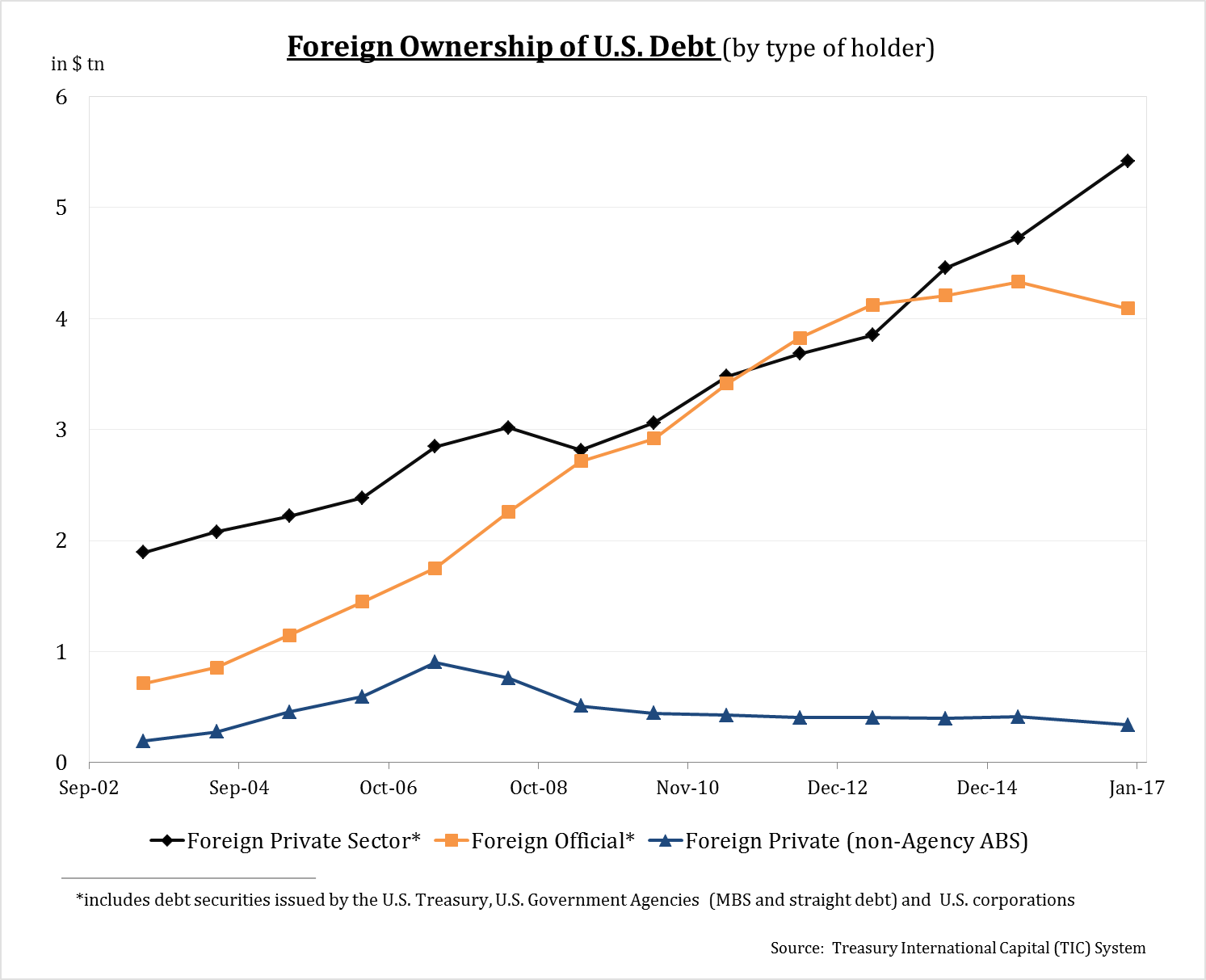

Foreign Ownership of US Debt

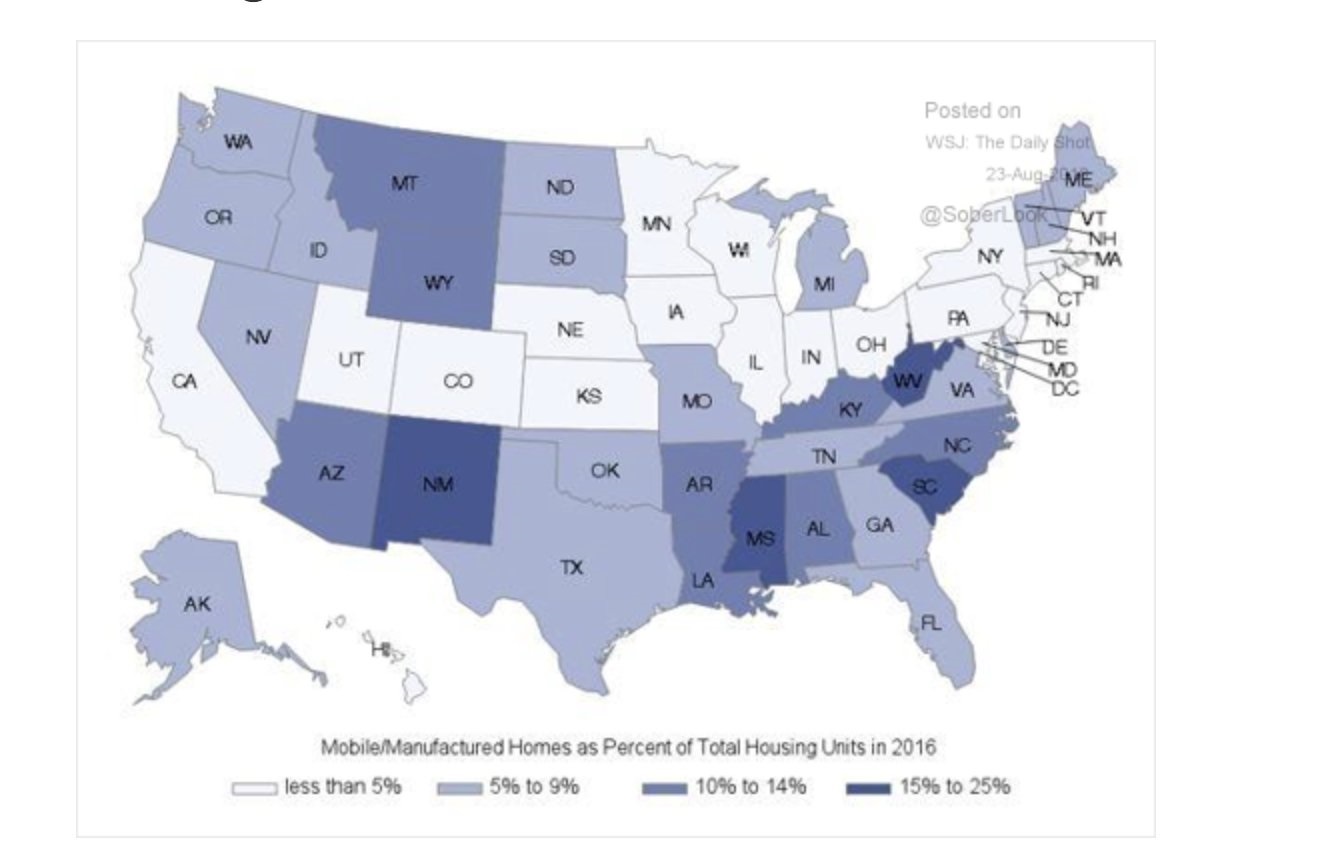

Mobile/Manufactured Homes as Percent of Total Housing

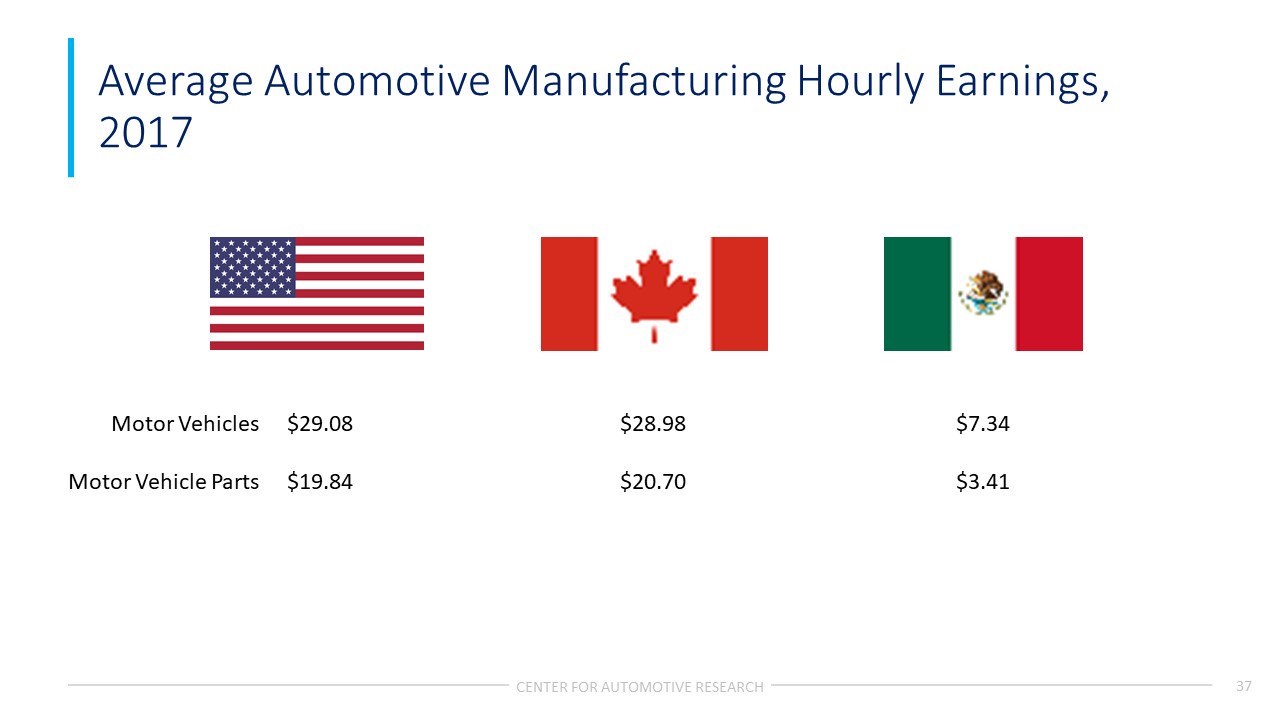

Automotive Manufacturing Hourly Earnings – North America

Highest Paying Jobs in the US

American Beers and the 5 Ultimate Producers

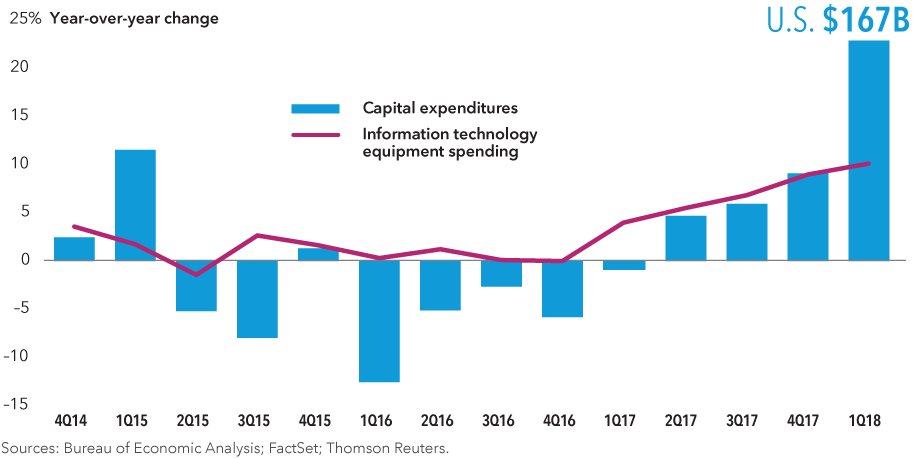

US Capex

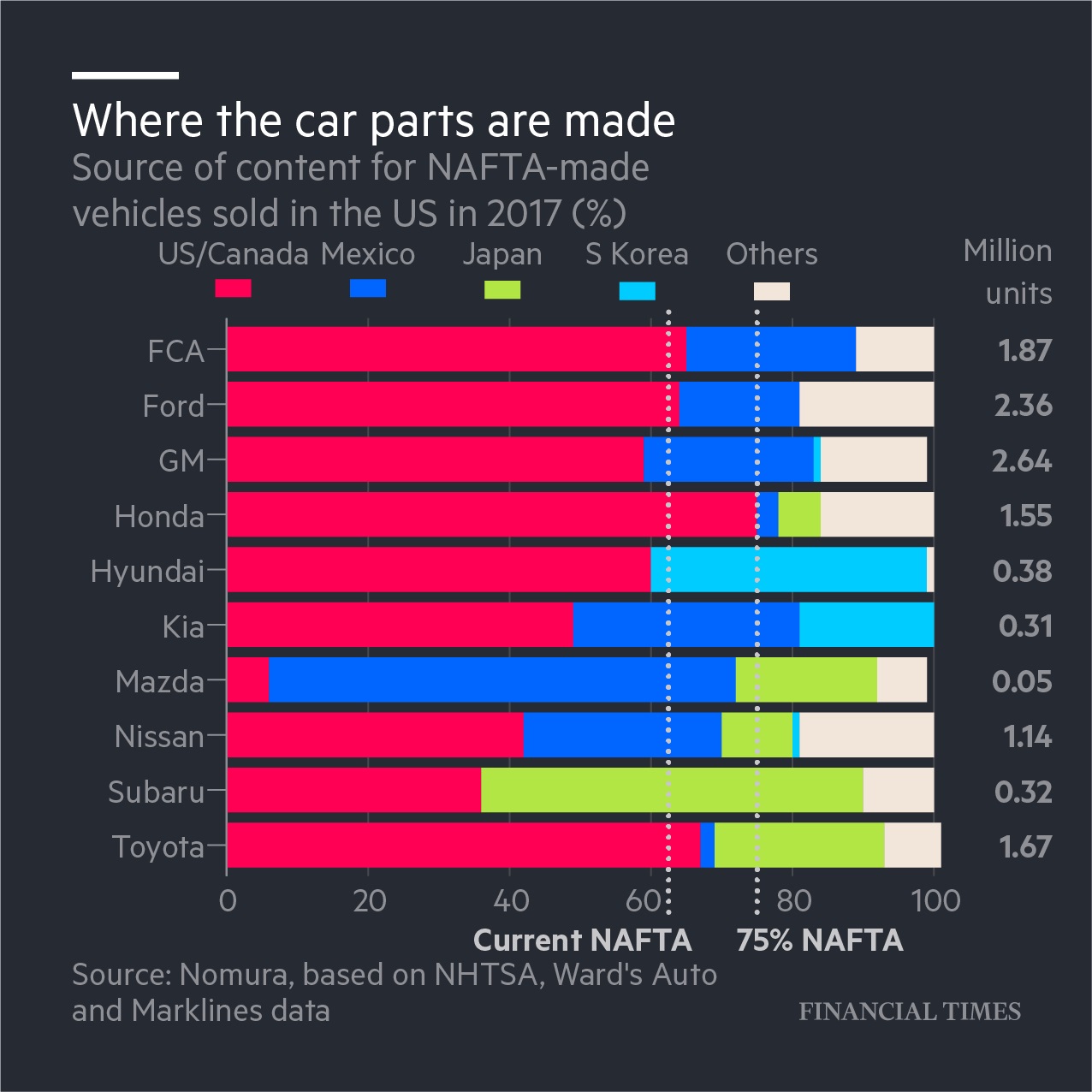

US Cars – where they are made

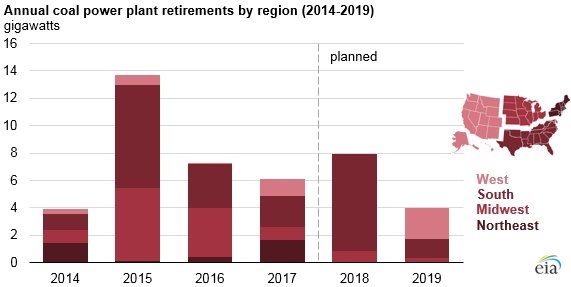

United States – Coal Power Plant Retirements

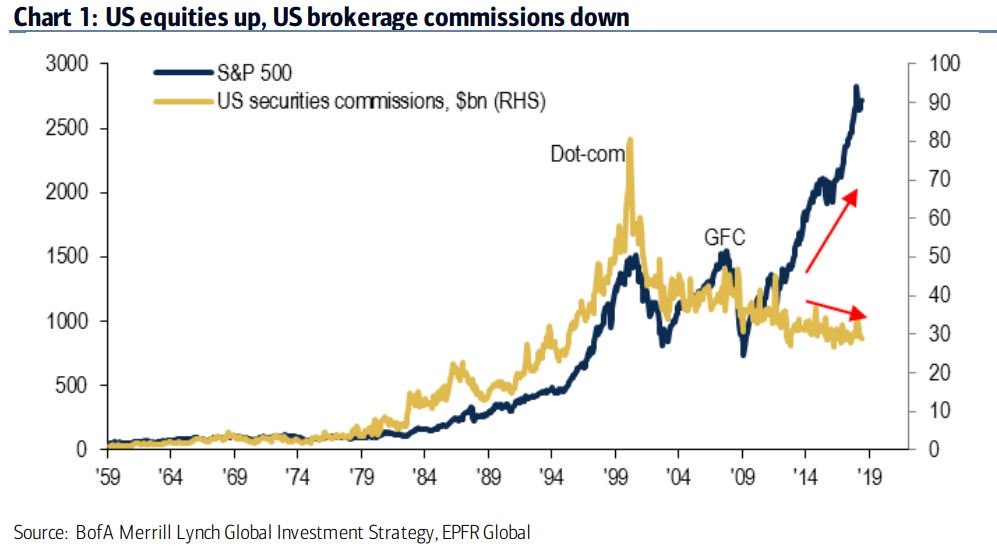

US Brokerage Commissions

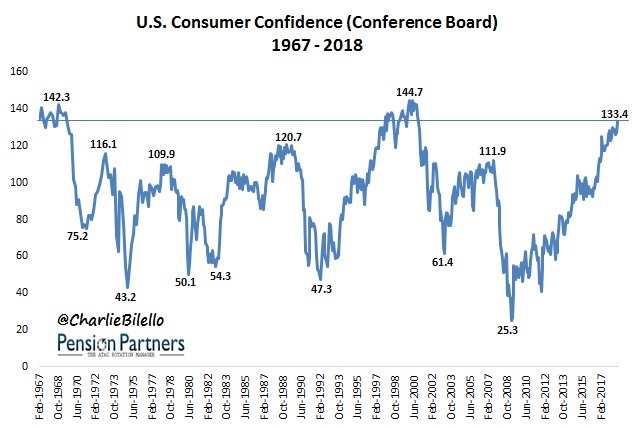

US Consumer Confidence

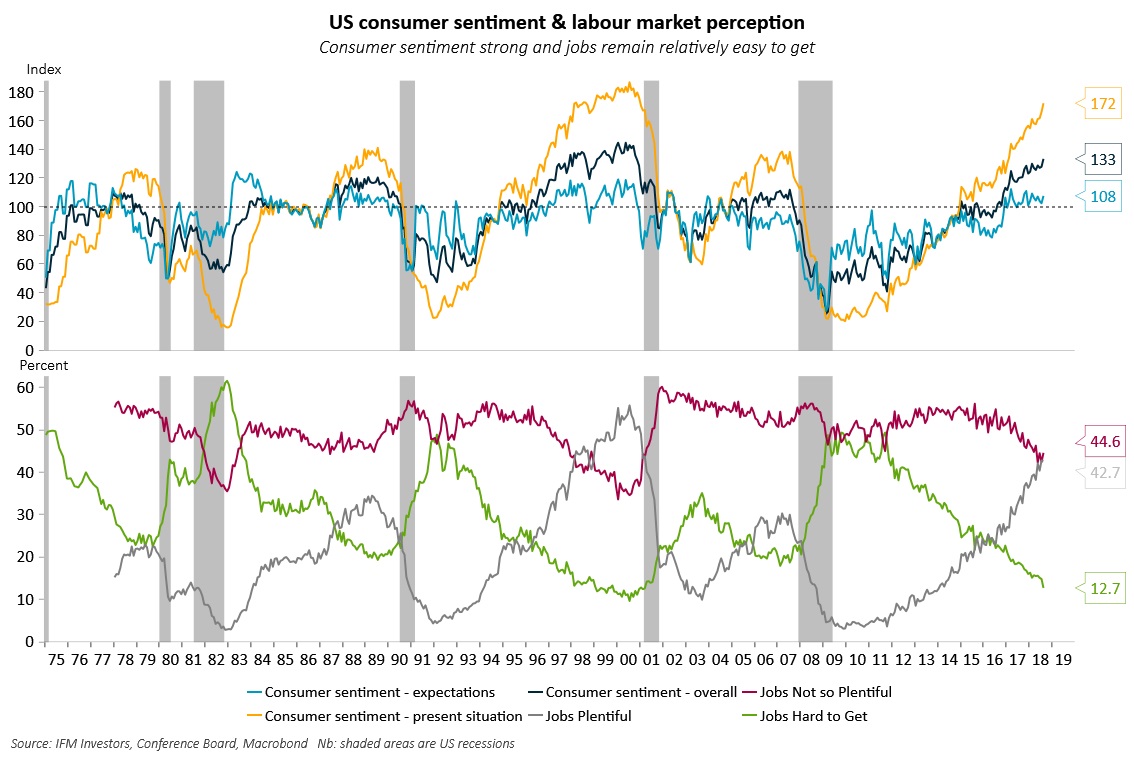

US Consumer Confidence & Labour Market Perception

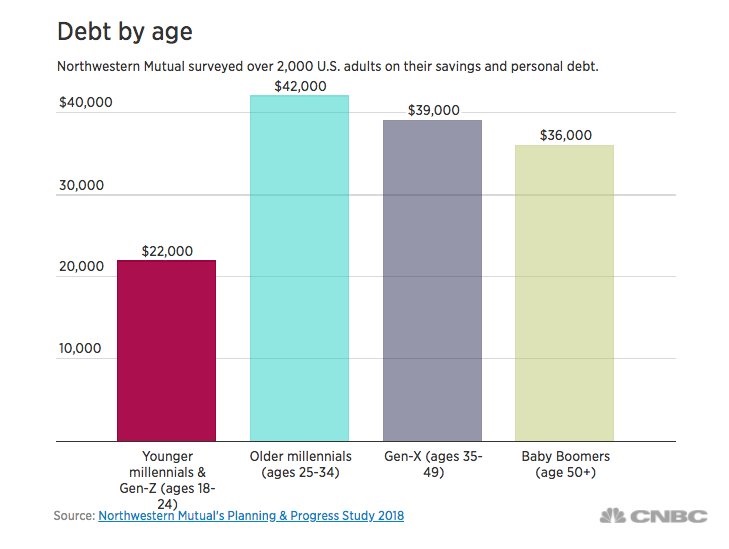

US Debt by Age Group

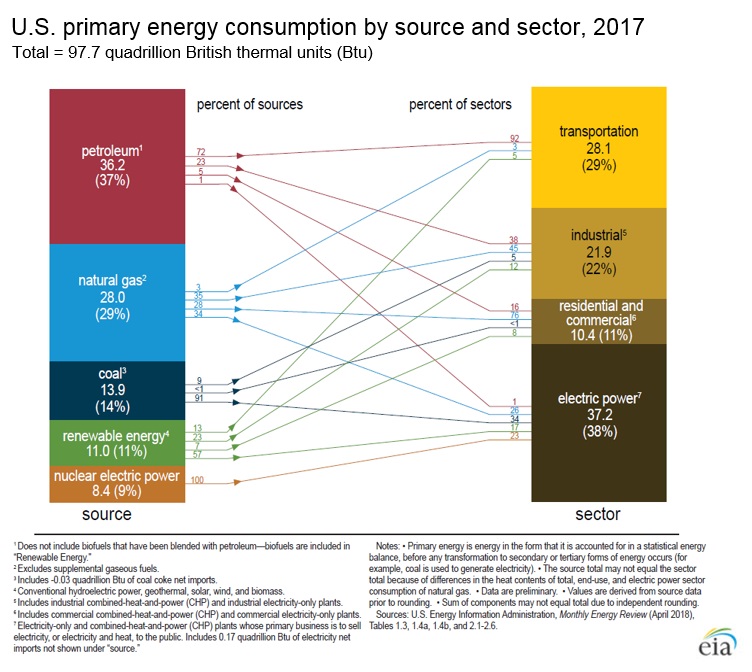

US Primary Energy Source & Consumption

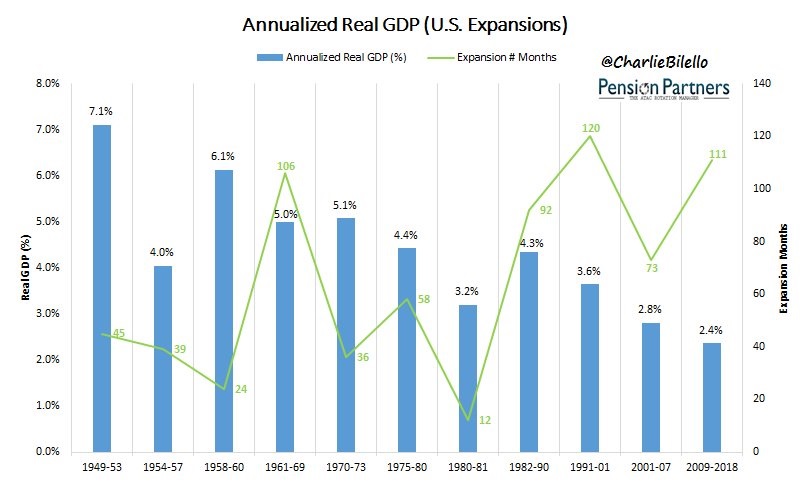

US Annualised Real GDP

