Australasia

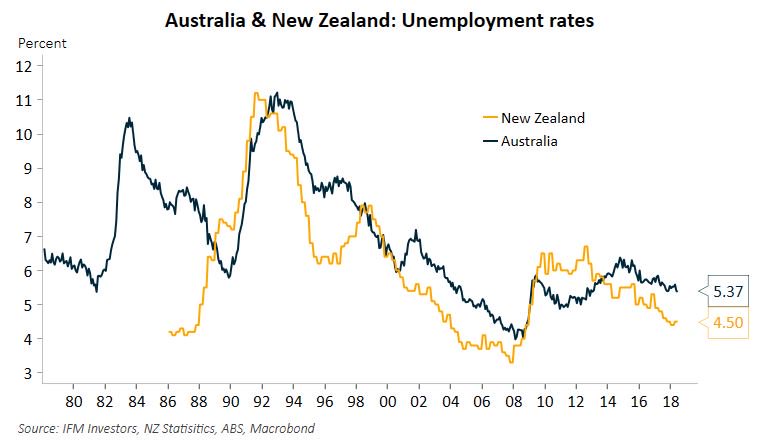

Australia & New Zealand – Unemployment

Australia & New Zealand – Participation

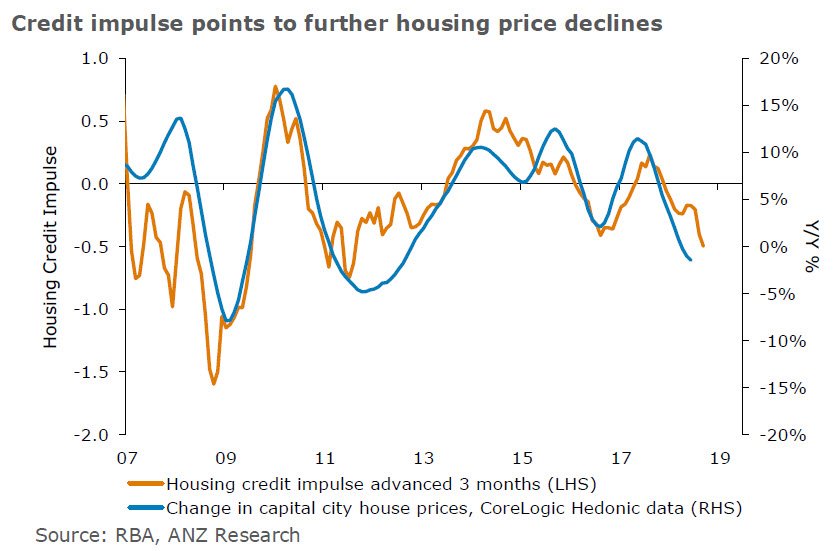

Australia – Housing Credit & House Prices

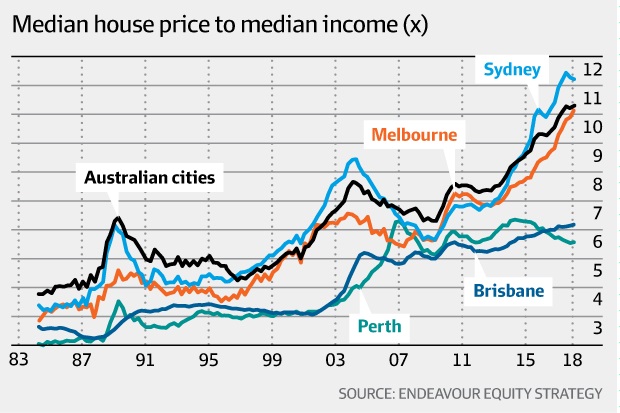

Australia – House Prices to Median Income

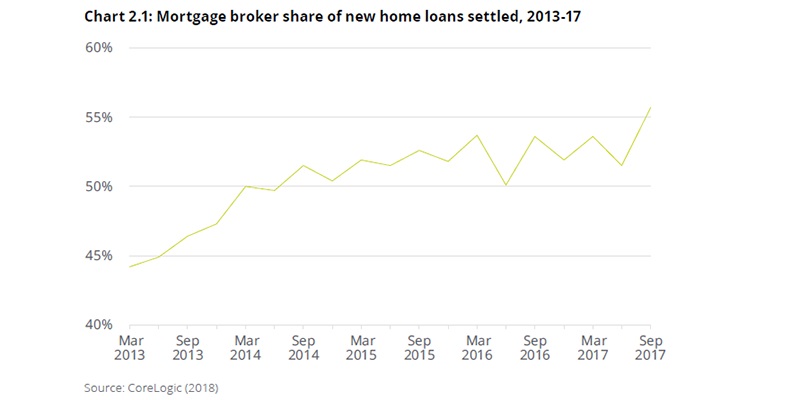

Australia – Mortgage broker Share of New Home Loans to 3Q 2017

Australia & Germany – Household Debt to House Prices

Australia – Merchandise Exports by Destination

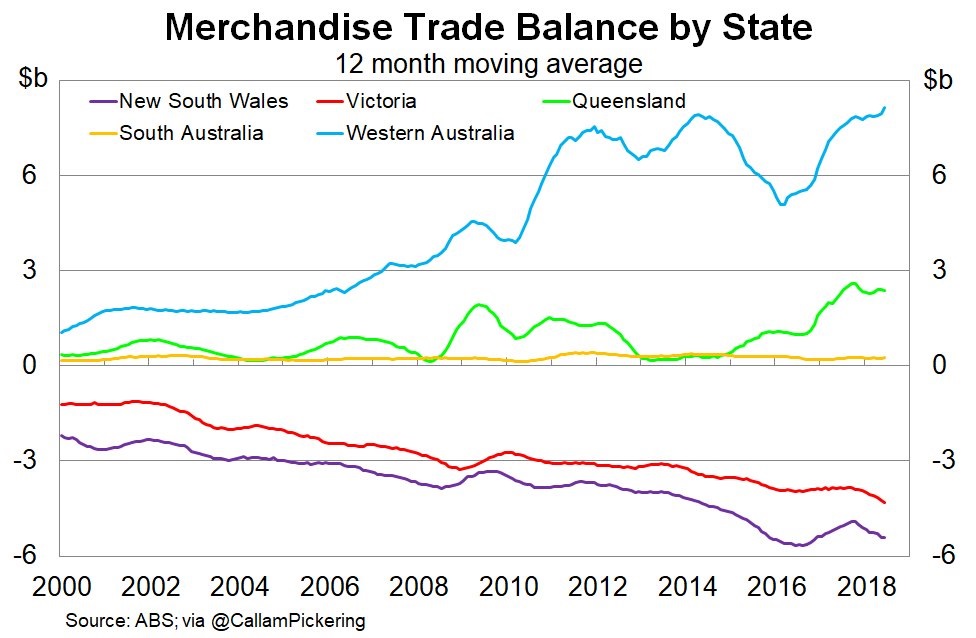

Australia – Merchandise Trade Balance by State

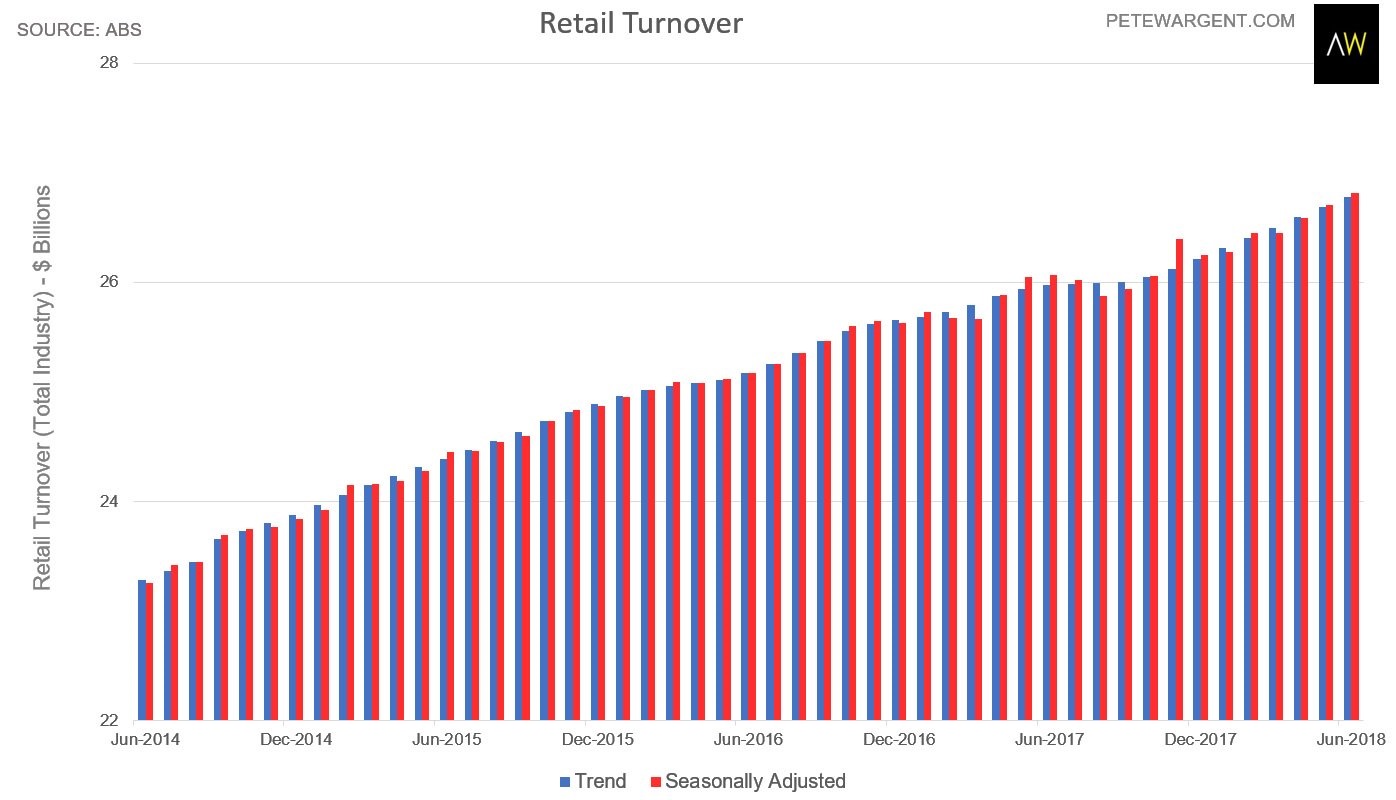

Australia – Retail Turnover

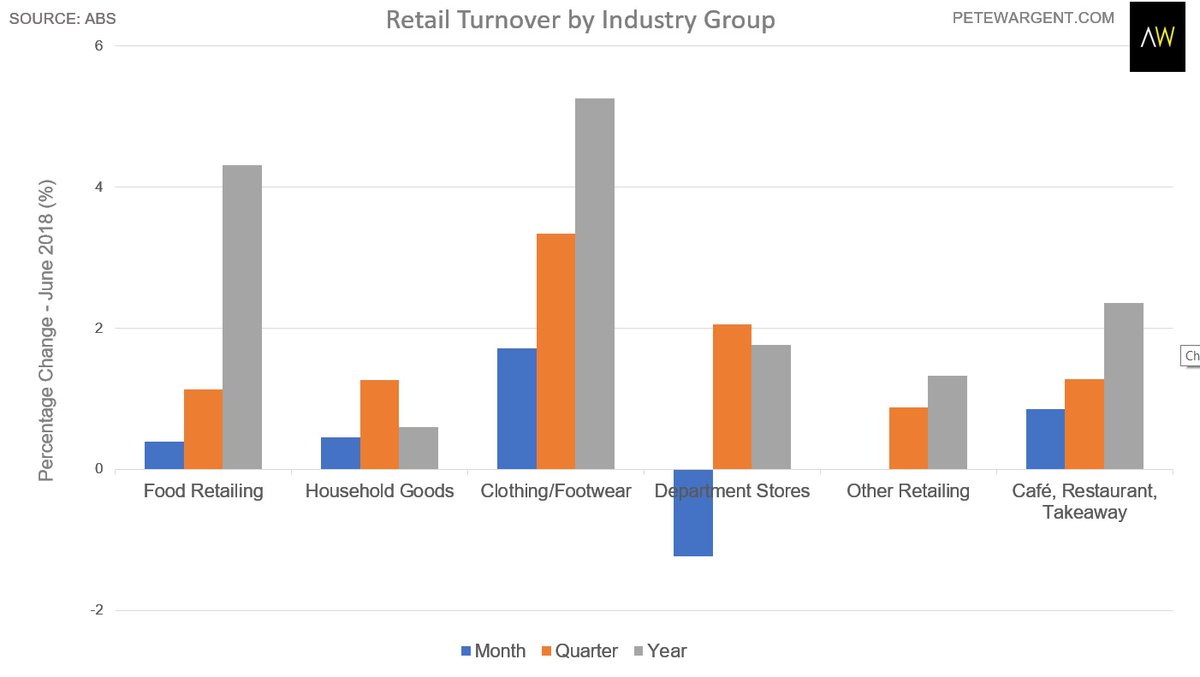

Australia – Retail Turnover by Sector

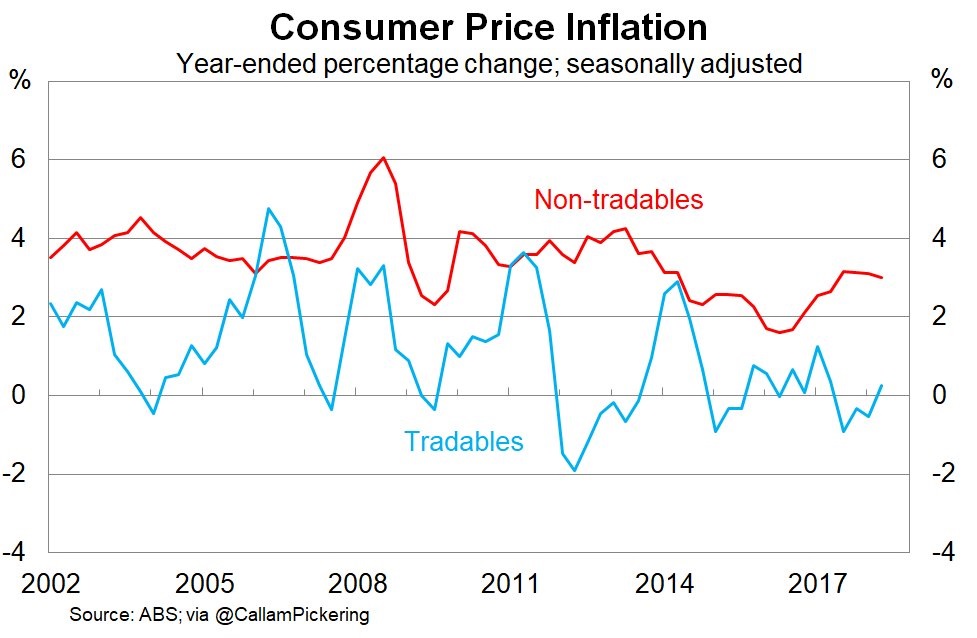

Australia – Tradable and Non – Tradable Inflation

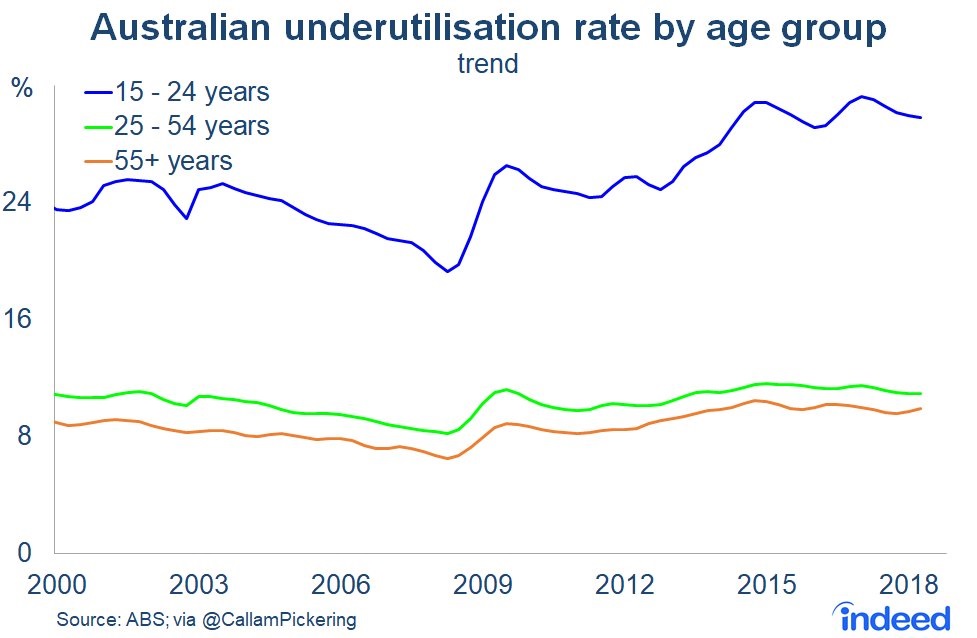

Australia – Underutilisation by Age group

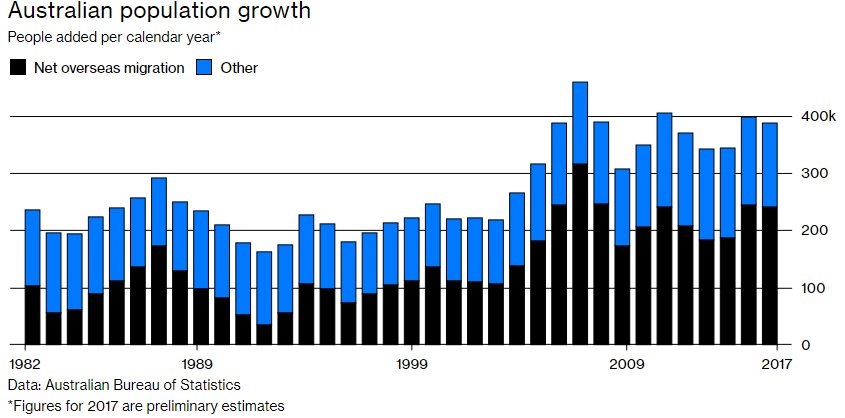

Australia – Population Growth

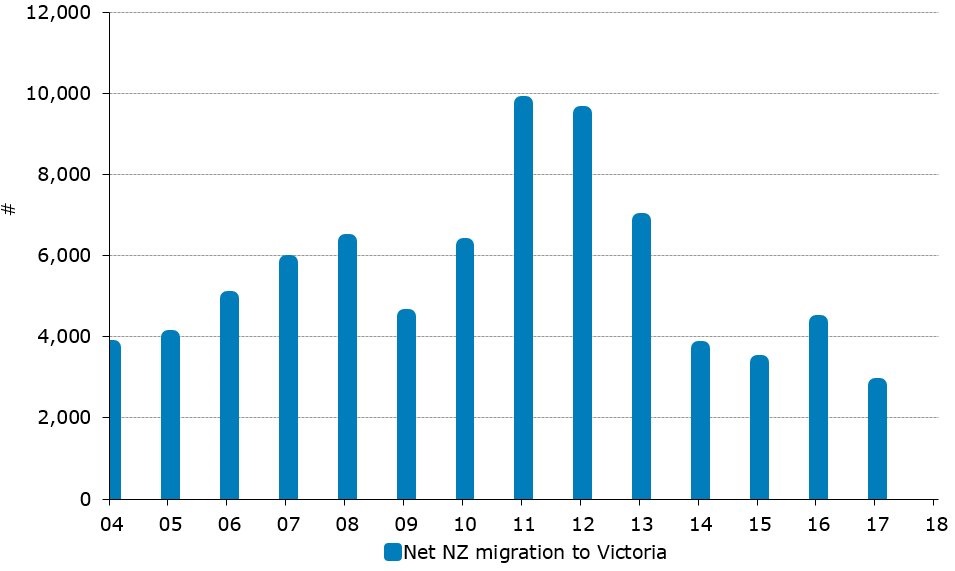

New Zealand Migration to Victoria

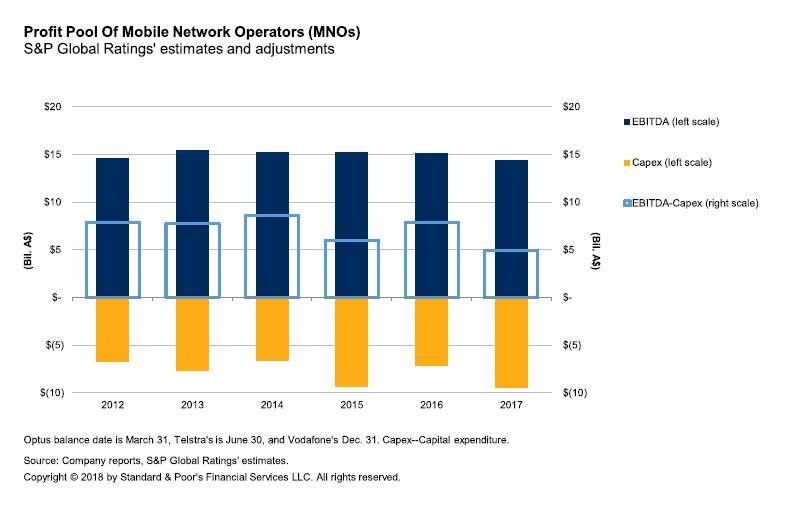

Australian Mobile Operators – EBITDA & Capex

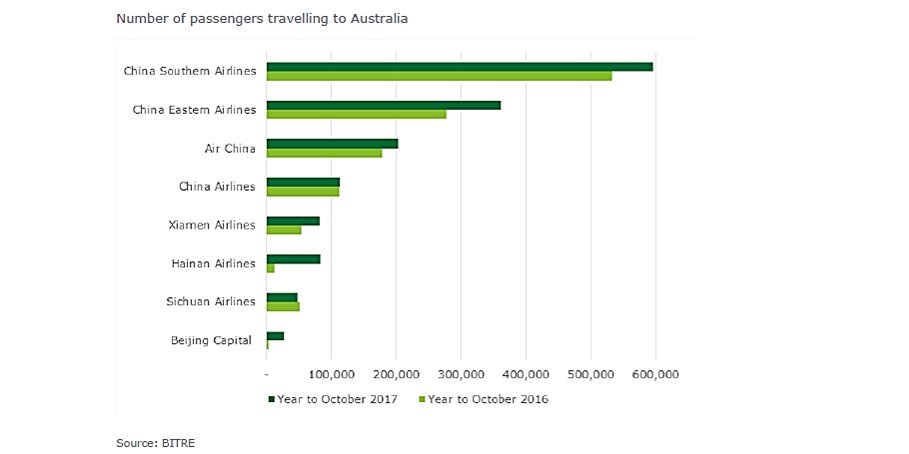

Chinese Airlines – Flights to Australia

United States – Americas

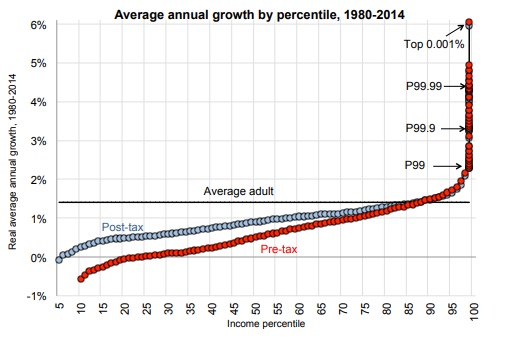

United States – Average Income Growth by Percentile between 1980 & 2014

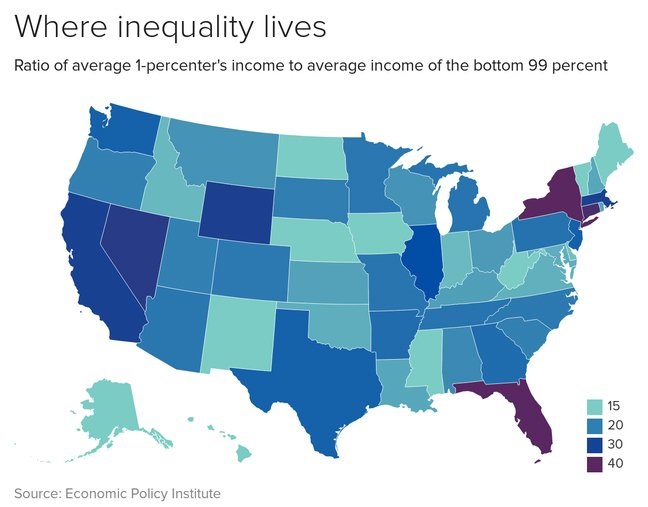

United States – Inequality by State

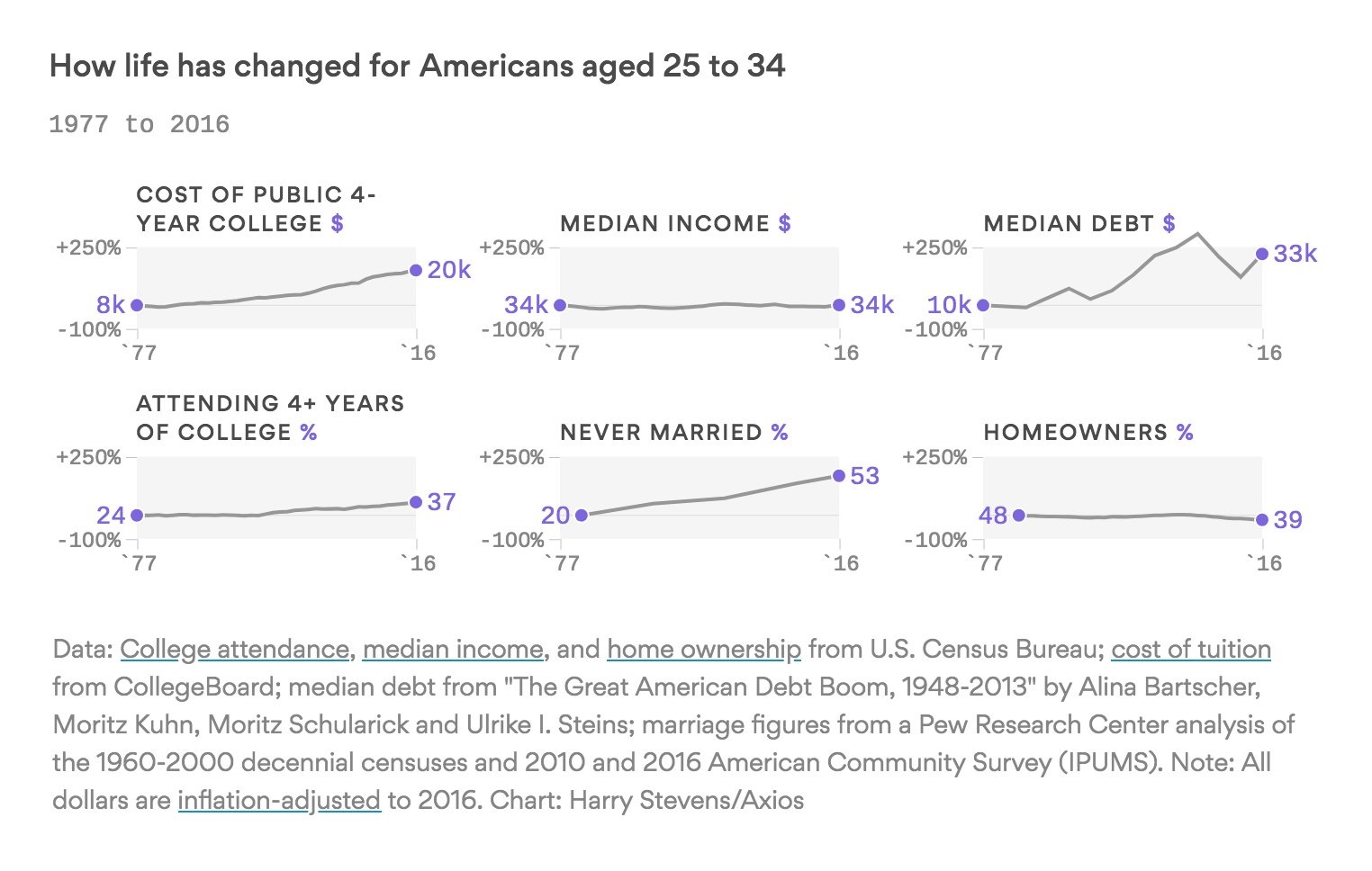

United States – Life Changes for 25-34 Year Old Americans between 1977 & 2016

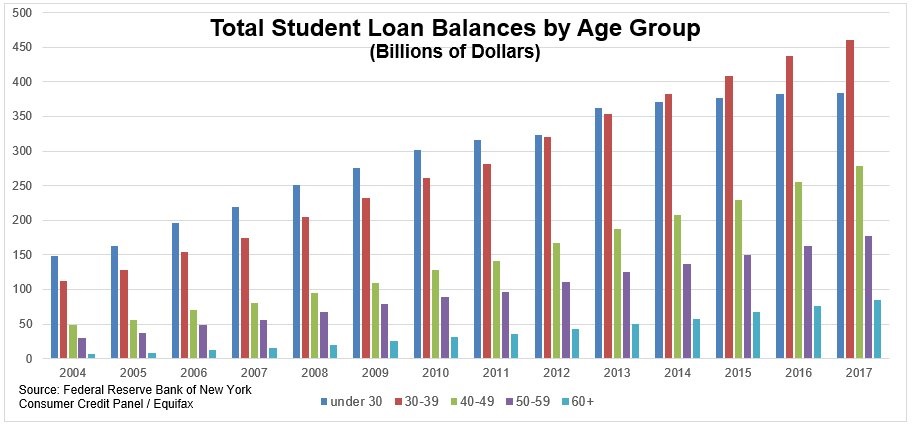

United States – Student Loan Balances by Demographic

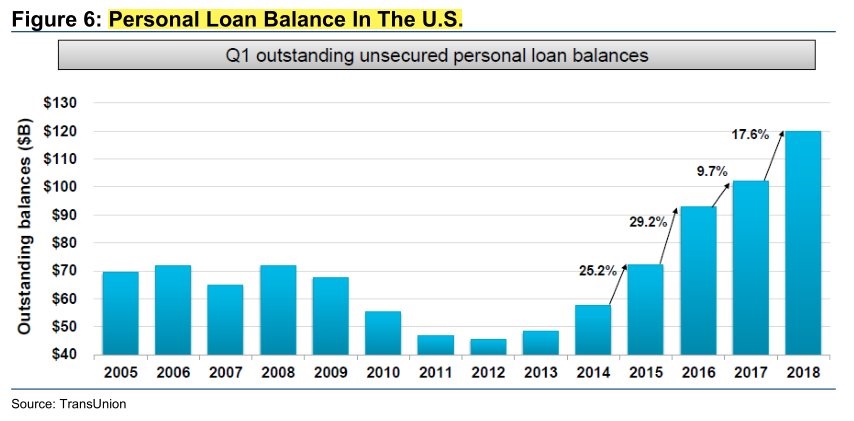

United States – Personal Loans

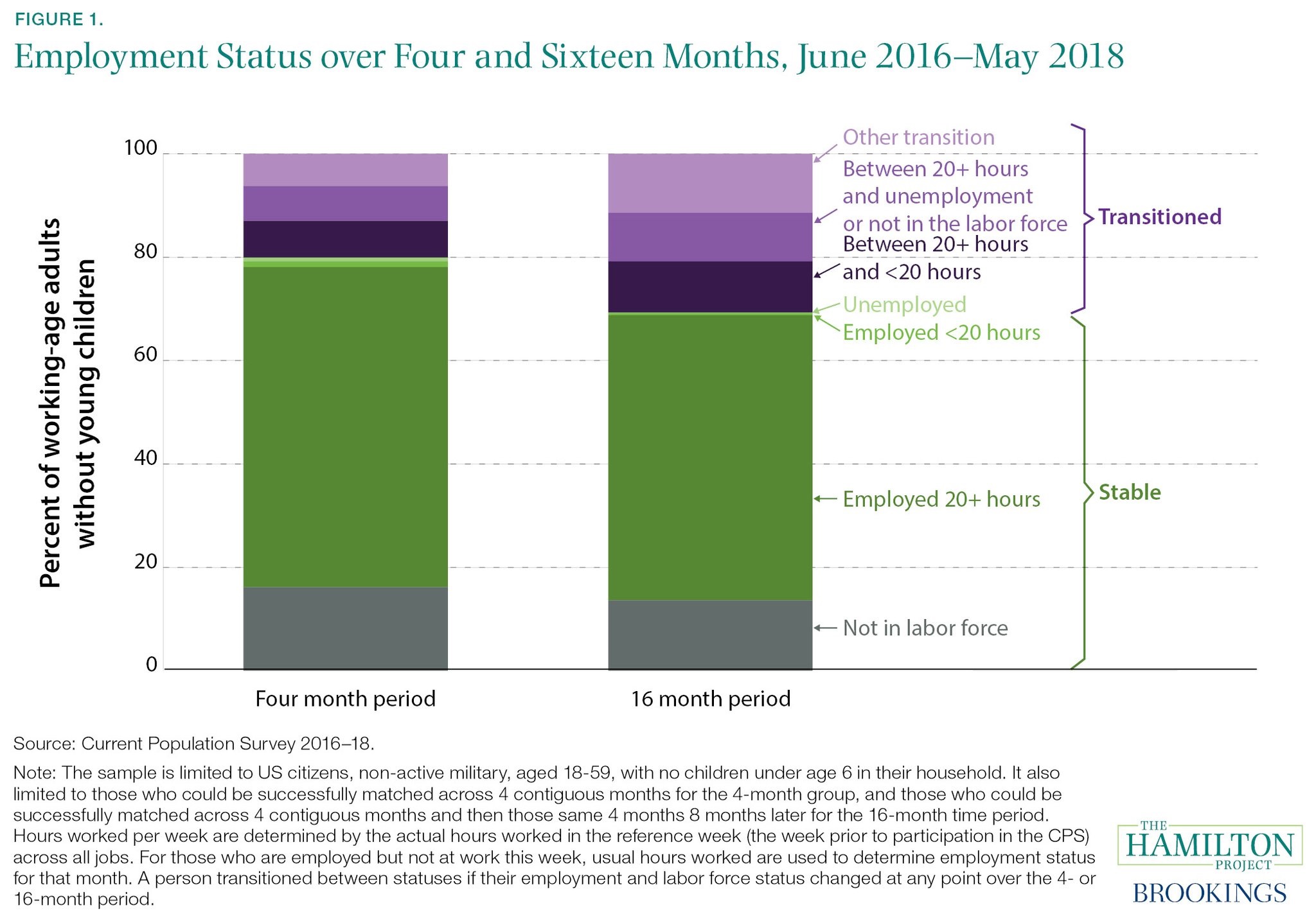

United States – Precarious Employment

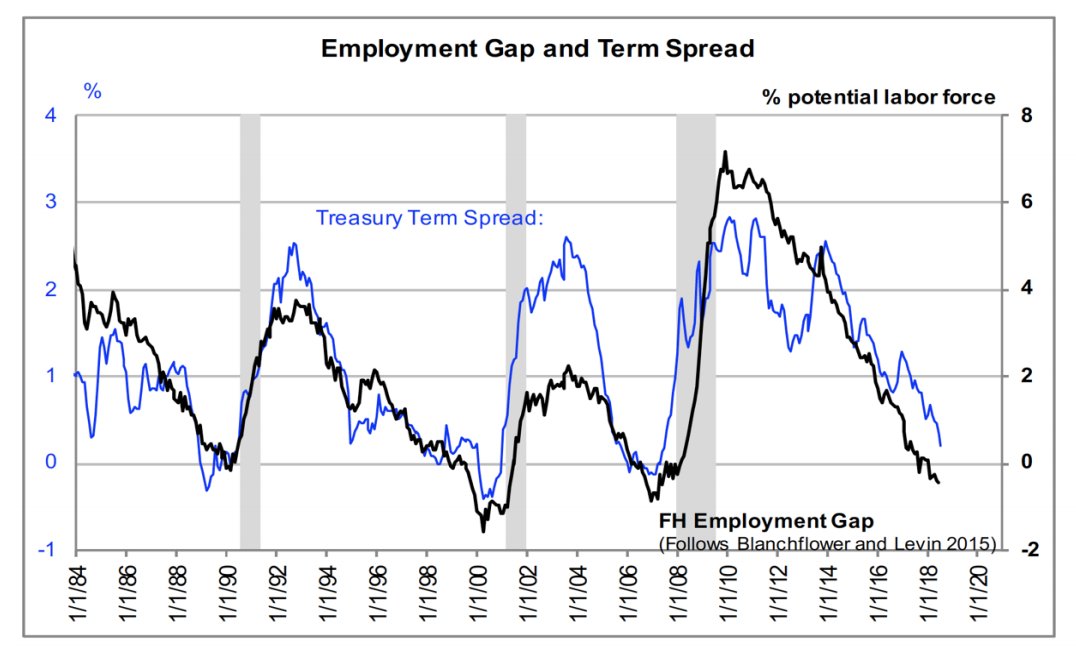

United States – Employment Gap & Term Spread

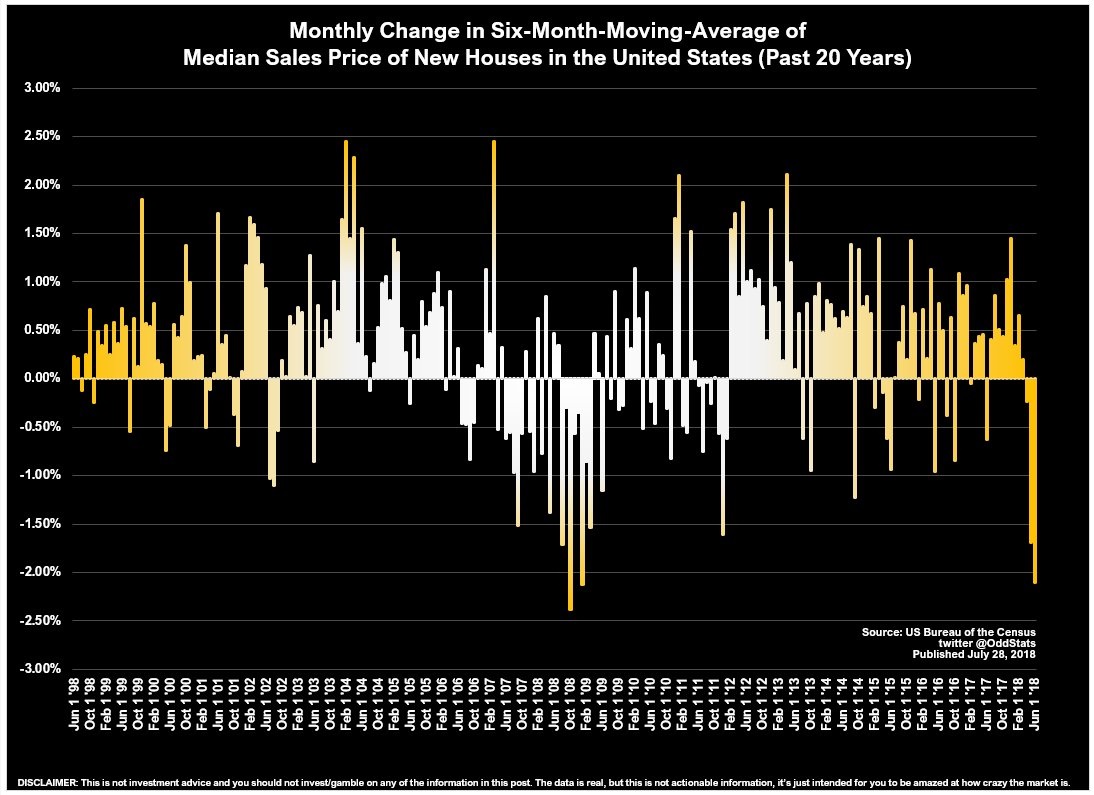

United States – Median Sales price of New Housing (6m moving average)