Consumption of Post Tax Income

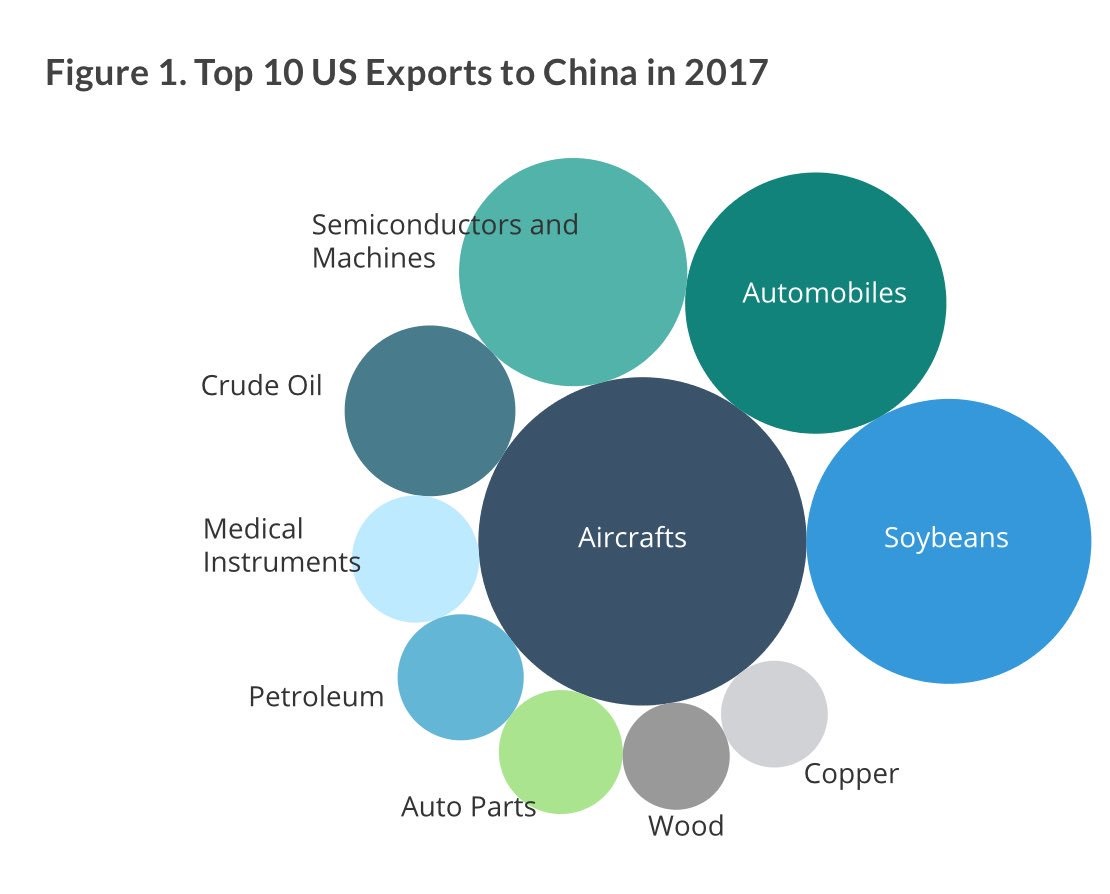

Major US Exports to China

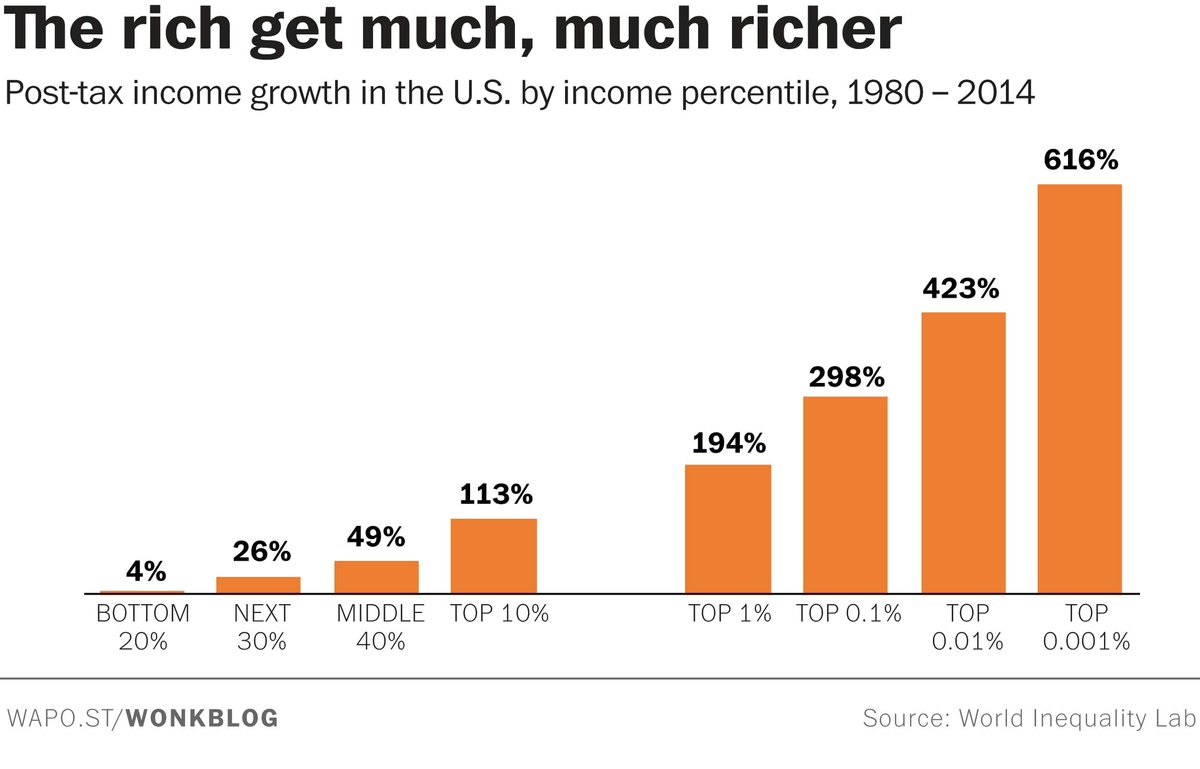

Post Tax Income growth

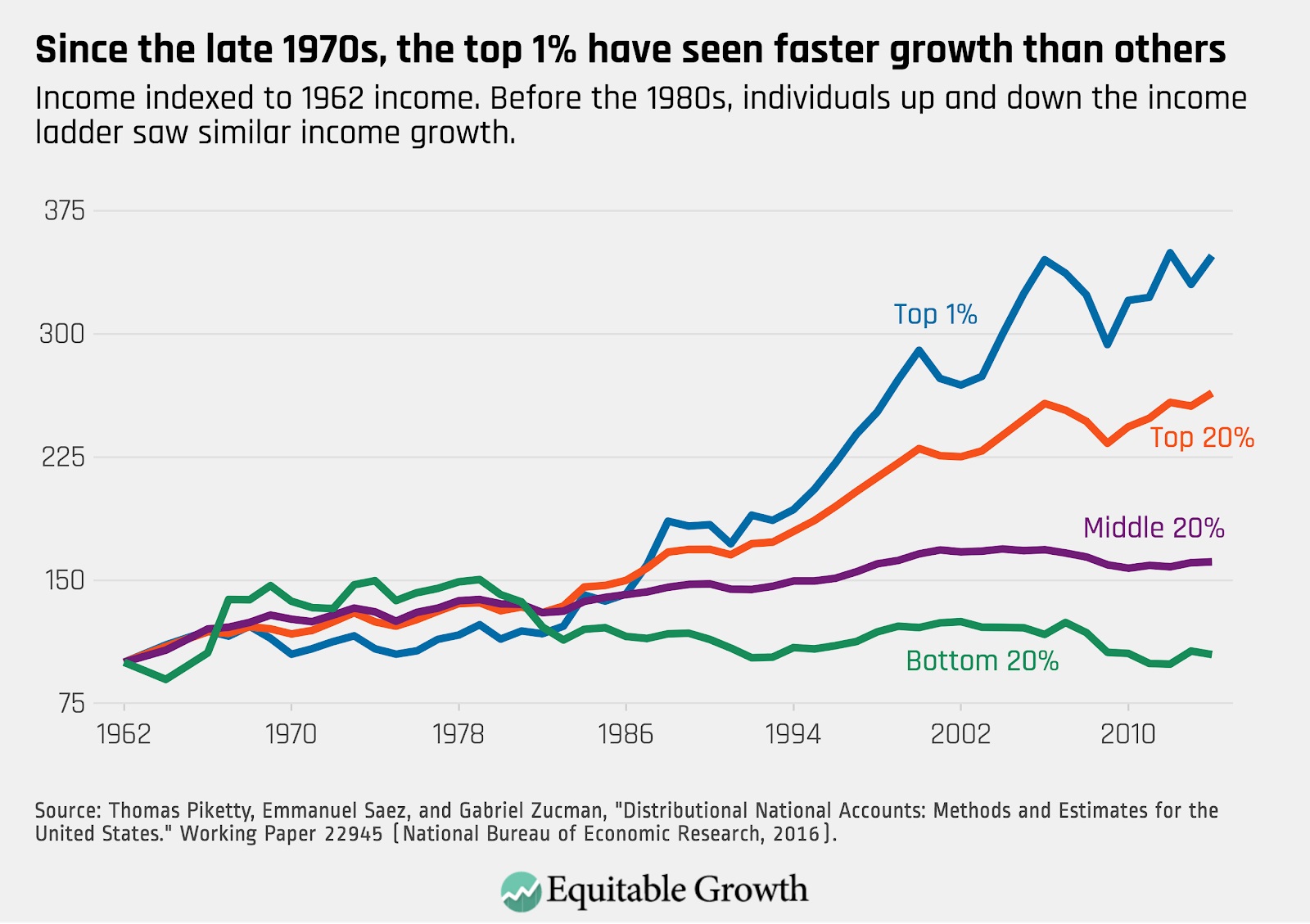

Post Tax Income growth 2

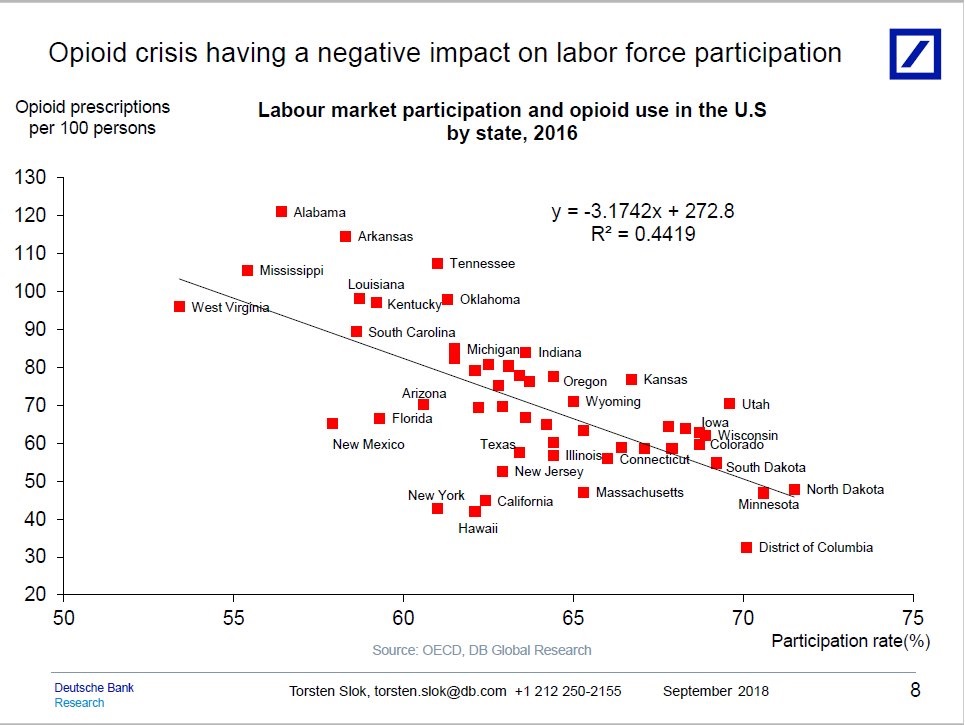

Labour Market Participation & Opioid Use

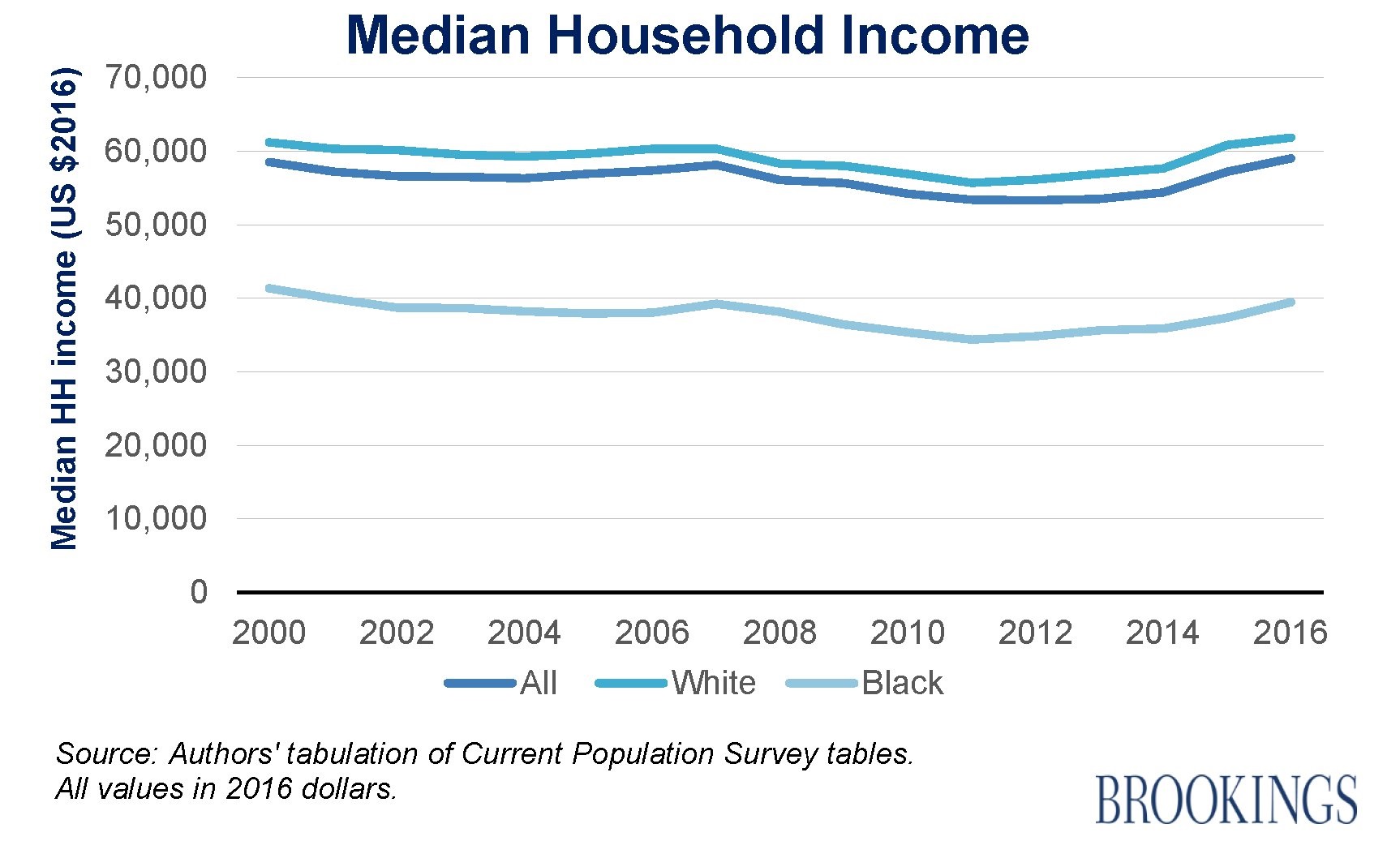

US – Median Household Income

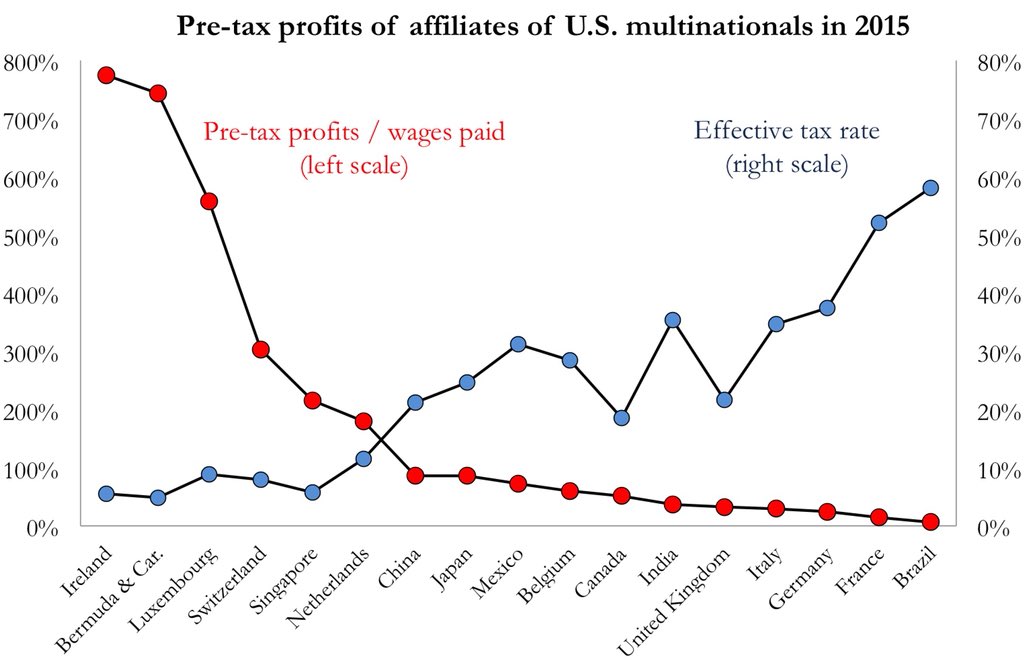

Pre Tax profits of US Multinationals

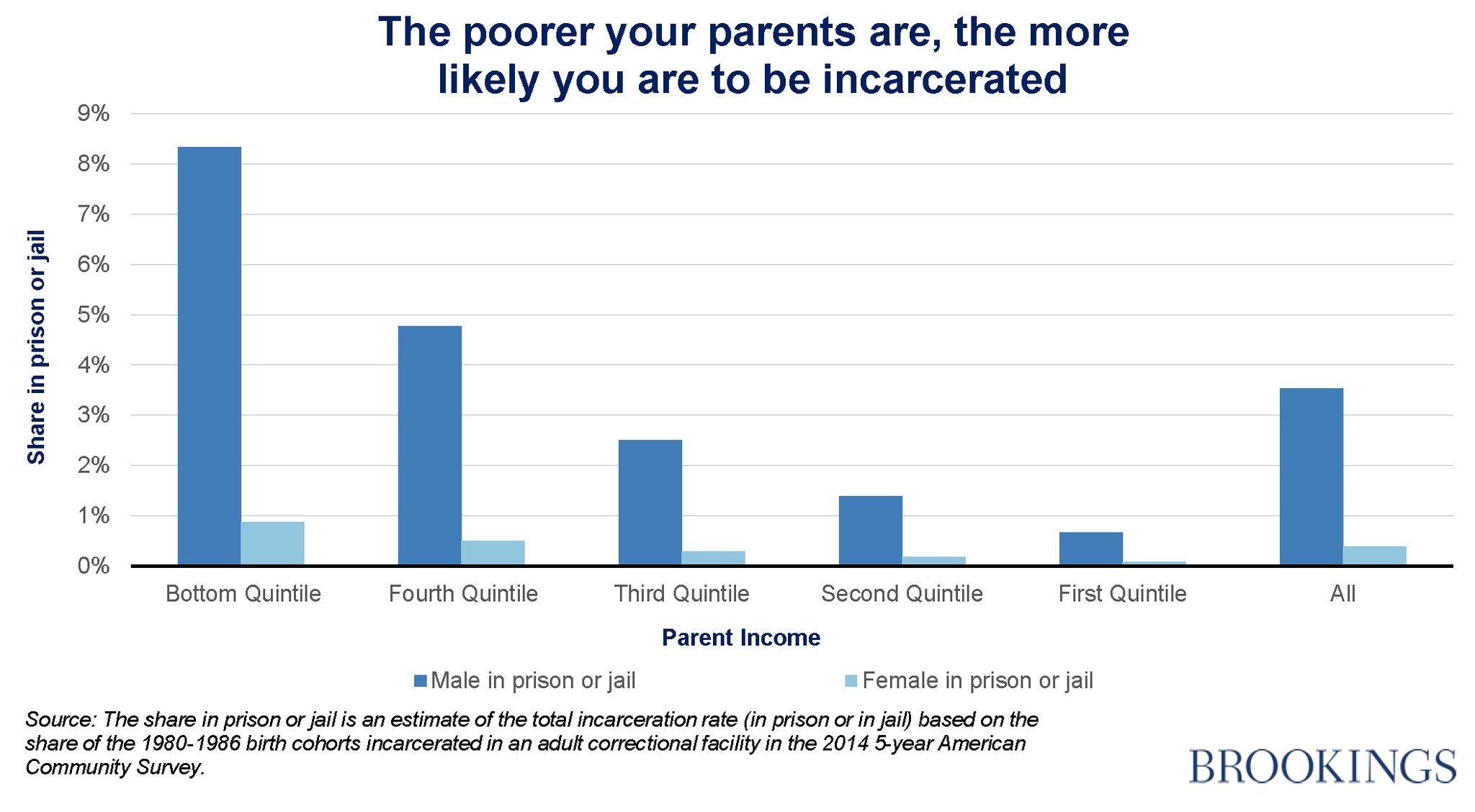

United States – Poverty & Incarceration

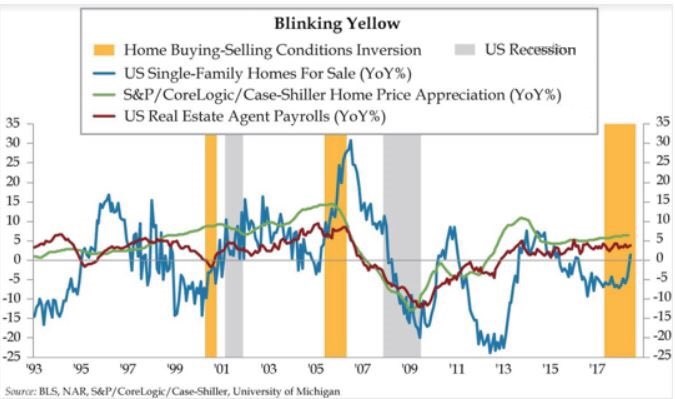

US Real Estate

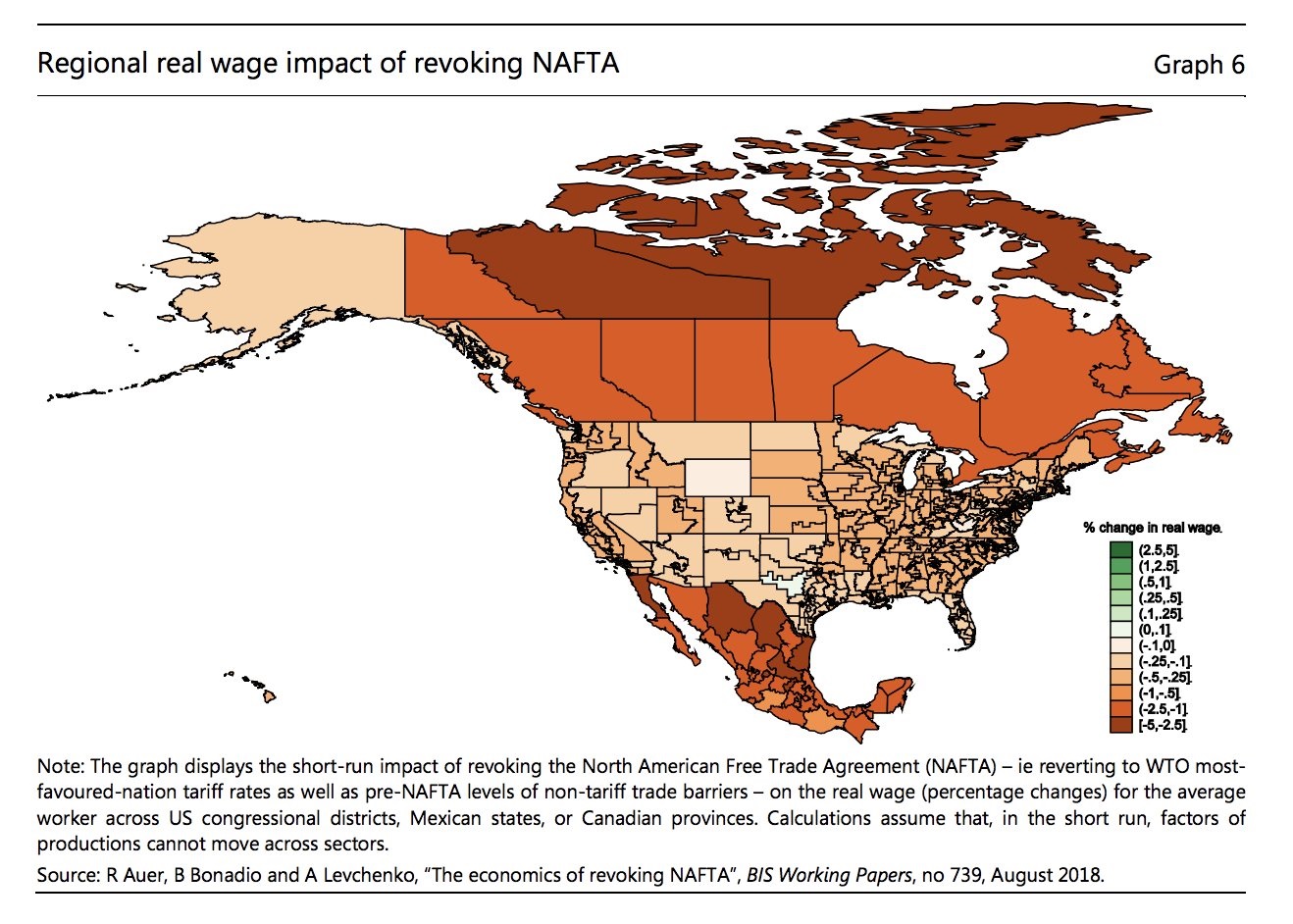

Impact of Revoking NAFTA

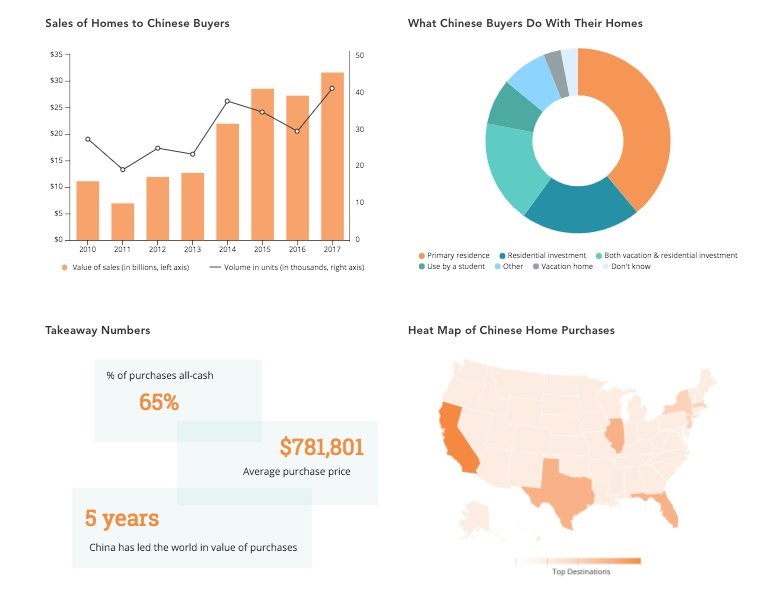

US Real Estate – Chinese Buyers

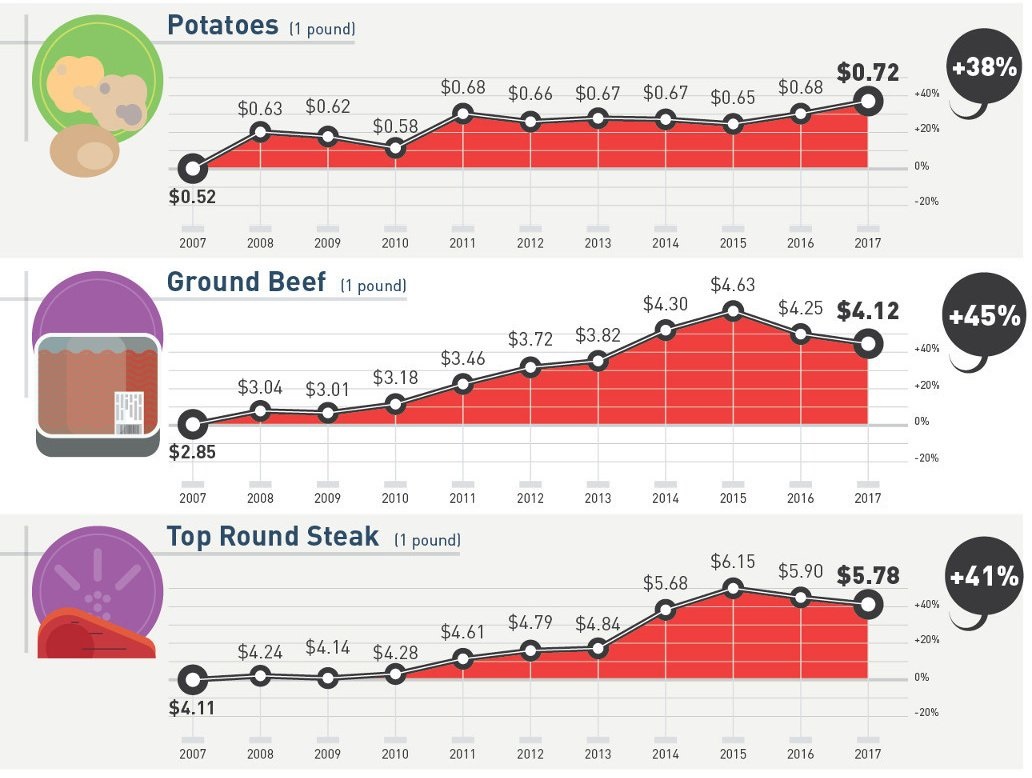

US Staple Food Items – Prices

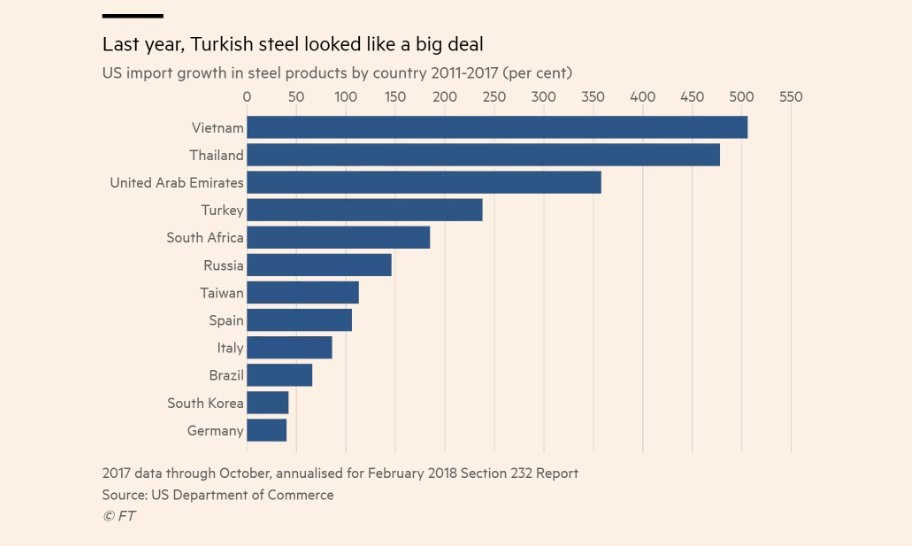

US Steel Imports

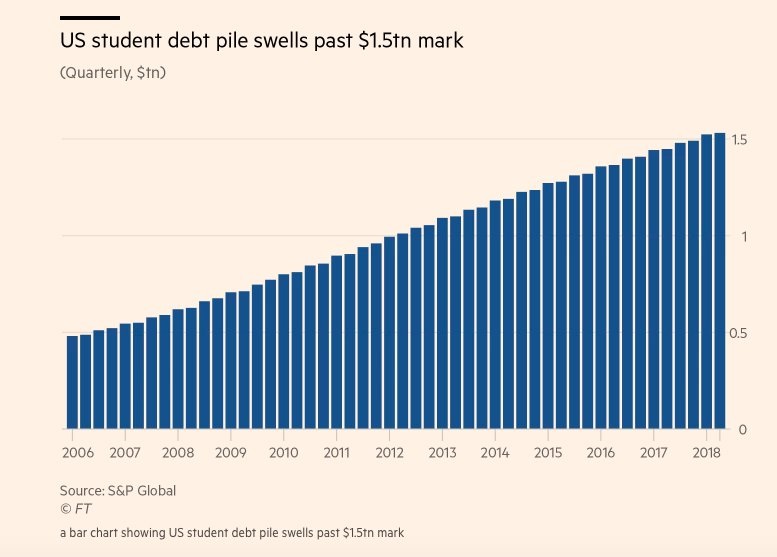

US Student Debt

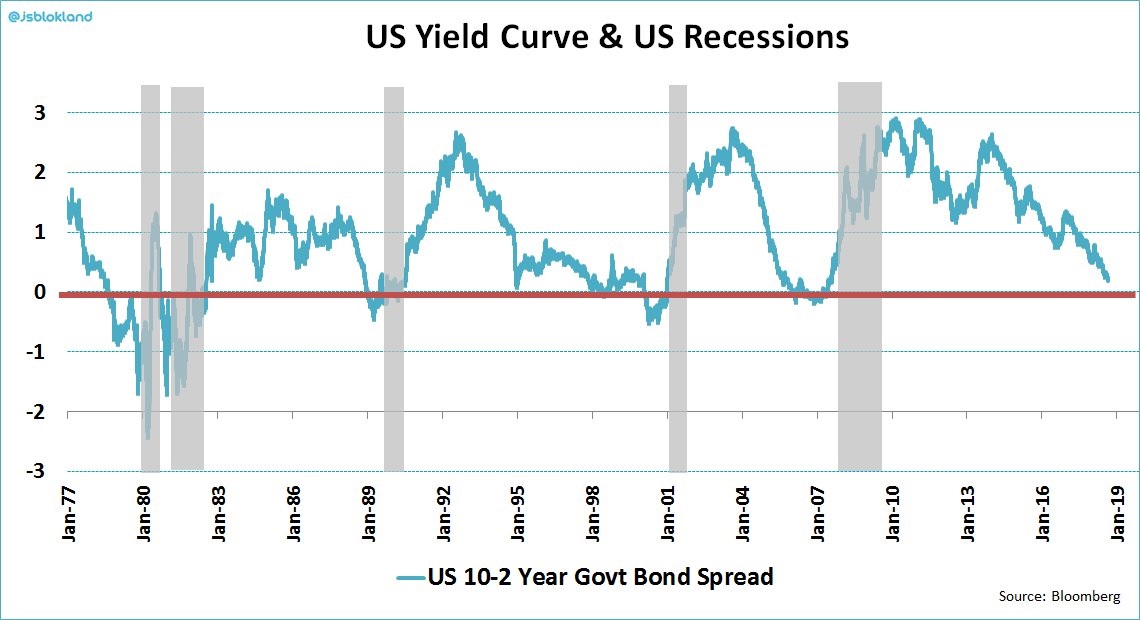

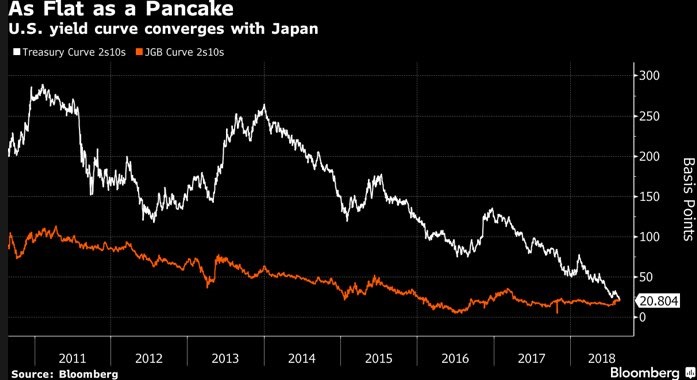

US Yield Curve & Recessions

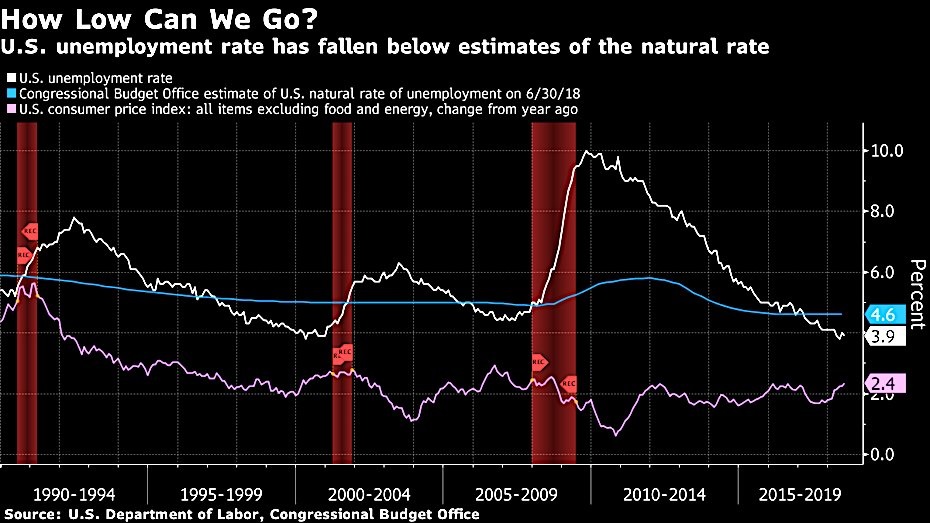

US Unemployment

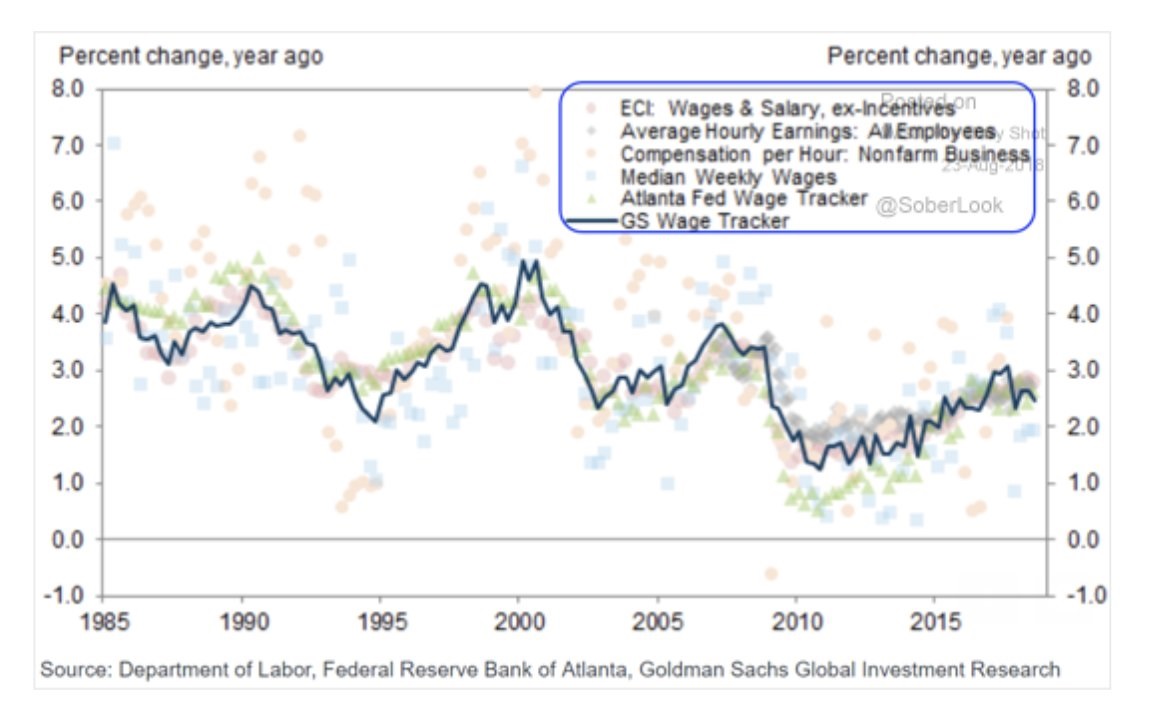

US Wages

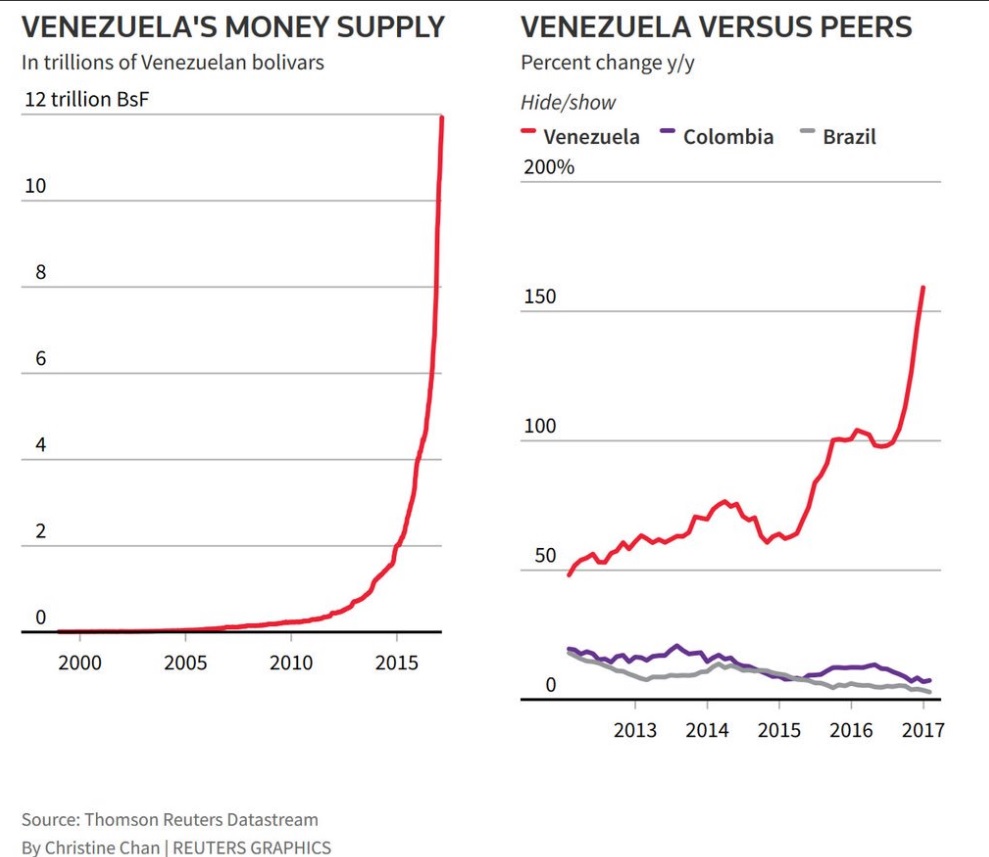

Venezuela Money Supply

Europe

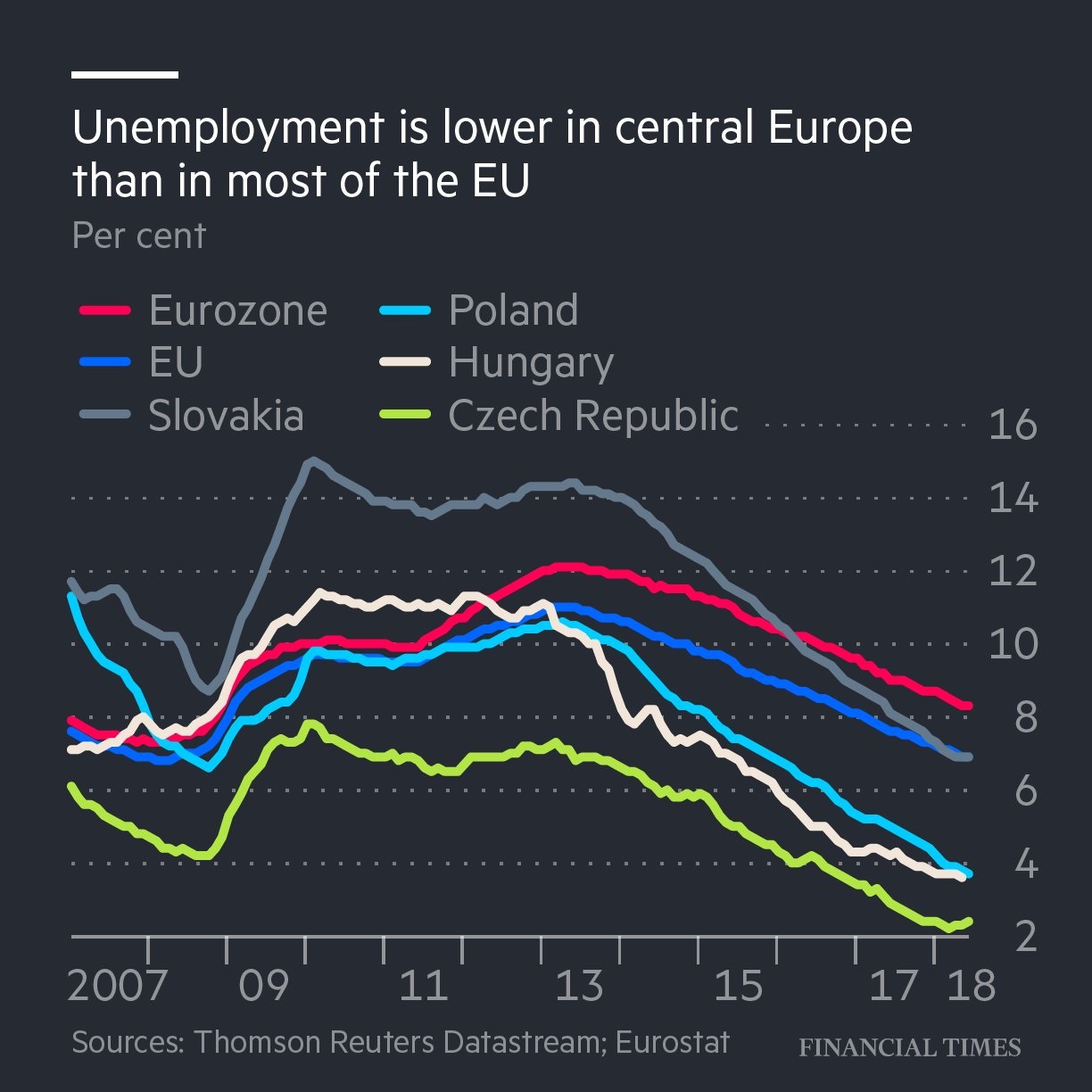

Unemployment – Central Europe

Wages – Central Europe

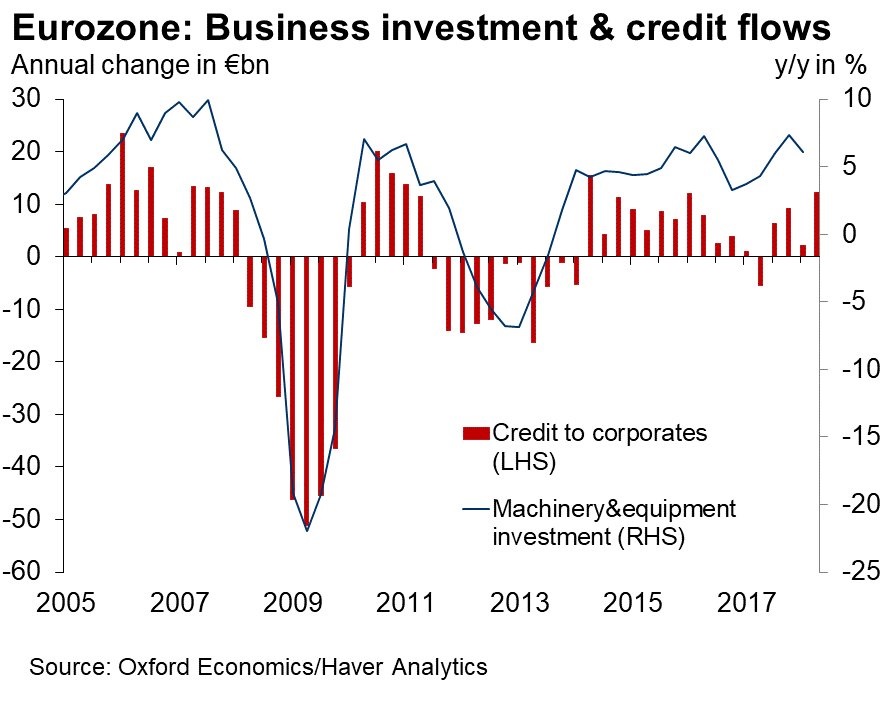

Business Investment & Credit

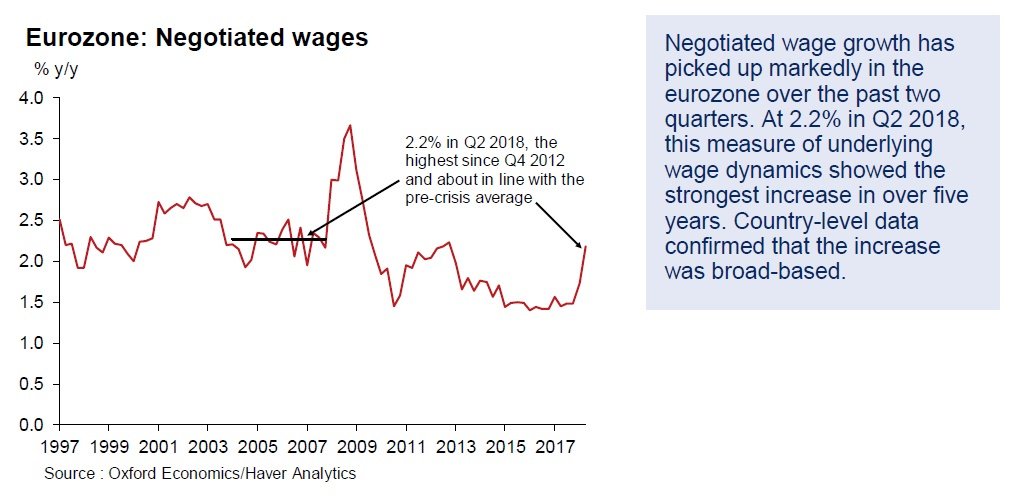

Eurozone – Negotiated Wages

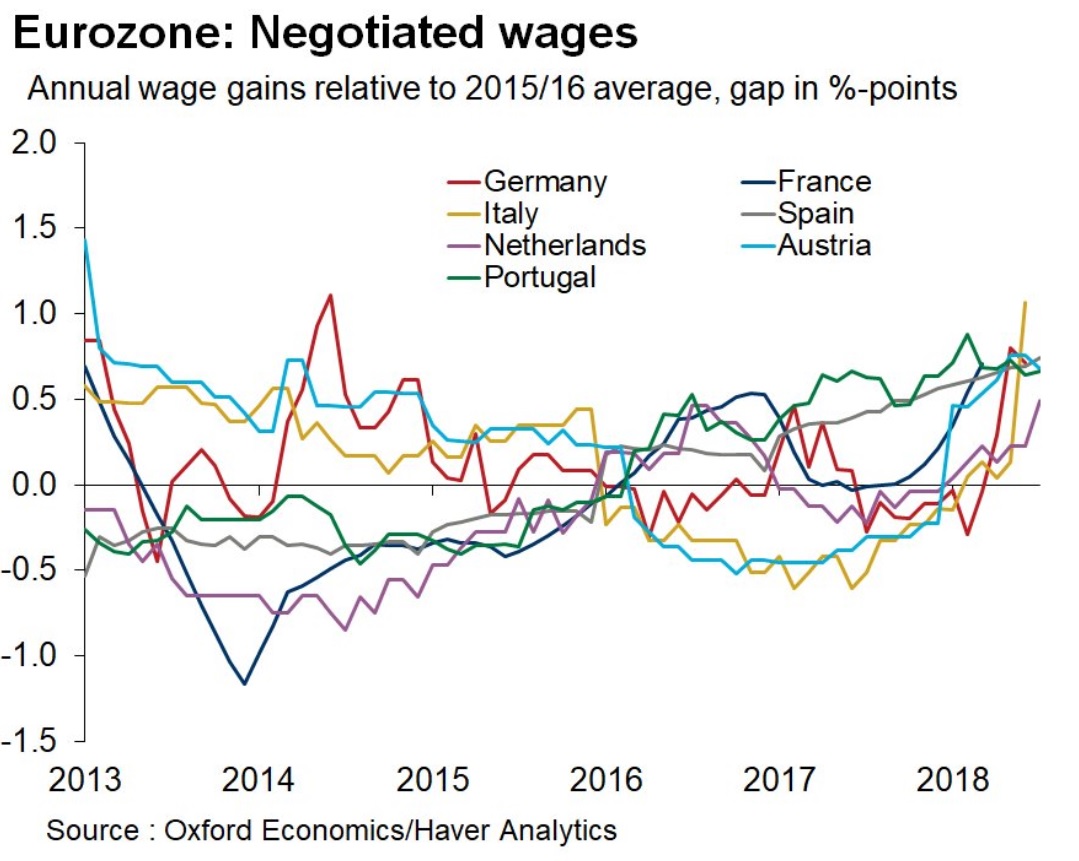

Eurozone – Negotiated Wages 2

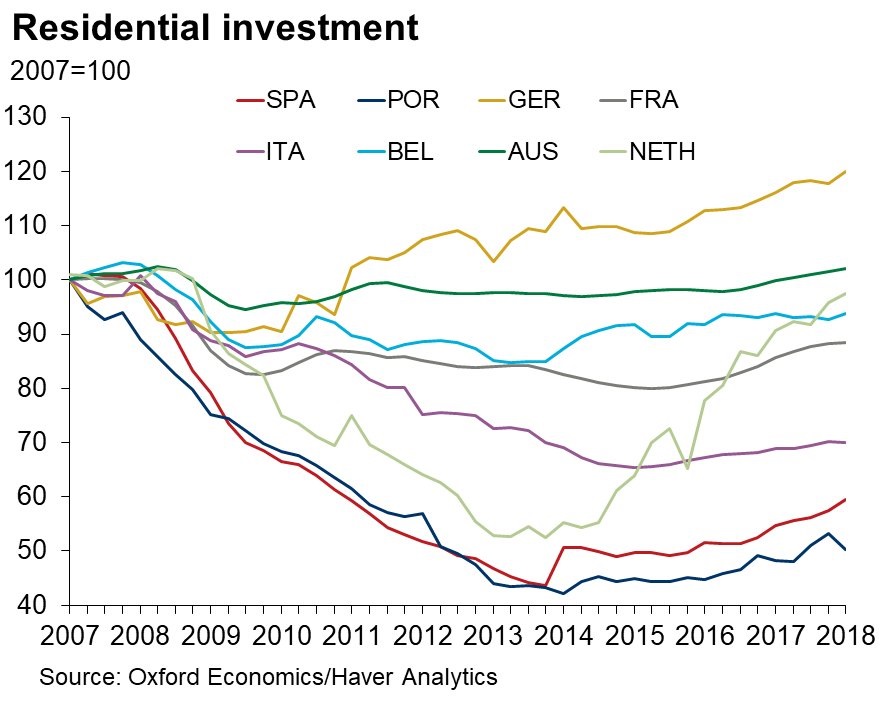

Residential Investment – Selected Euro Nations

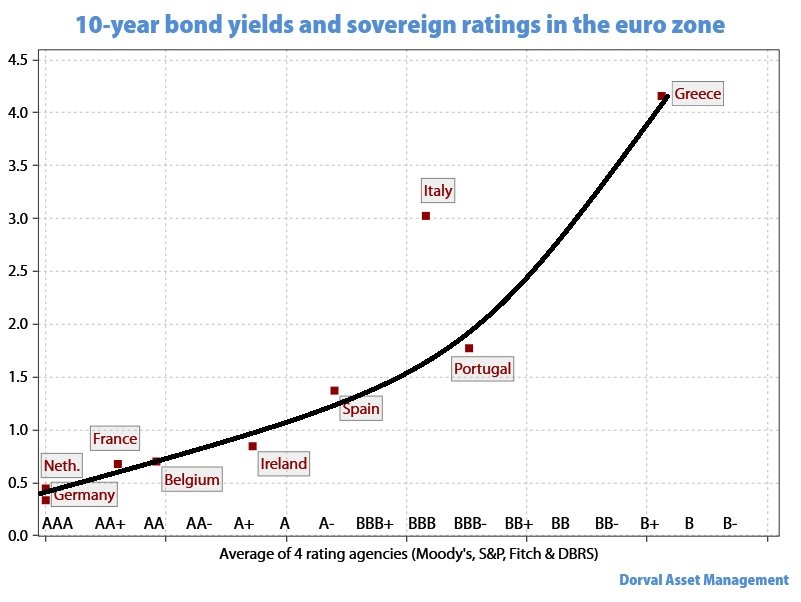

Euro Sovereign Ratings & 10Yrs

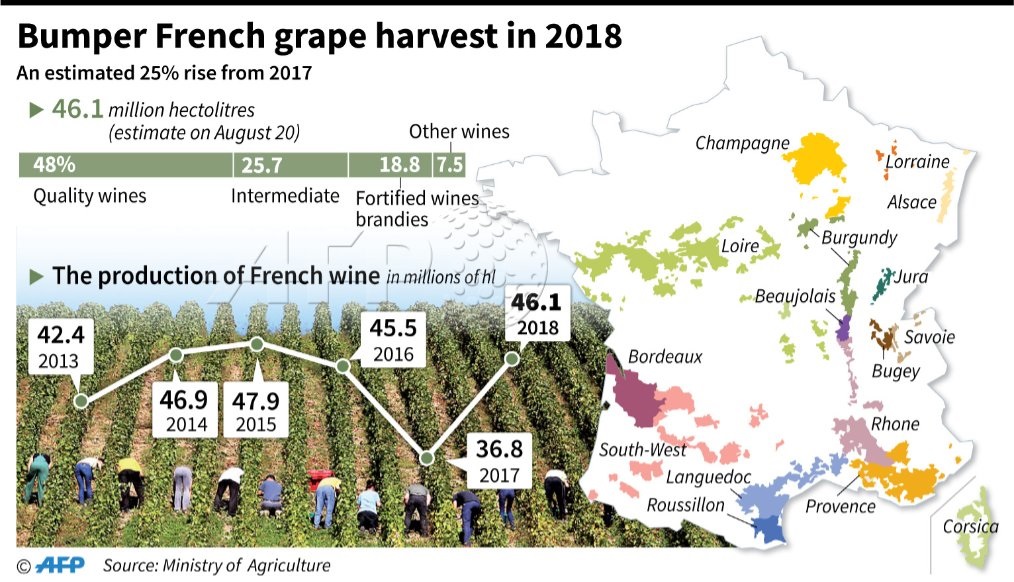

French Grape Harvest 2018

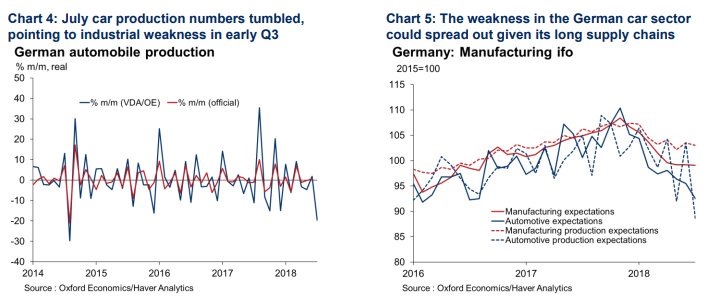

Germany Automobile Production & Manufacturing Sentiment

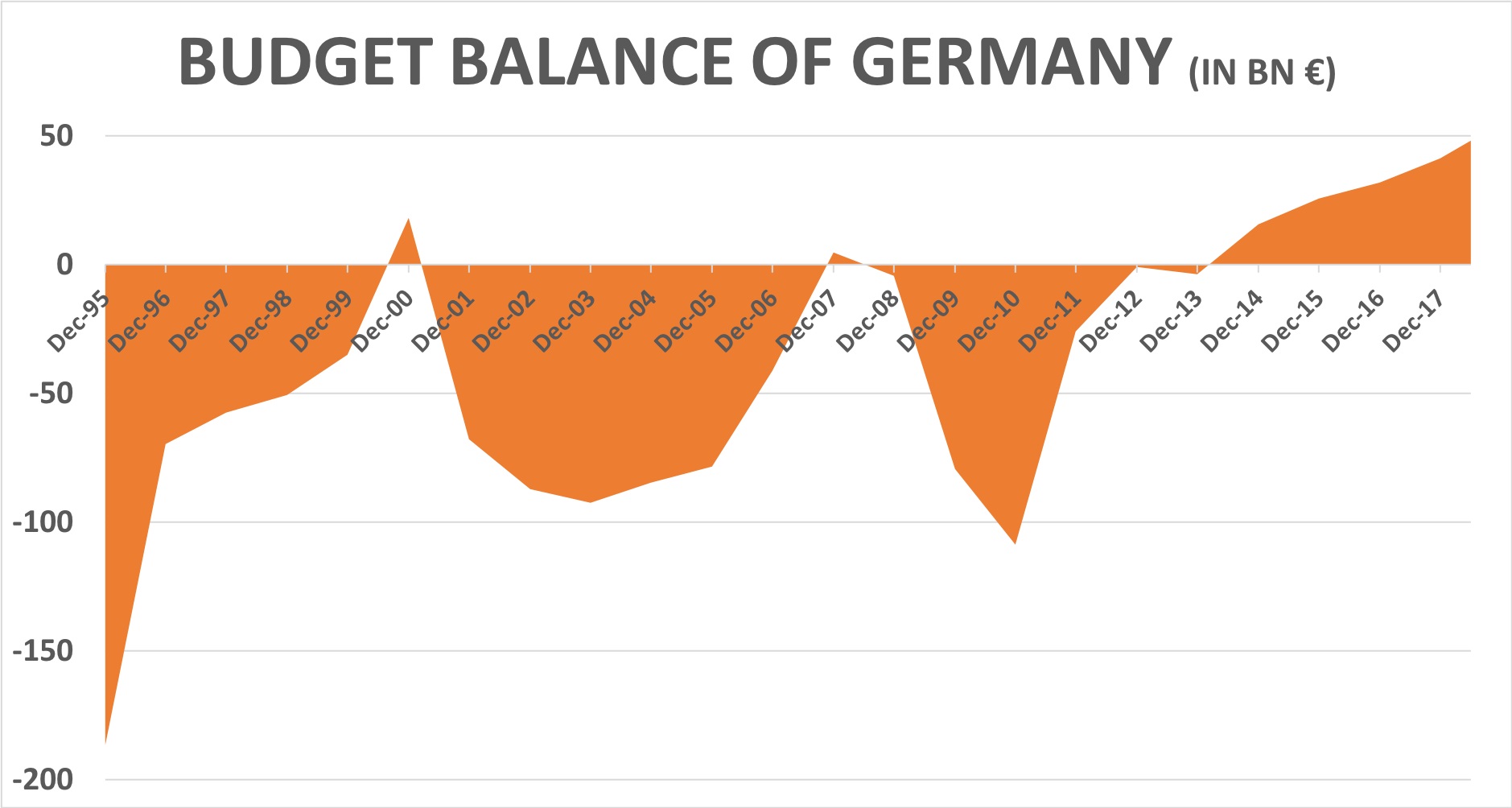

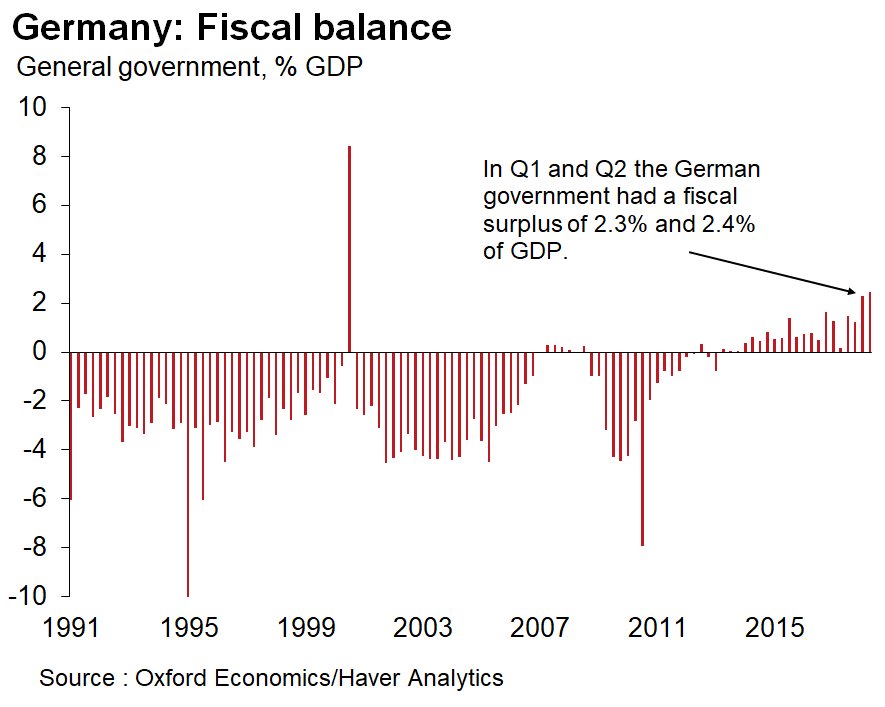

Germany – Budget Balance