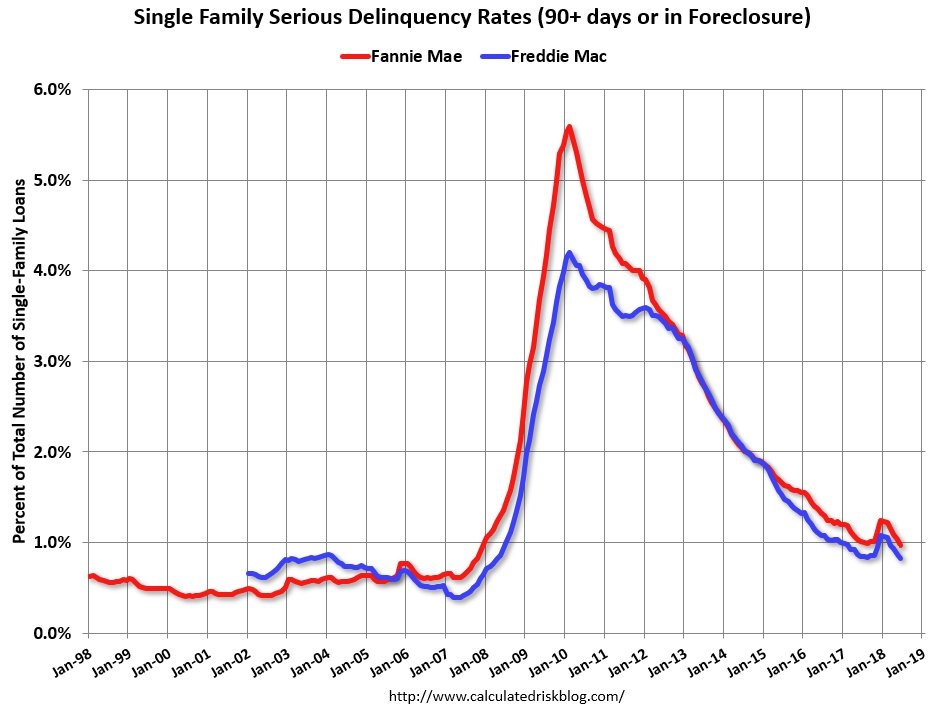

United States – Mortgage Delinquency

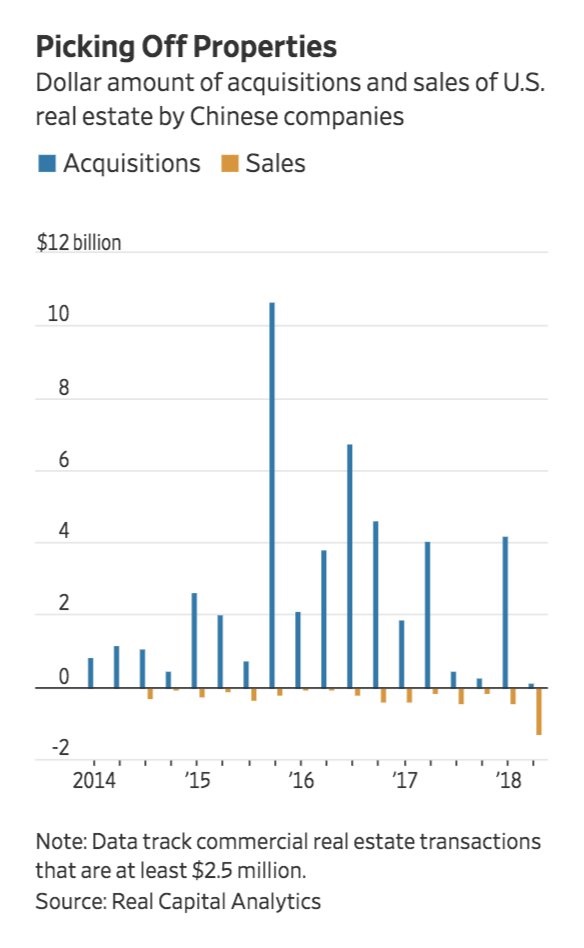

United States – Real Estate Acquisitions & Sales by Chinese companies

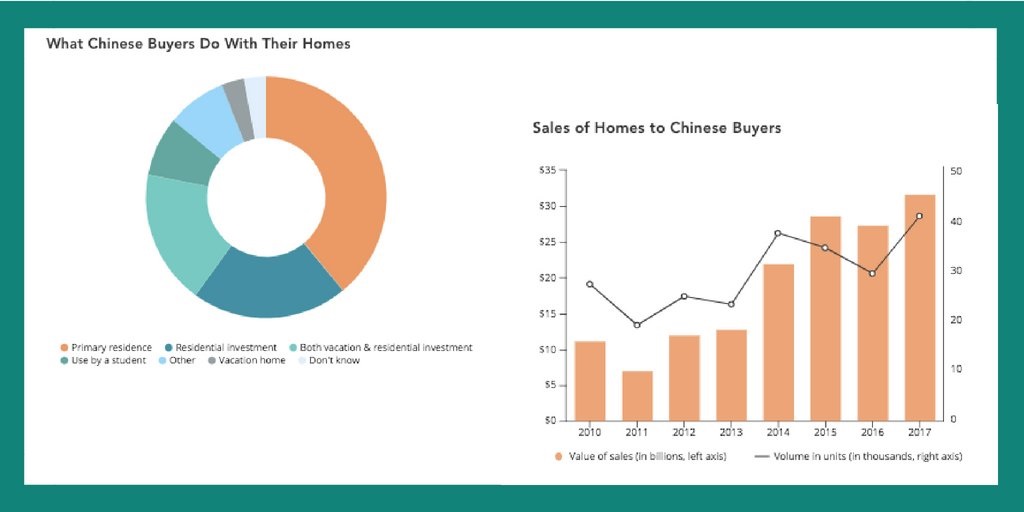

United States – Sales of Homes to Chinese Buyers and Intent of Purchase

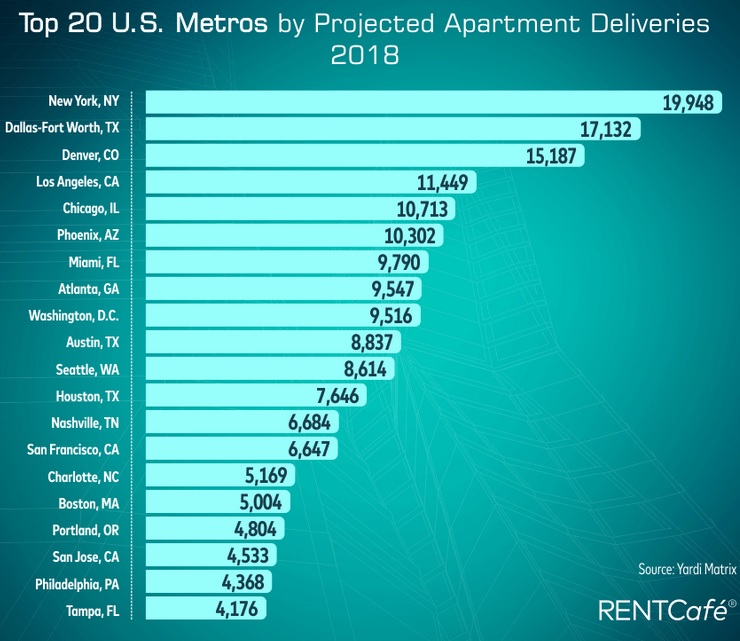

United States – Major Cities & Projected New Apartments 2018

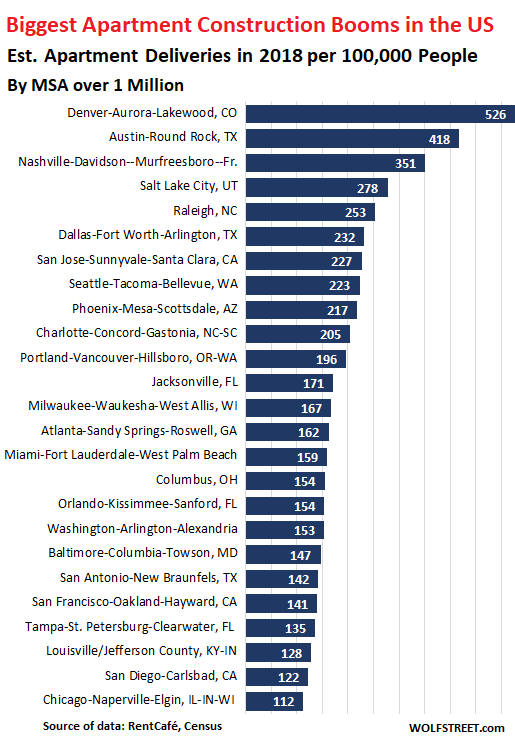

United States – New Apartments in Major Metropolitan Areas

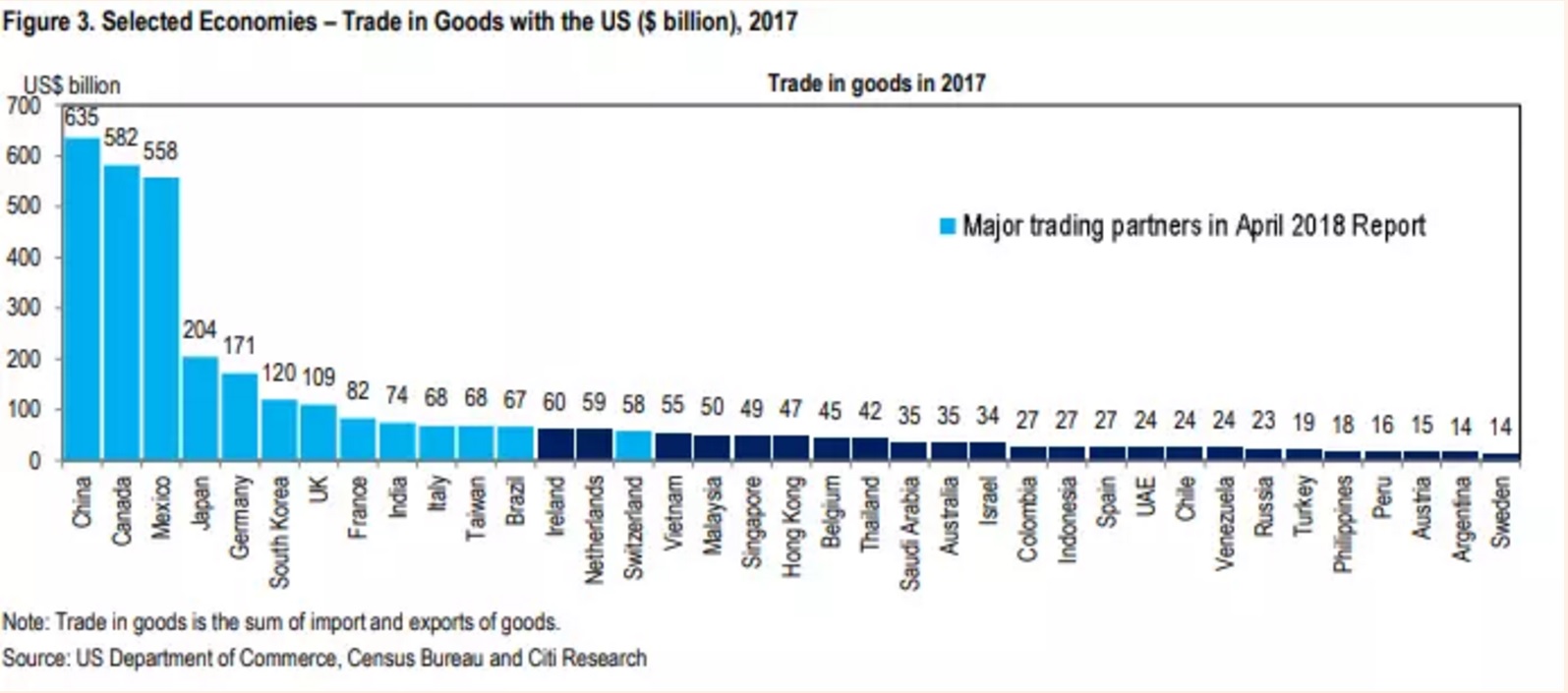

United States – Selected Trade Partners & Goods Balance

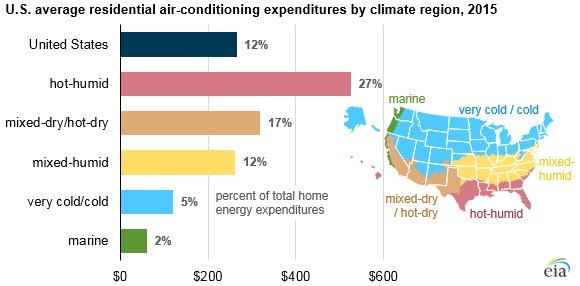

United States – Aircon Expenditure by Region

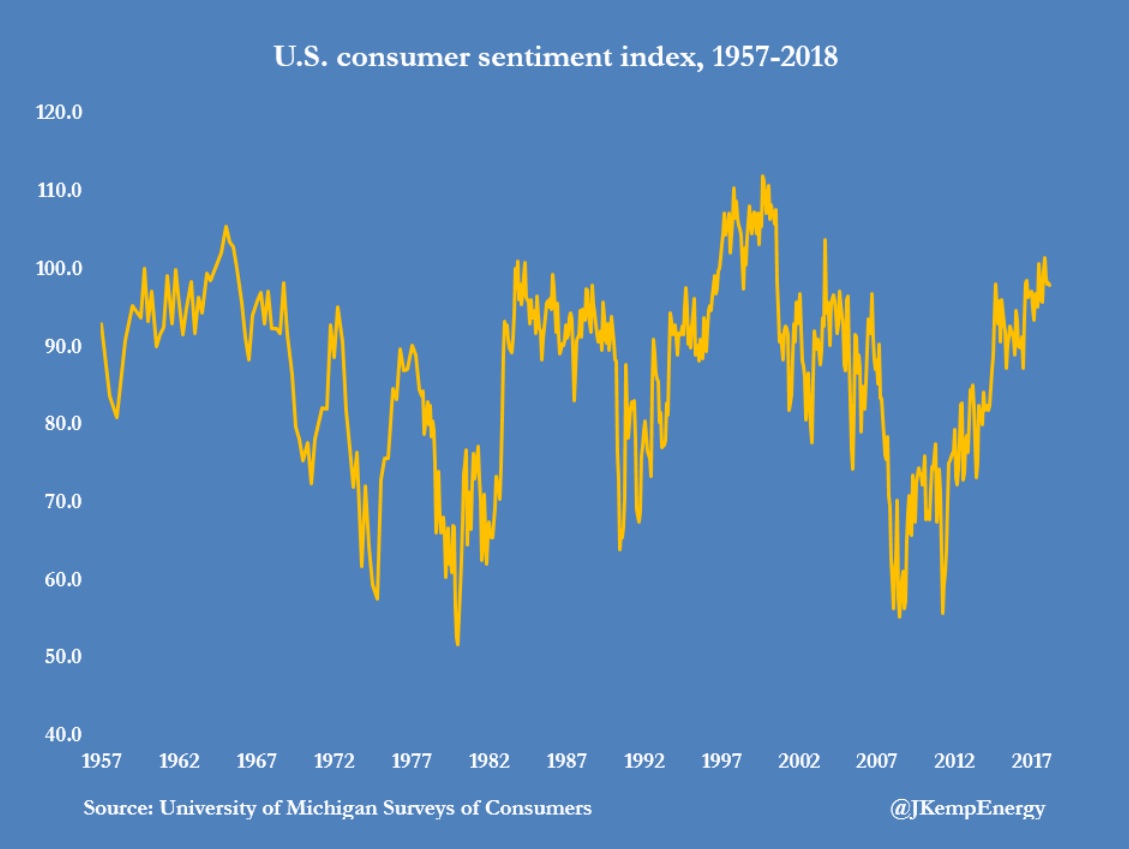

United States – Consumer Sentiment

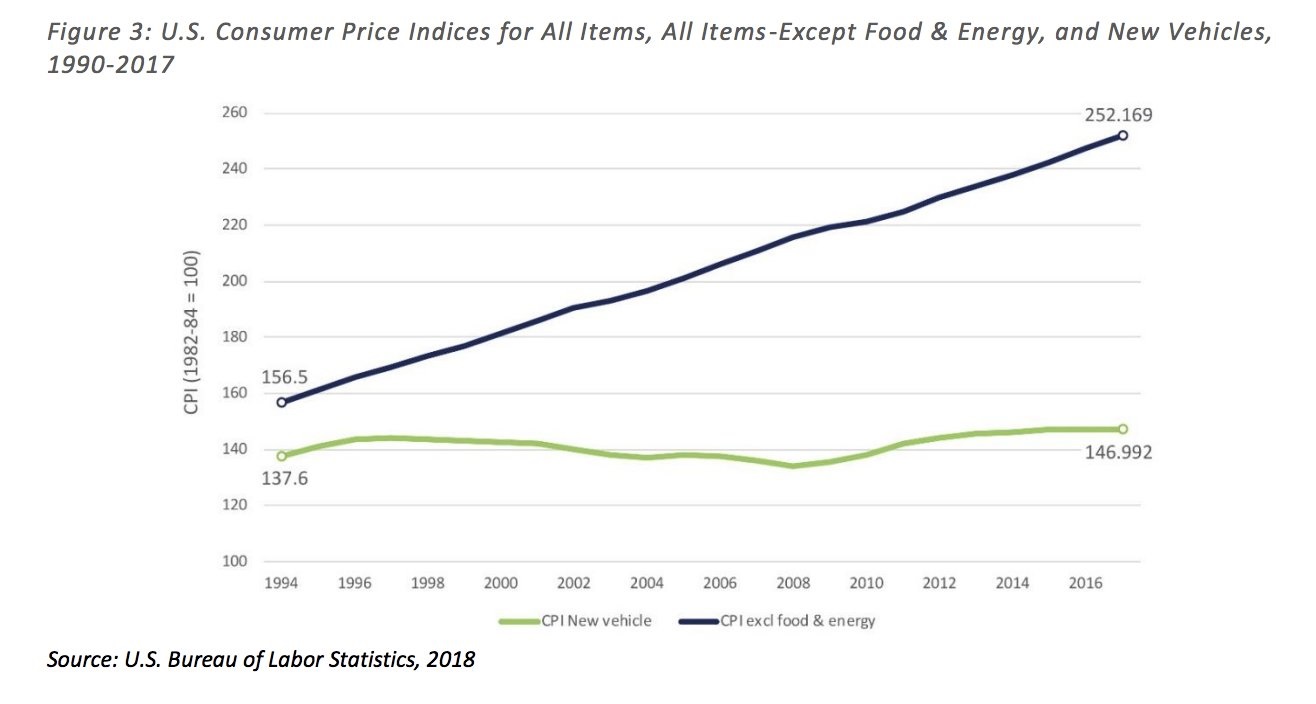

United States – CPI & New Vehicles

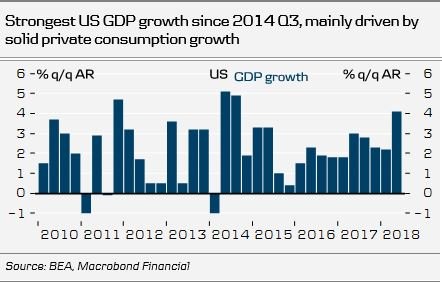

United States – GDP

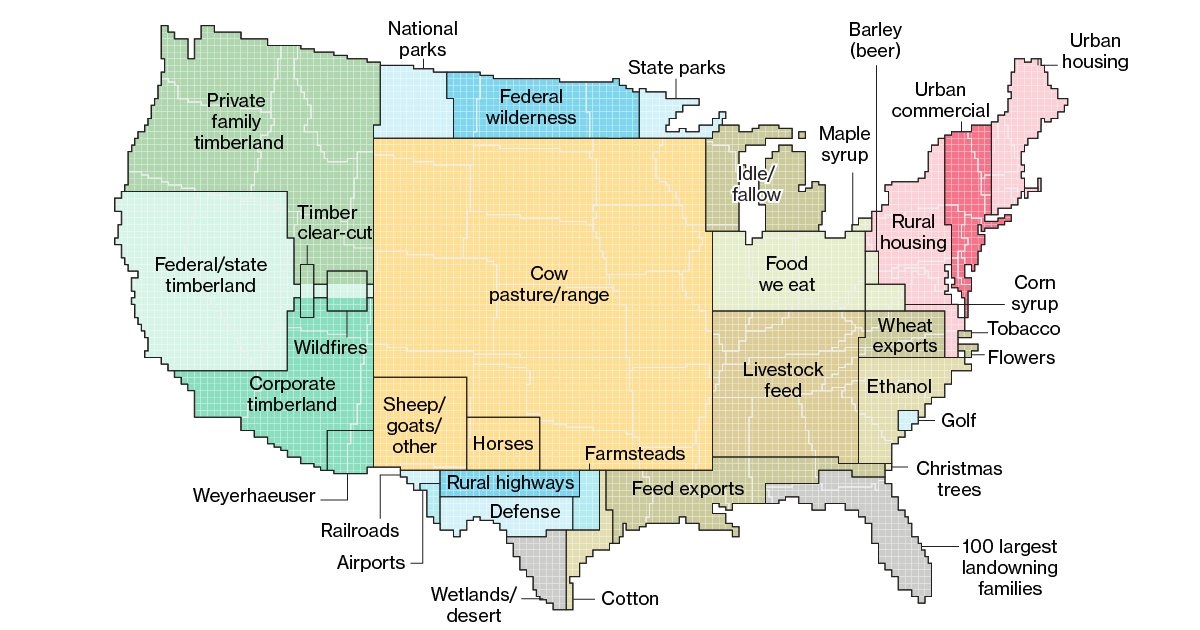

United States – Land Use

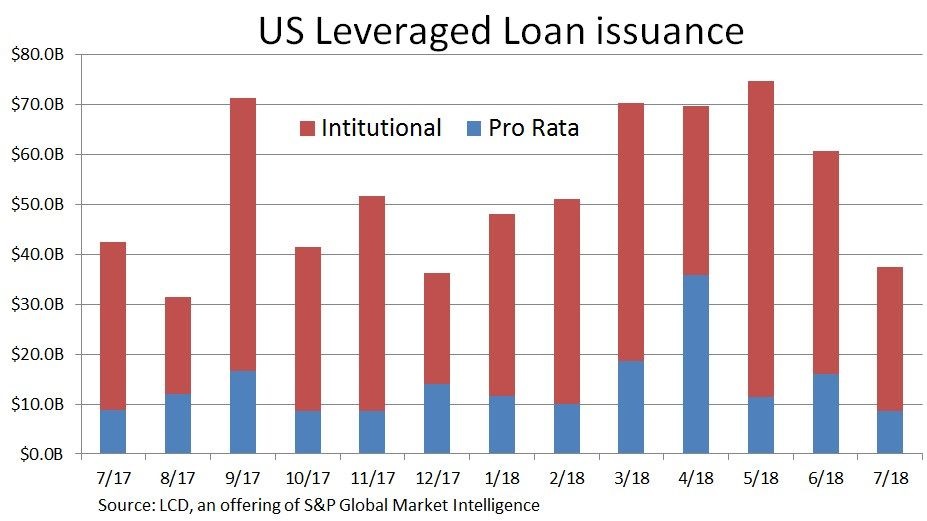