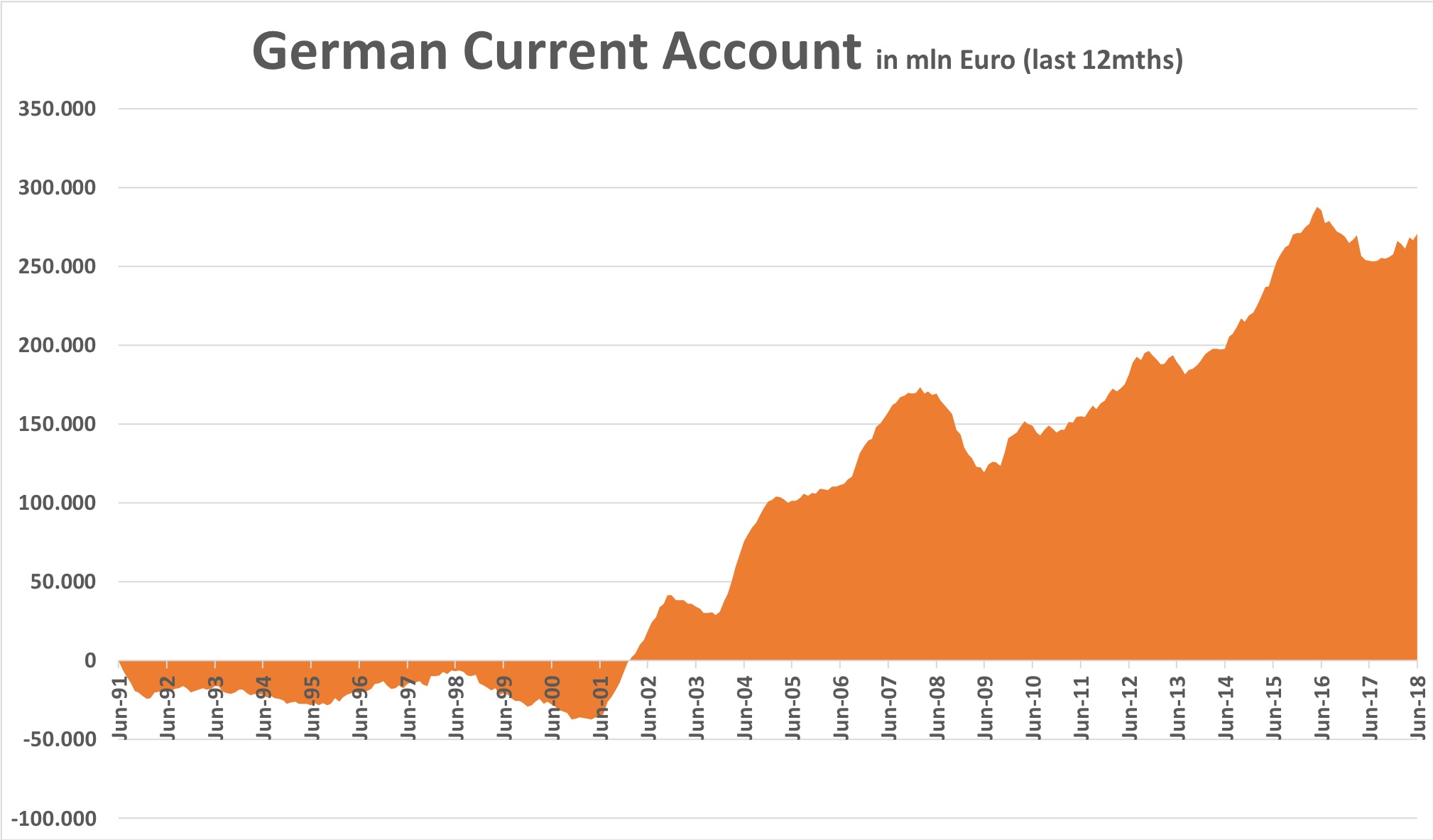

Germany – Current Account

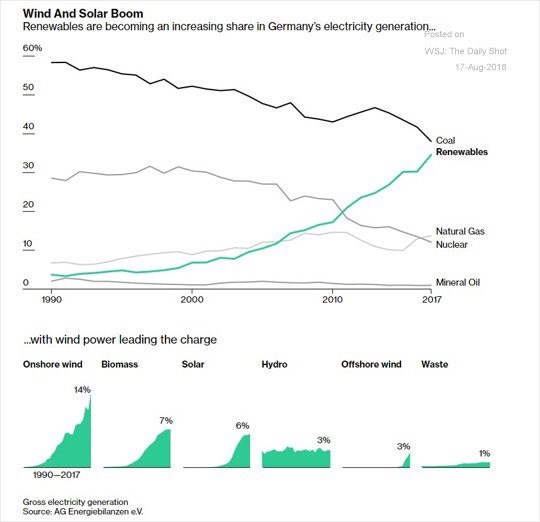

Germany – Renewable Energy

Germany – Fiscal Balance

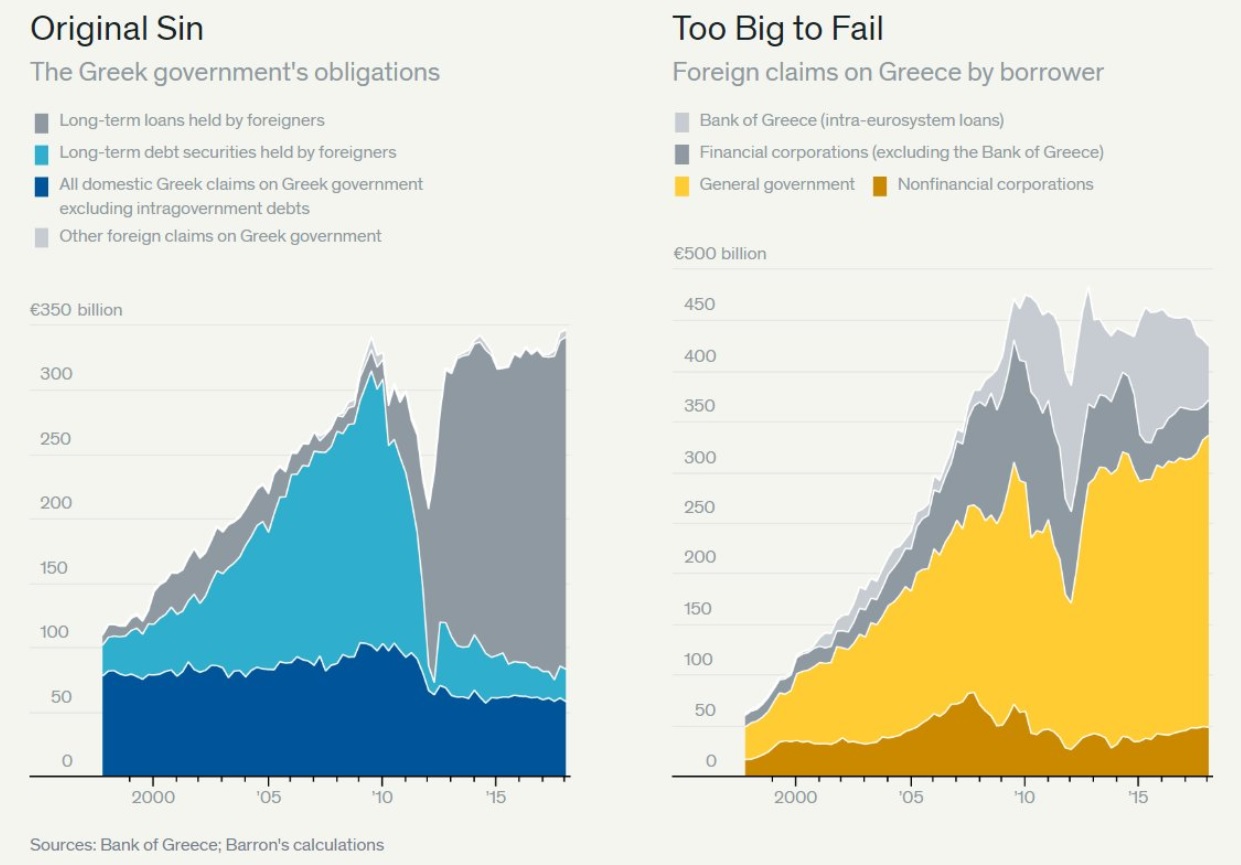

Greece – Debt

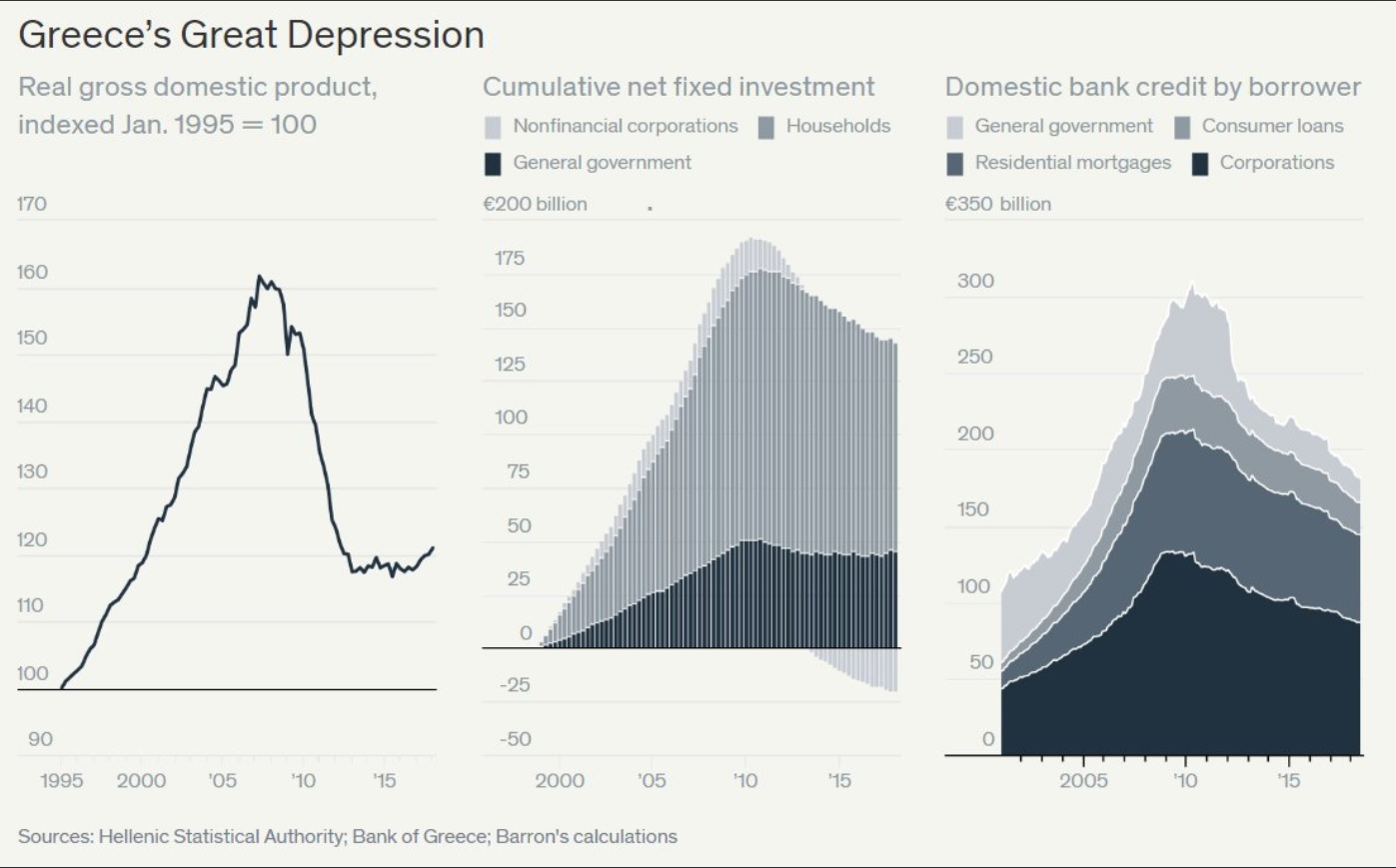

Greece – Depression

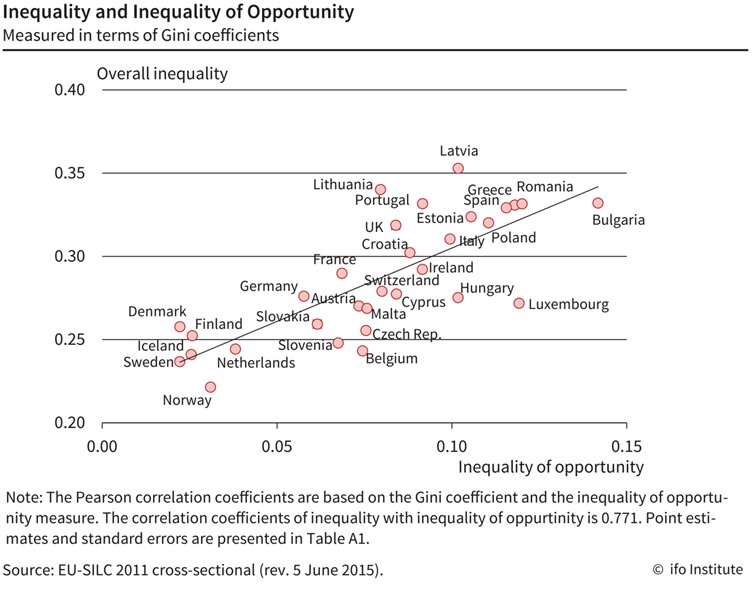

Eurozone – Inequality

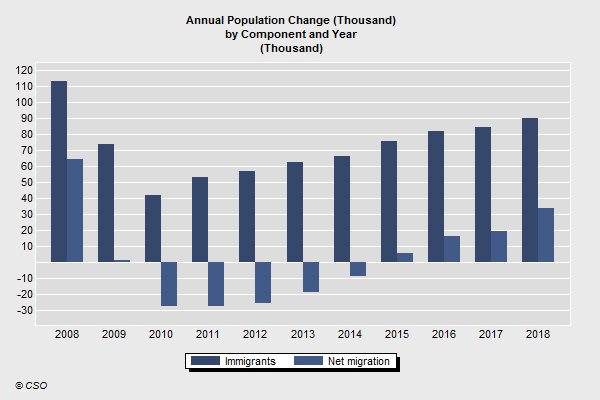

Ireland – Immigration

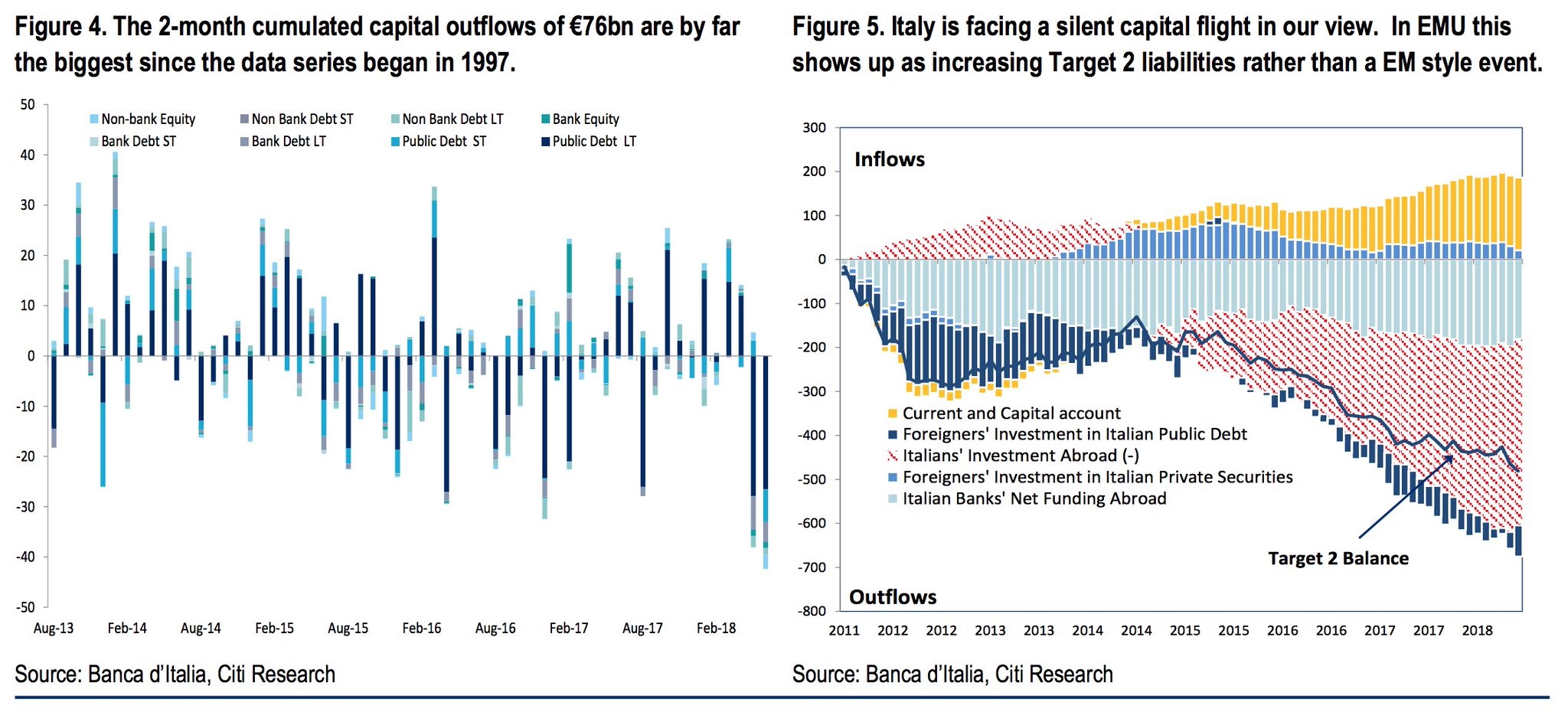

Italy – Capital Flows

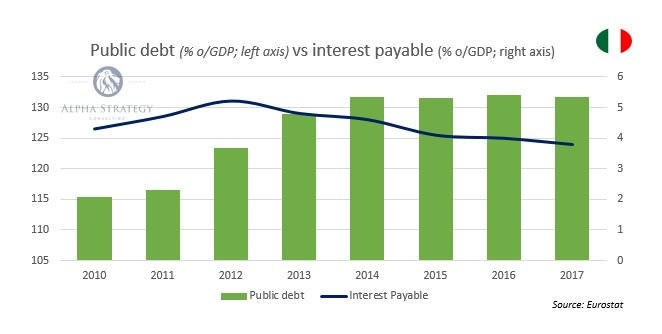

Italy – Public Debt & Interest

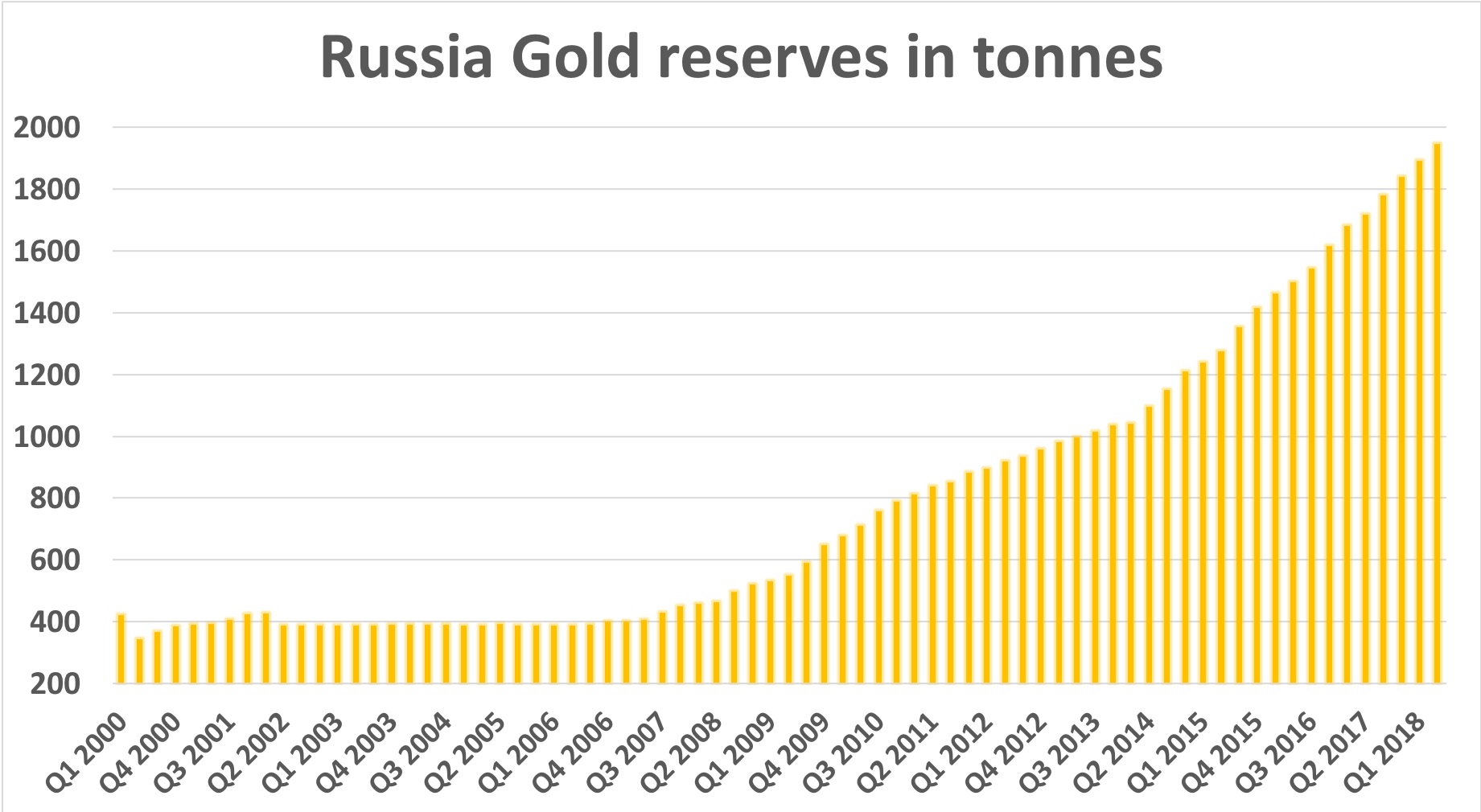

Russia – Gold Reserves

Russian Economy in Relation to Europe

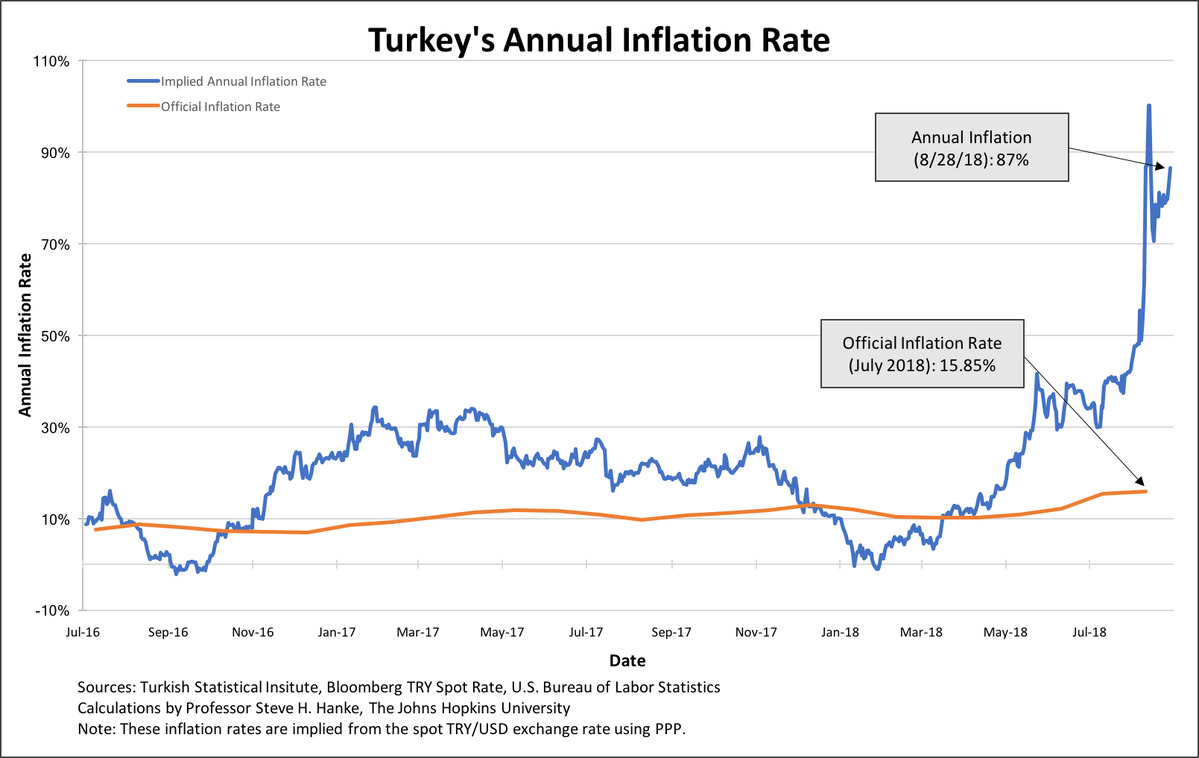

Turkey – Inflation

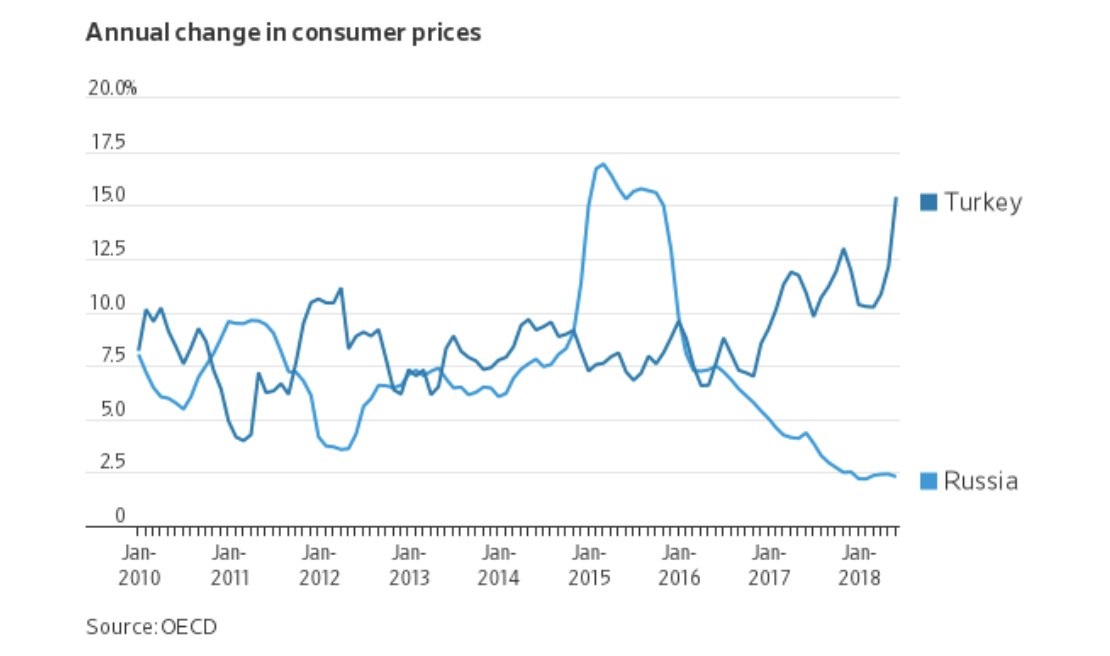

Turkey & Russia – Consumer Prices

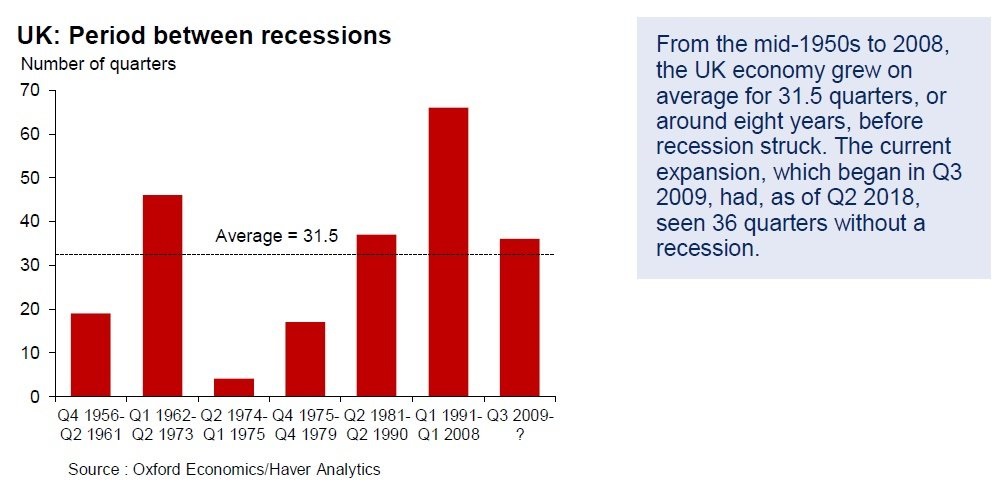

United Kingdom – Time Between Recessions

China & Asia

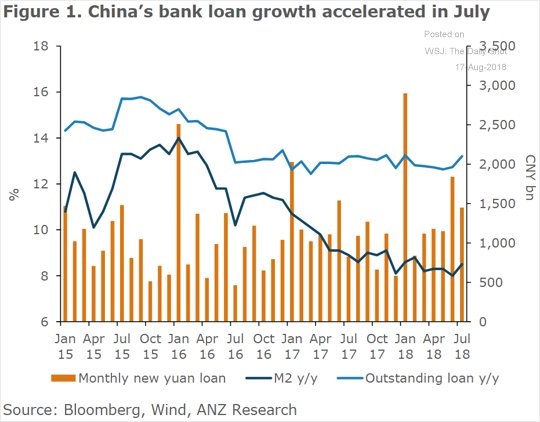

China – Bank Lending

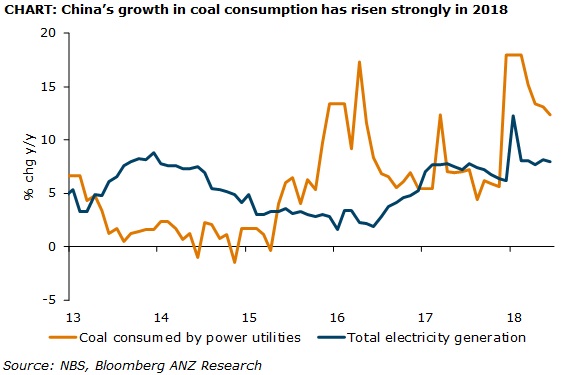