United States – Leveraged Loans

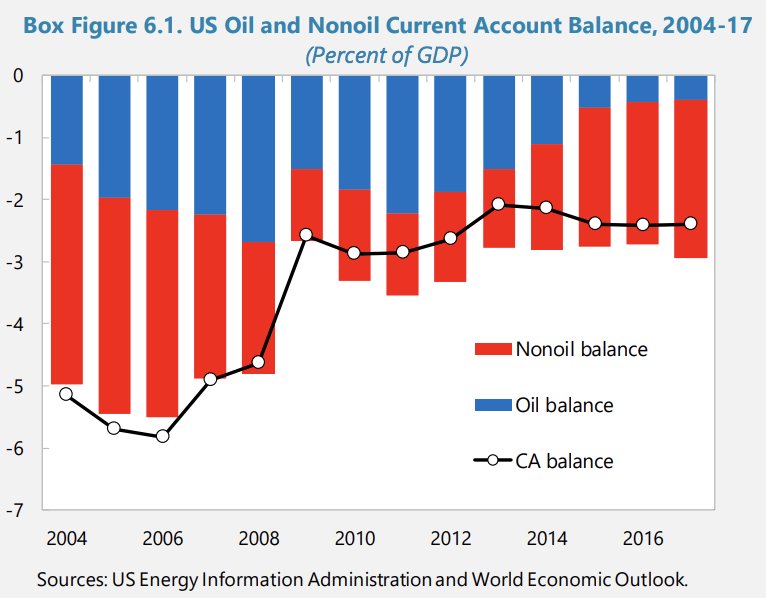

United States – Oil & Non-Oil Current Account

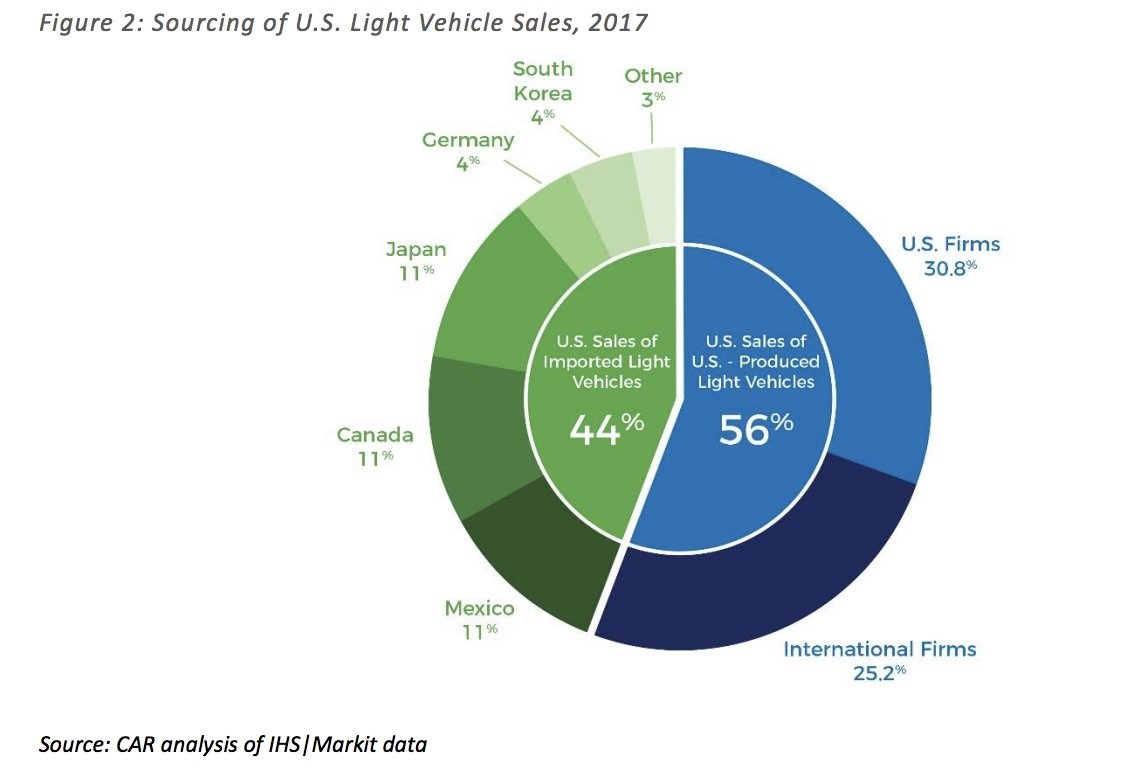

United States – National Origin of Light Vehicle Sales

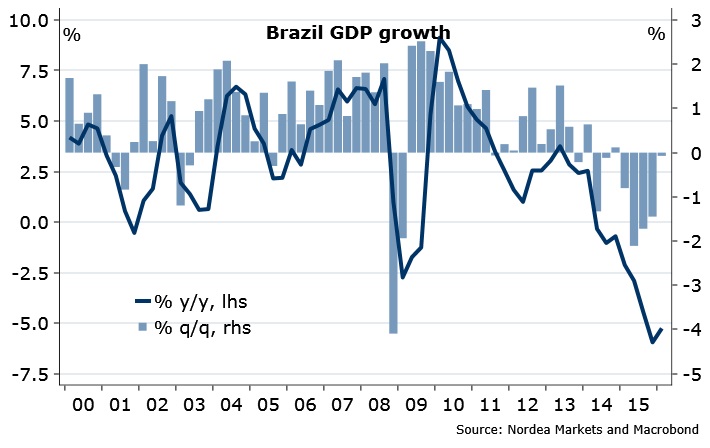

Brazil – GDP Growth

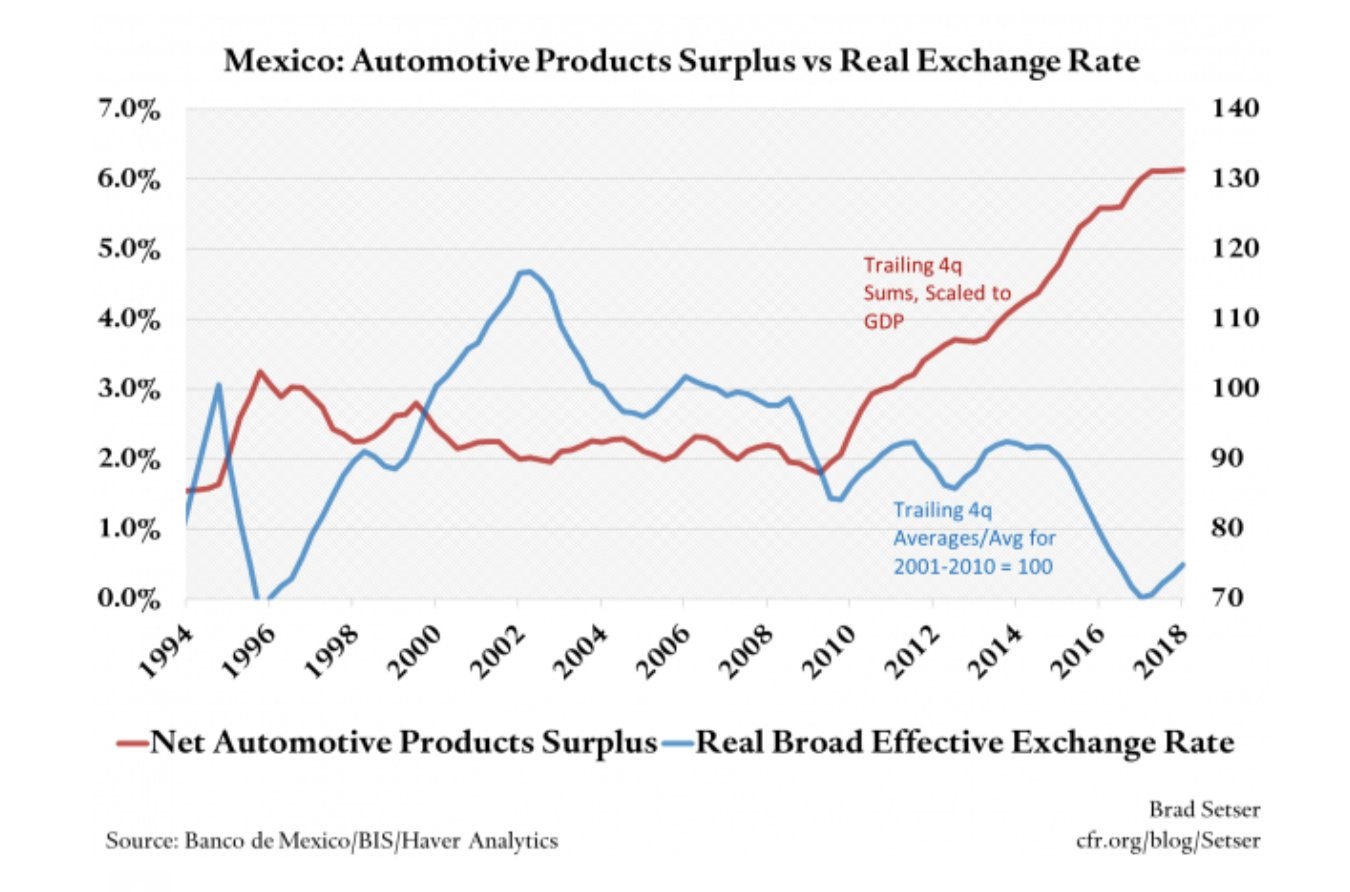

Mexico – Automotive Products Exports & Currency

China – Asia

Beijing Real Estate

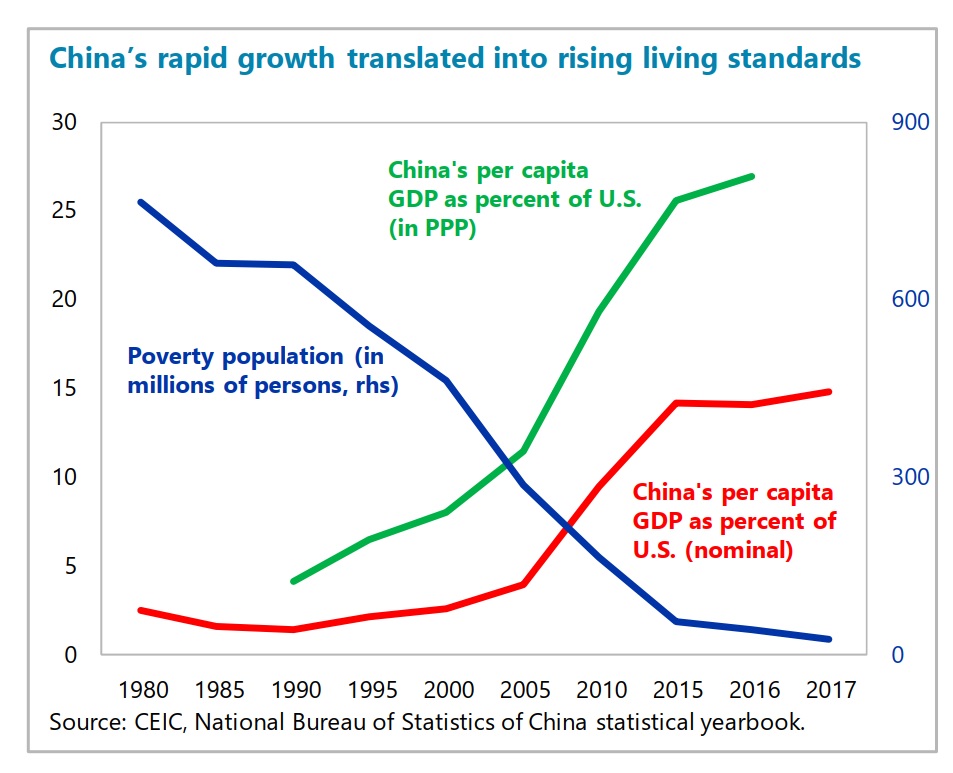

China Per Capita GDP & Poverty

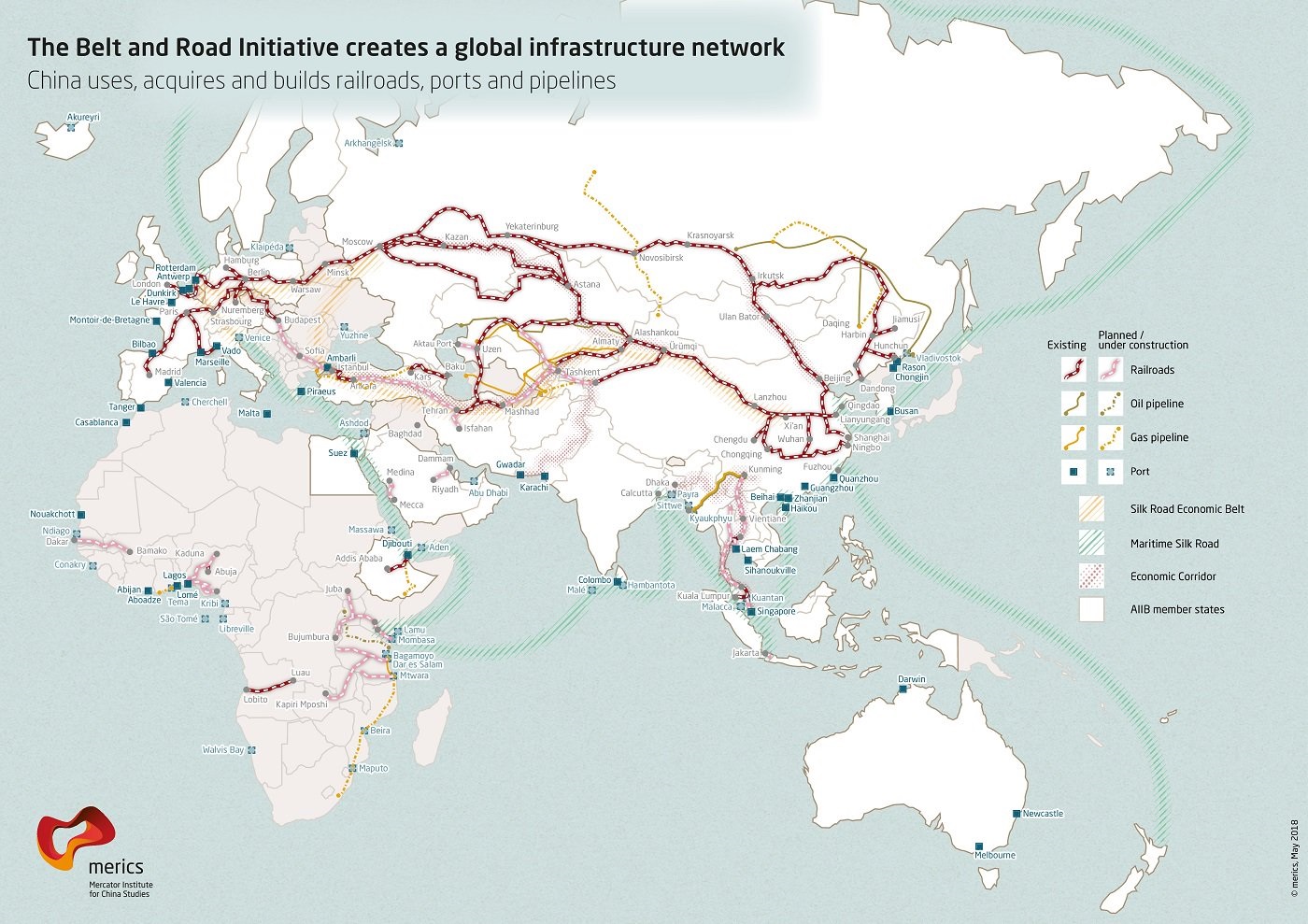

China – Belt and Road Infrastructure

China Crayfish Production

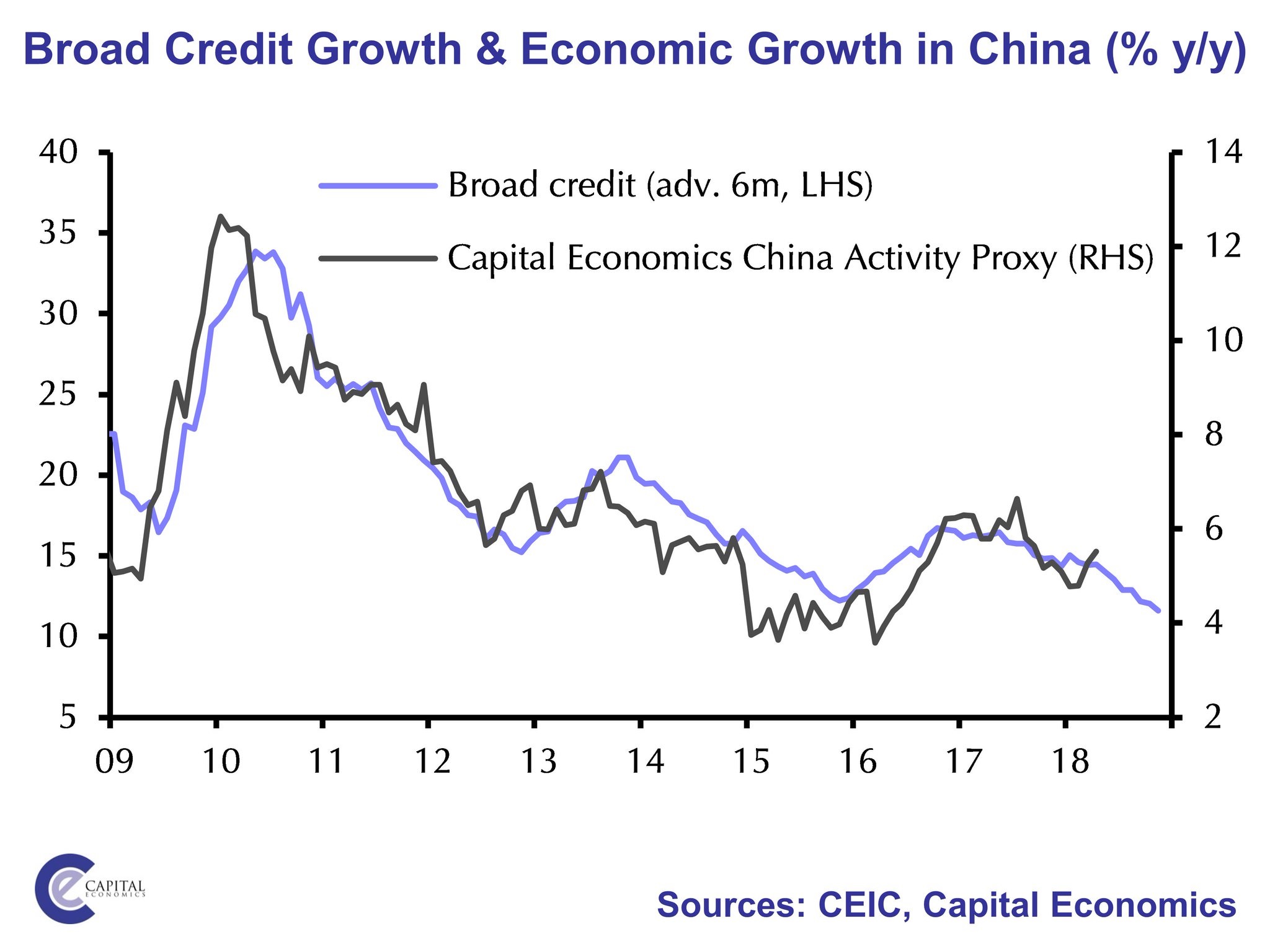

China Credit Growth

China GDP – Contributions

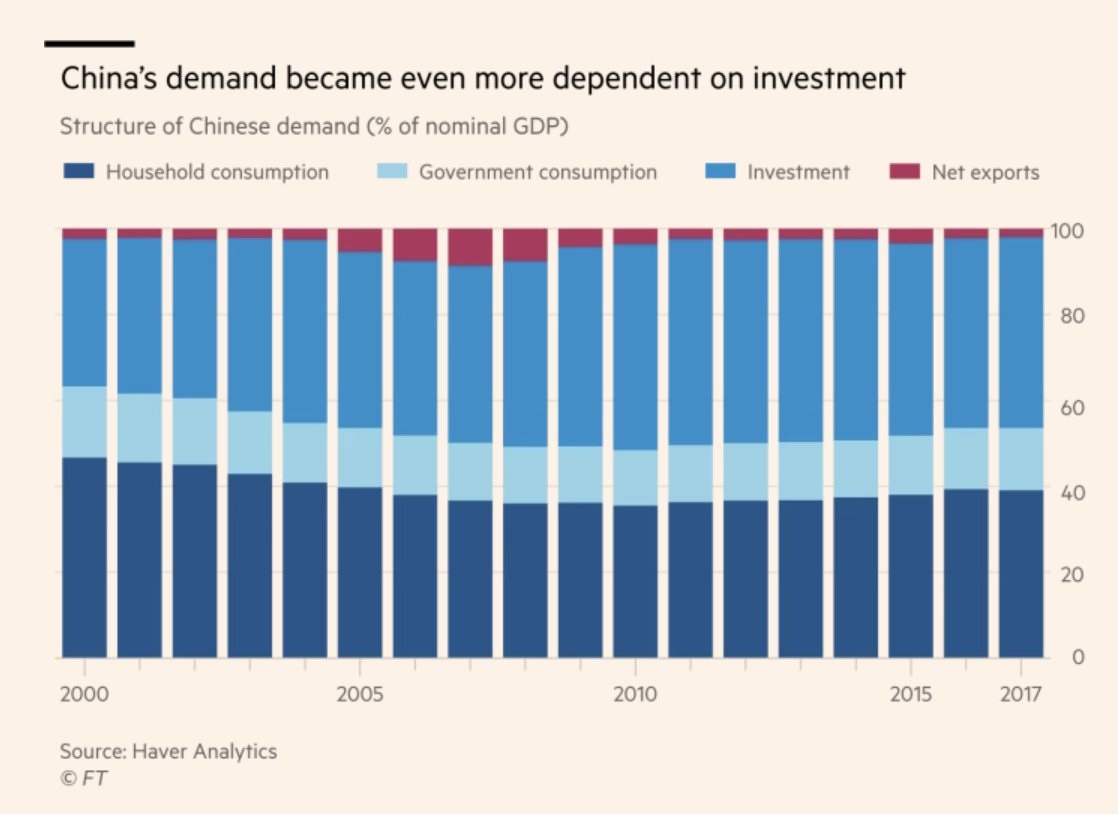

China – Structure of Demand

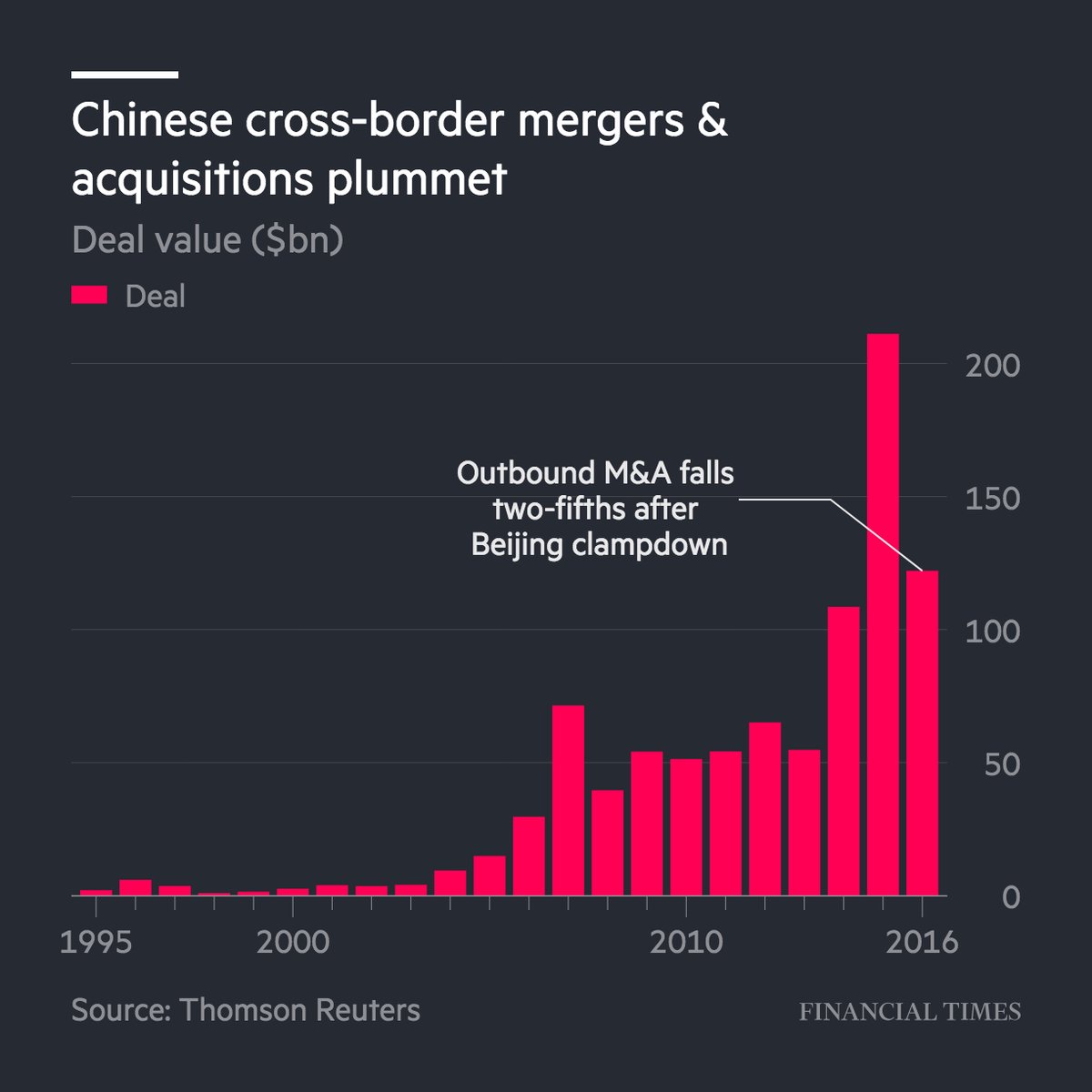

China – Cross Border M&A

China – Provinces with larger economy than United Kingdom

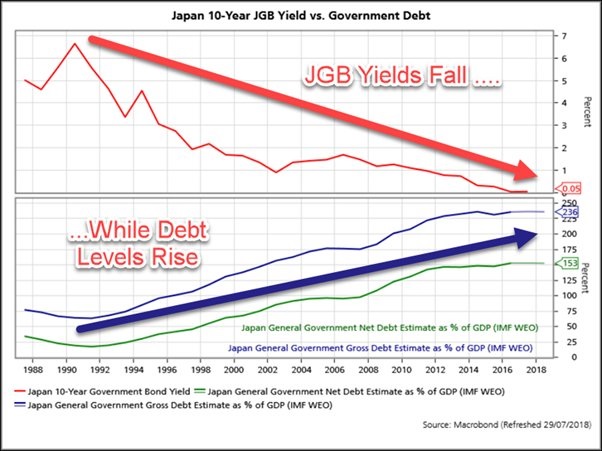

Japan Government Bonds & Japanese Debt

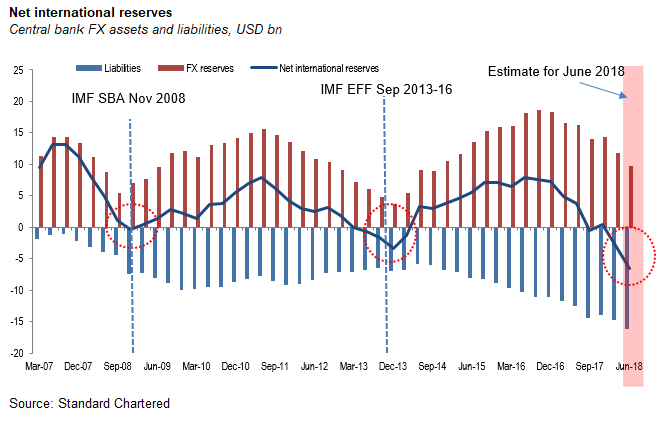