China – Coal Consumption

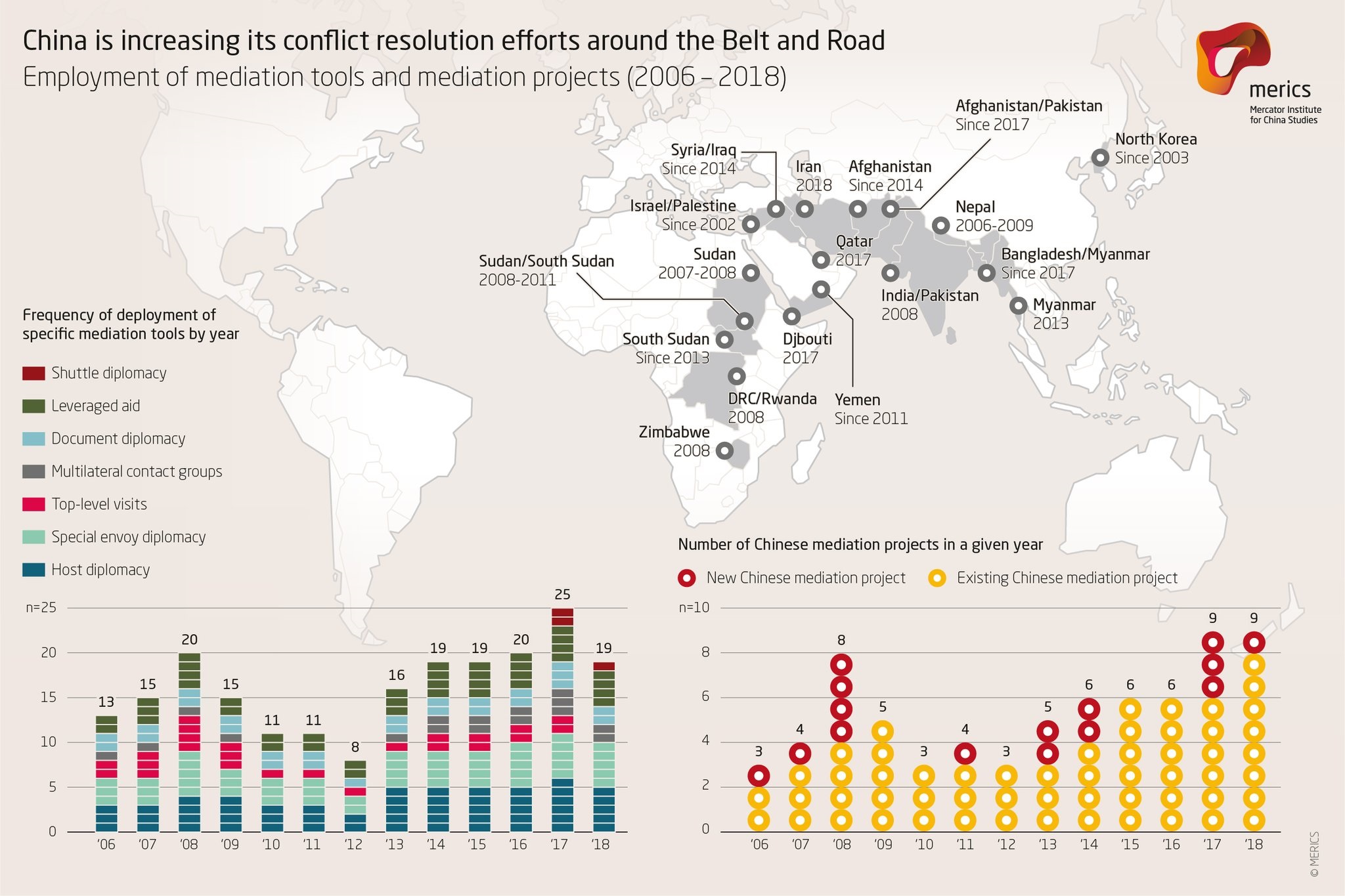

China – Global Conflict Resolution Efforts

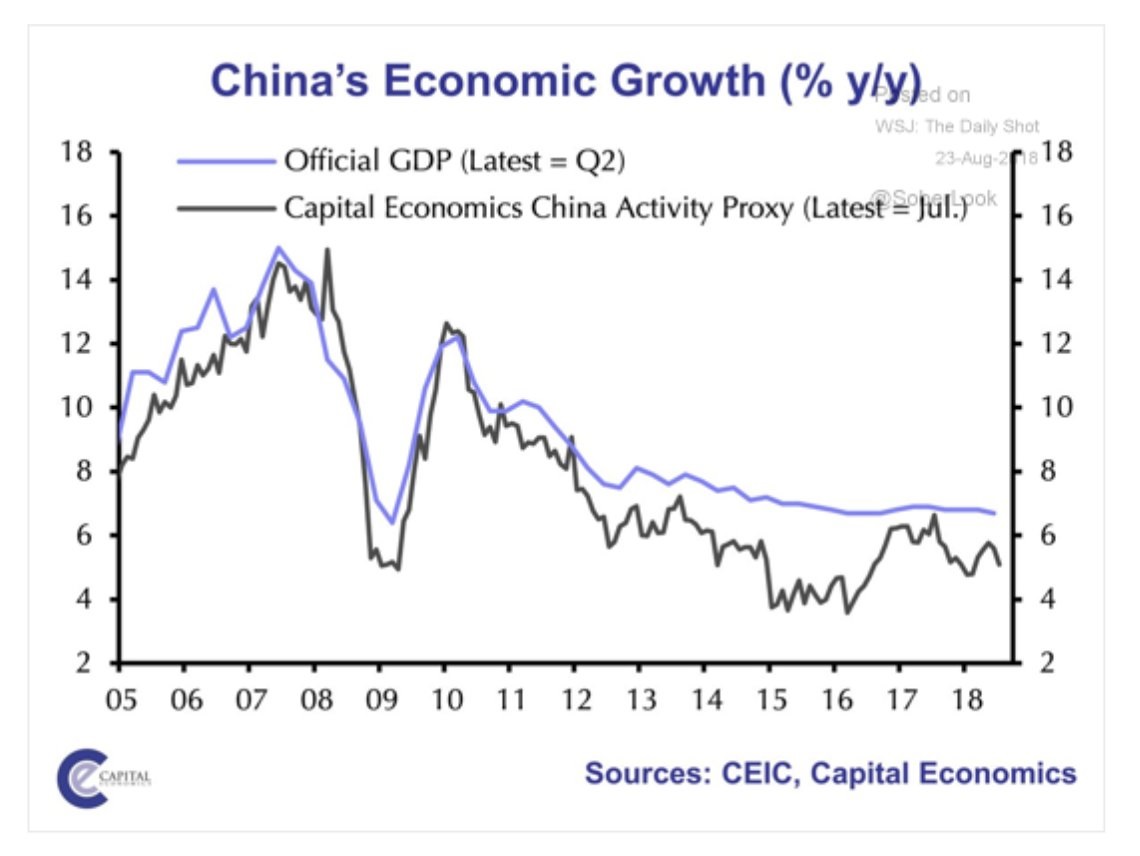

China – Economic Growth

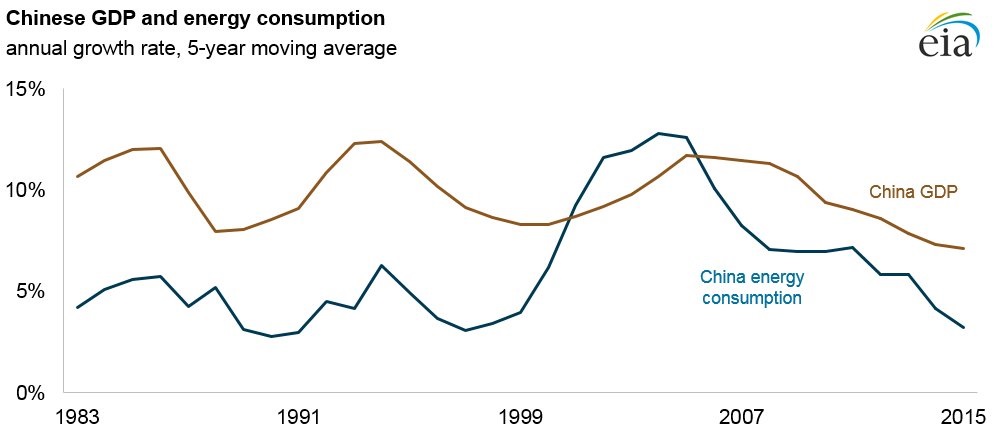

China – GDP & Energy Consumption

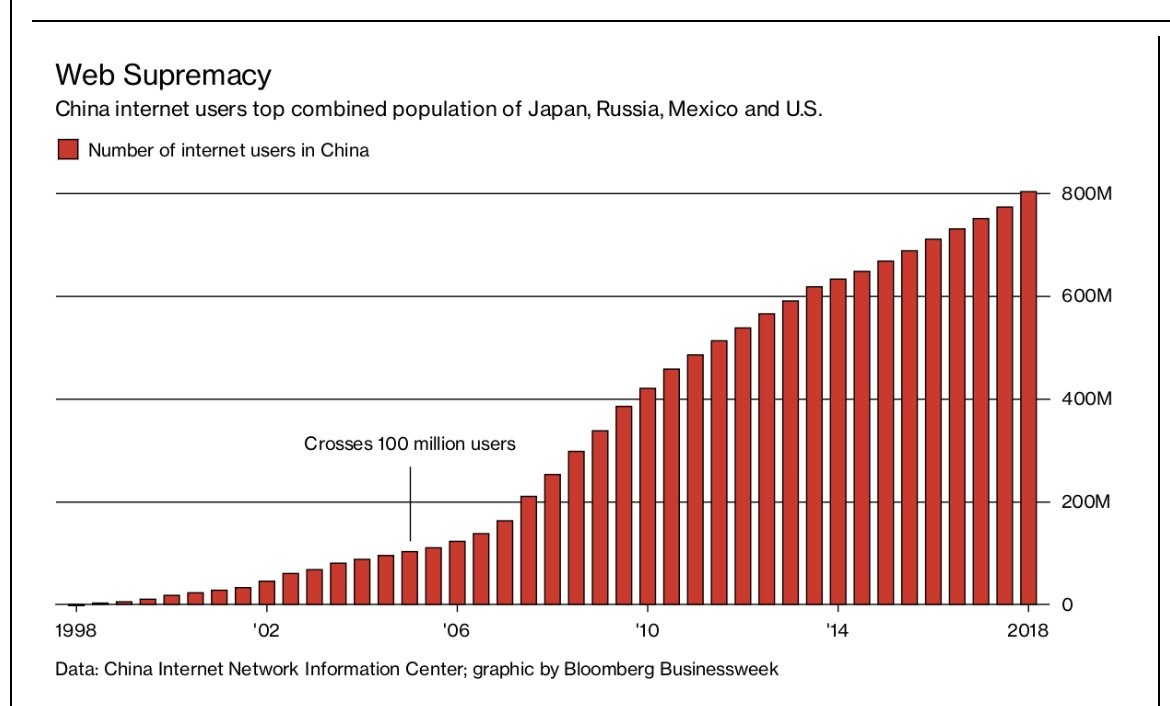

China – Internet Users

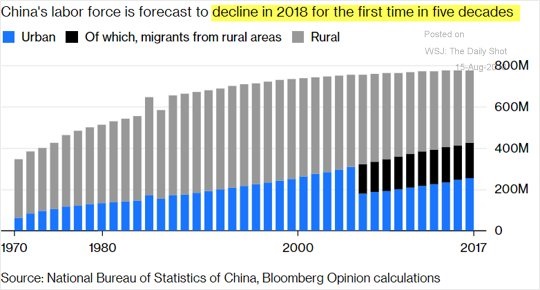

China – Labour Force

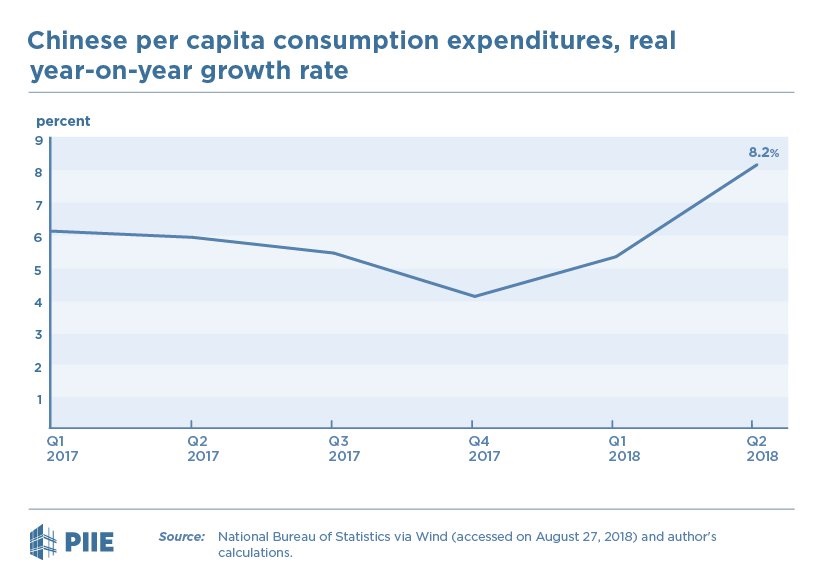

China – Per Capita Consumption

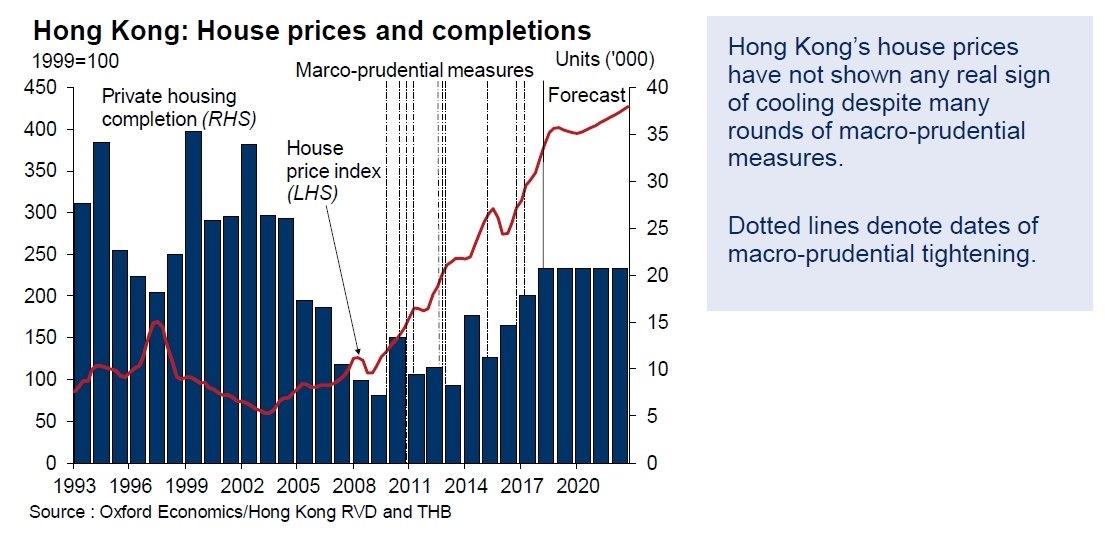

Hong Kong – House Prices & Completions

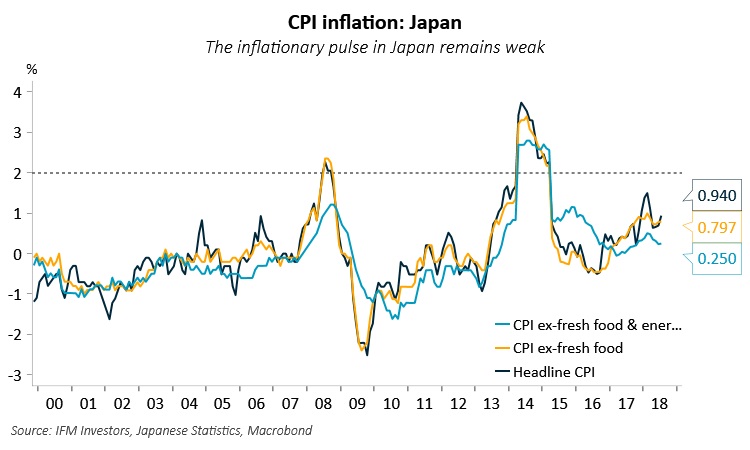

Japan – CPI

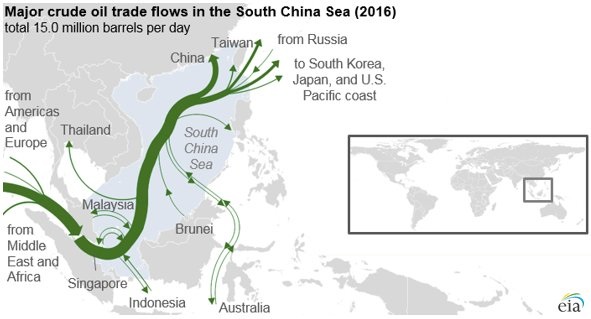

South China Sea – Crude Oil Flows

South Korea – Goods & Services Exports

Commodities

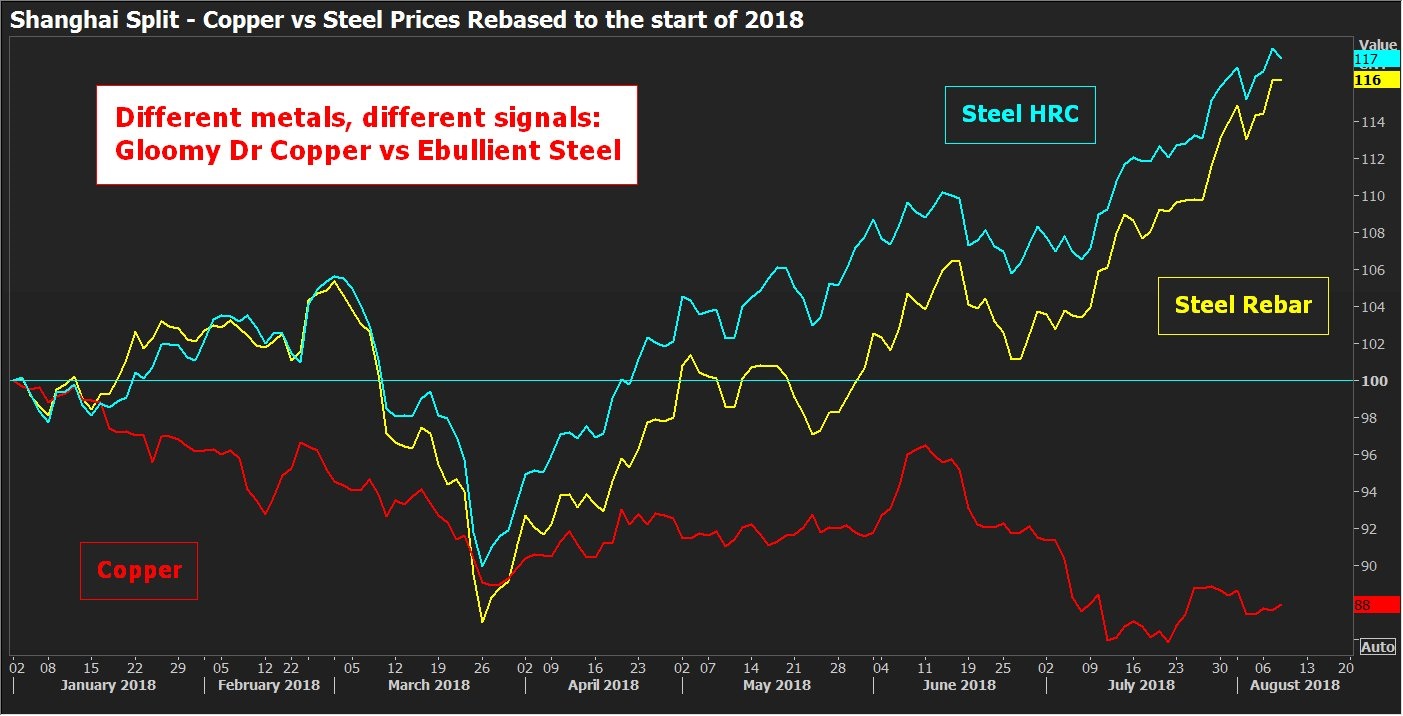

Steel & Copper – Shanghai Prices

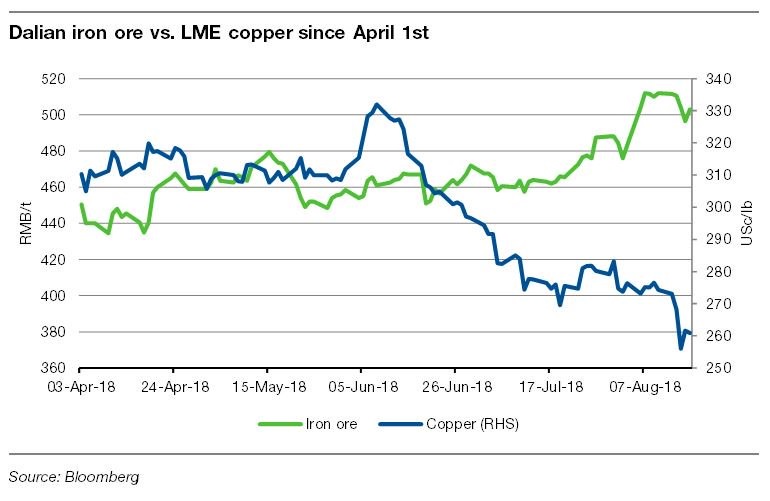

Dalian Iron Ore v Copper

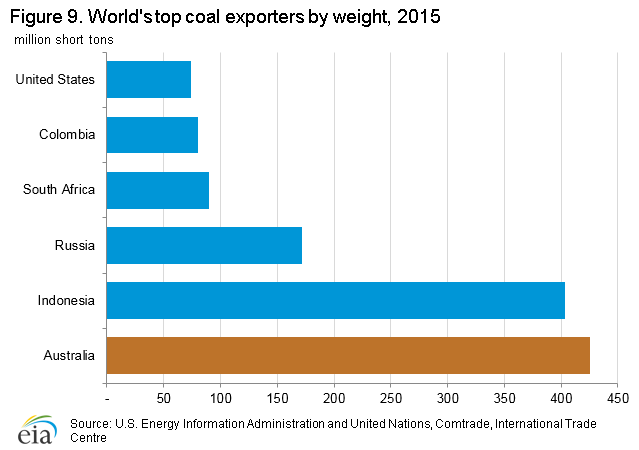

Coal Exporters

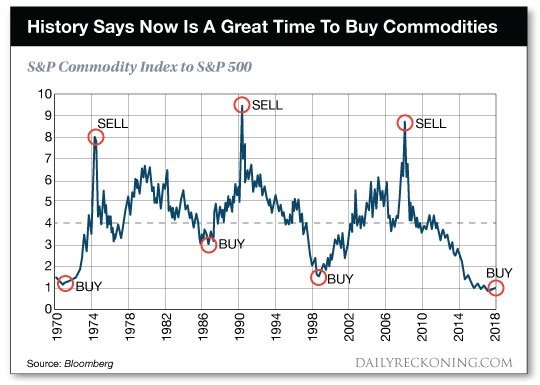

Commodities Per Se – Time to Buy?