Pakistan – Net Balance

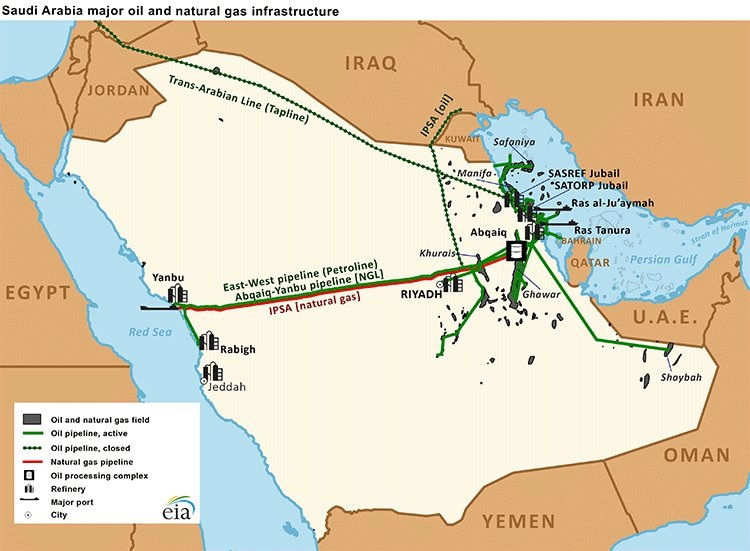

Saudi Arabia – Oil & Gas Infrastructure

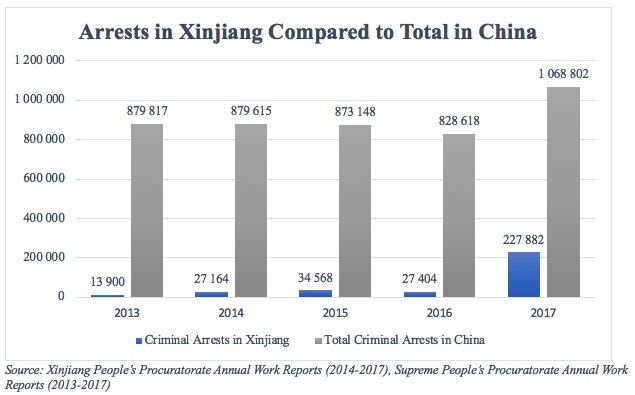

China – Xinjiang Arrests

Europe

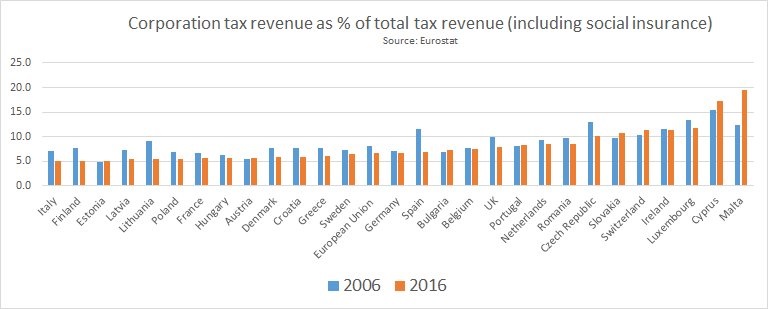

Europe Corporate Taxes

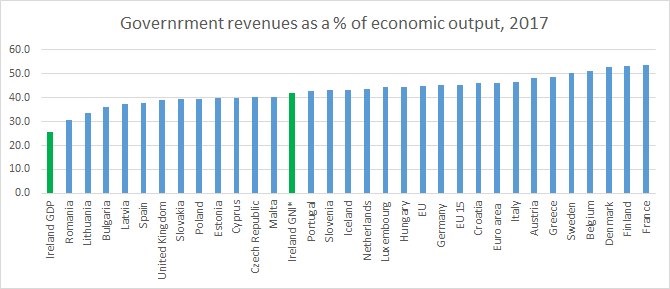

Europe – Government Revenues to Economic Output

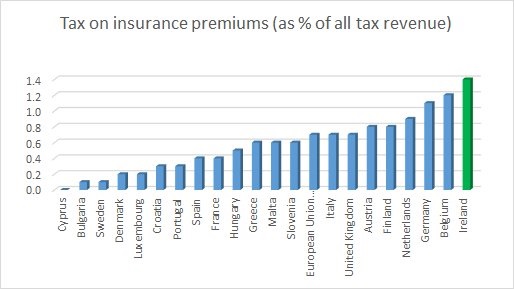

Europe – Taxes on Insurance Premiums

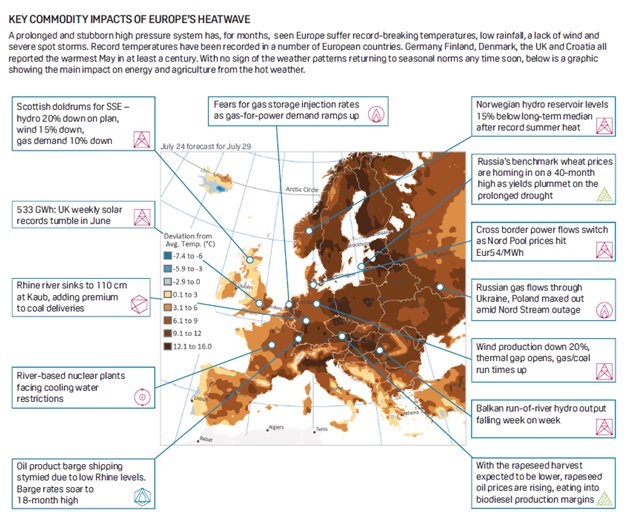

Europe – July 2018 Heatwave

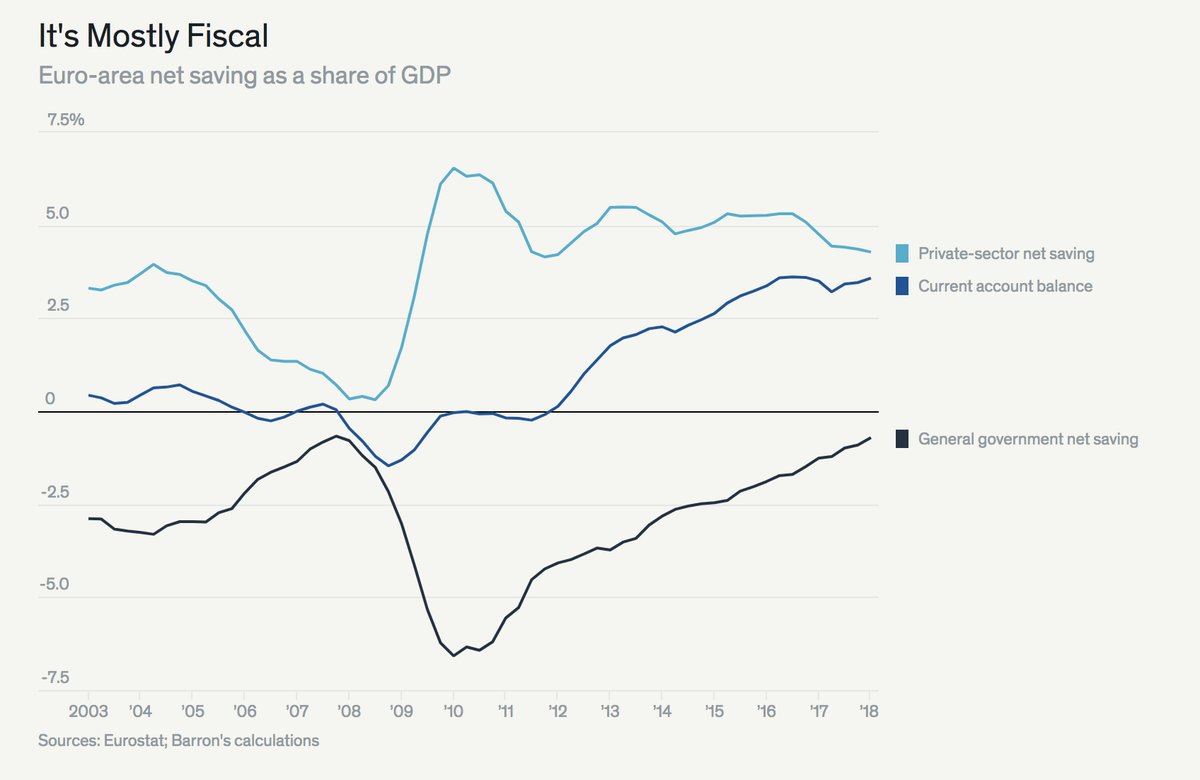

Europe – Net Saving to GDP

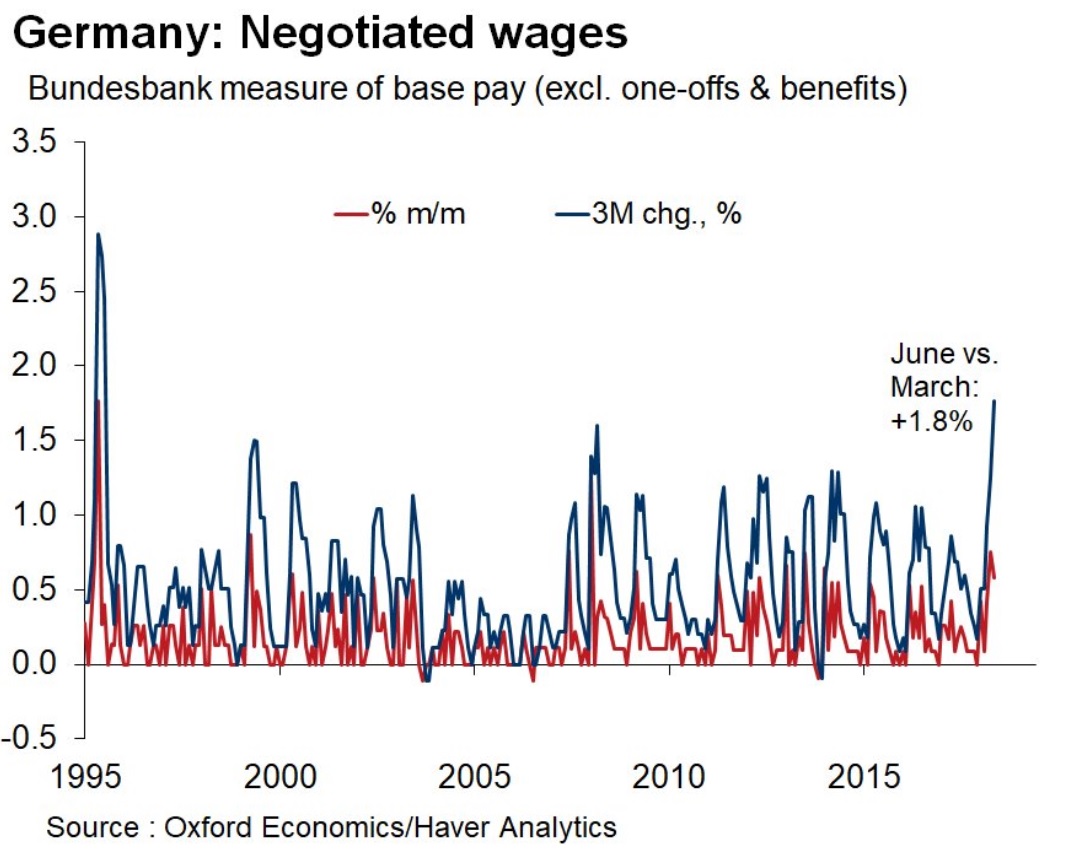

Germany – Negotiated Wages

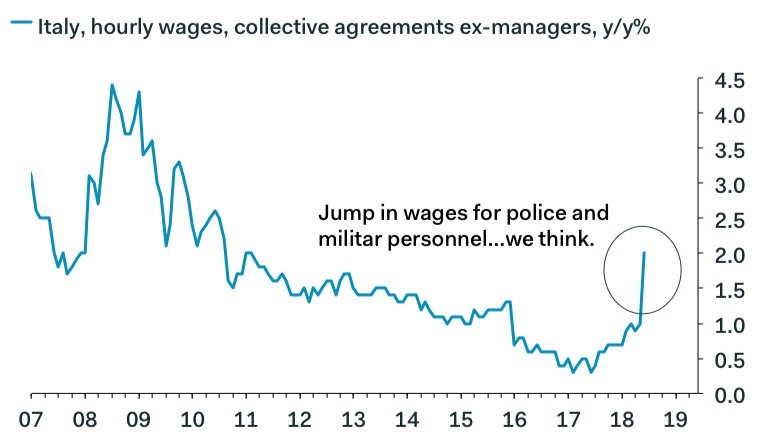

Italy – Wages

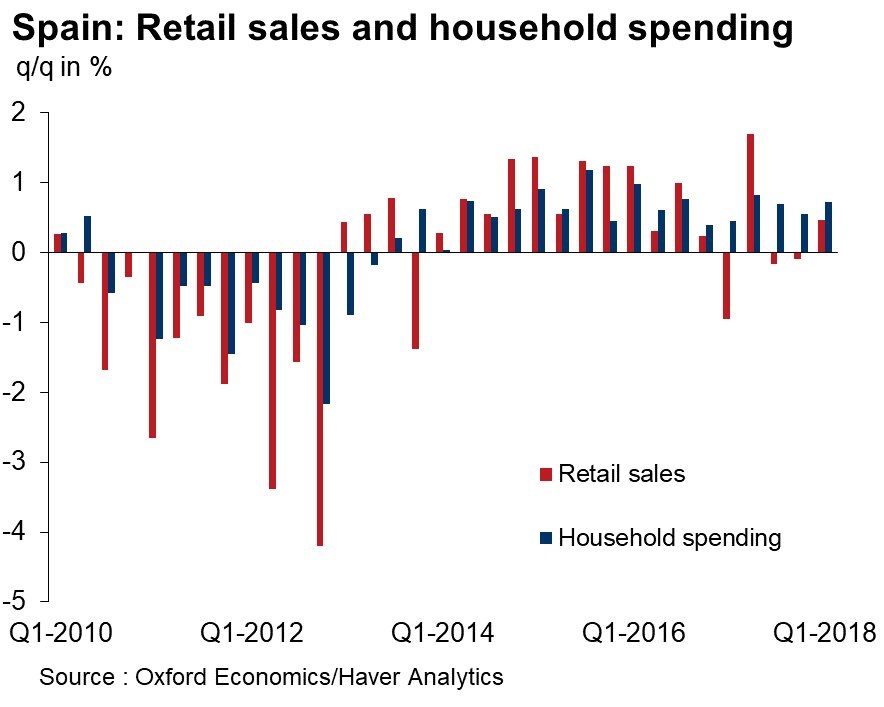

Spain – Retail Sales & Household Spending

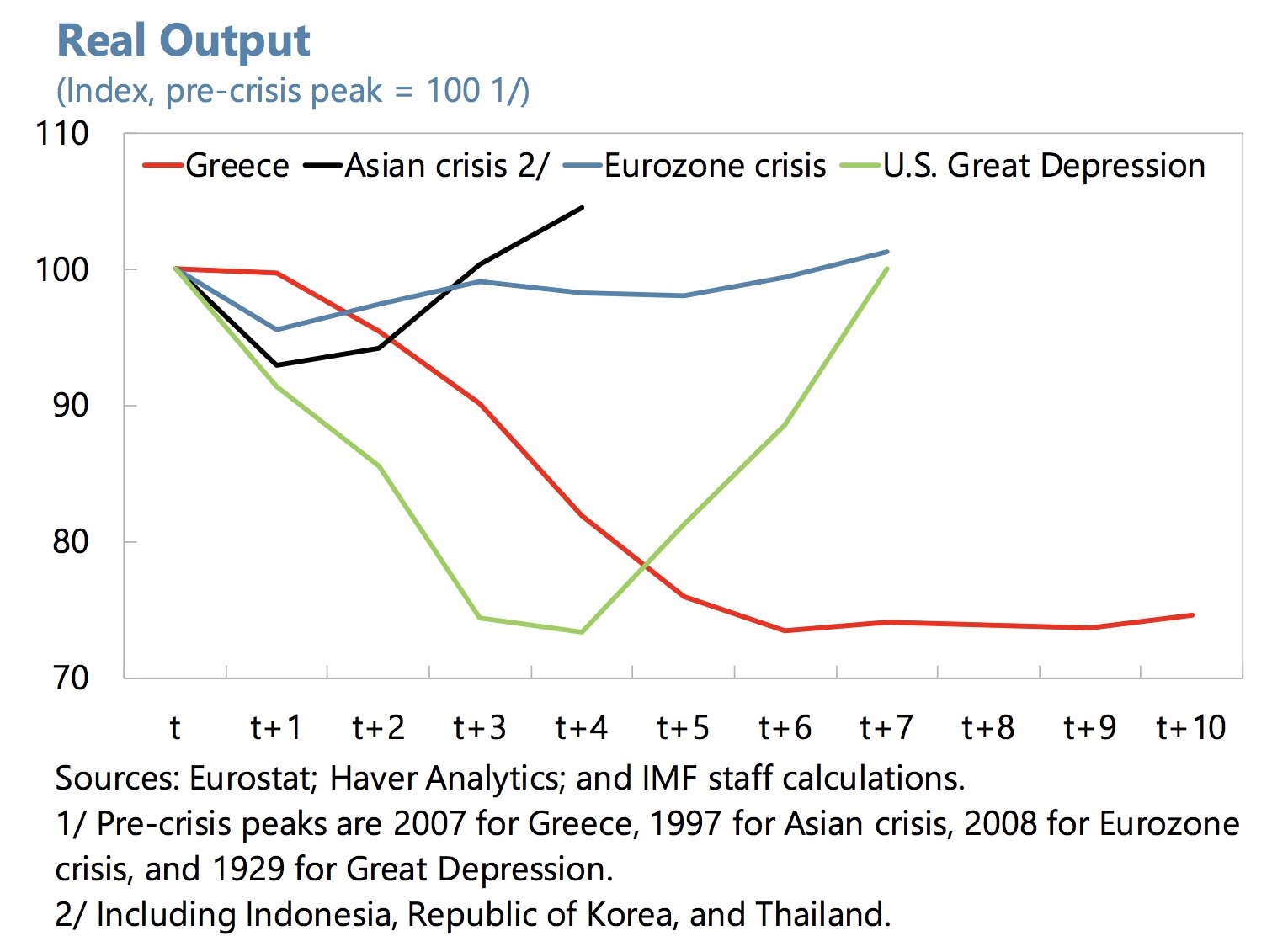

The Greek Disaster

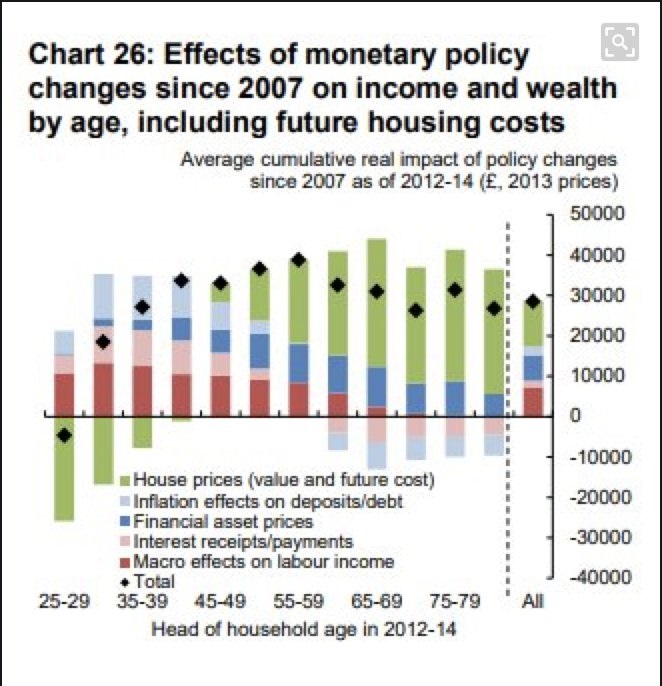

United Kingdom – Effects of post 2007 Monetary Policy

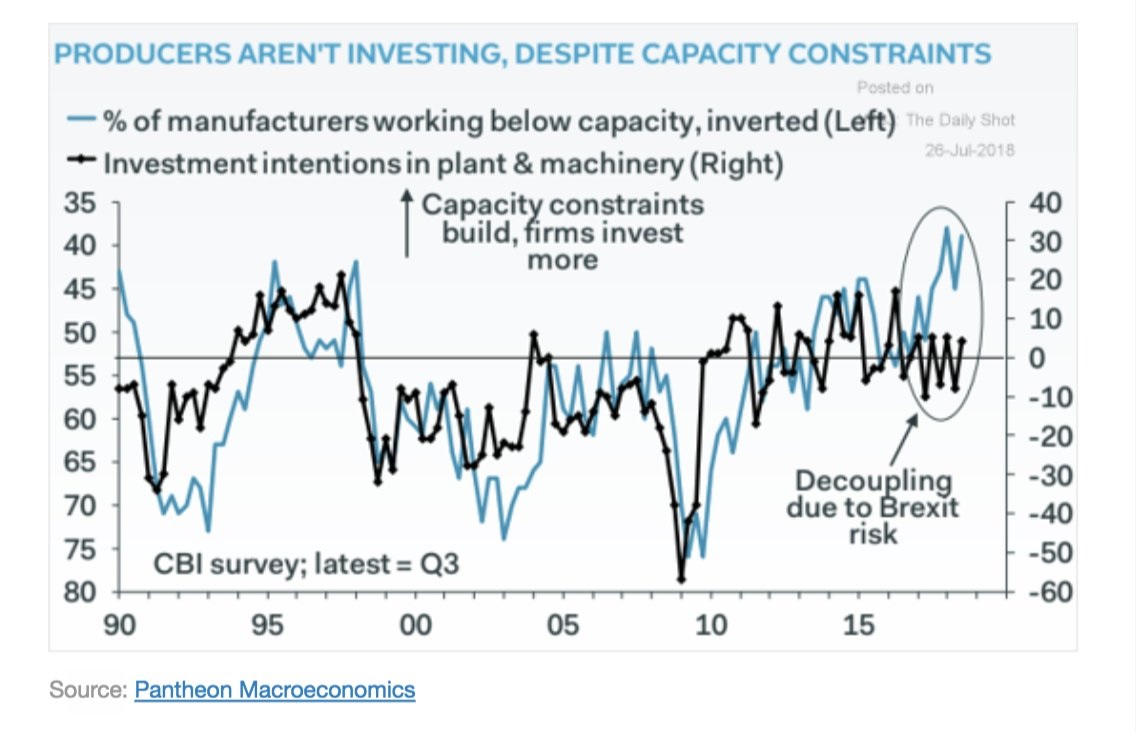

United Kingdom – Plant & Machinery Investment