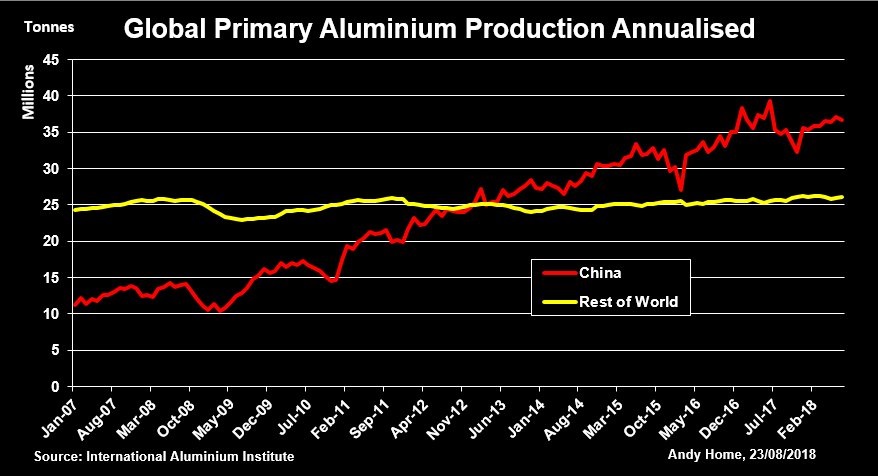

Global Aluminium – China v Rest of World

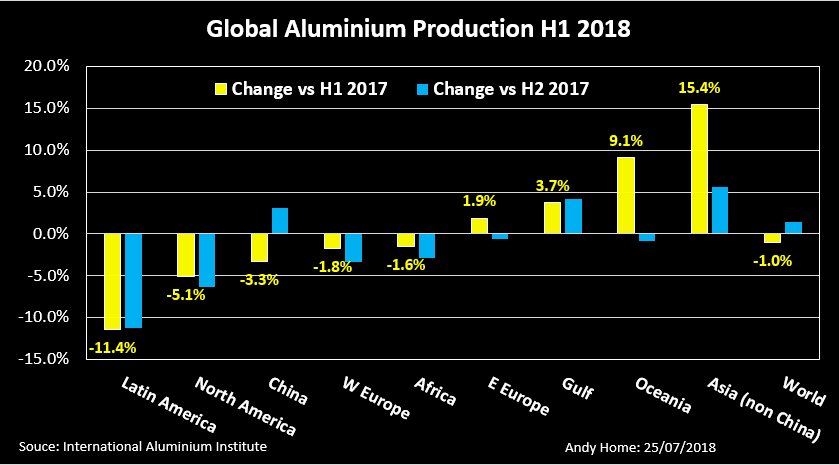

Aluminium – 2018 Production by Region

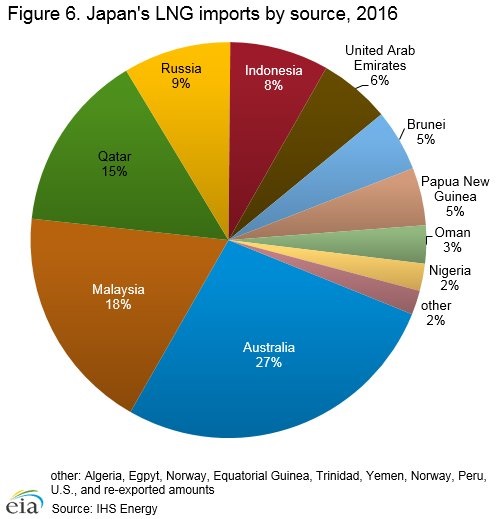

Japan – LNG Imports

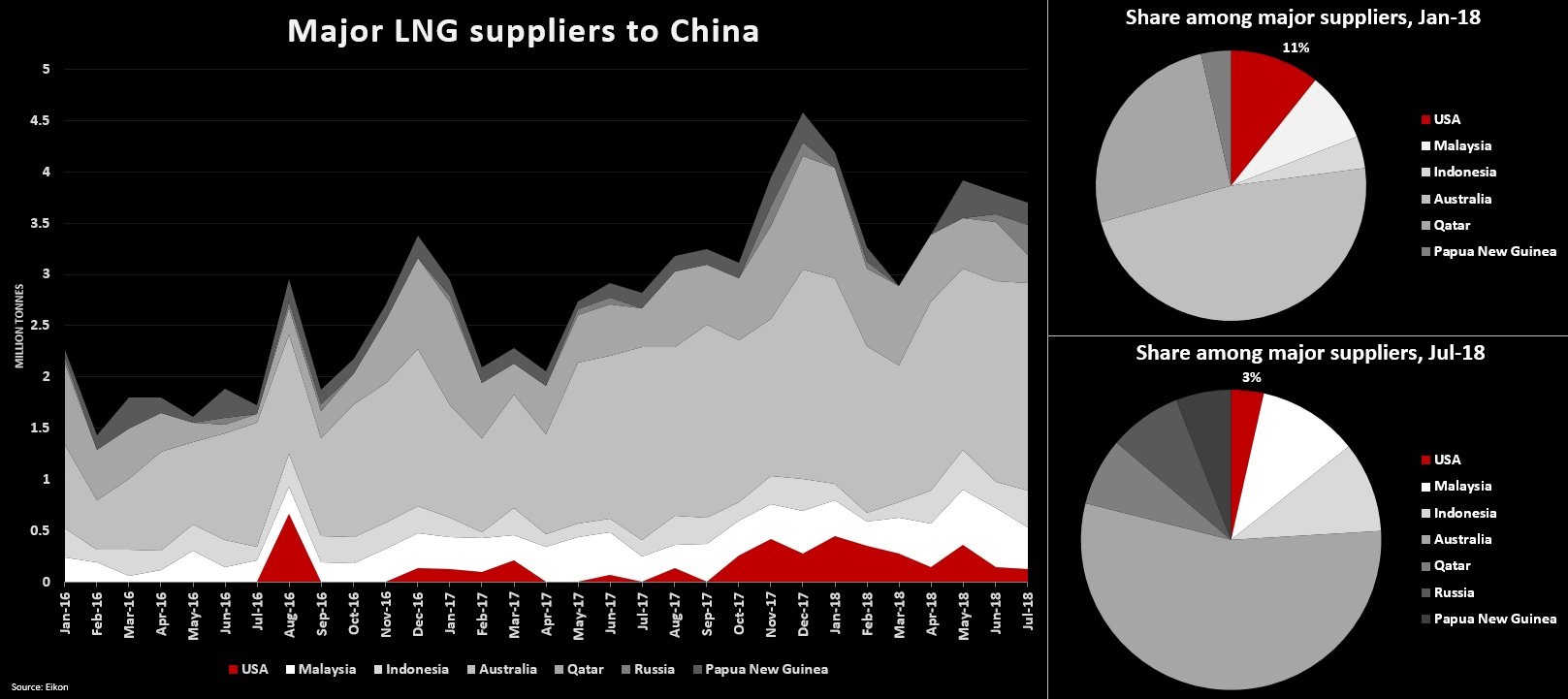

China – LNG Imports

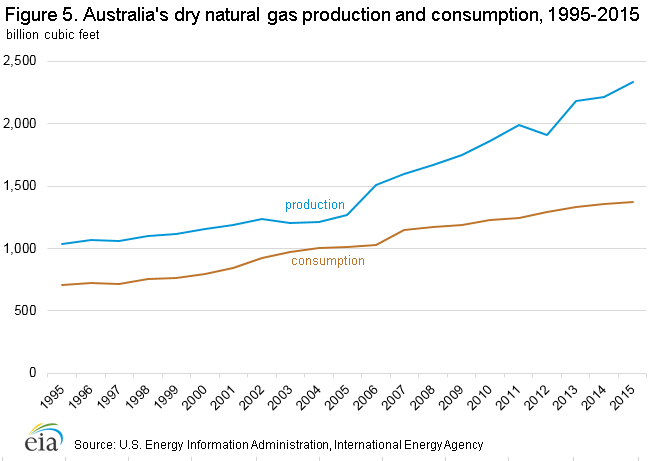

Australia – Natural Gas Consumption & Production

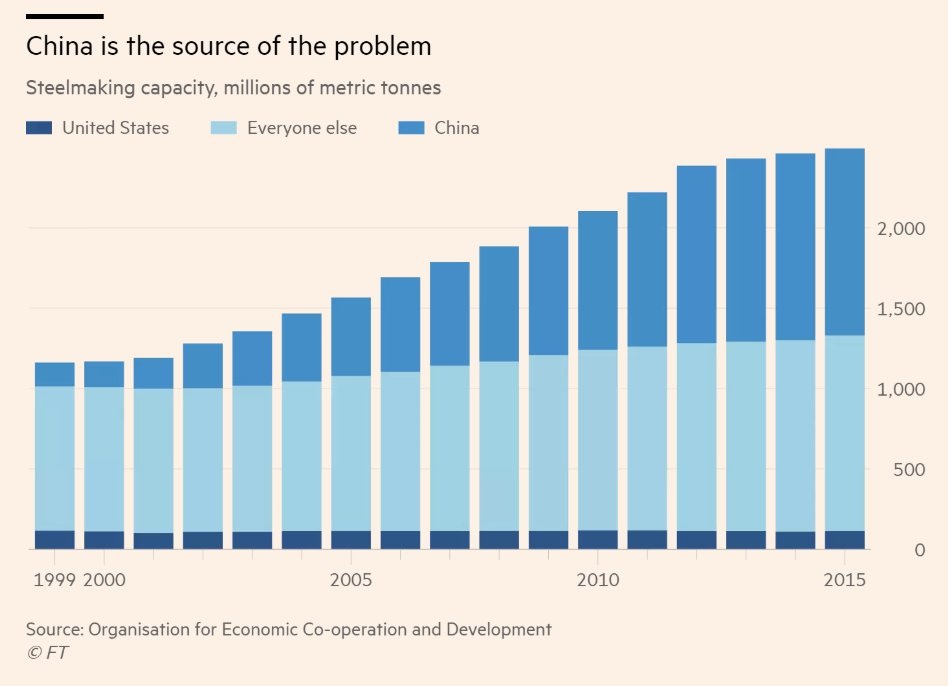

Steelmaking Capacity

Capital Markets

China – NPLs

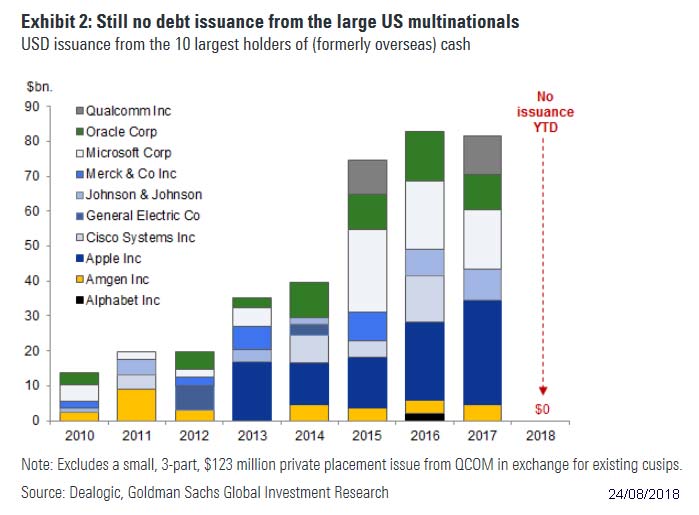

Large US Based Multinationals – 2018 Debt Issuance

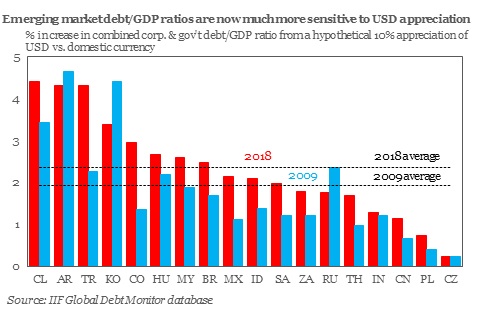

EM Debt to GDP Increases

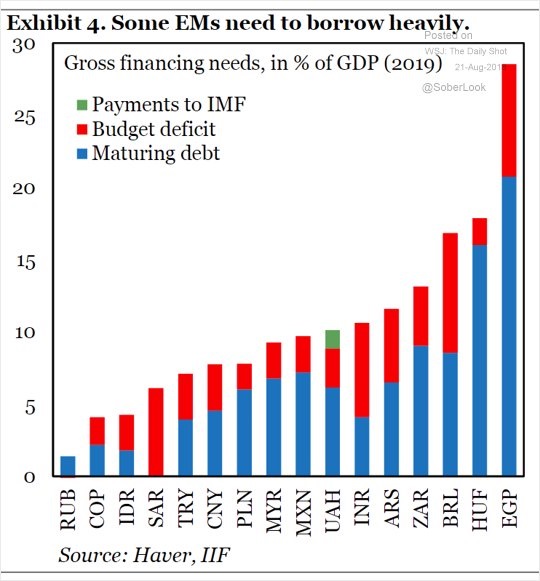

EM Financing Needs

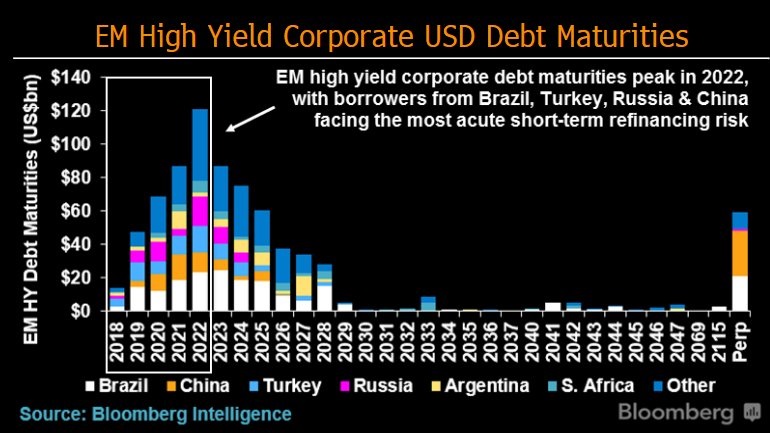

EM High Yield Corporate Debt Maturity Schedule

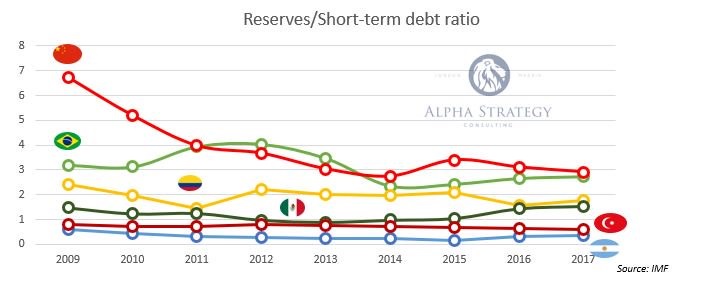

Selected EM – Reserves to Short Term Debt

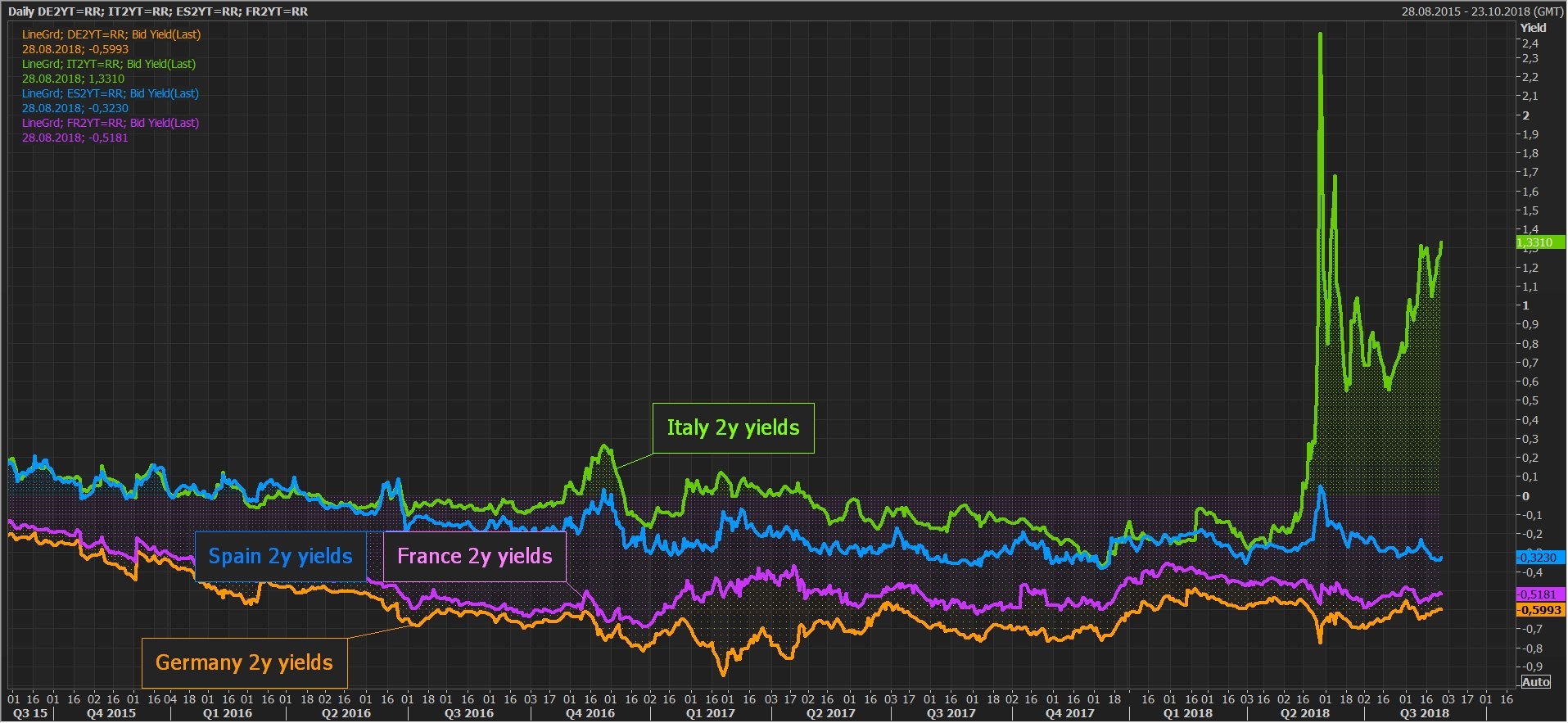

Selected Euro 2Yrs

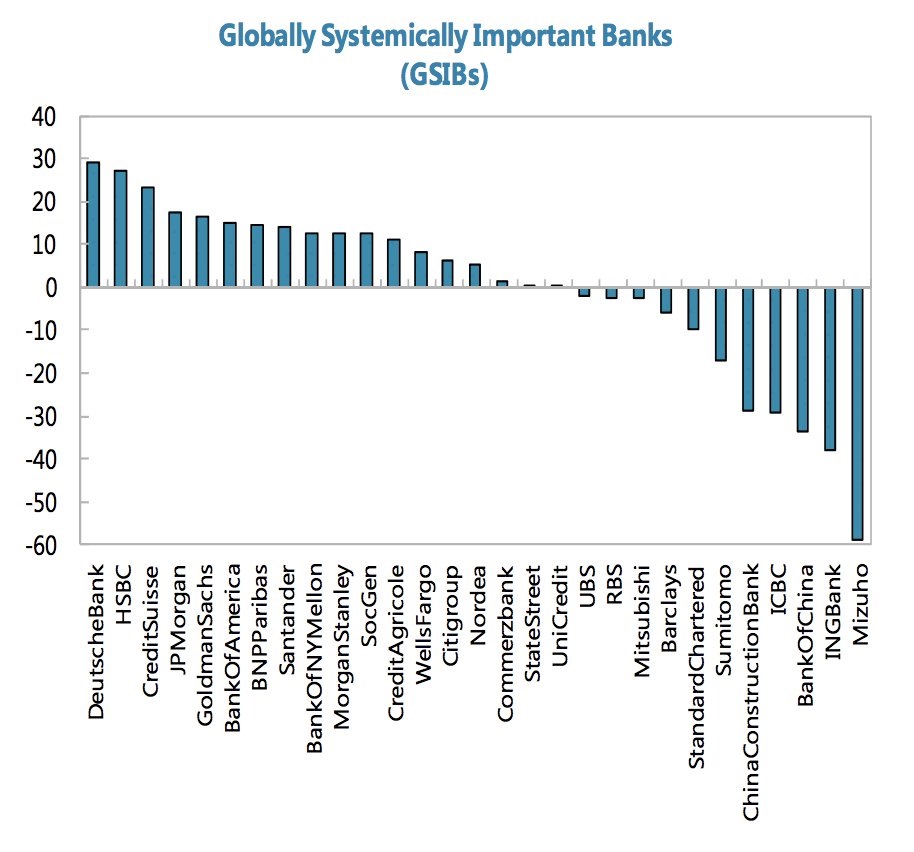

Globally Systemically Important Banks

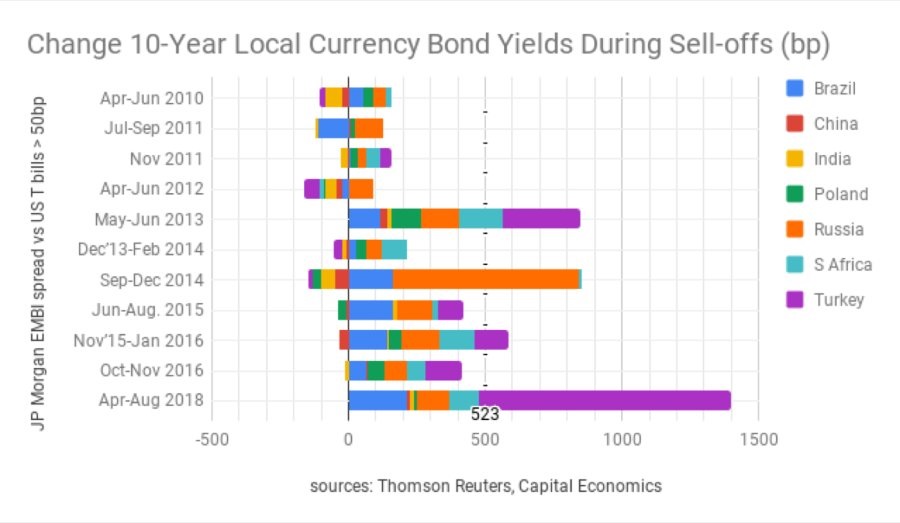

Selected EM Debt Implosions – Last decade