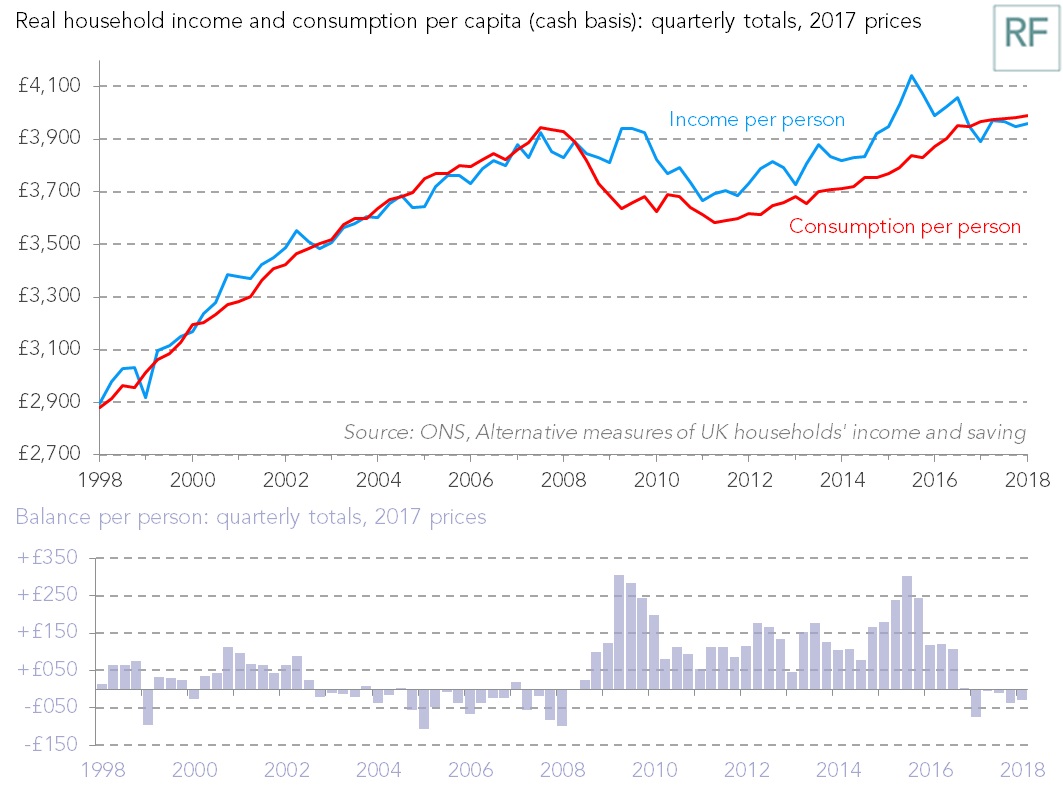

United Kingdom – Household Income & Consumption

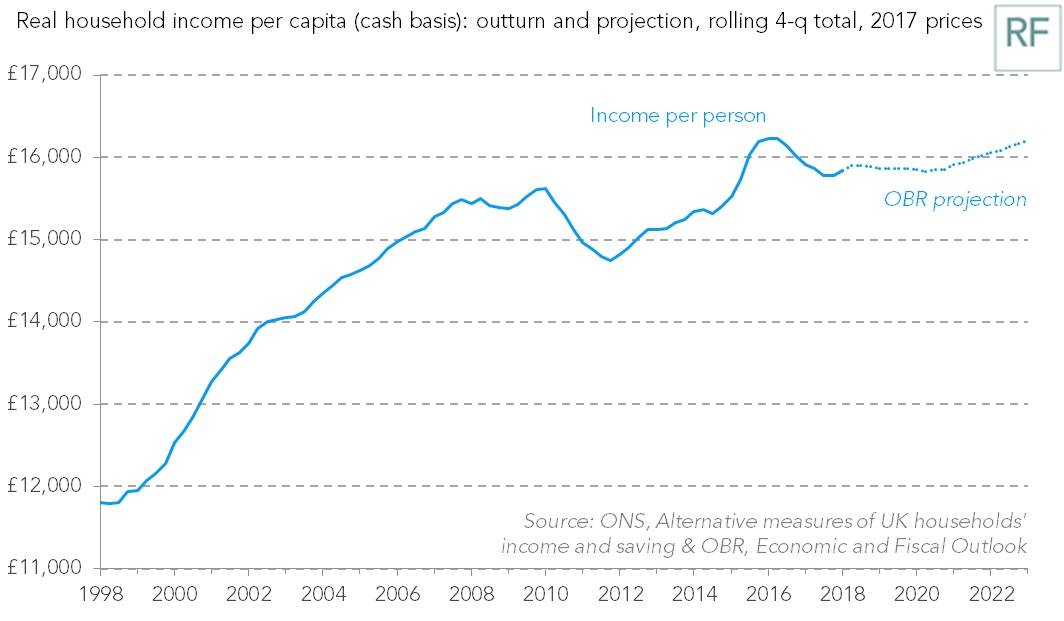

United Kingdom – Real Household Income Per Capita

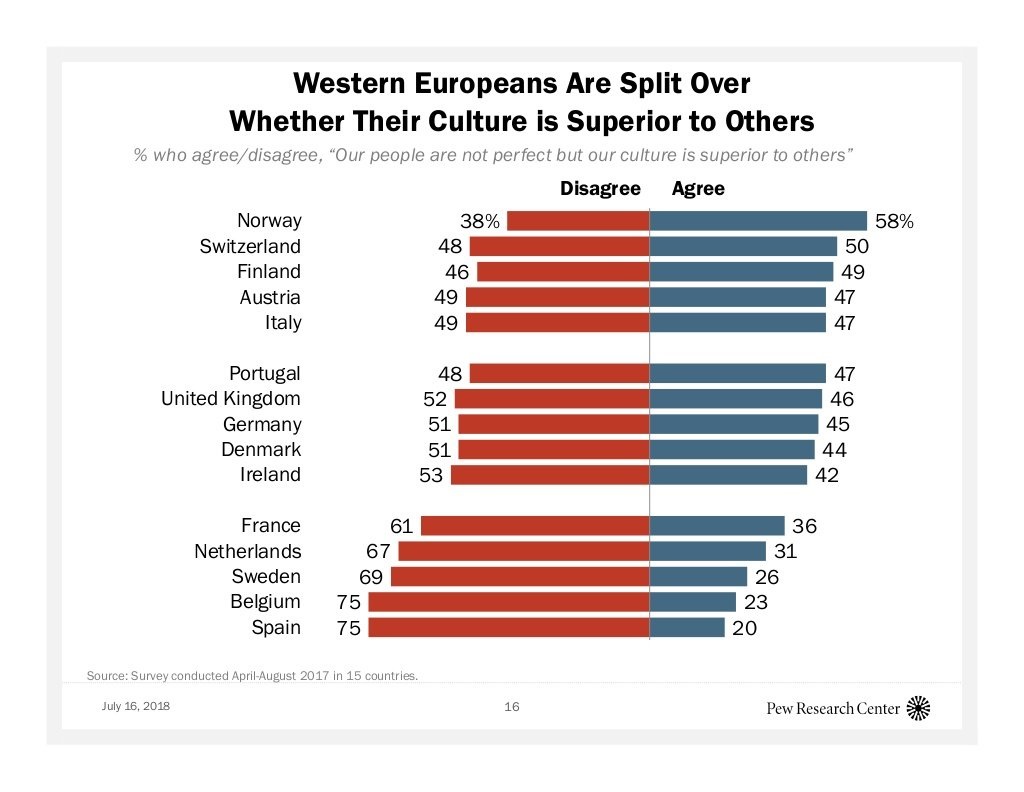

Europe – Perception of Cultural Superiority

Commodities

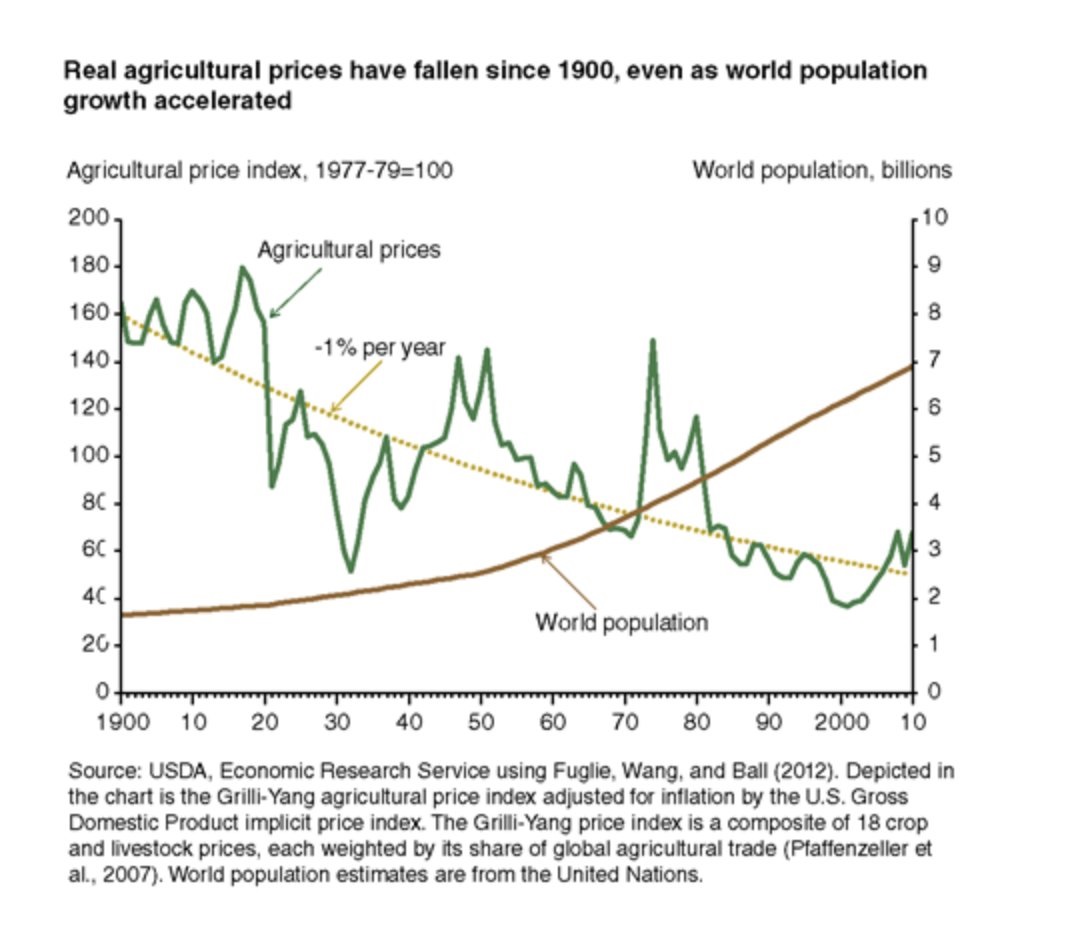

Real Agricultural Prices & Population

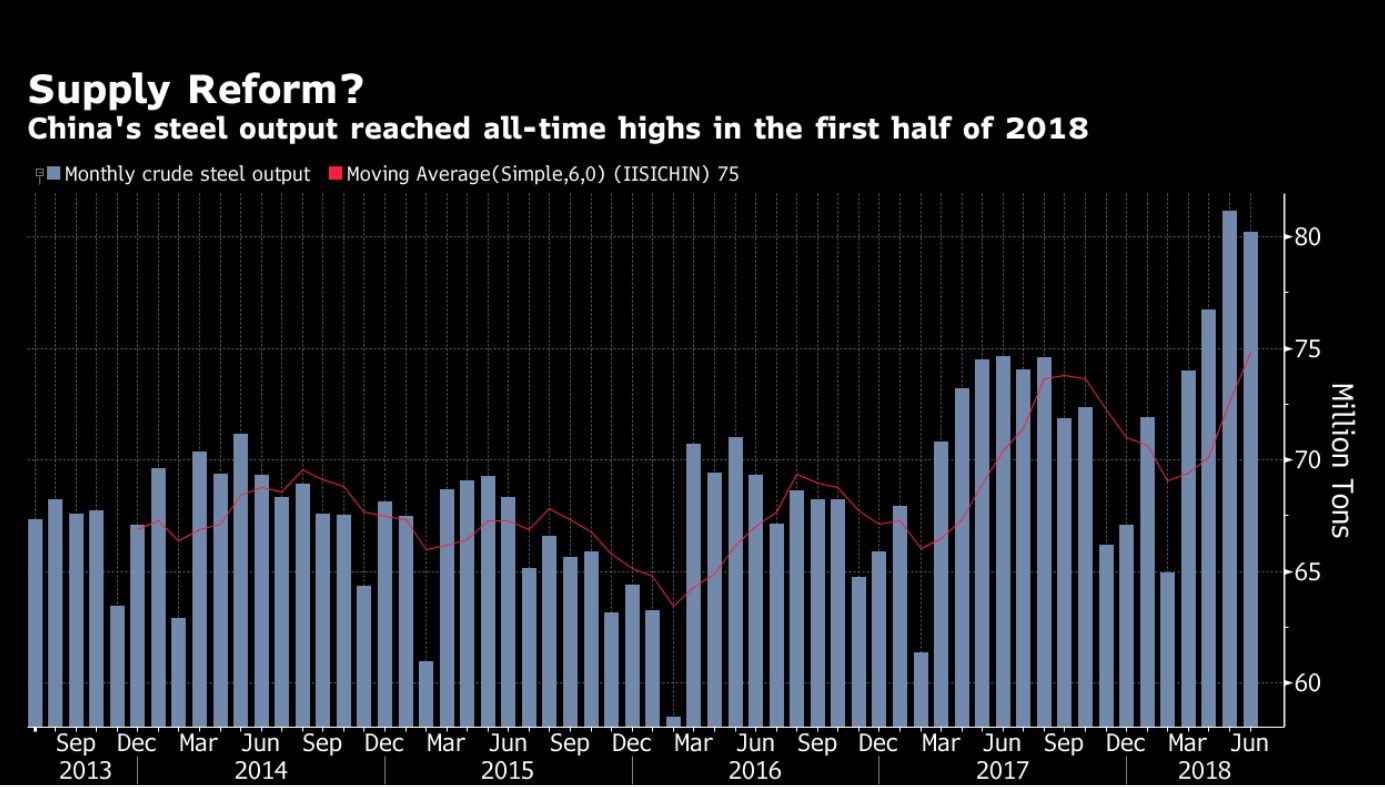

China Steel Output

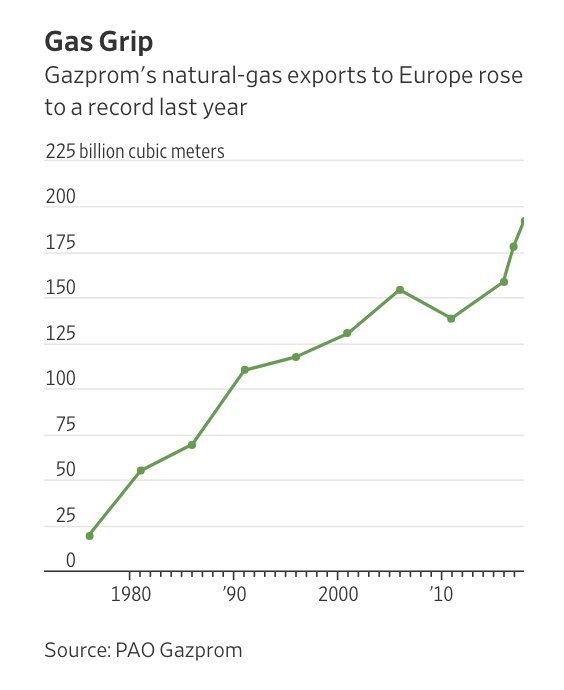

Gazprom – Exports to Europe

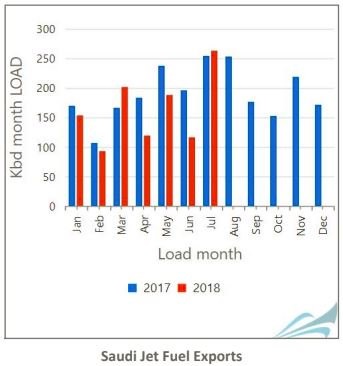

Saudi Jet Fuel Exports

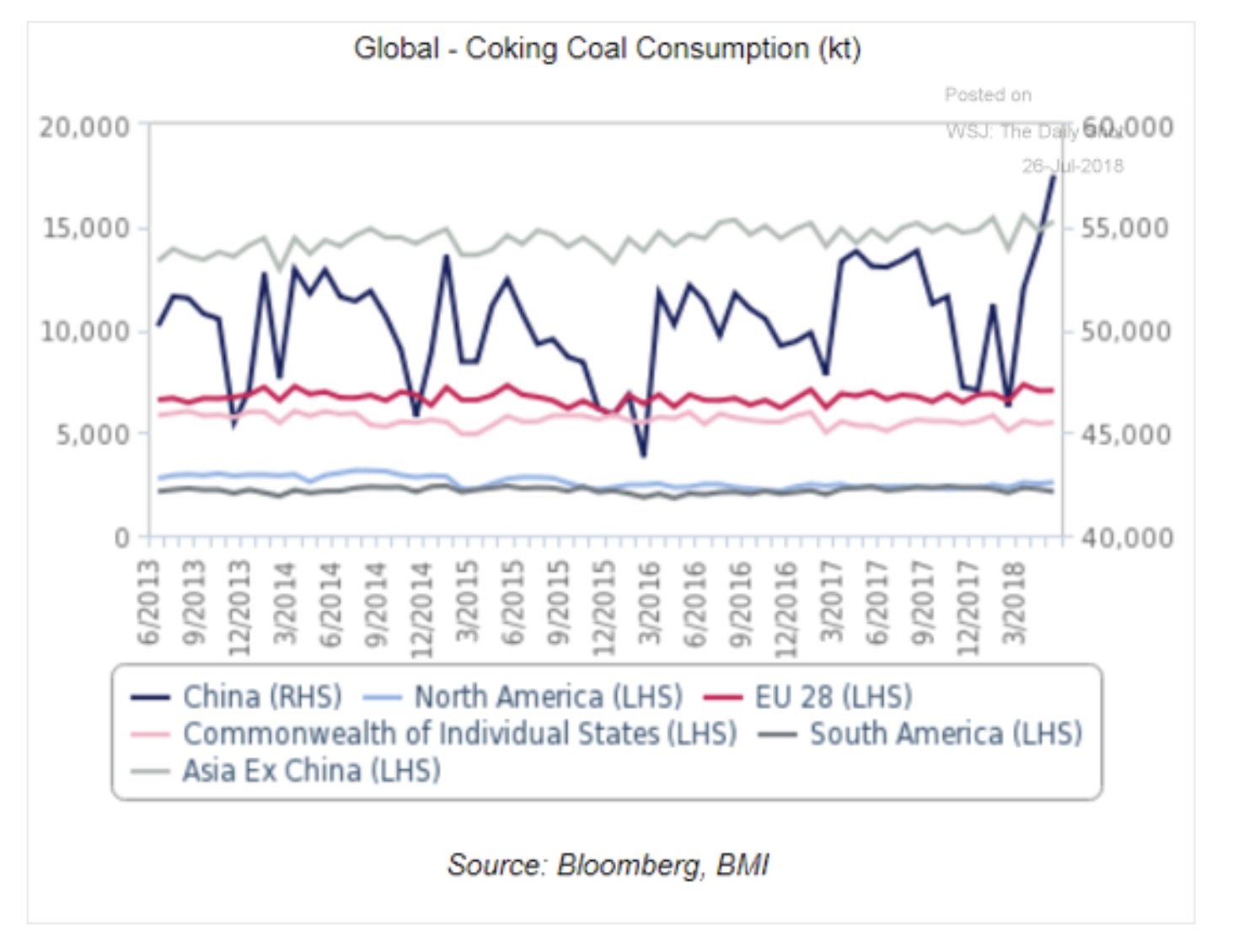

Global Coking Coal

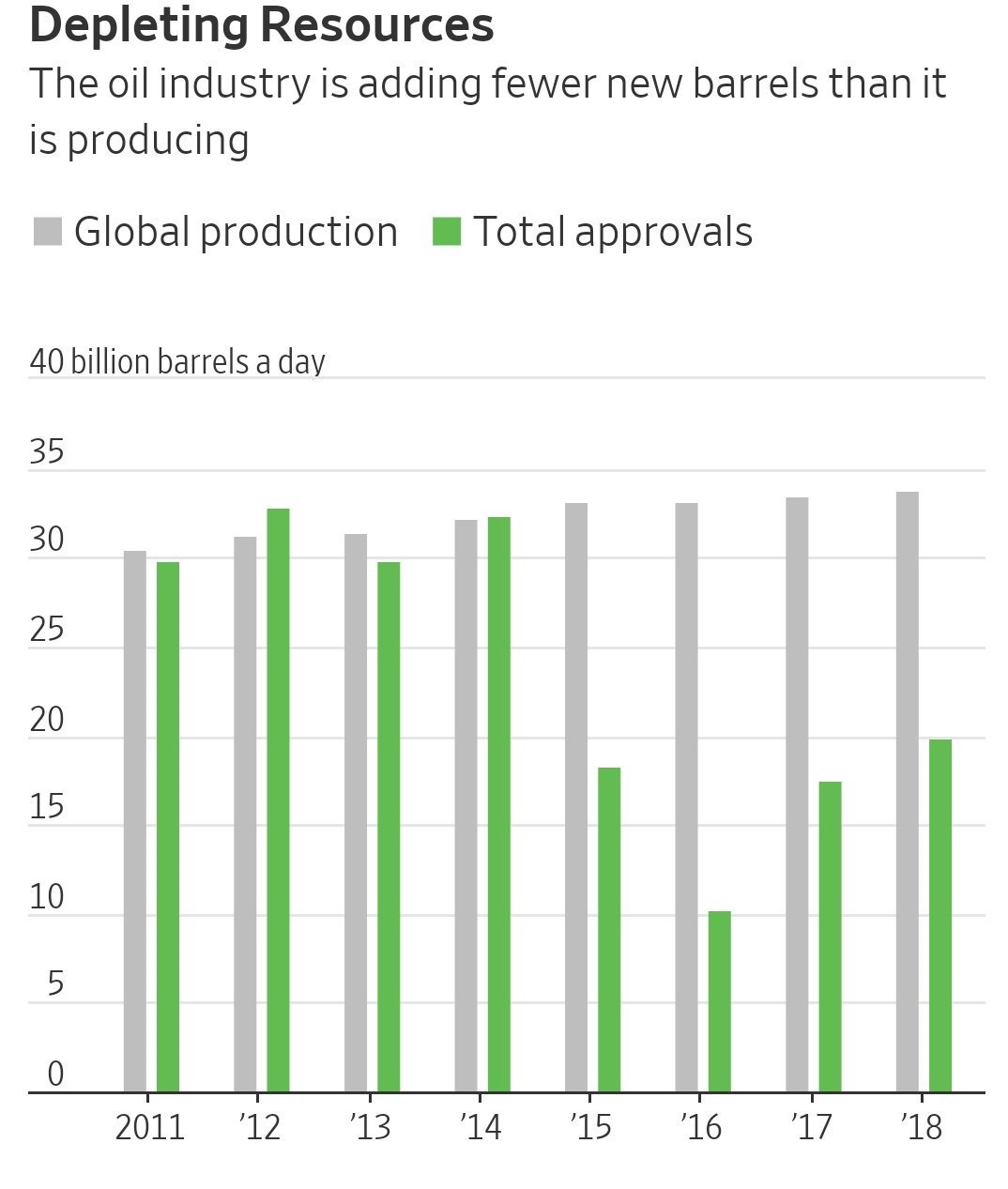

Oil – Resource Depletion

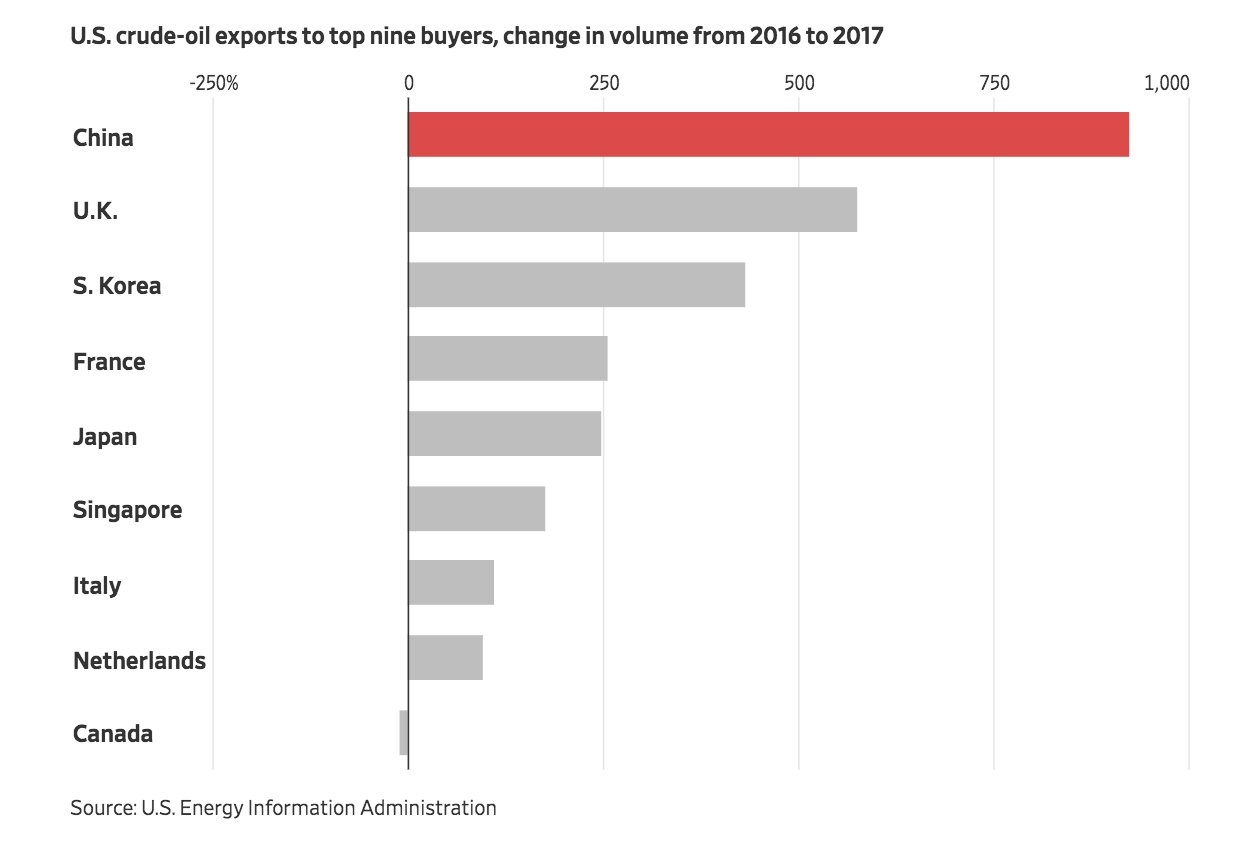

US Crude exports – Volume changes 2016-2017

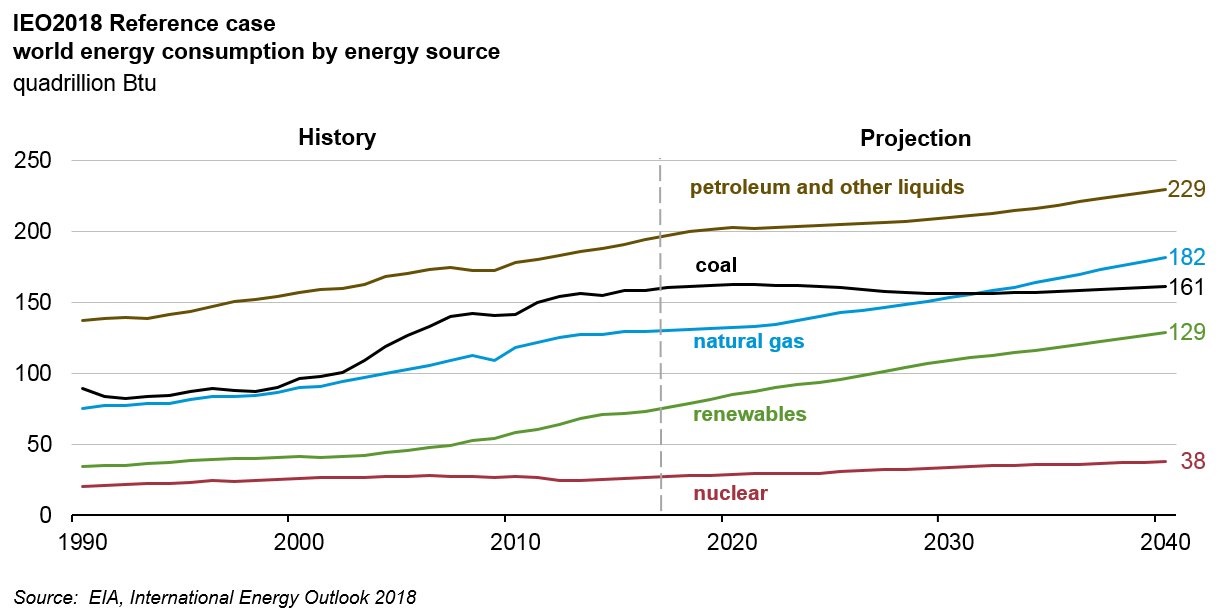

Global Energy Consumption by Source

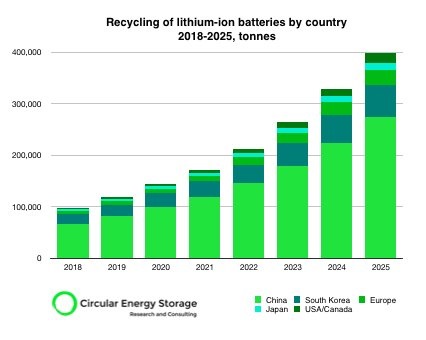

Lithium-Ion Battery Recycling

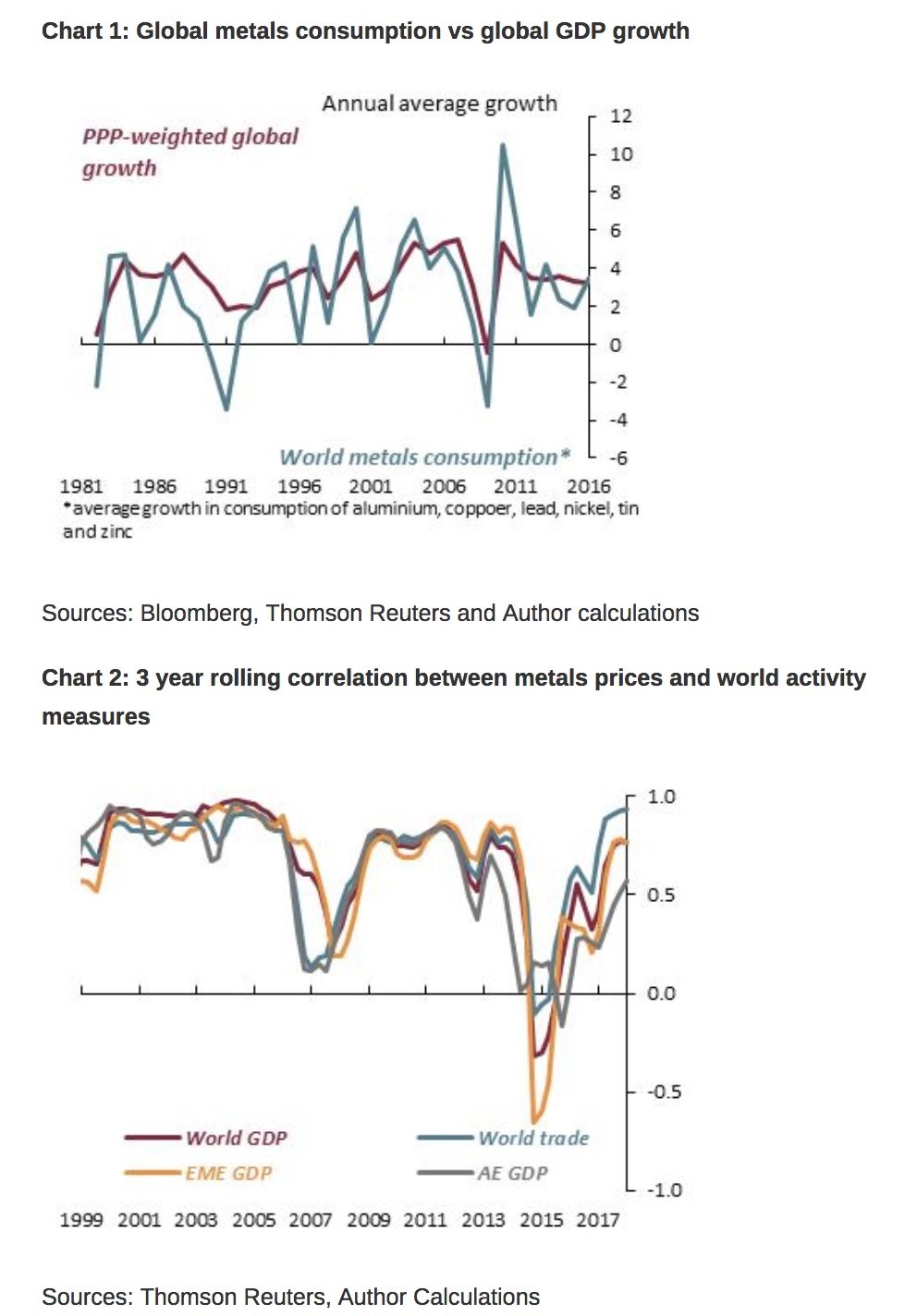

Global Metals and Global GDP/Activity

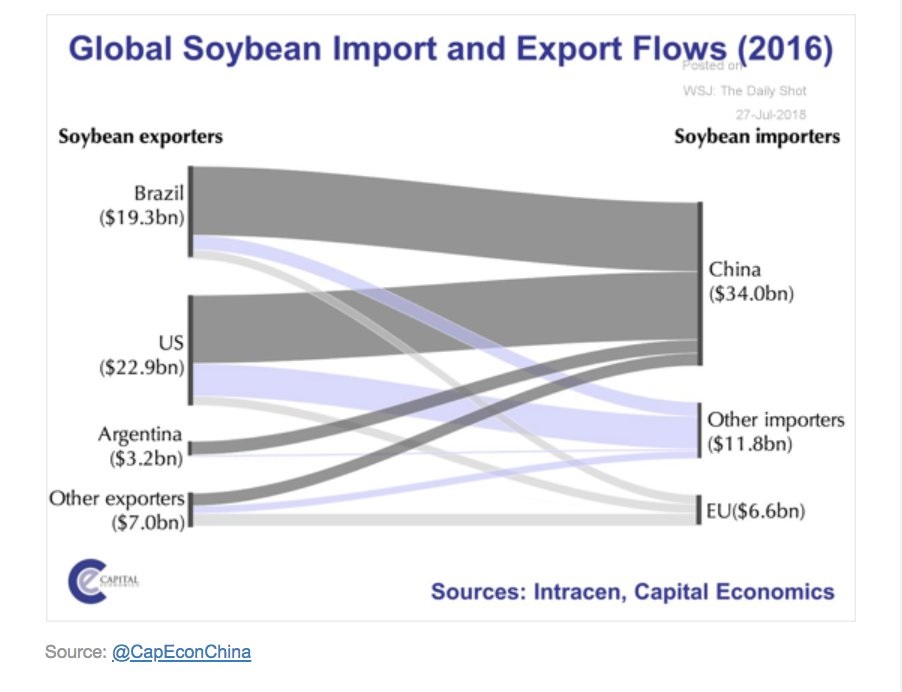

Global Soybean Flows

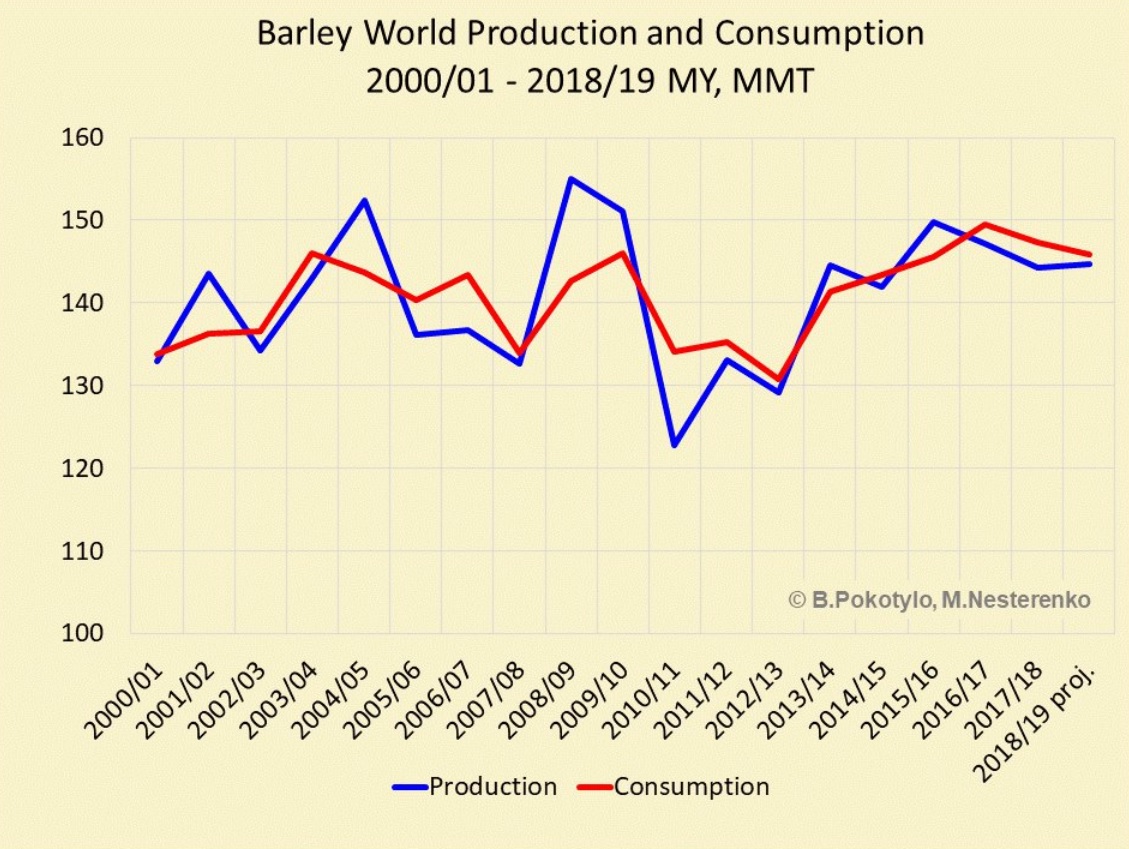

Barley – World Production & Consumption

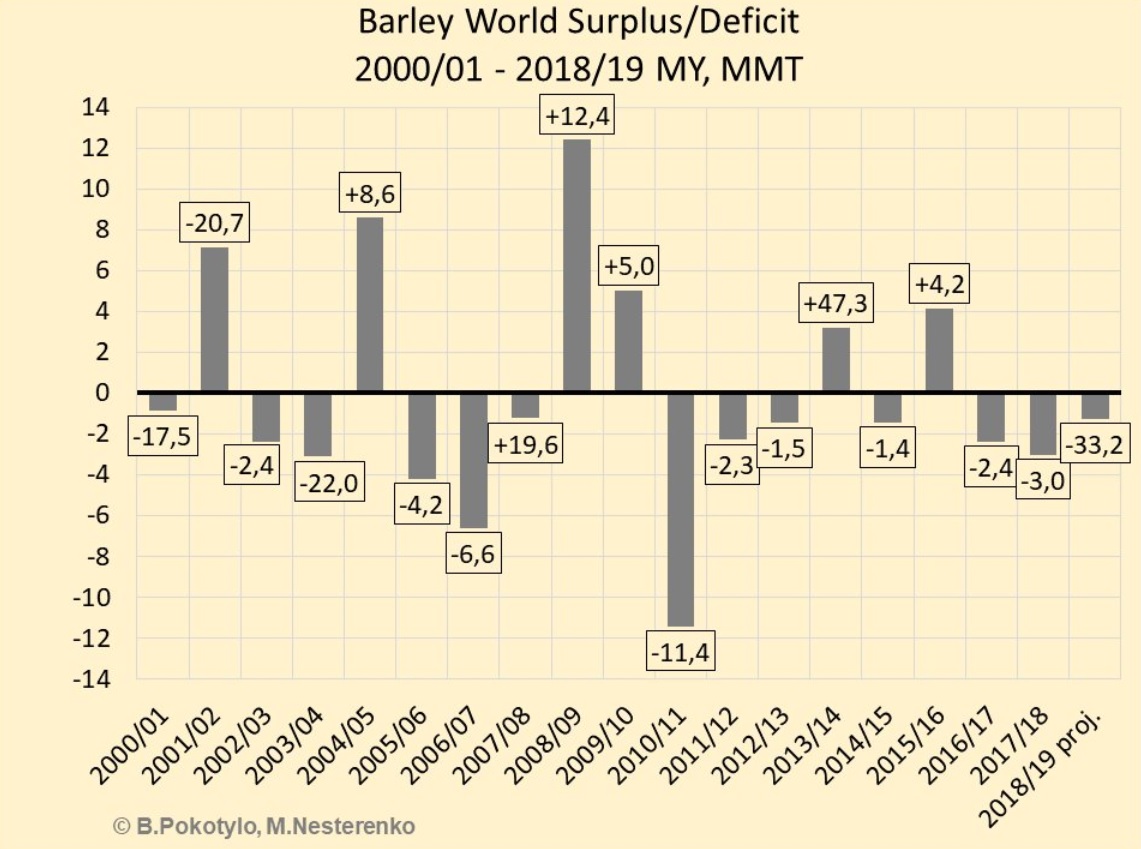

Barley – Global Balance

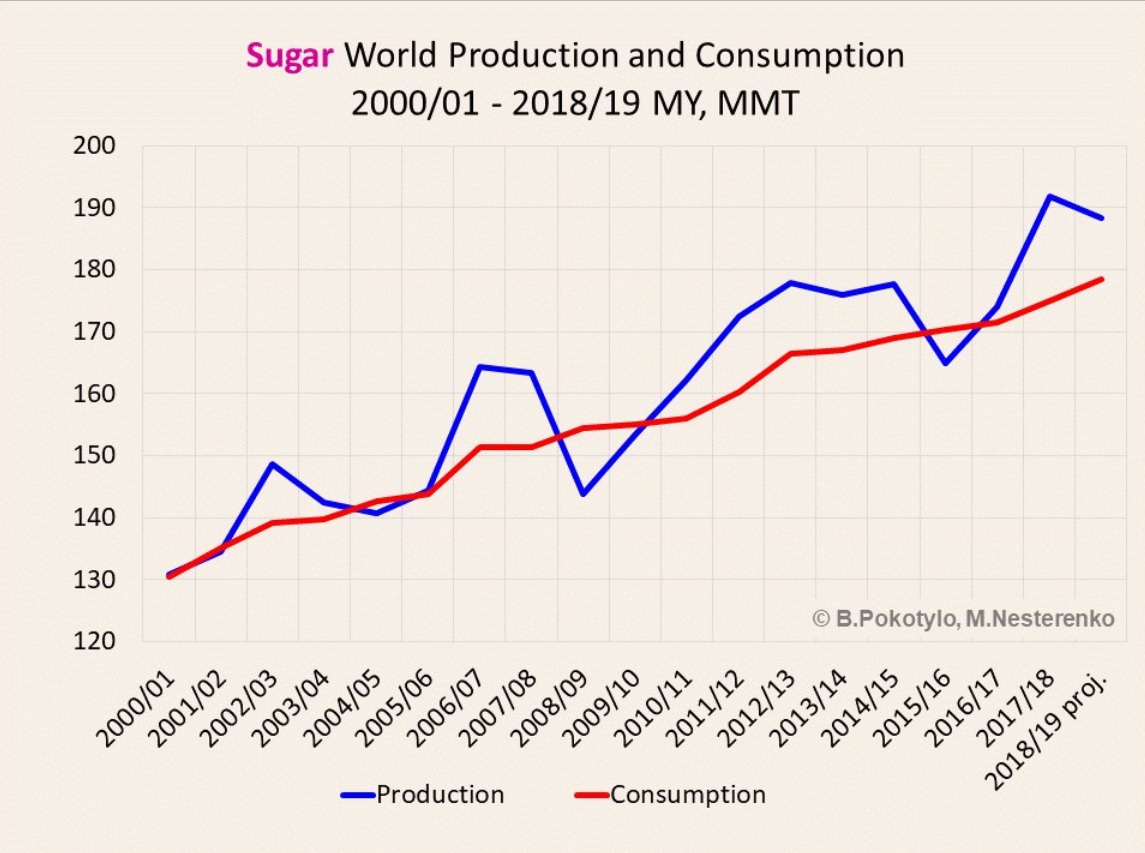

Global Sugar – Production & Consumption

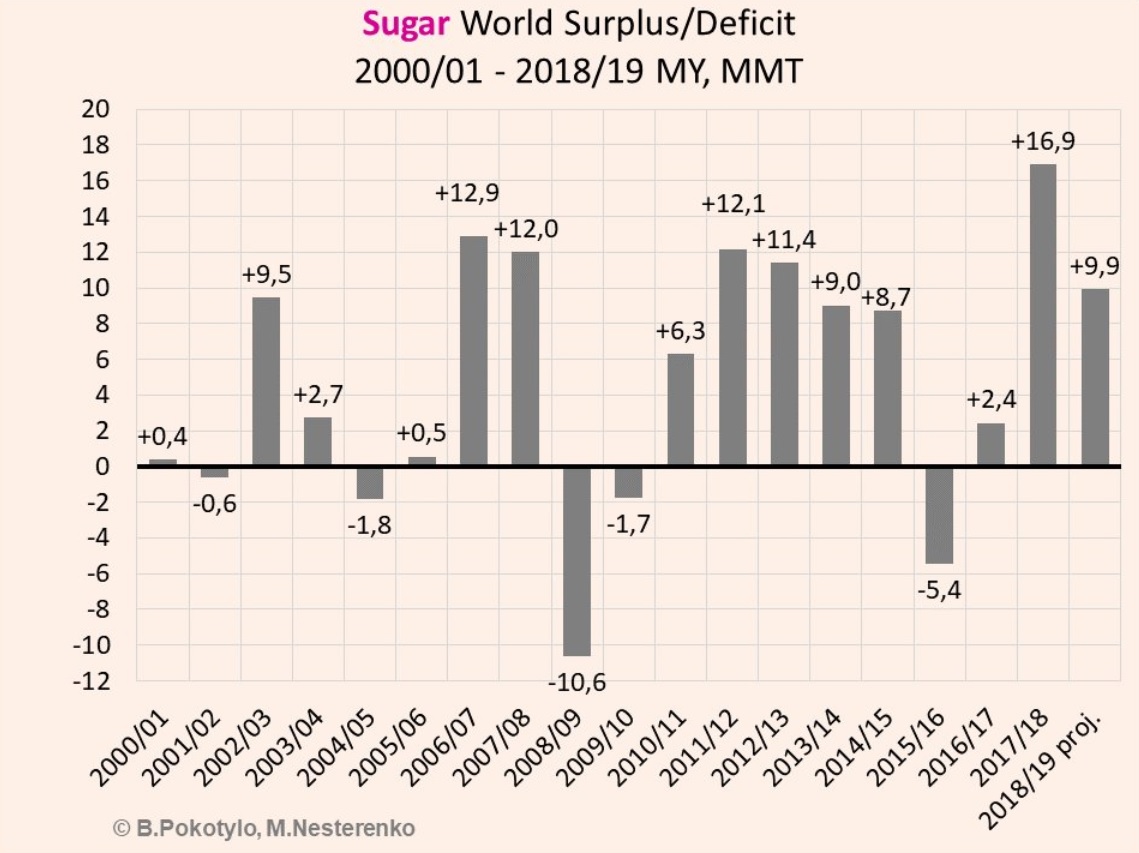

Sugar – Global Balance

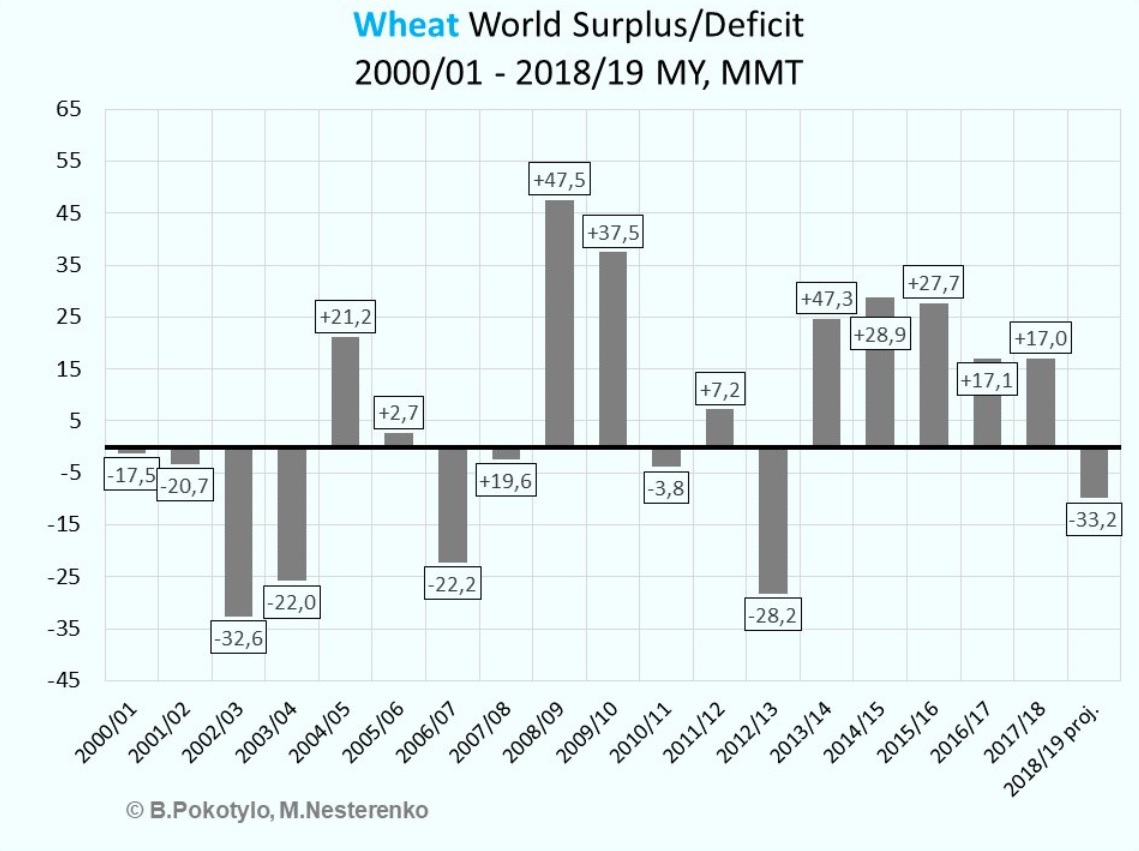

Global Wheat Balance

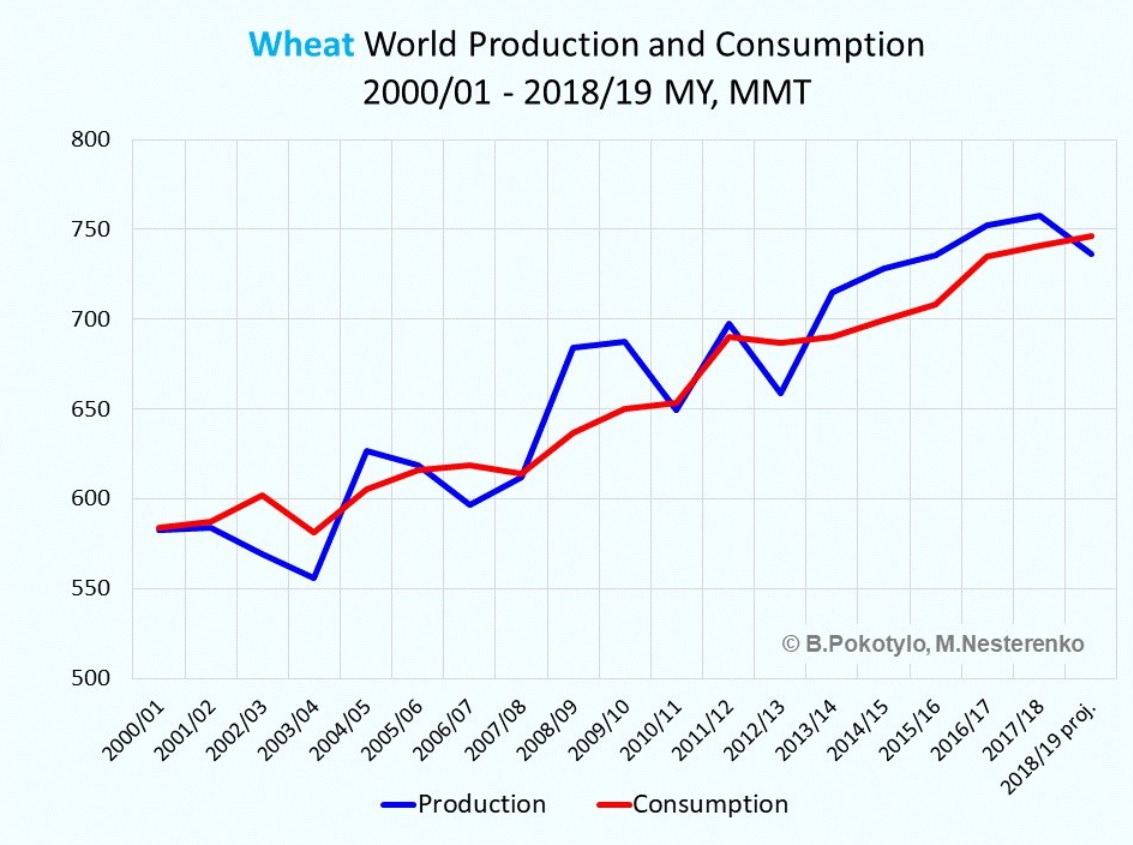

Wheat – Global Production & Consumption

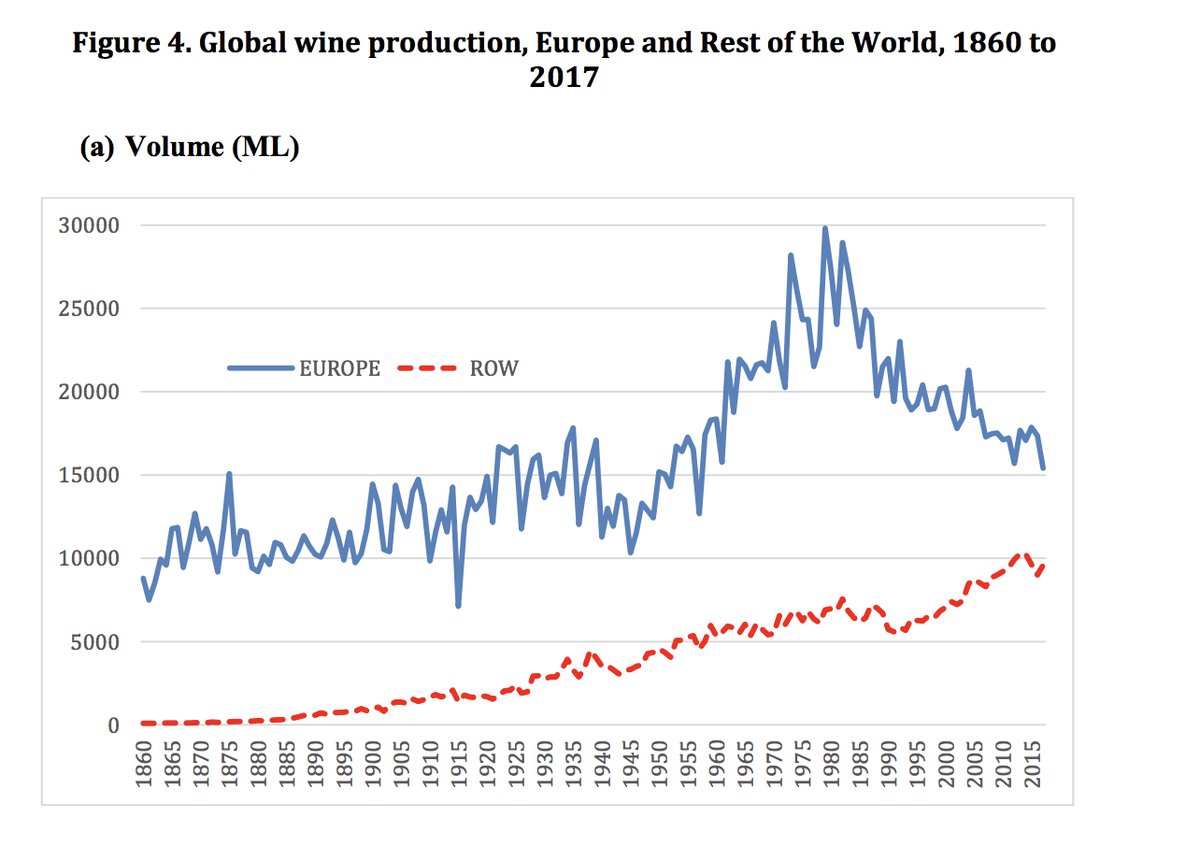

Global Wine Production

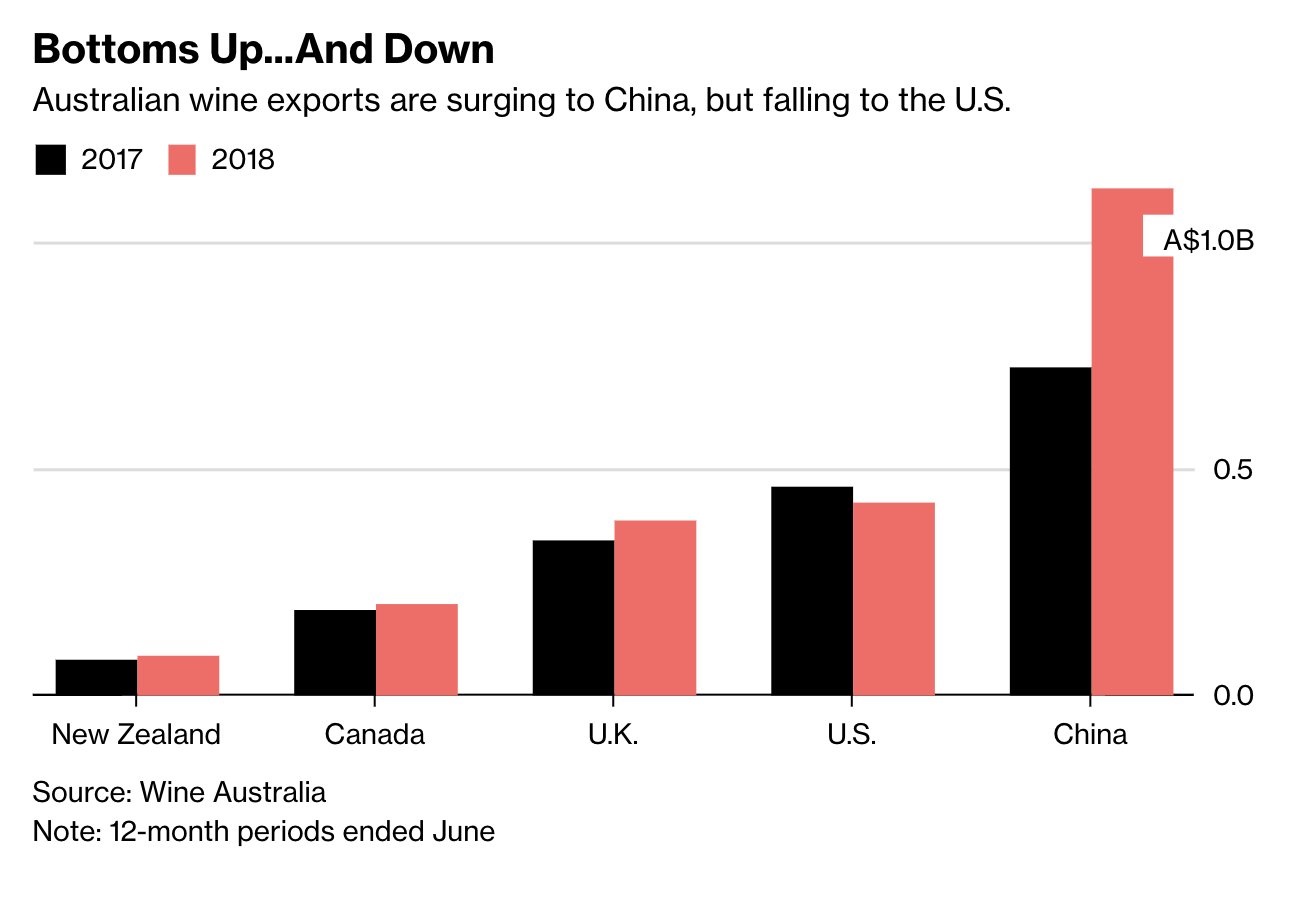

Australian Wine Exports

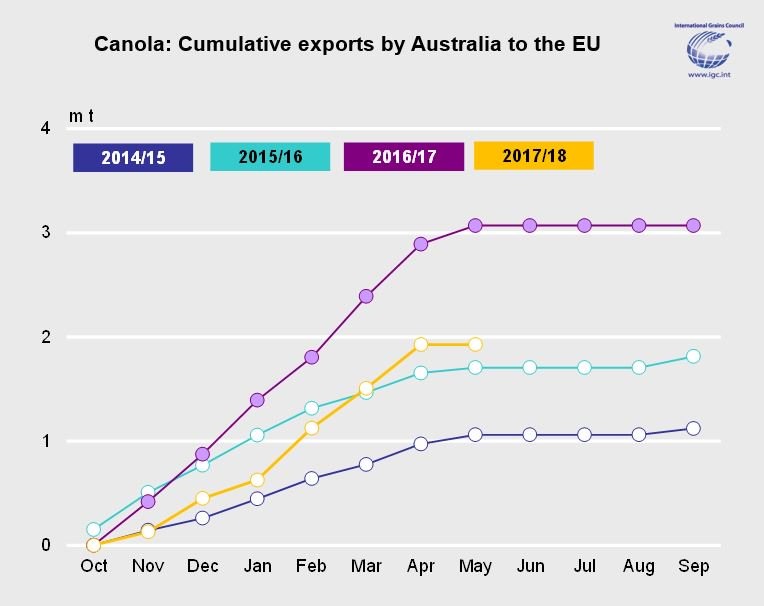

Canola – Australian Exports to EU

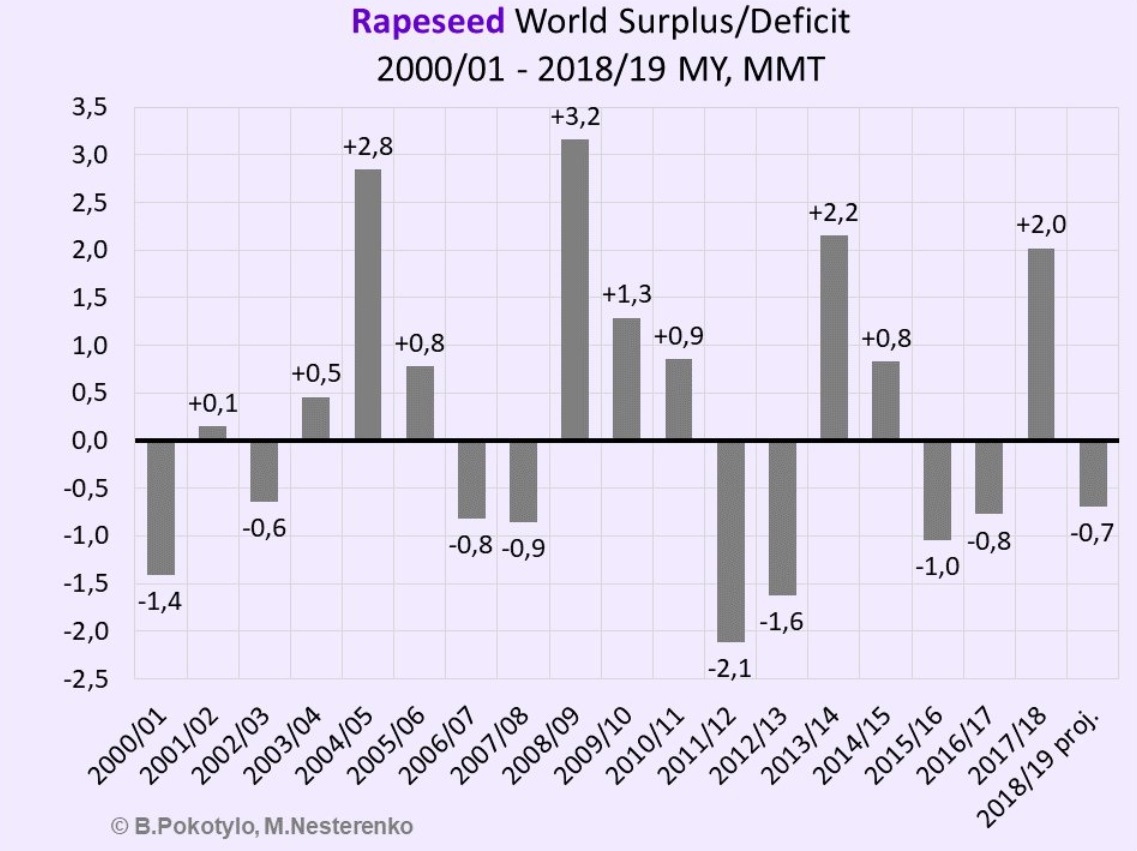

Rapeseed – Global Balance

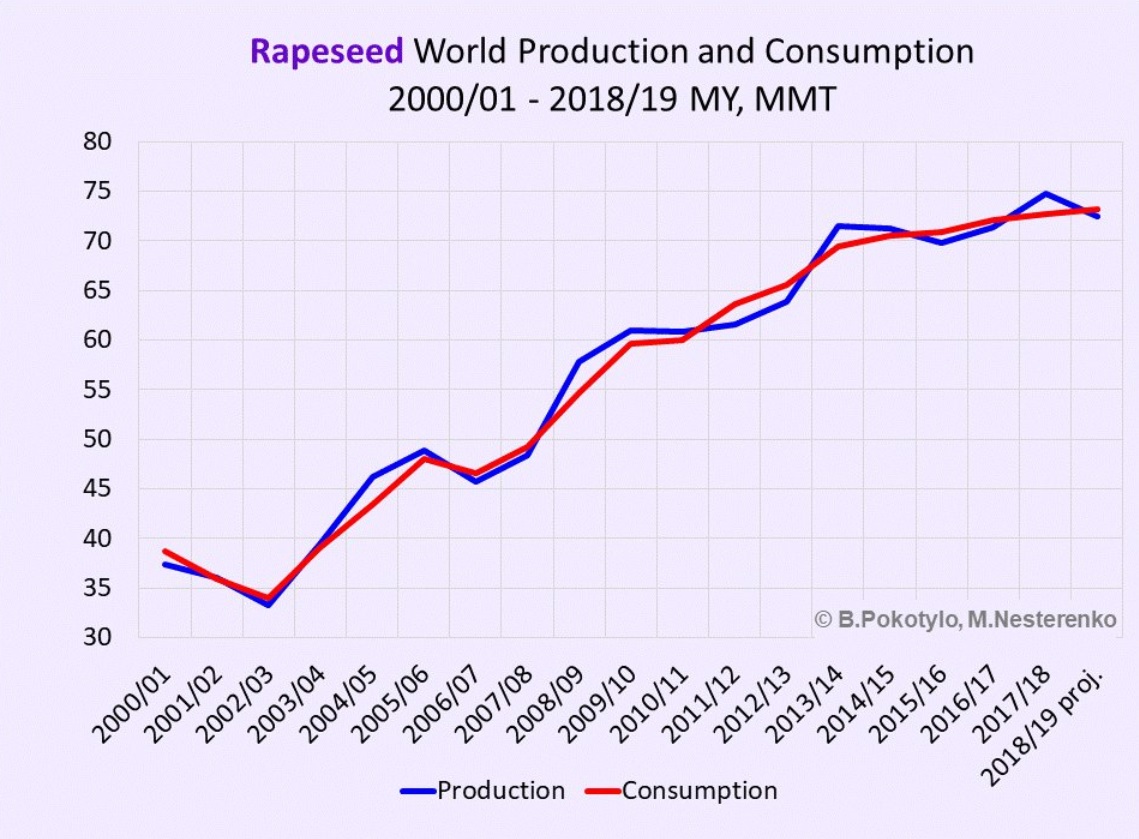

Rapeseed Global Production & Consumption

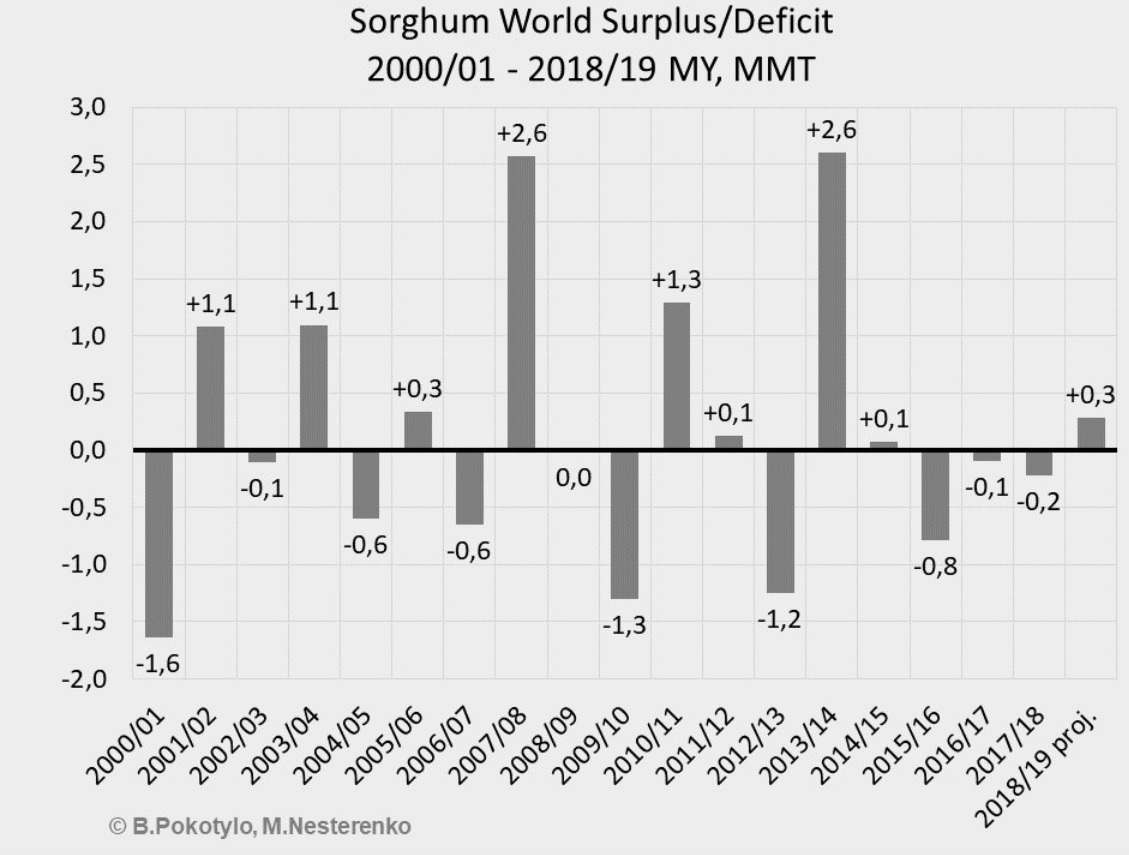

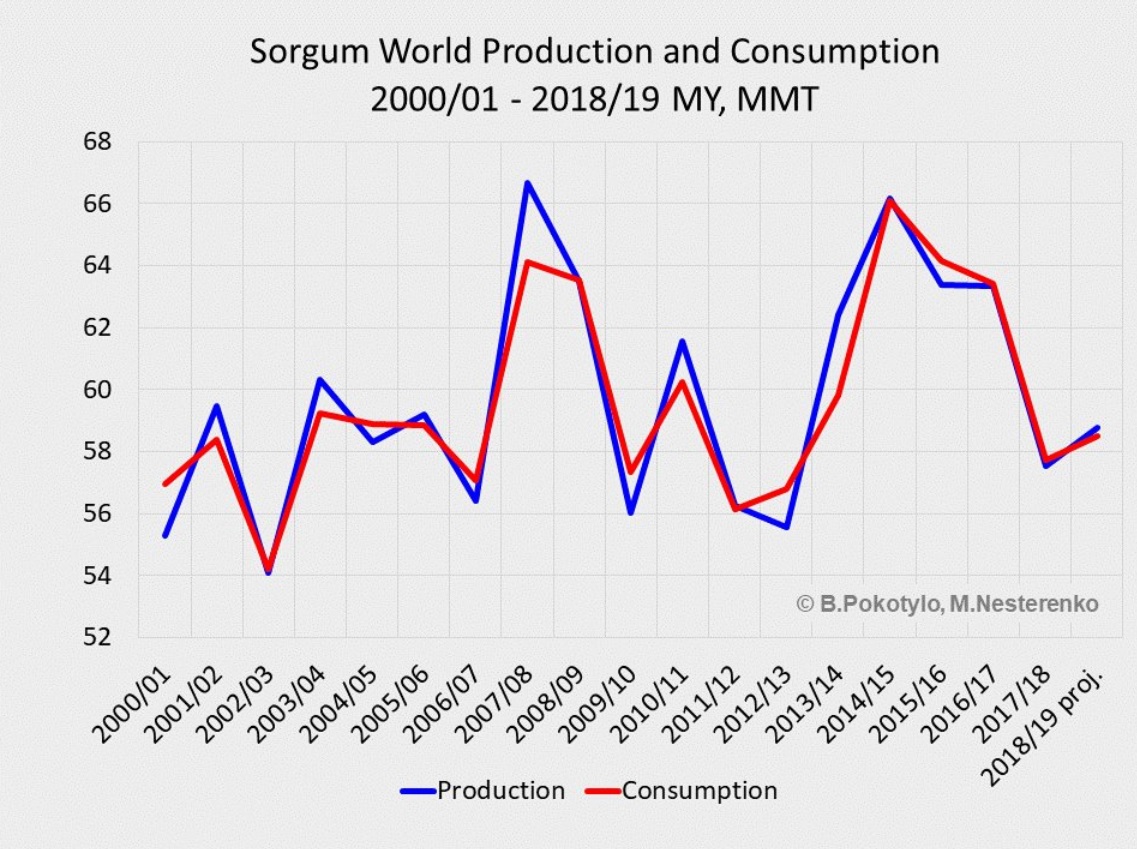

Sorghum – Global Balance

Sorghum Global Production & Consumption