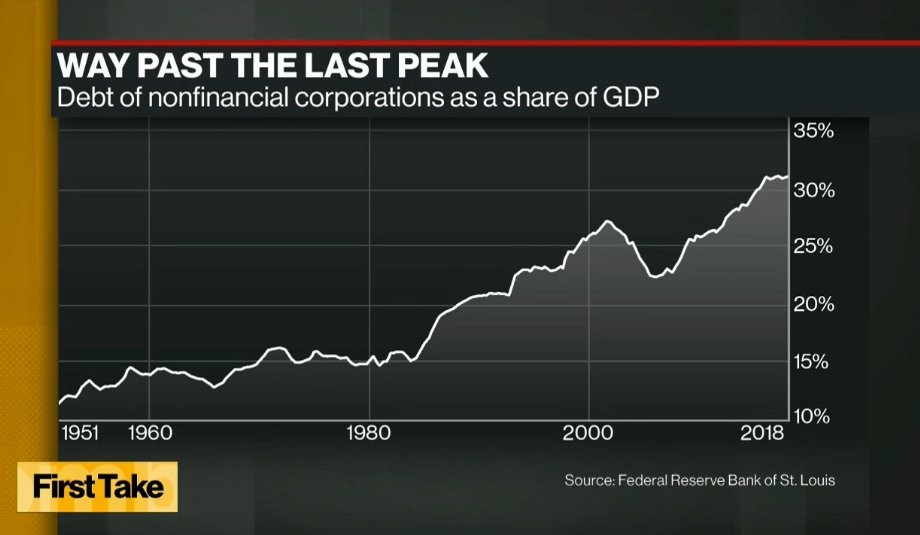

US Non Financial Corporate Debt to GDP

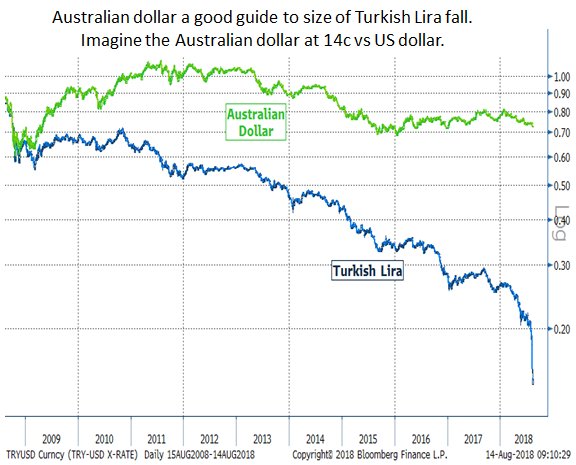

Australian Dollar & Turkish Lira – the last 10 years

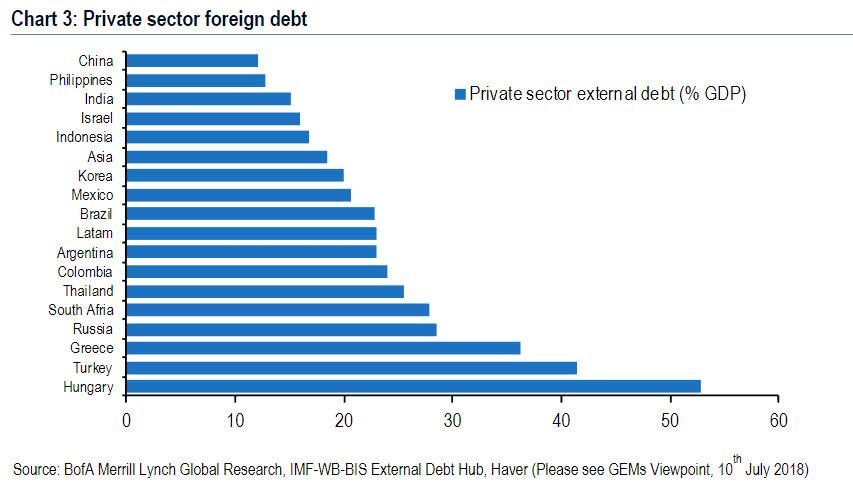

Selected EM Private Foreign Debt

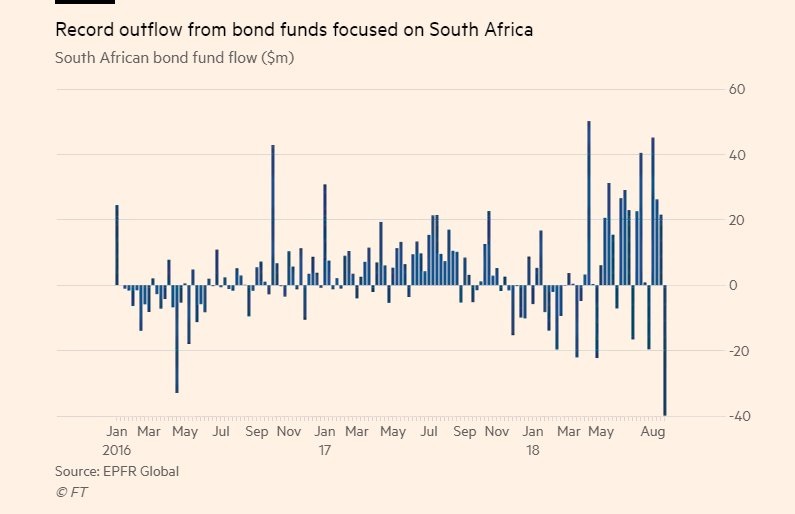

South Africa – Fund Flows

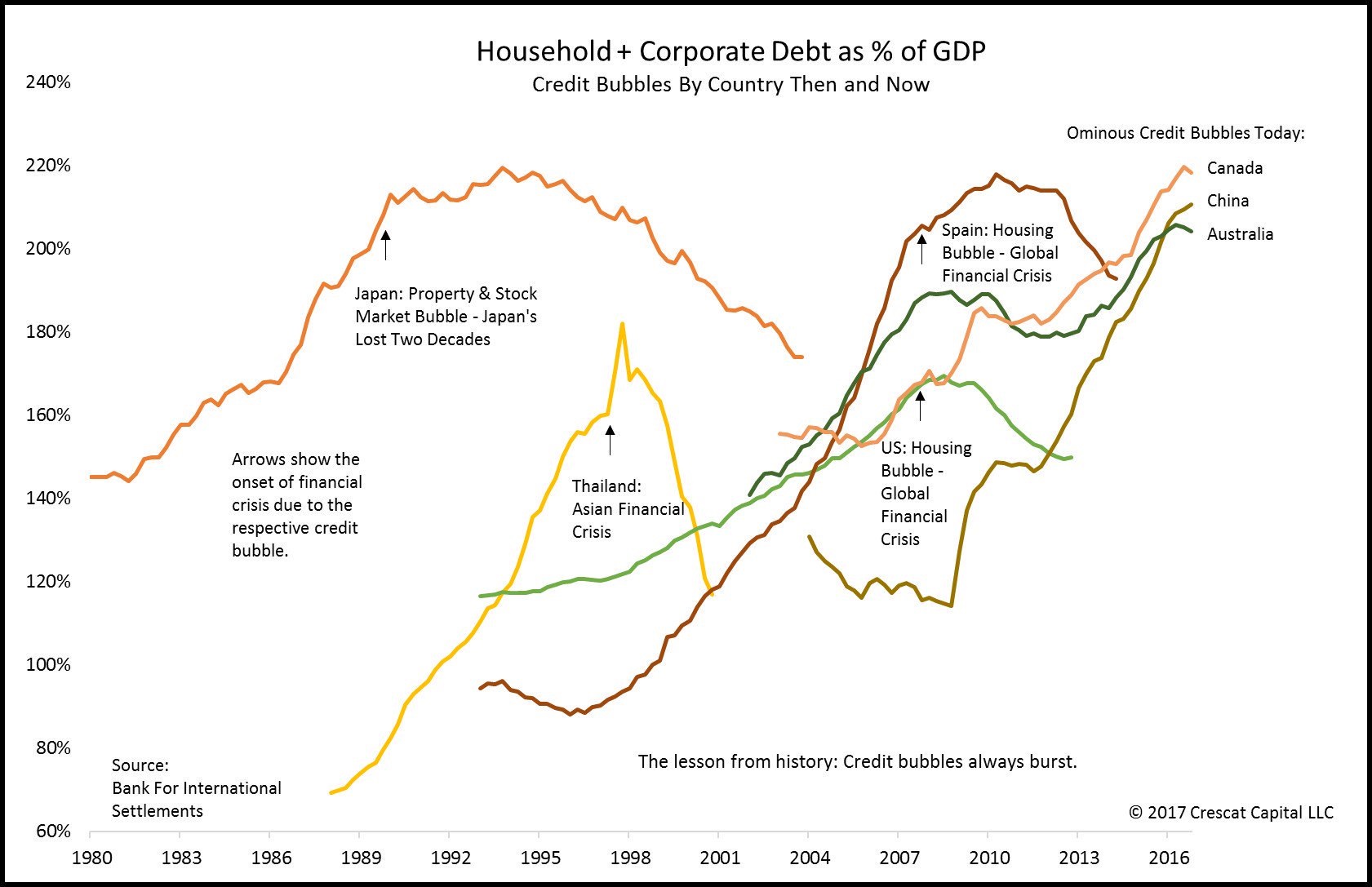

Household & Corporate Debt to GDP – The Greatest Bubbles

Japan & US Yields

UST Spreads

Global Macro

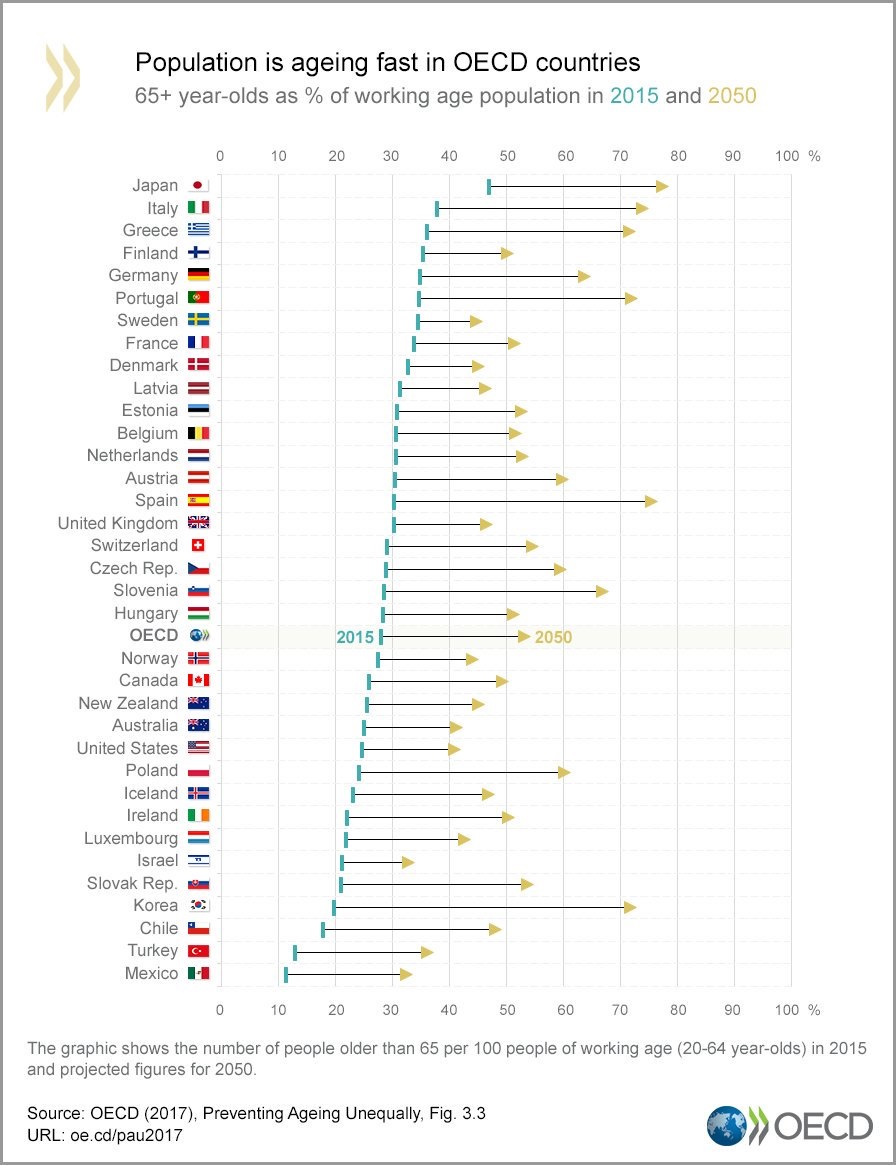

OECD – Ageing

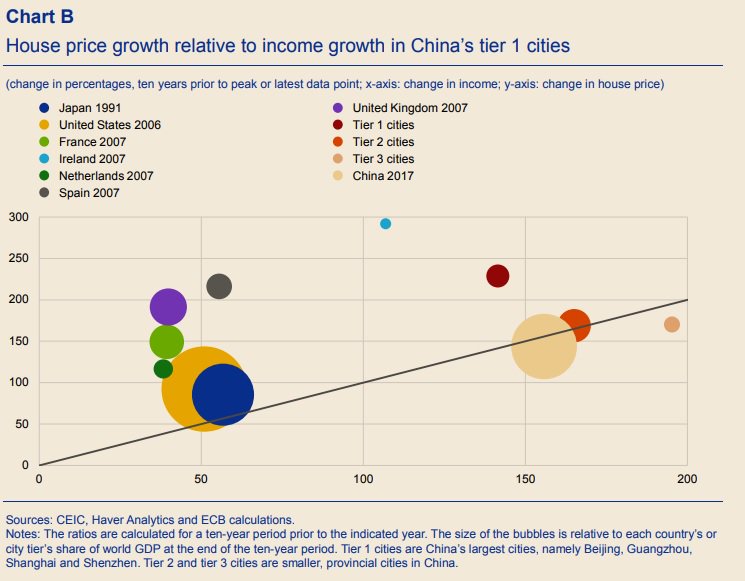

Housing Bubbles – China v Selected Historical International Bubbles

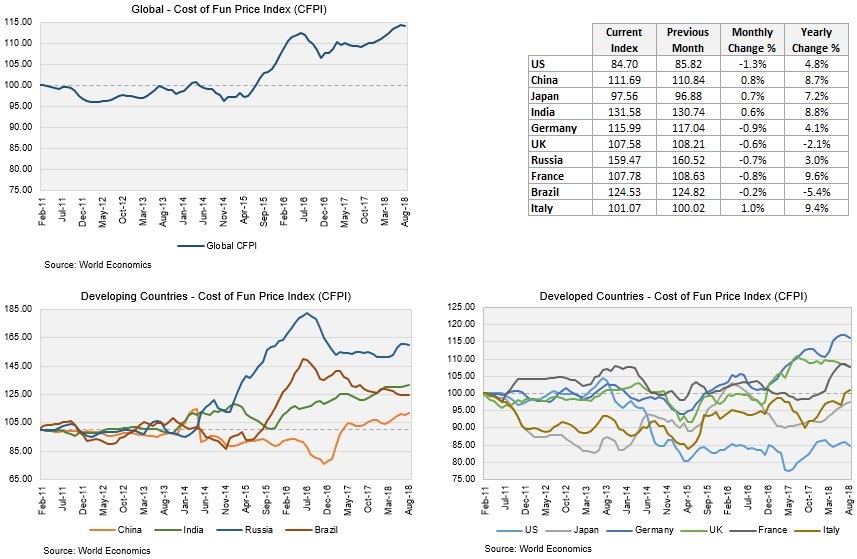

Cost of Fun – Global Comparison

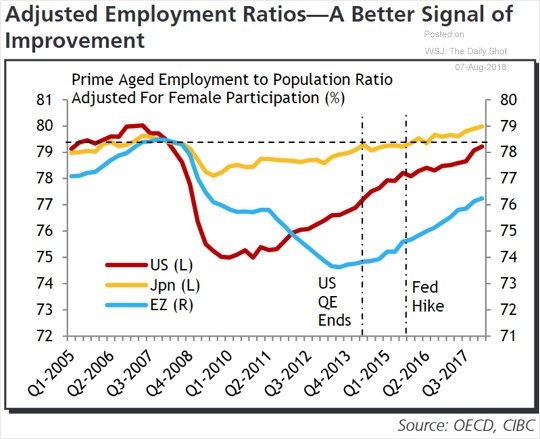

Prime Age Employment Ratios – Major Economies

Emerging Markets & Metals

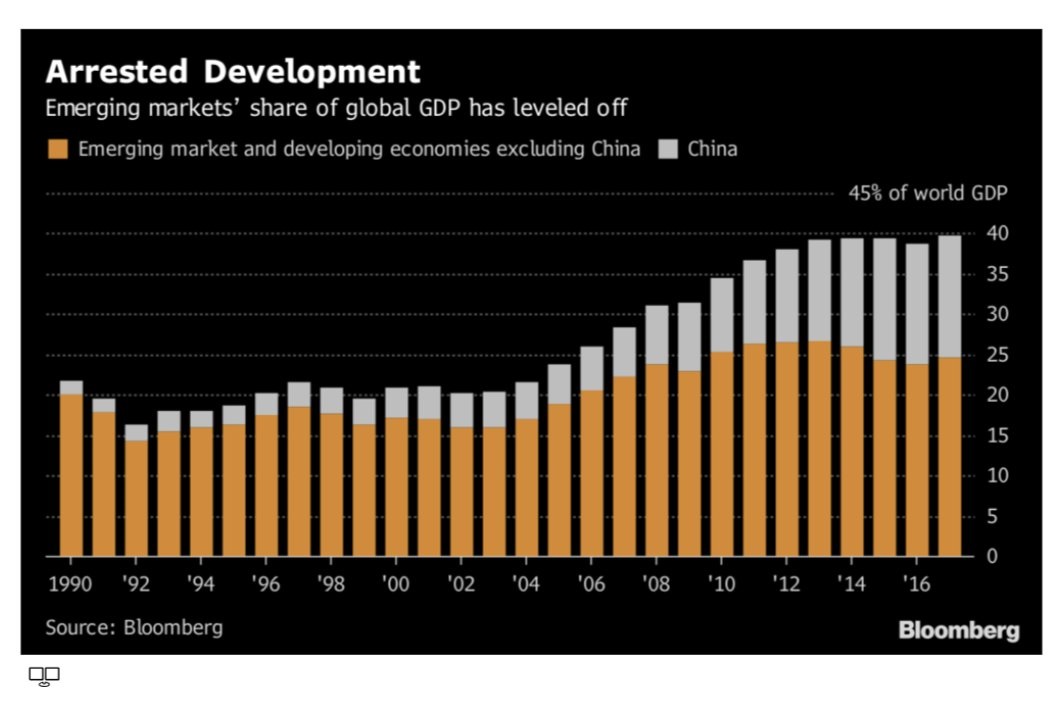

Emerging Markets & Global GDP

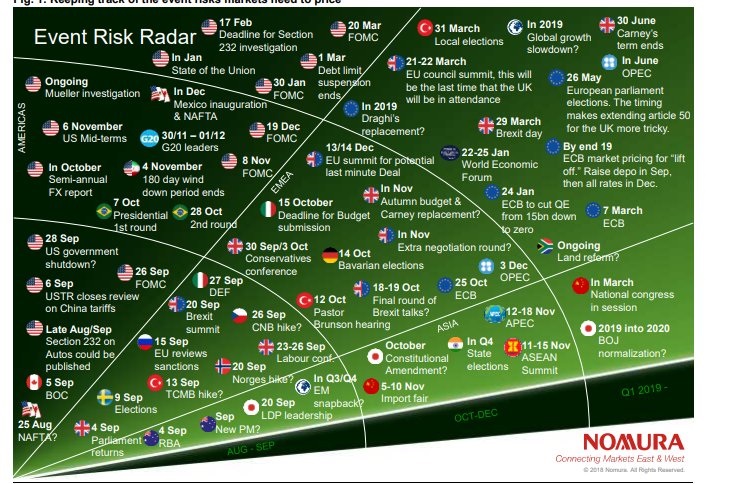

Event Risk radar – Next 6 Months

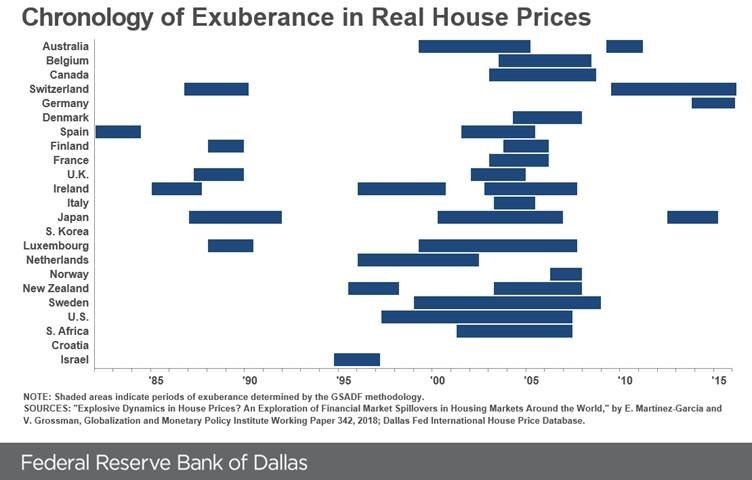

House Price Exuberance – Global Comparison (……..and I don’t think they have Australia right)