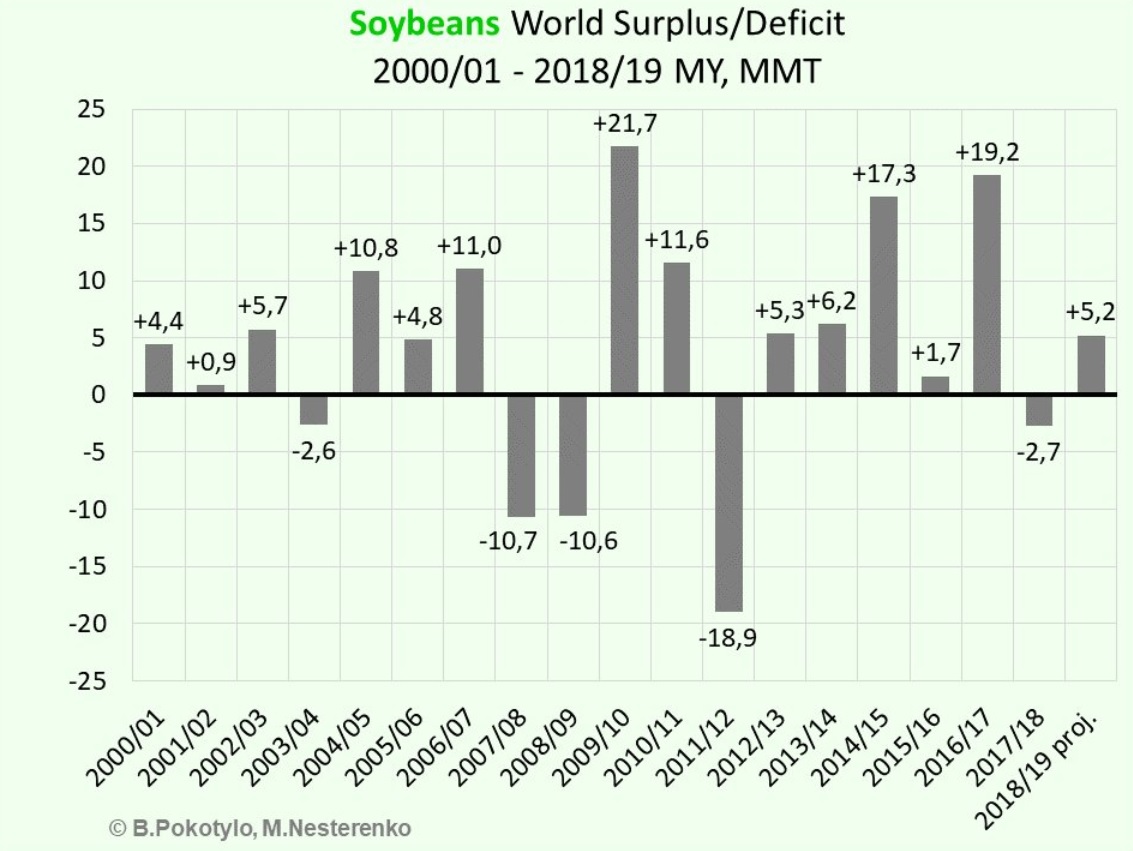

Soybeans – Global Balance

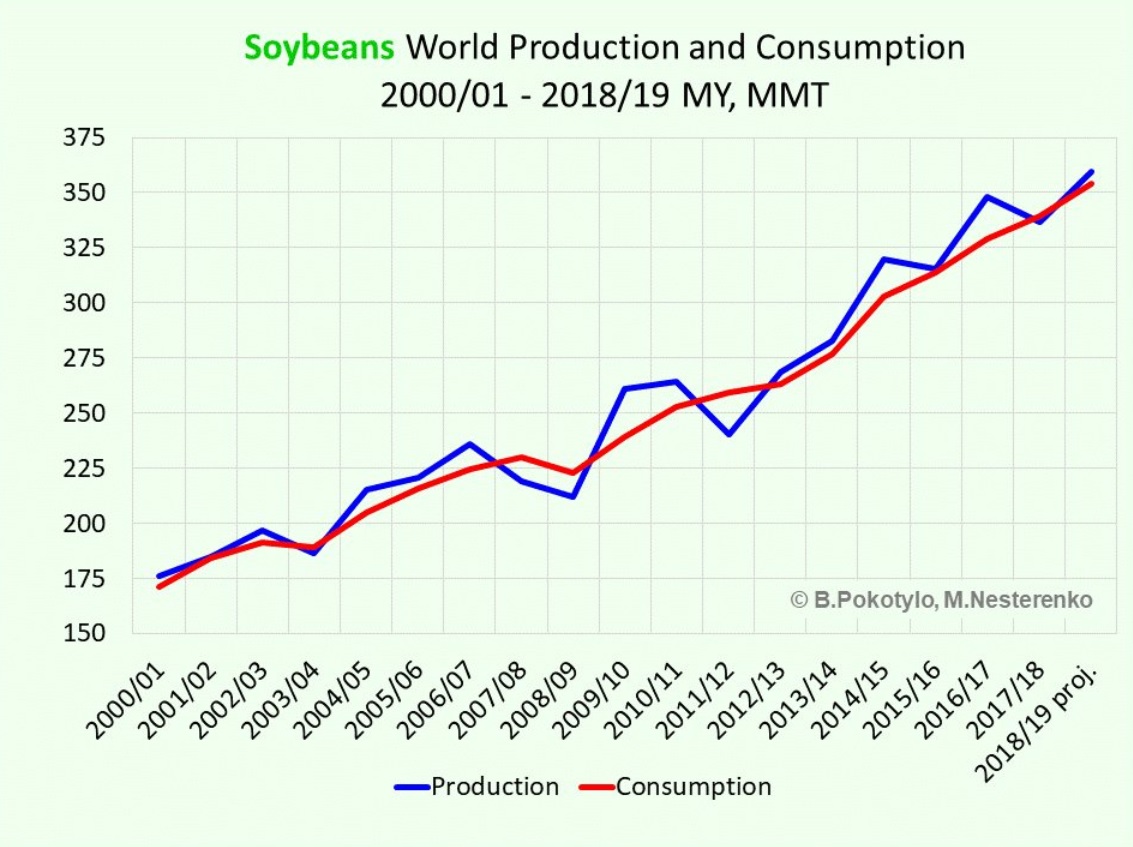

Soybeans – Global Production & Consumption

Capital Markets

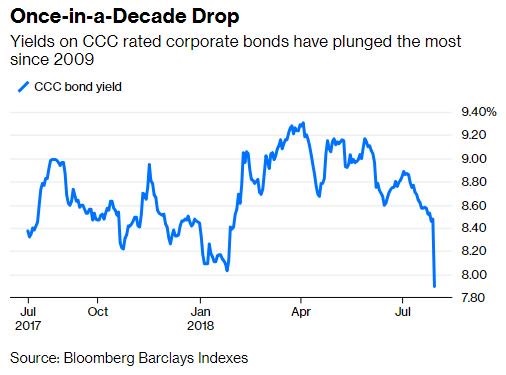

CCC Rated Yields

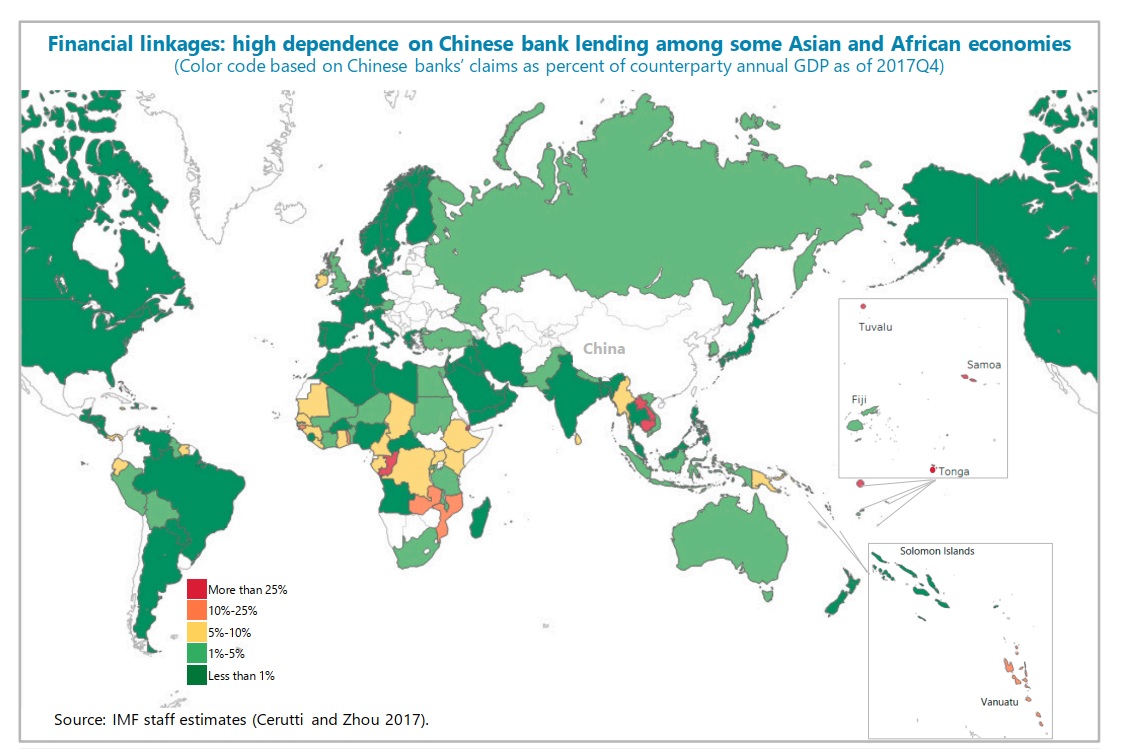

Finance System Dependence on China

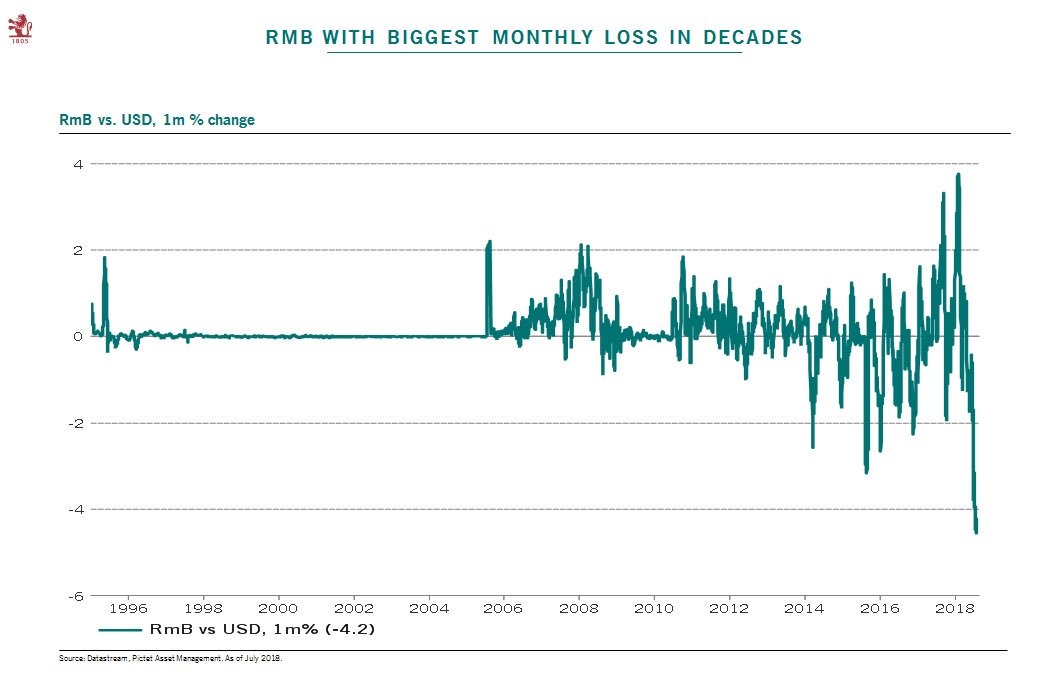

RMB to USD

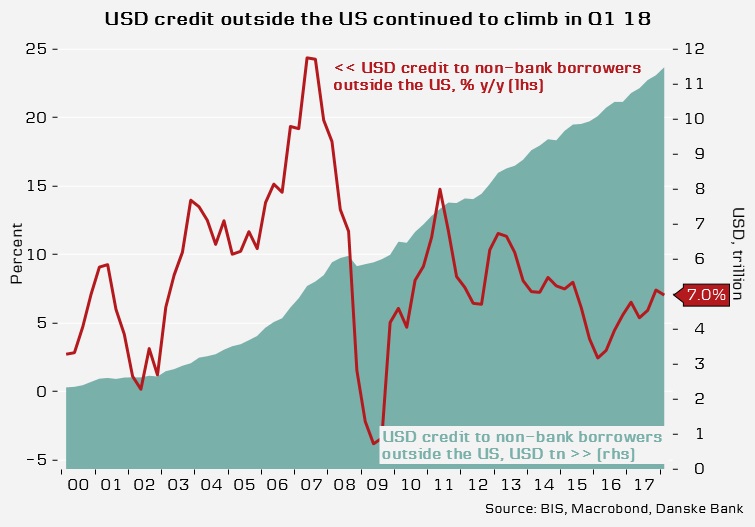

United States Credit Outside the United States

Global Macro

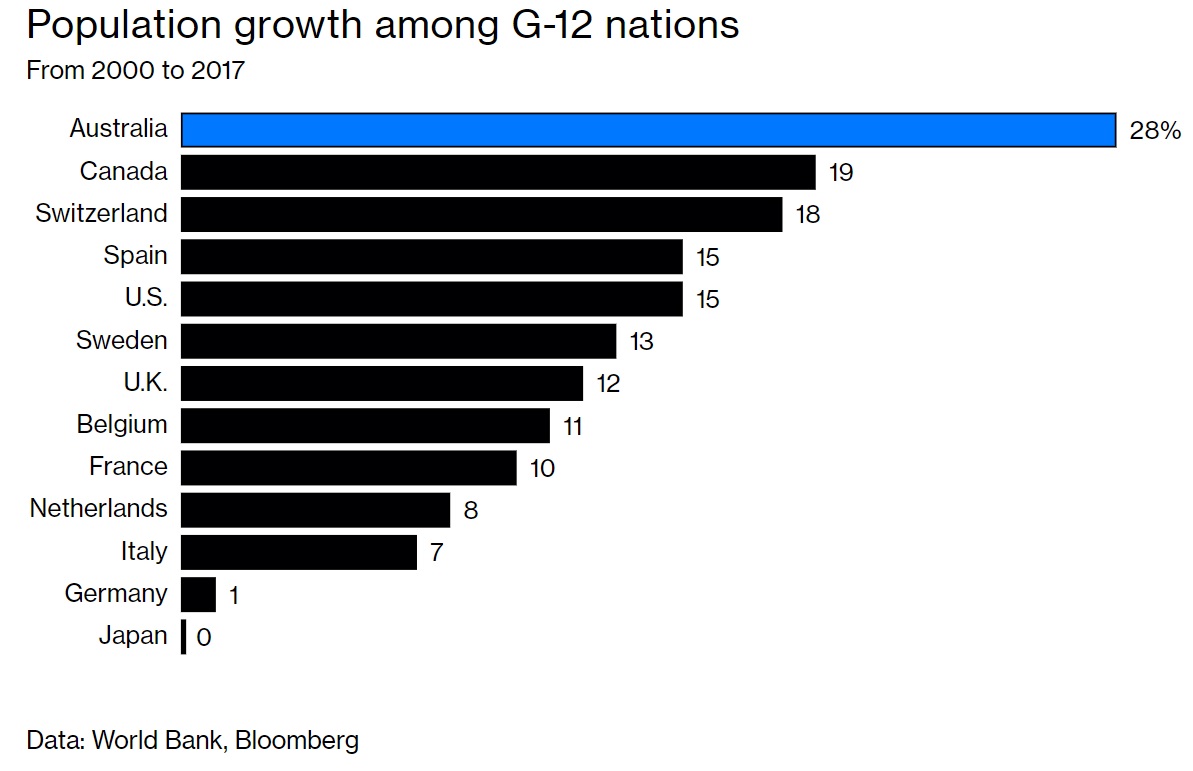

Population Growth – G12

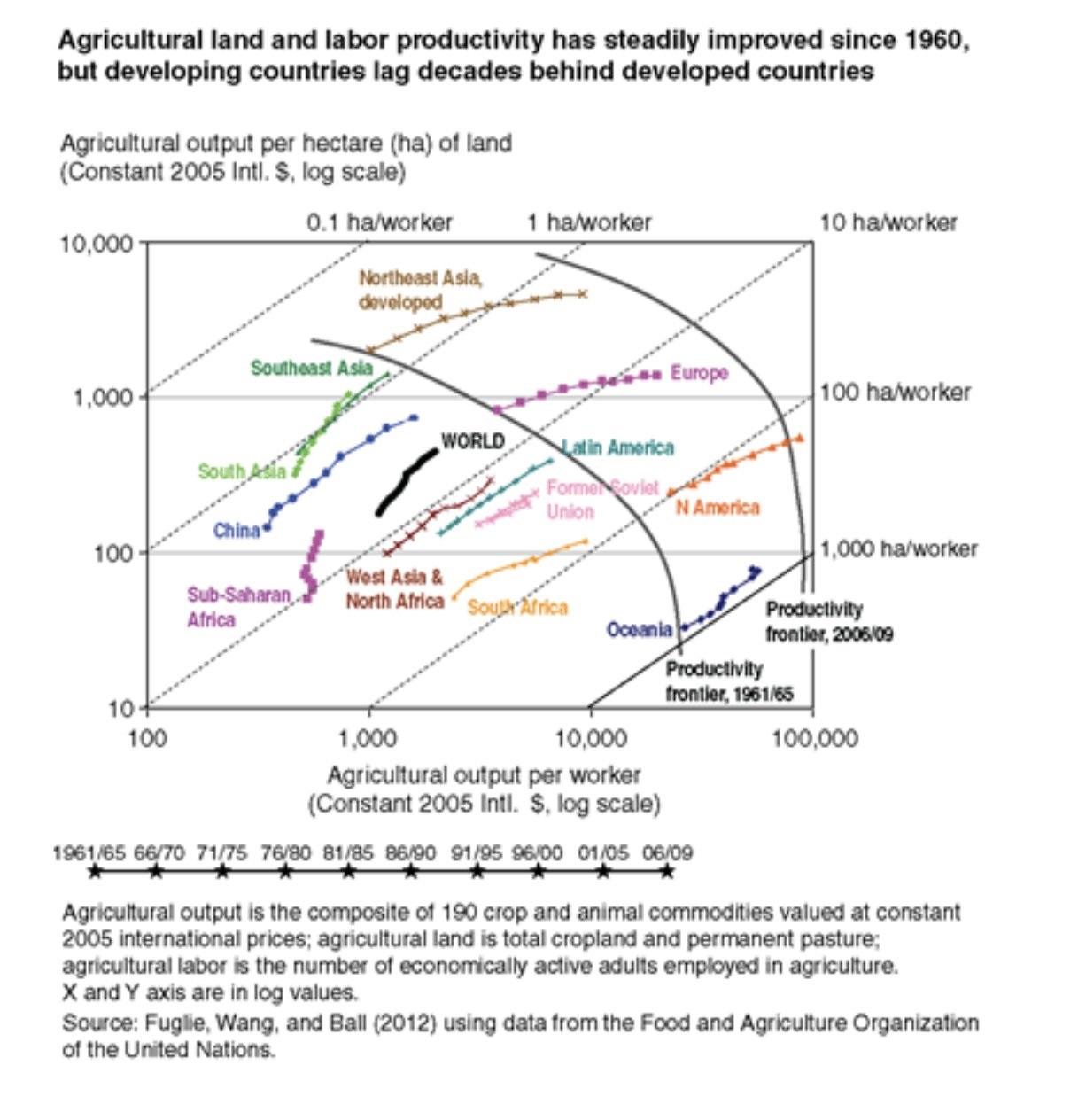

Agricultural Productivity

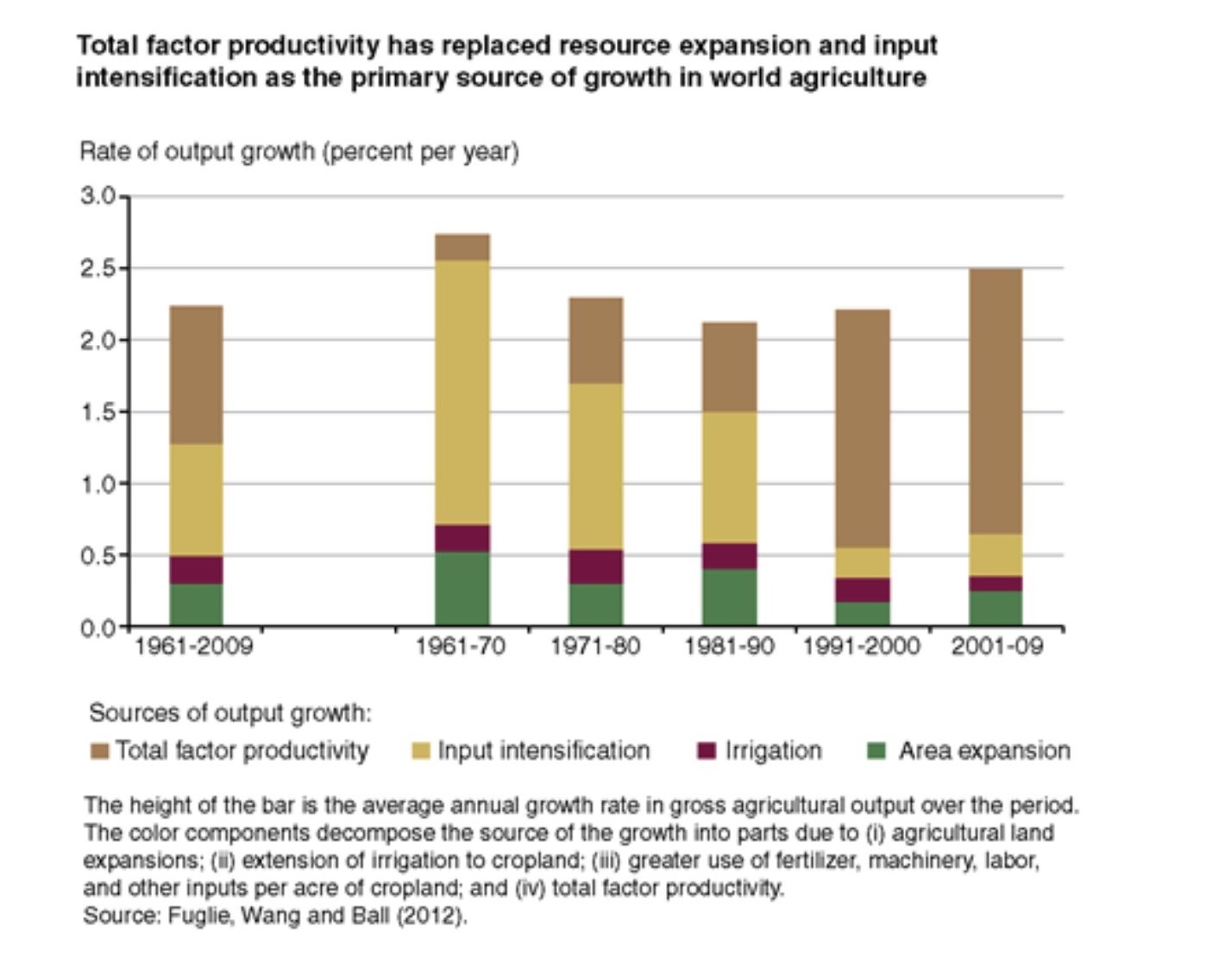

Global Agriculture – Total Factor Productivity

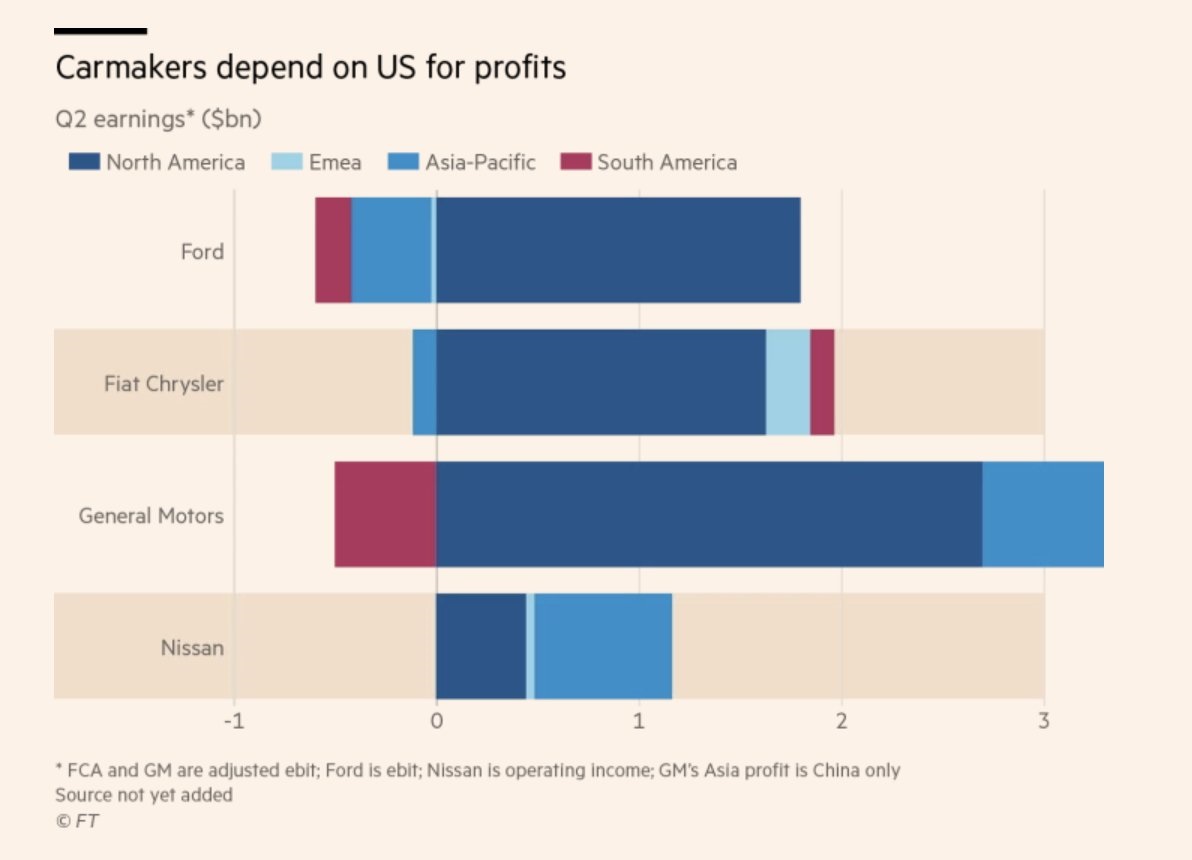

Carmaker profits – Regional Contribution

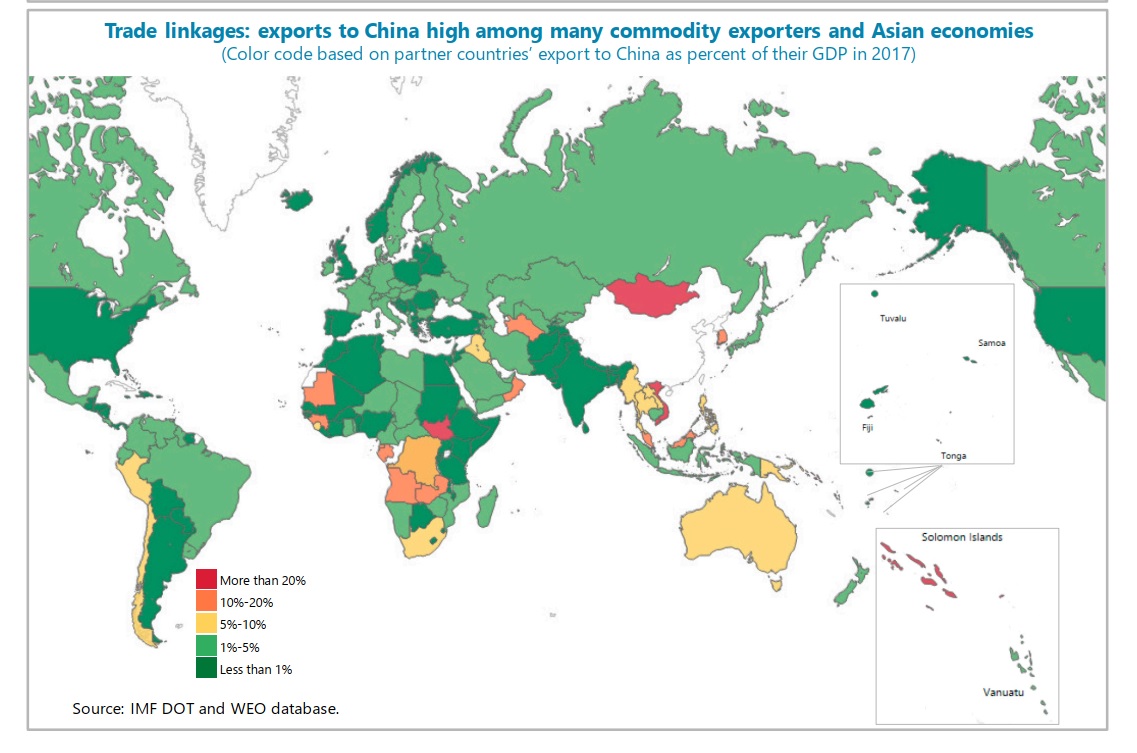

Trade Dependence on China

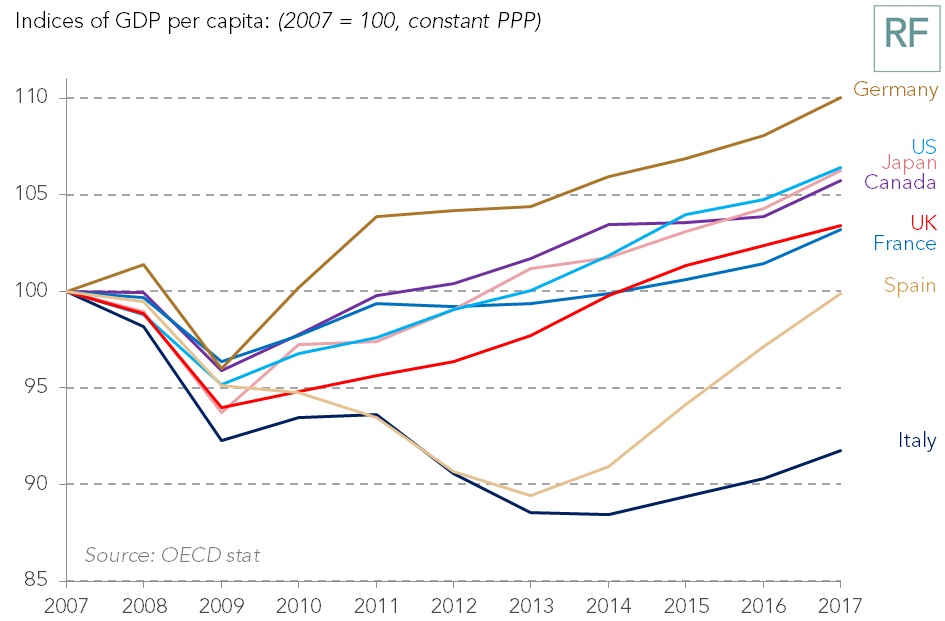

GDP Per Capita – Selected Nations

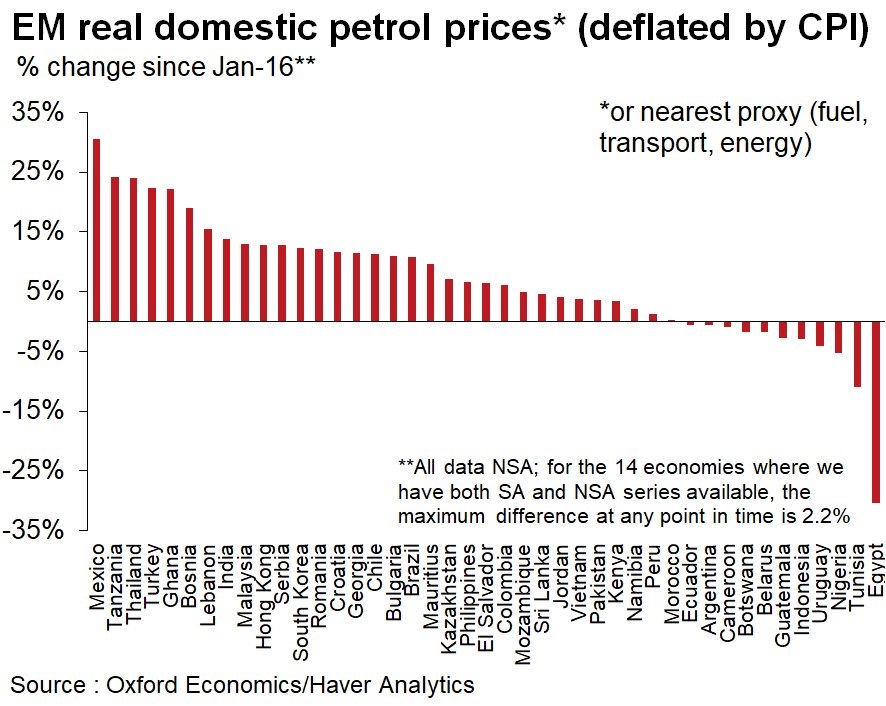

Emerging Market Domestic Petrol Prices since Jan 2016