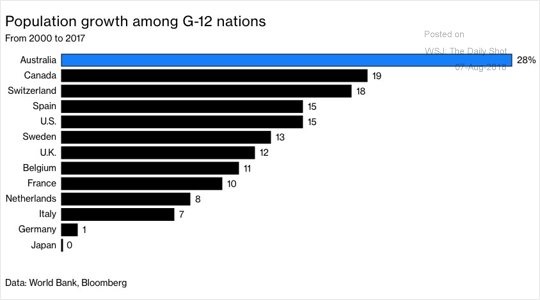

G12 Population Growth

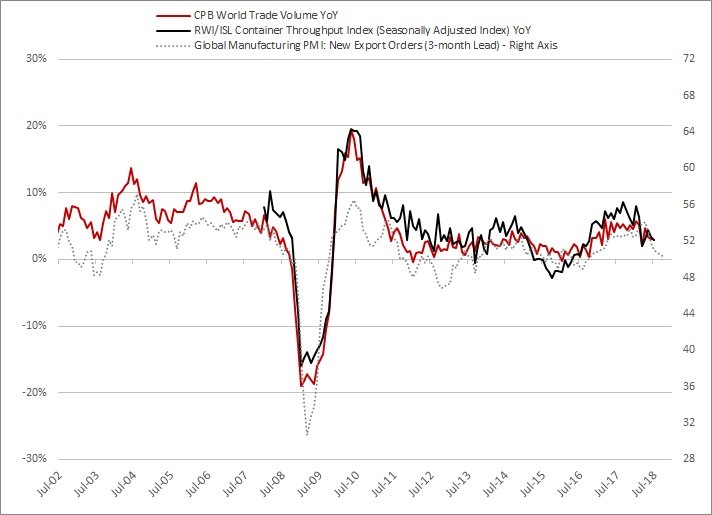

Global Trade

Global Property & GDP

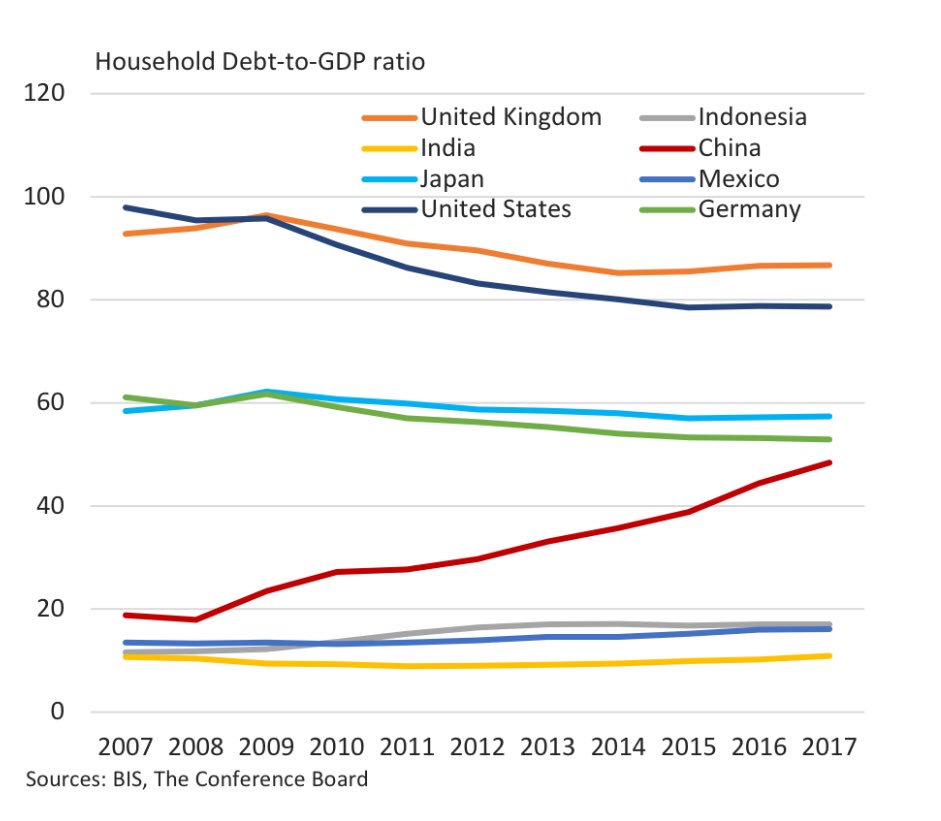

Household Debt to GDP – Selected International

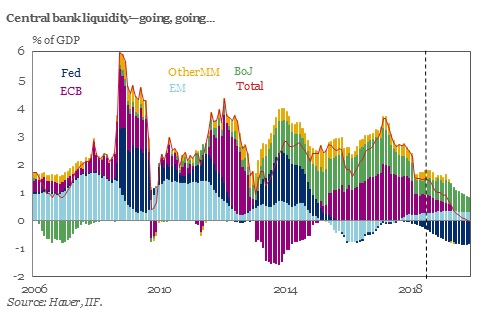

Central Bank Liquidity

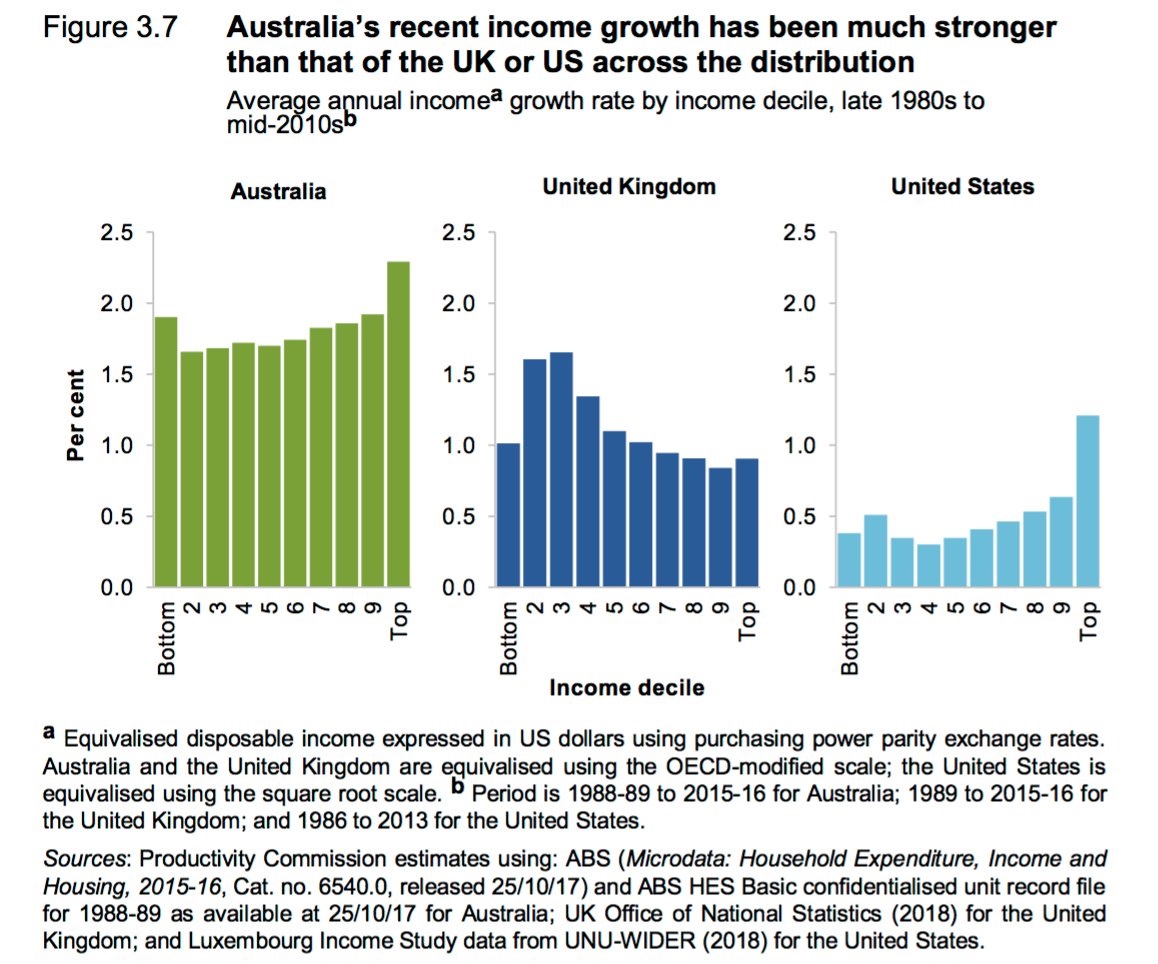

United States, United Kingdom, Australia – Income Growth

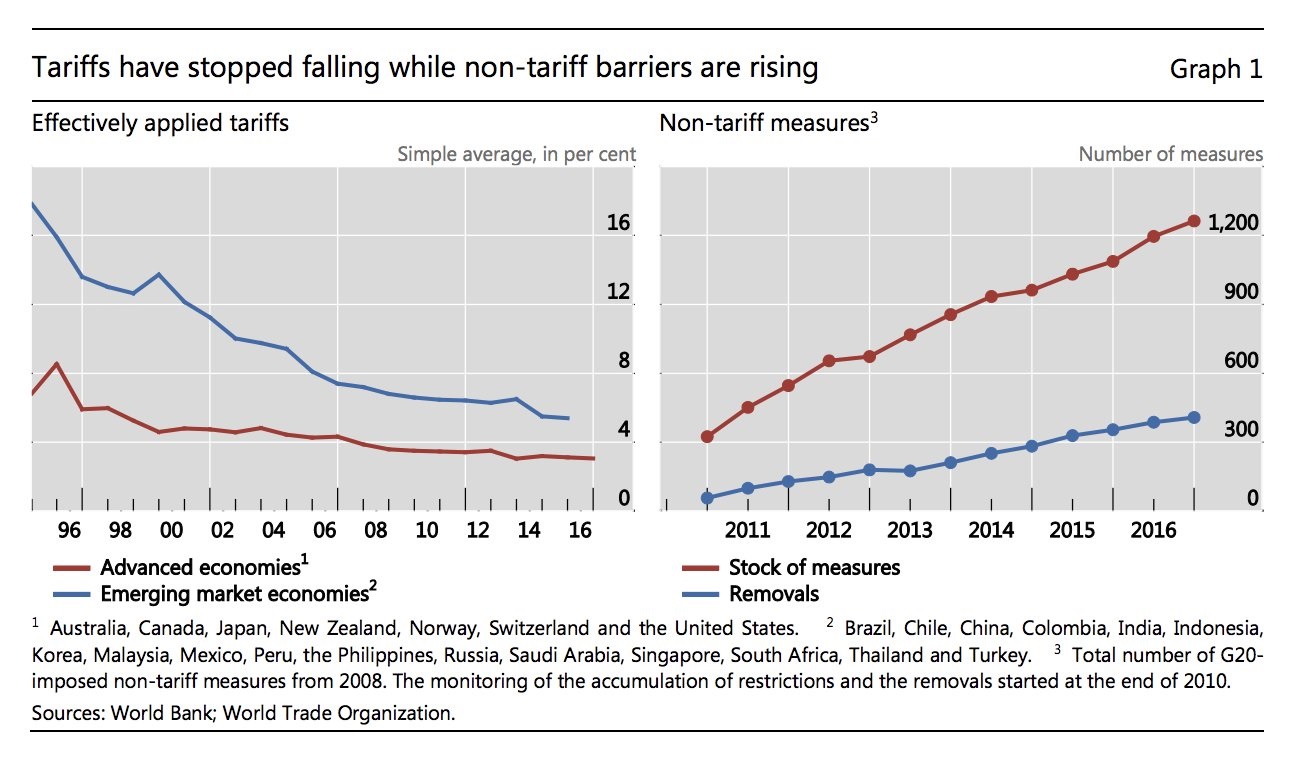

Global Tariffs

…and furthermore…

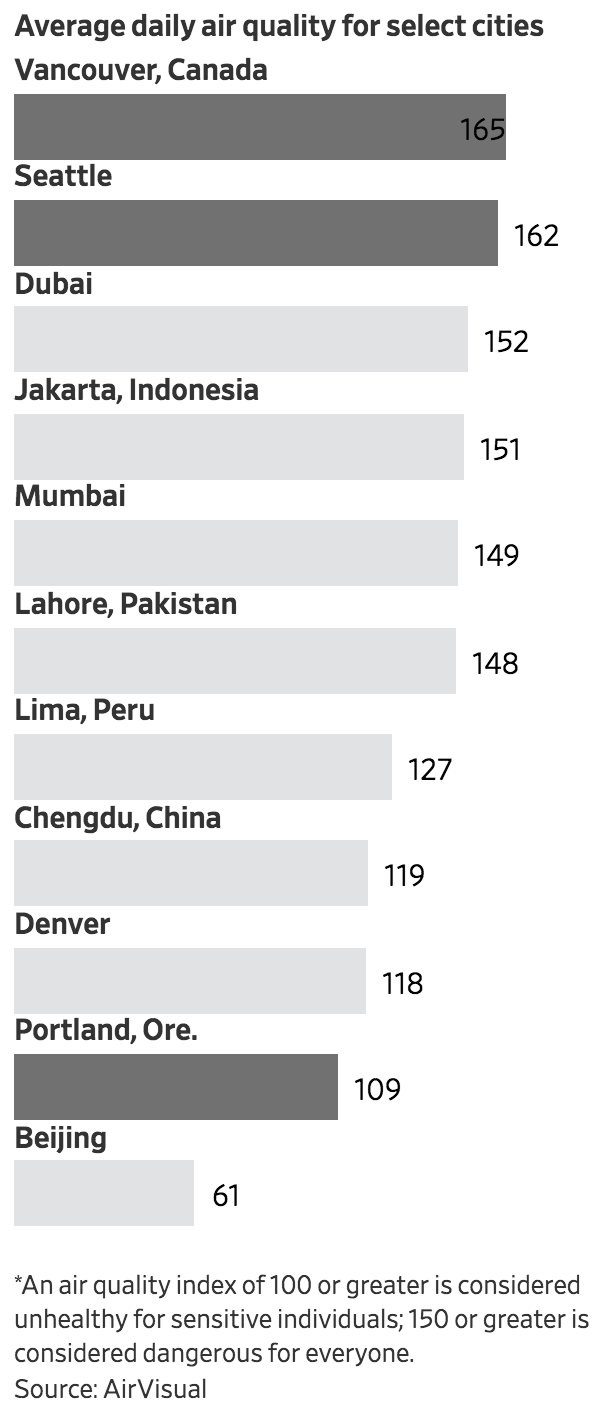

Average Air Quality – Selected Cities

Average paper Length in Major Economics Journals

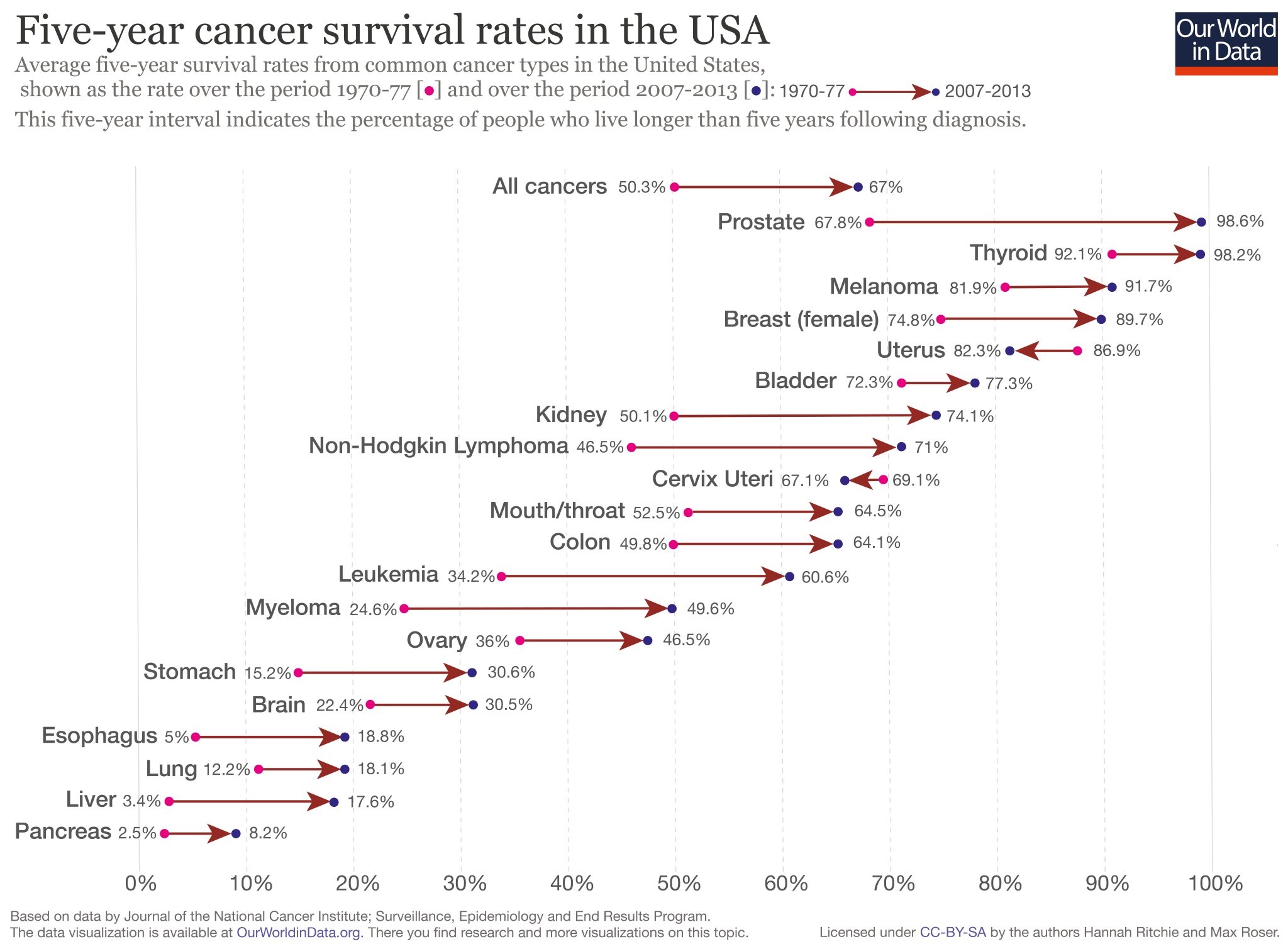

Five Year Cancer Survival Rates – United States

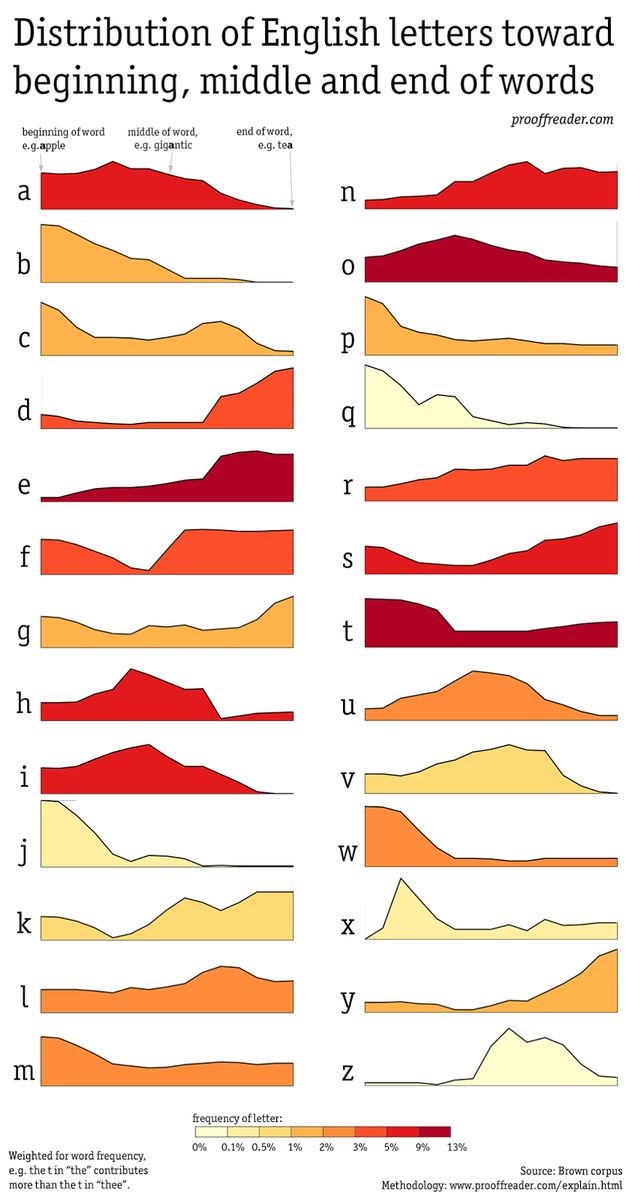

Letter Distribution in Words – English

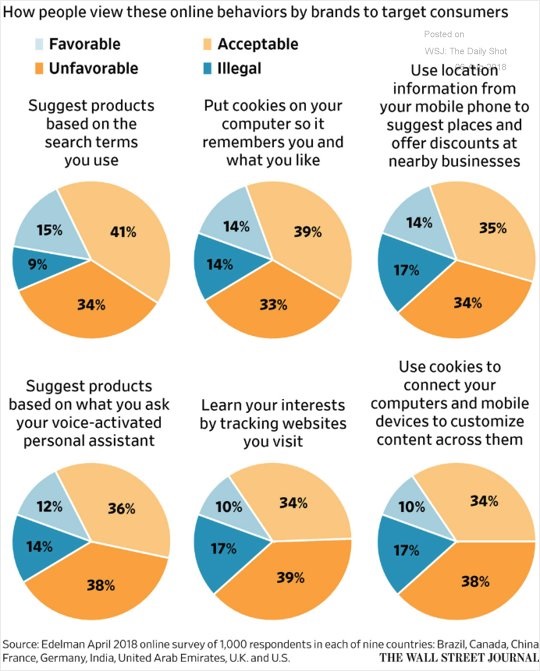

Thoughts About Cookies

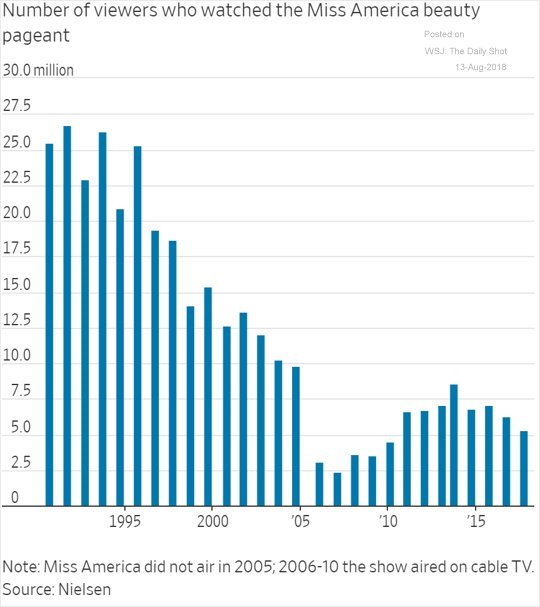

Miss America Beauty Pageant Viewers

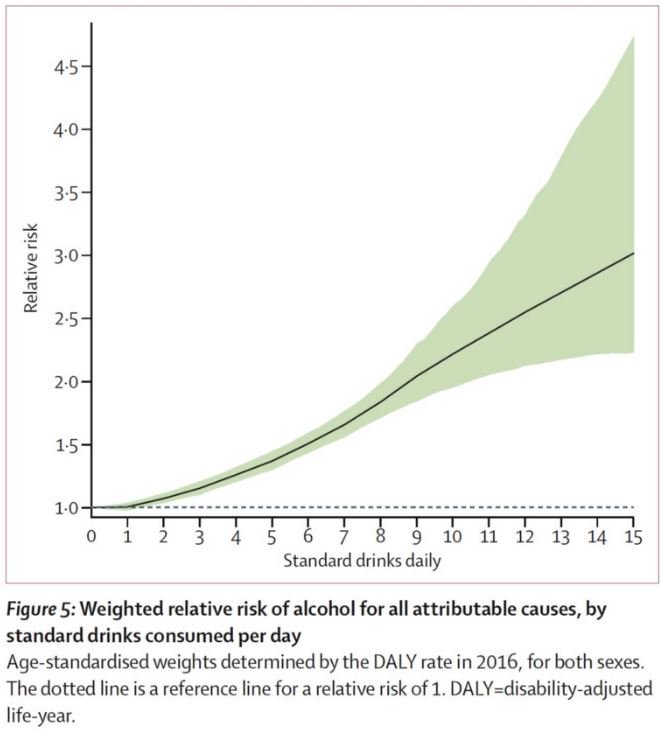

The Risks of Alcohol

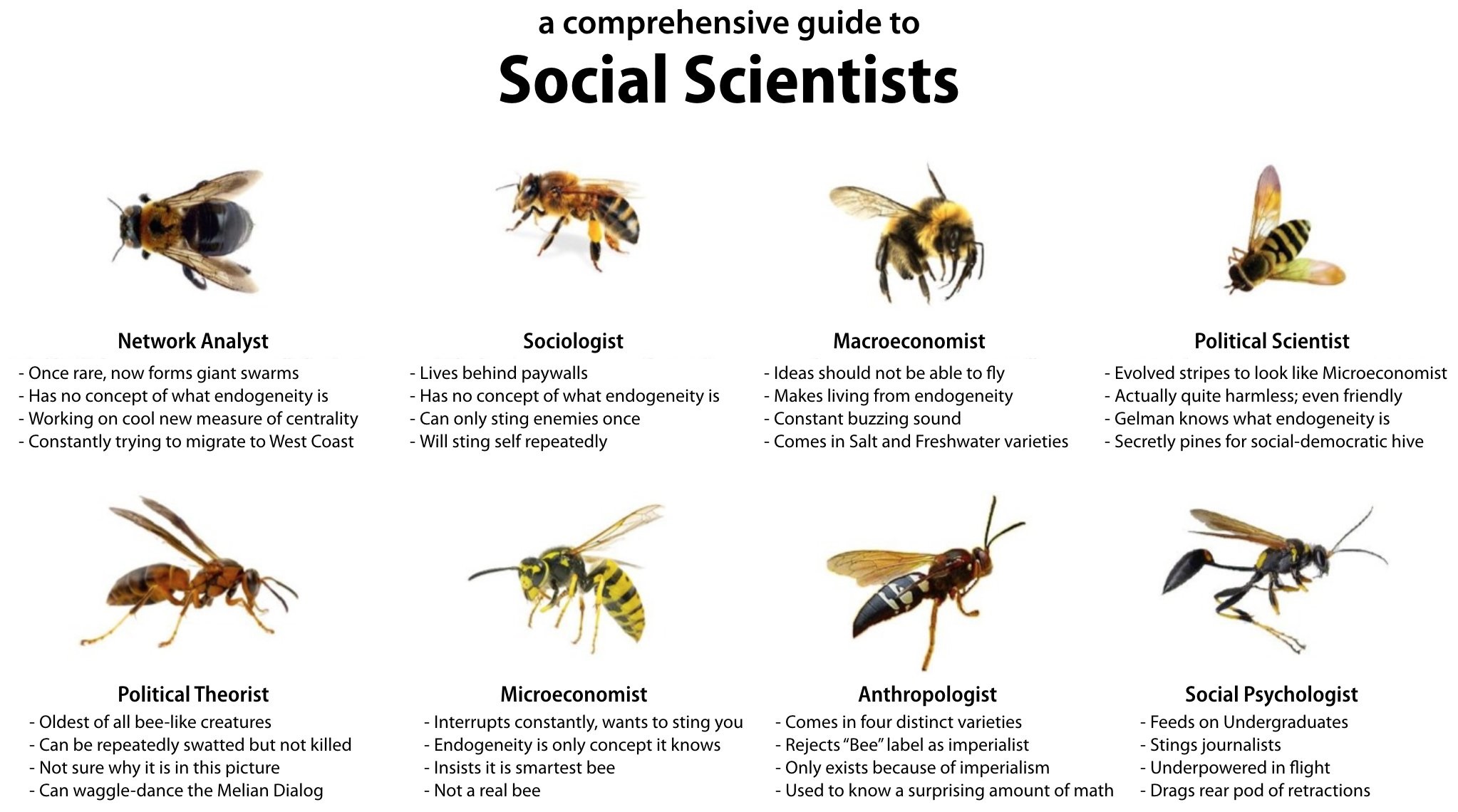

Social Science Types

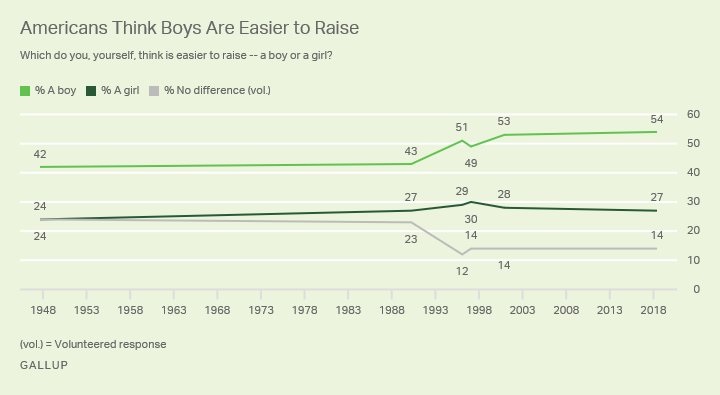

Americans and Easier to Raise

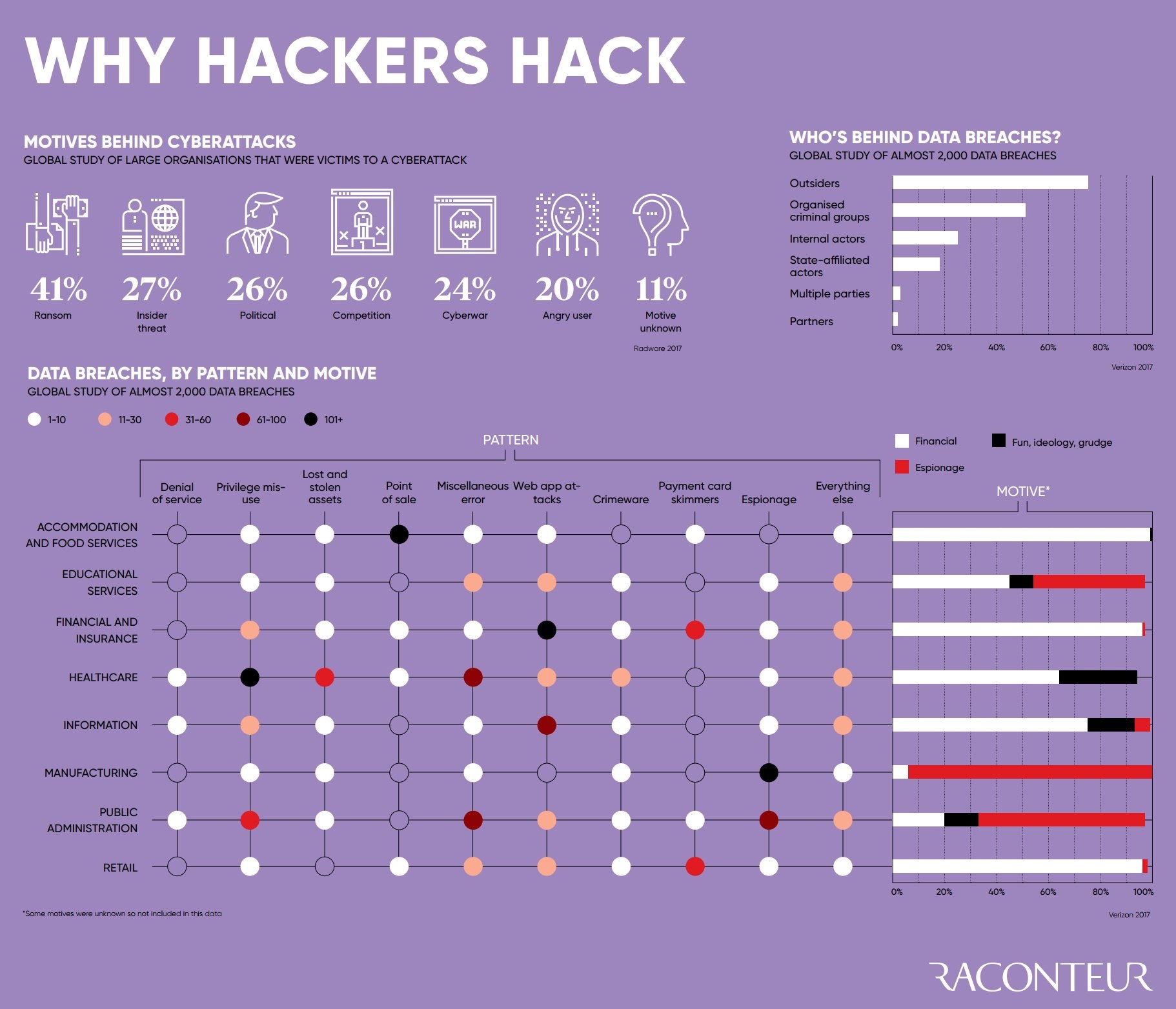

Why Hackers Hack

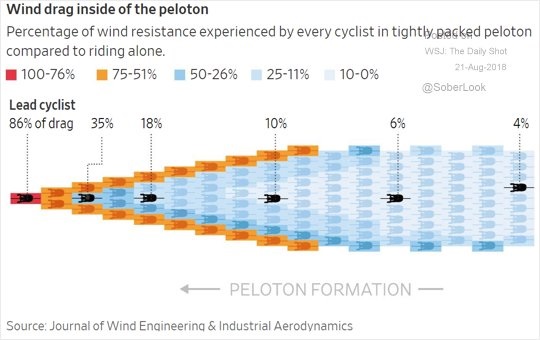

The Peleton and its Effect