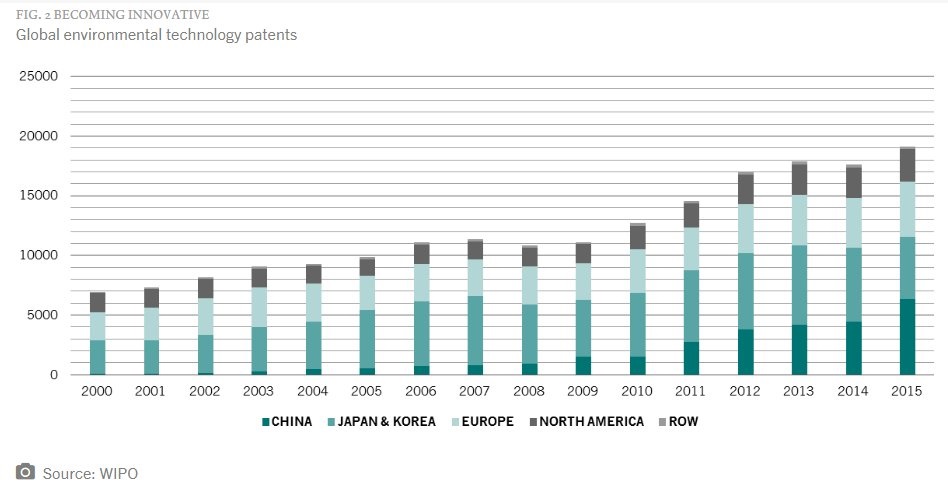

Global Environmental Technology Patents

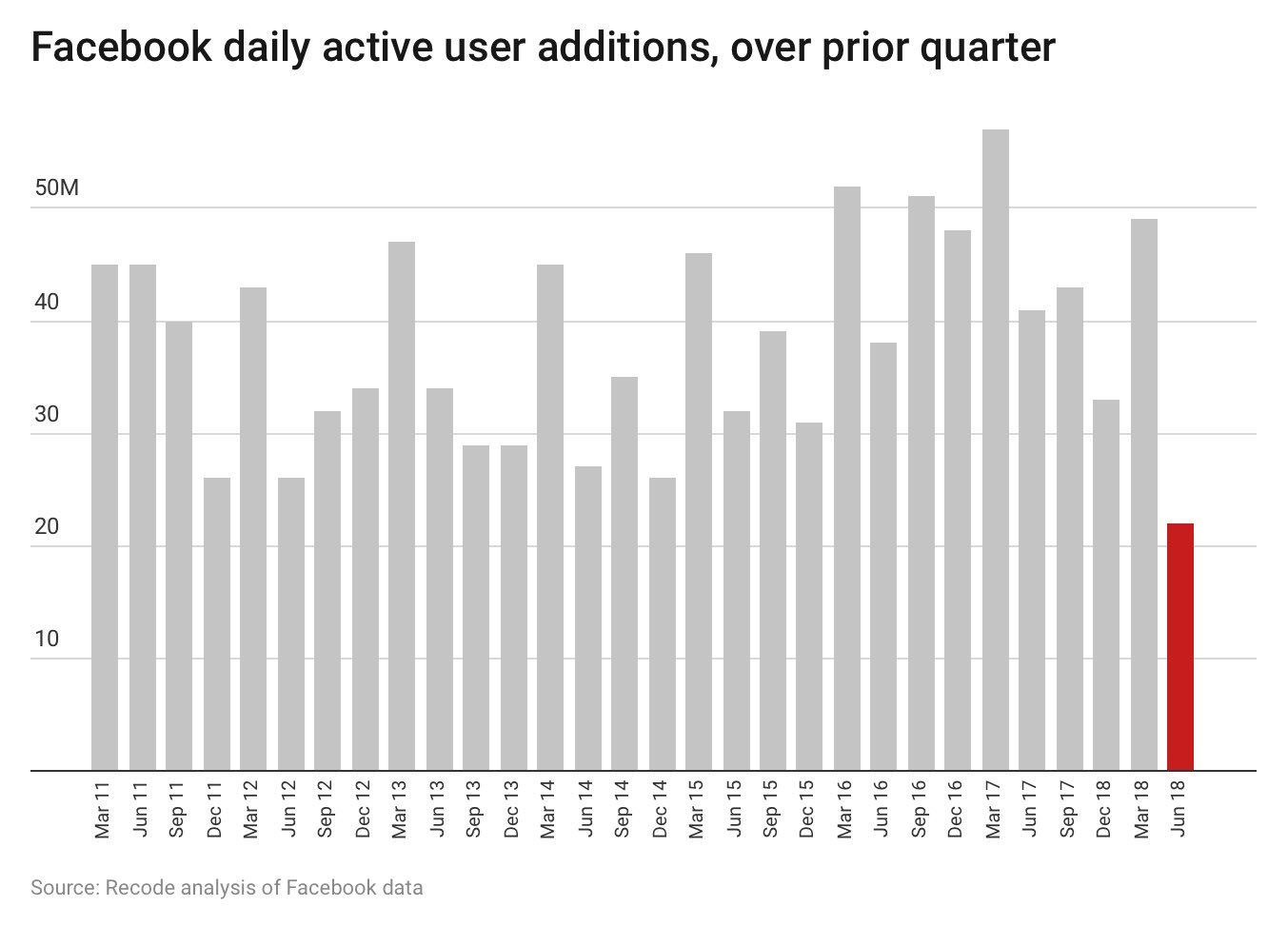

Facebook New Users

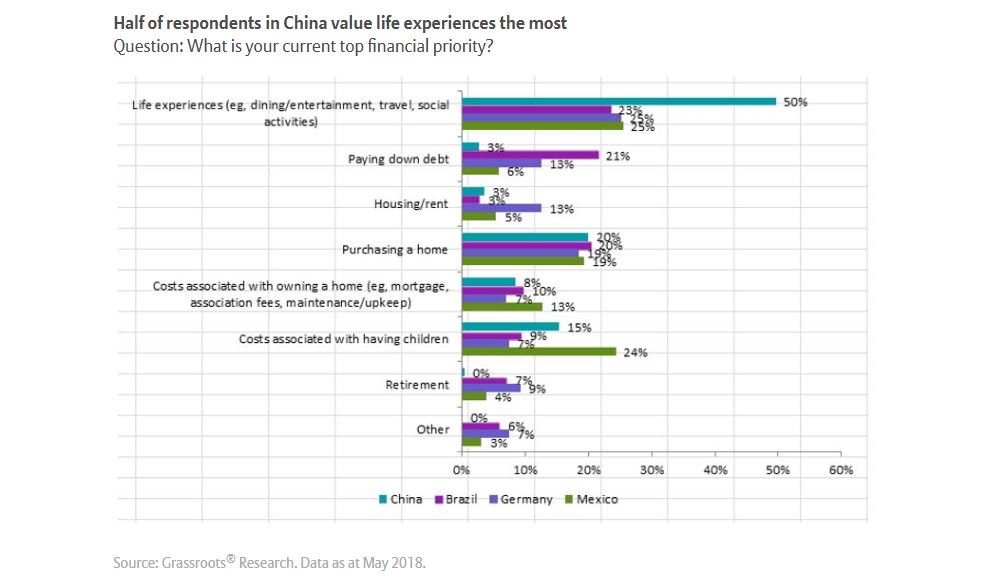

Financial Priorities – Selected Nations

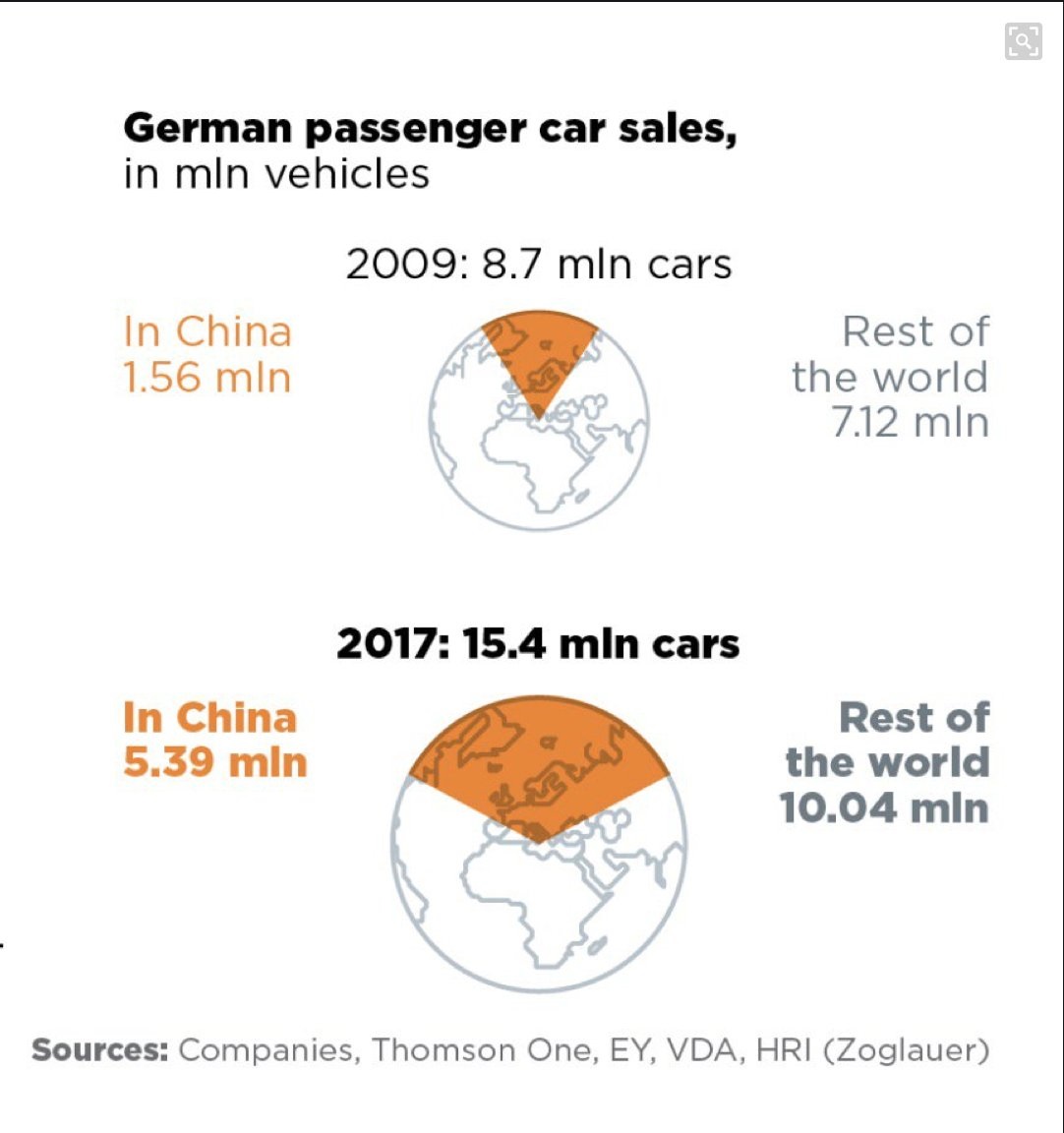

German Car Sales in China

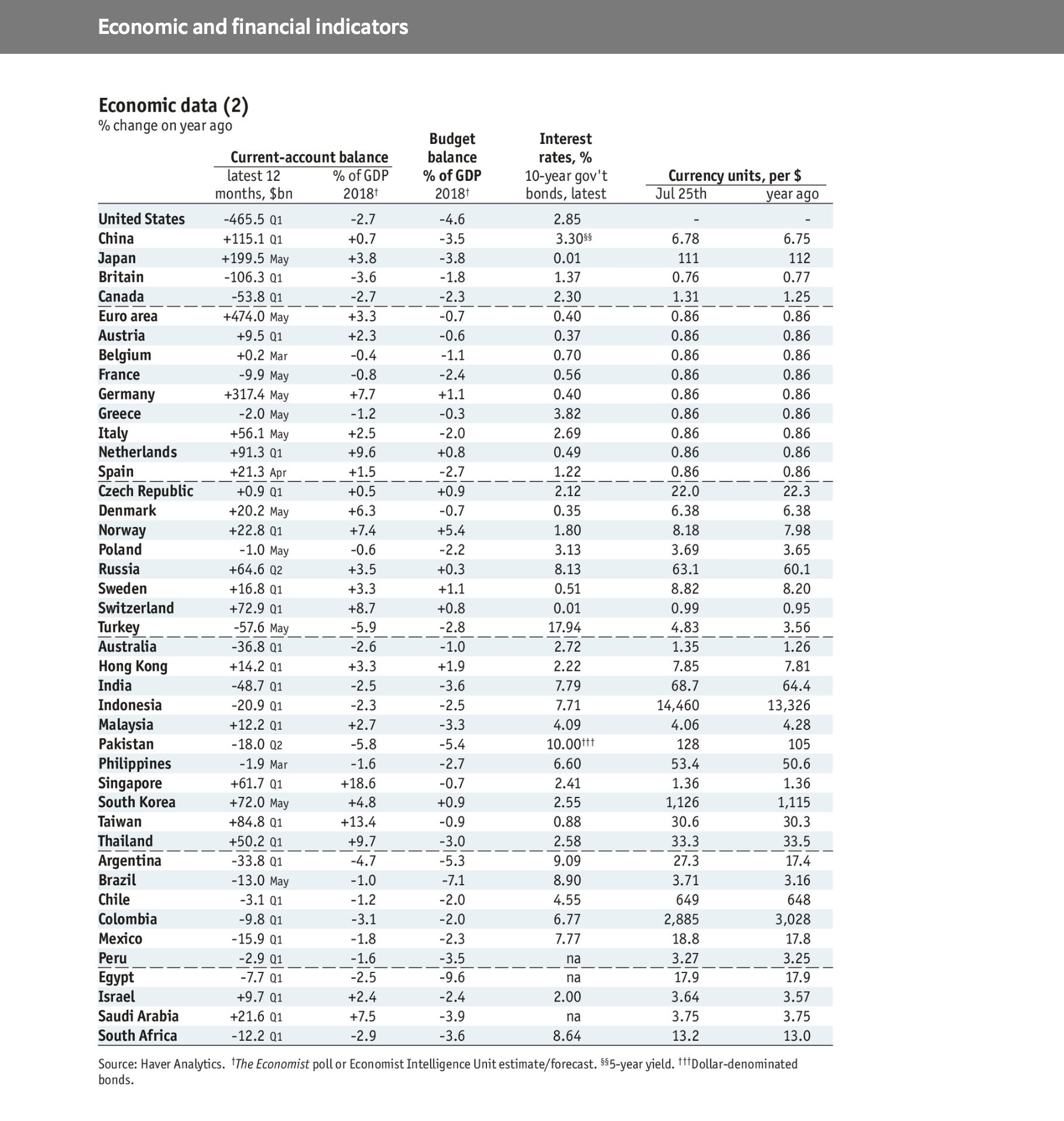

Major OECD – Current Account, Budget Balance, Interest Rates, Currency

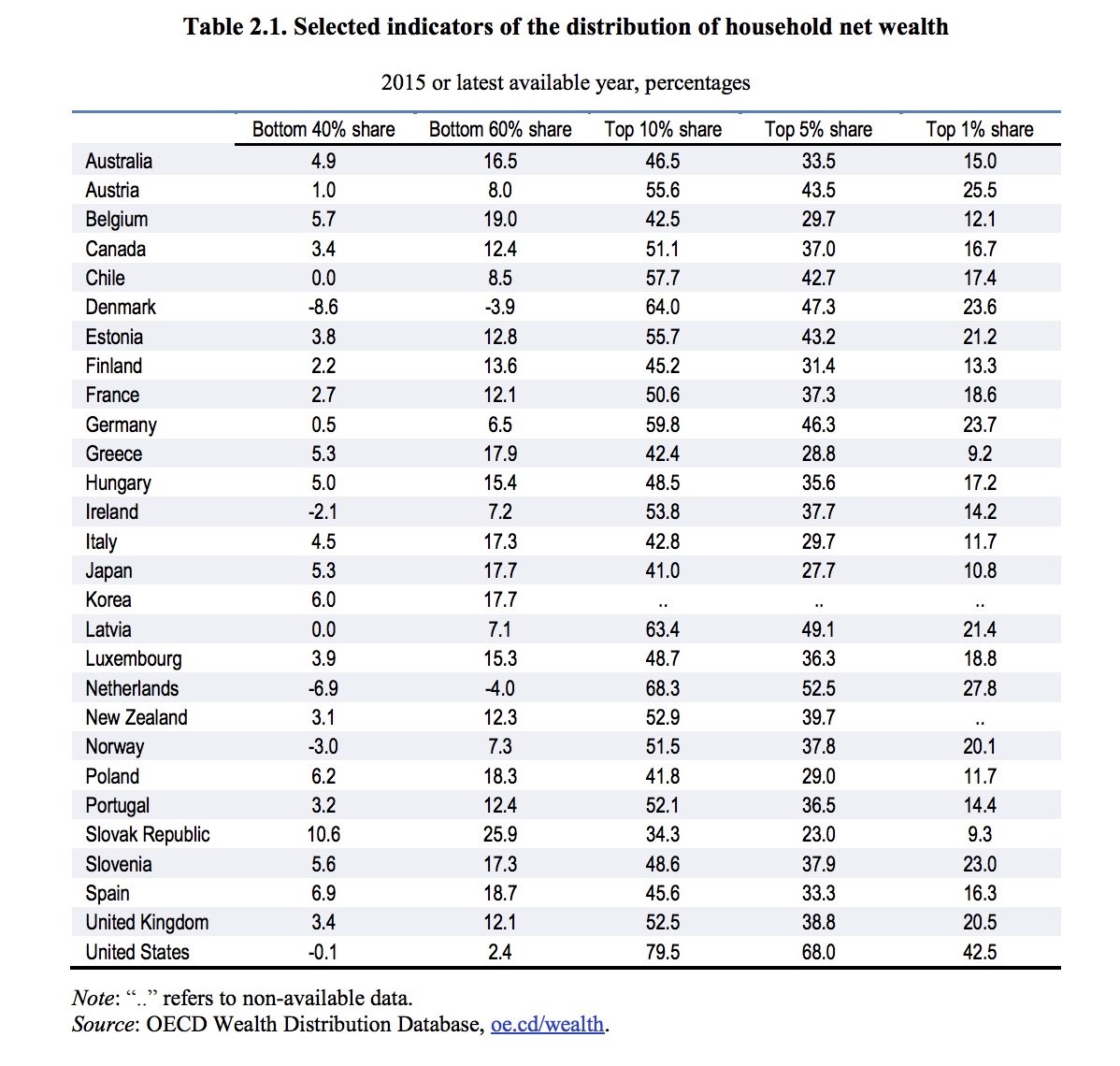

Major OECD Wealth Distribution

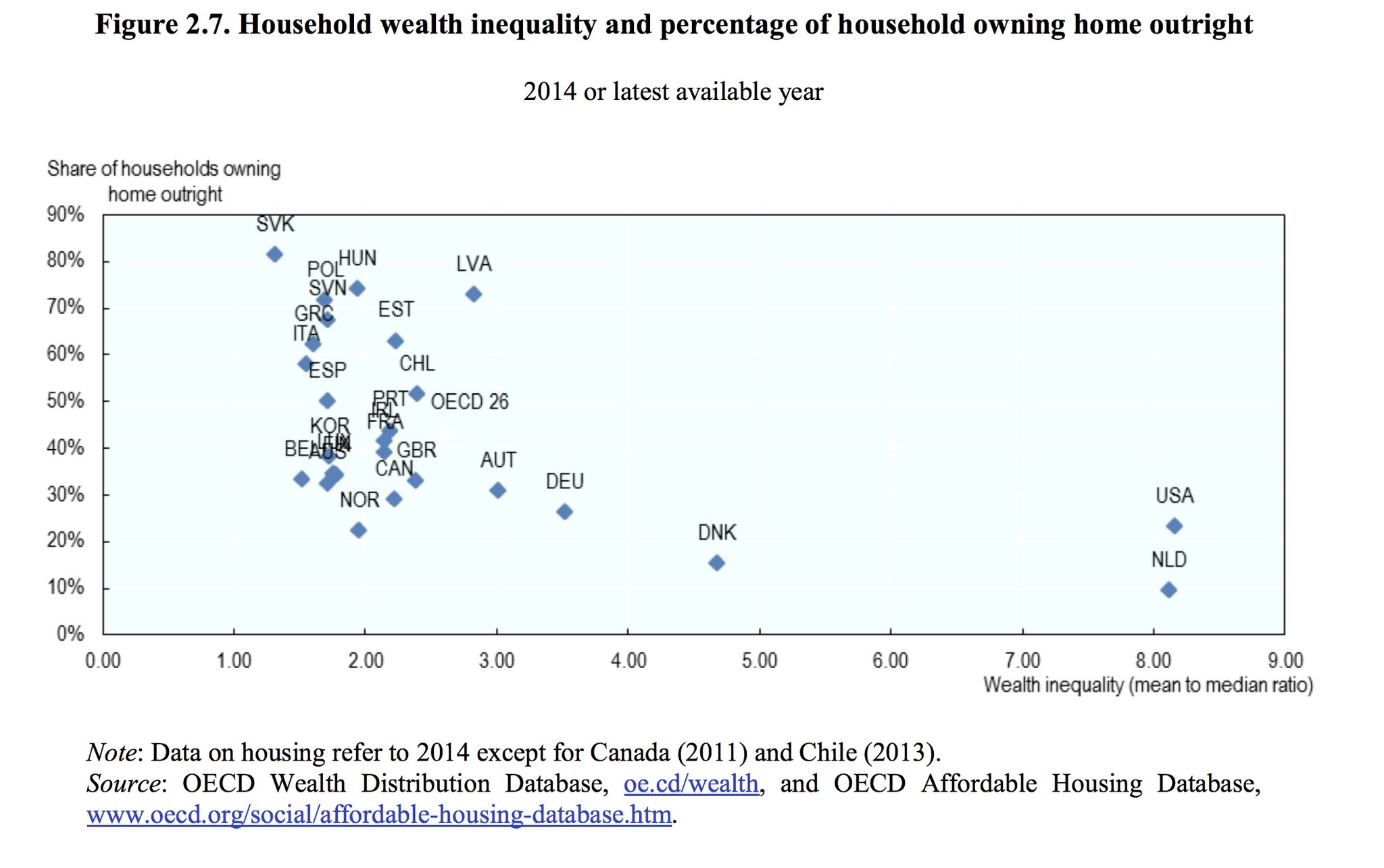

OECD – Household Wealth & Outright Home Ownership

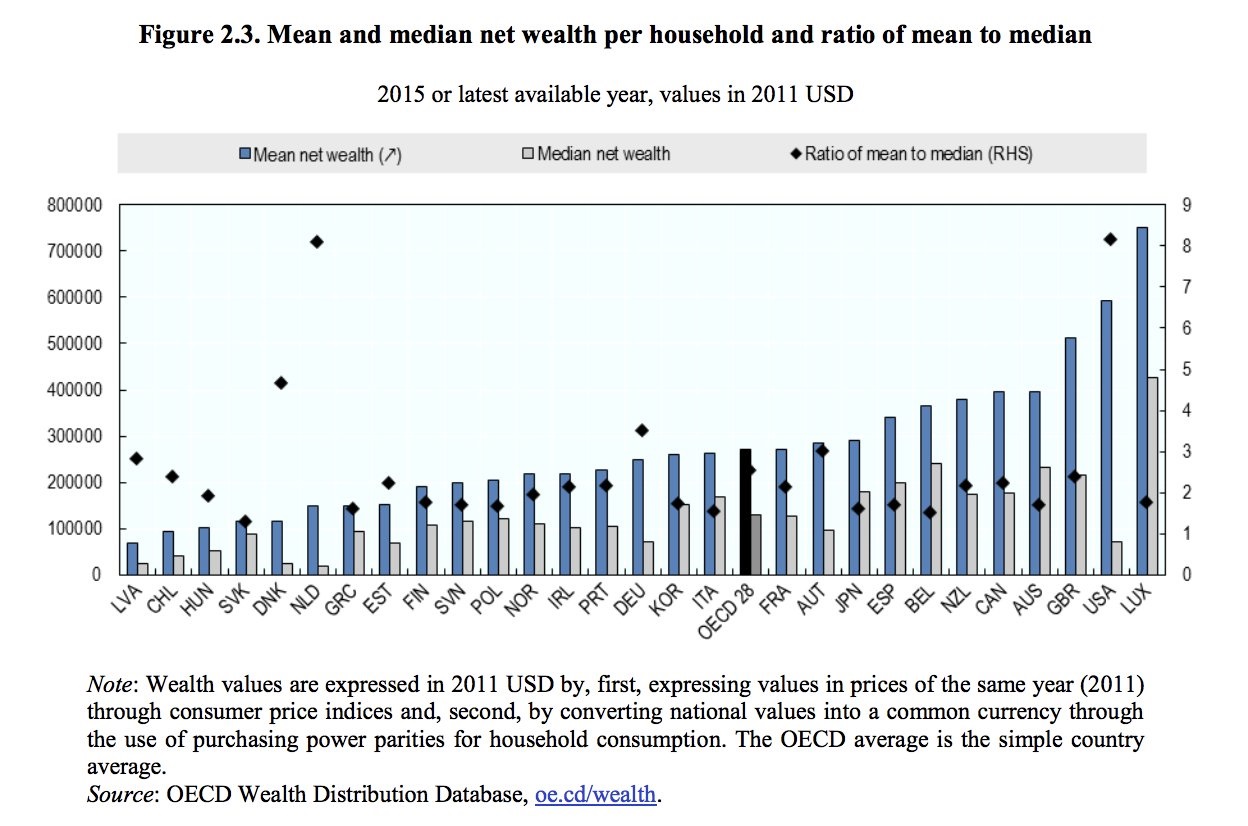

OECD – Mean & Median Net Wealth

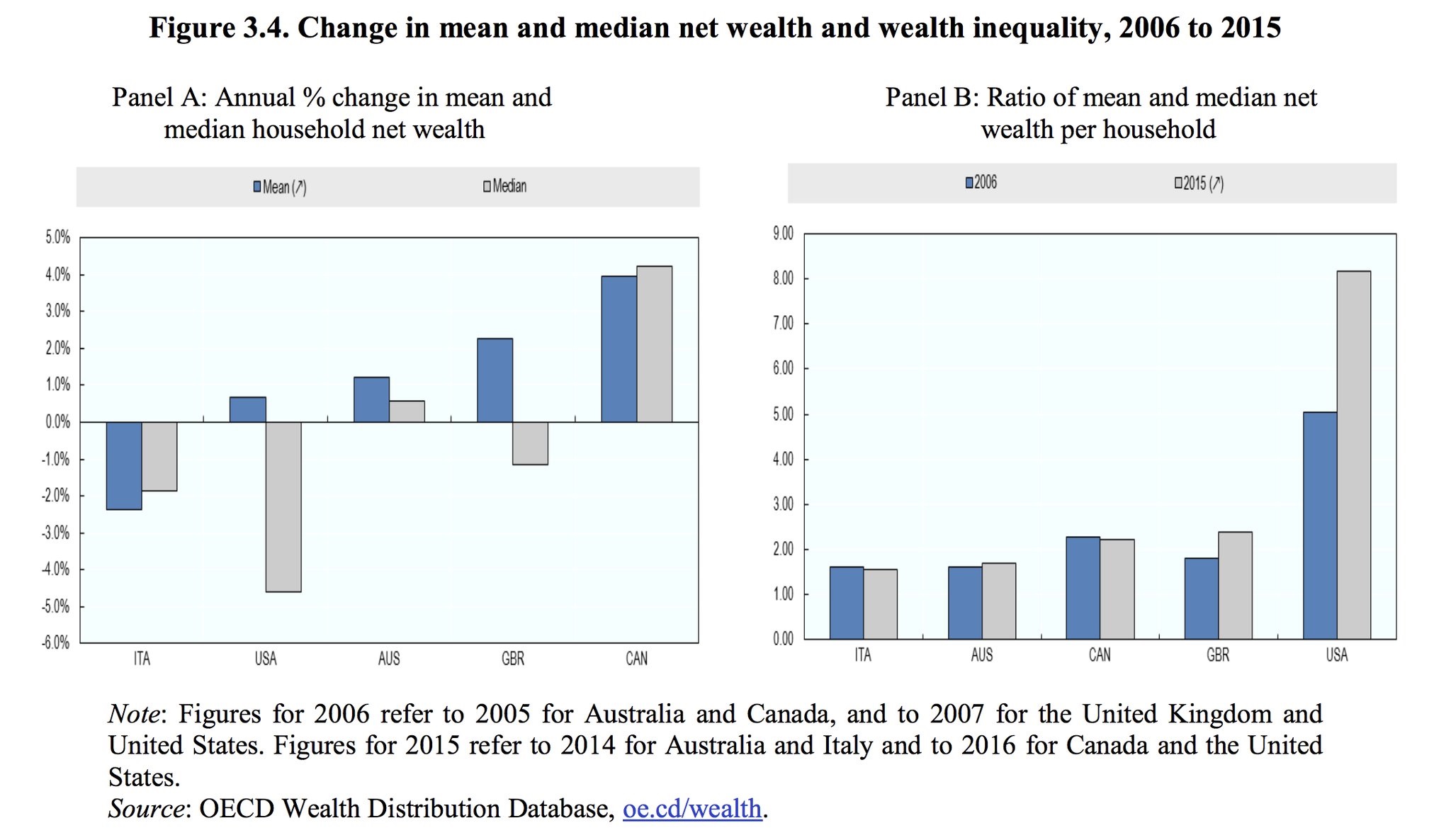

OECD – Changes in Mean & Median Net Wealth, Wealth Inequality 2006 – 2015

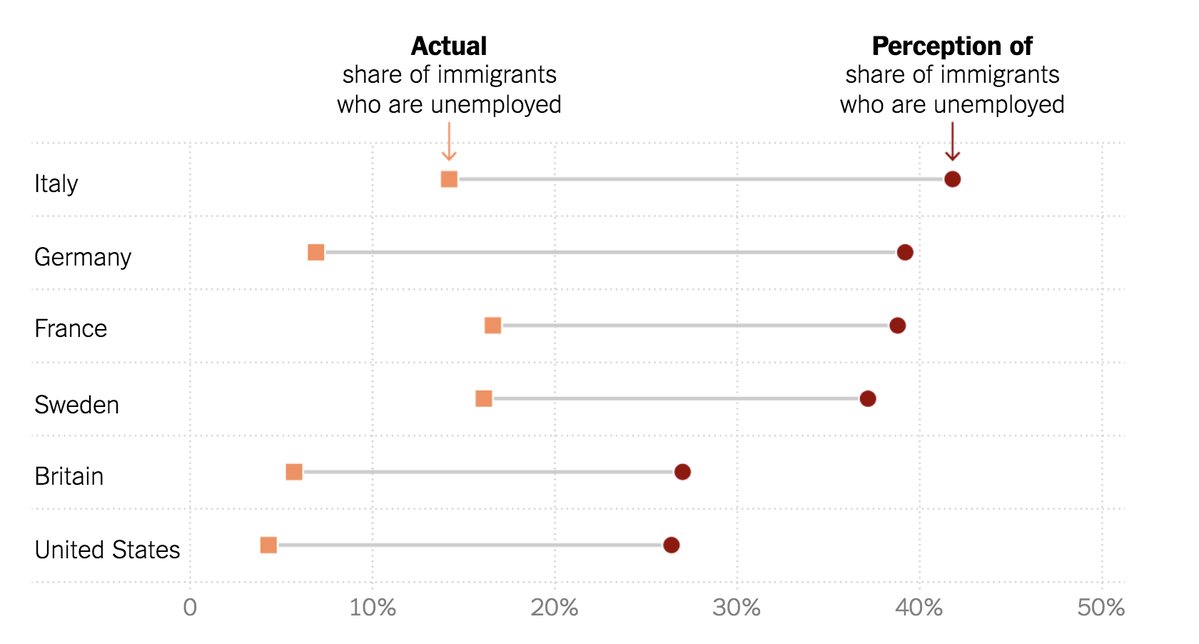

Selected Nations – Actual and Perceptions of Migrant Unemployment

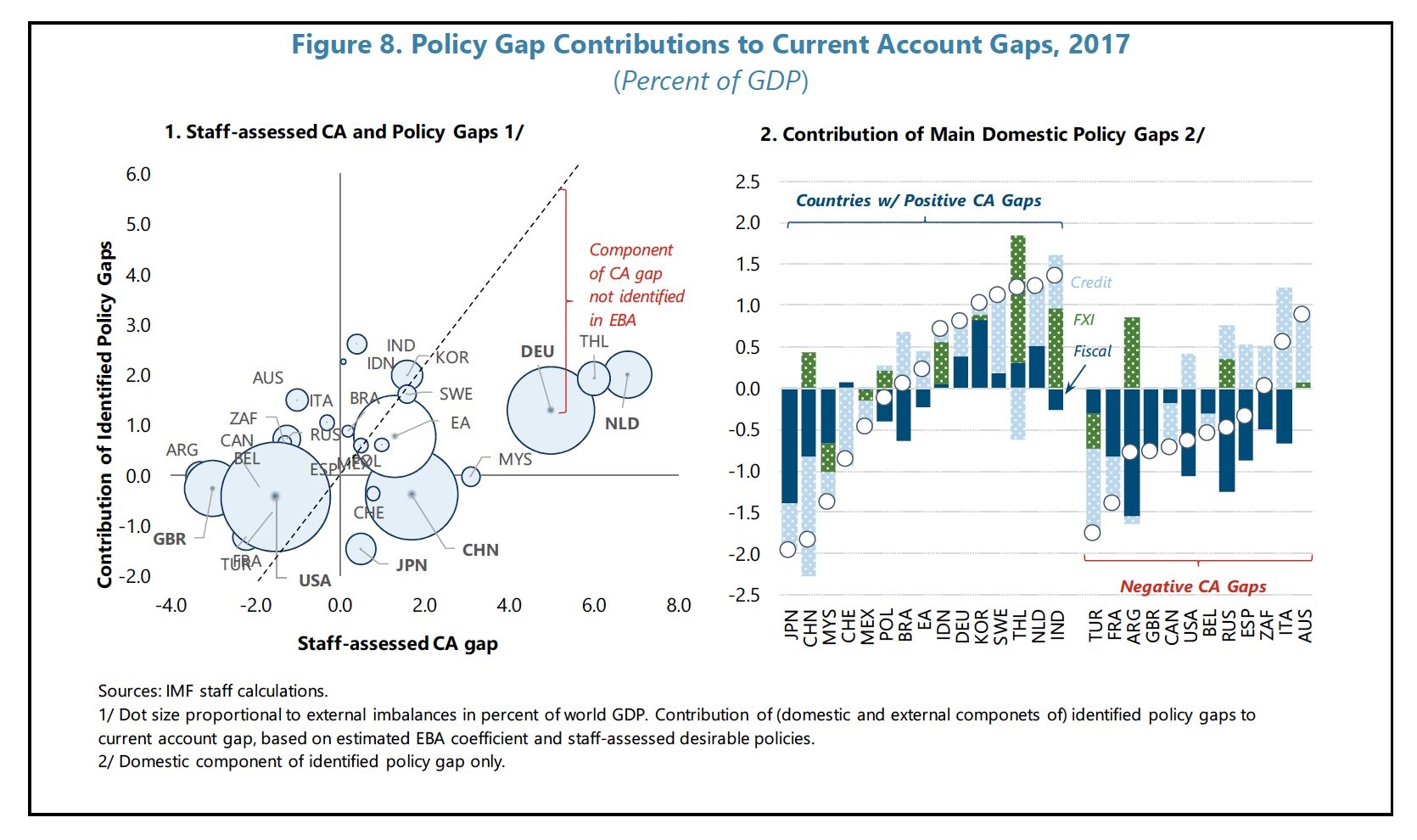

Selected Developed World Policy Gap & Current Accounts (note Australia)

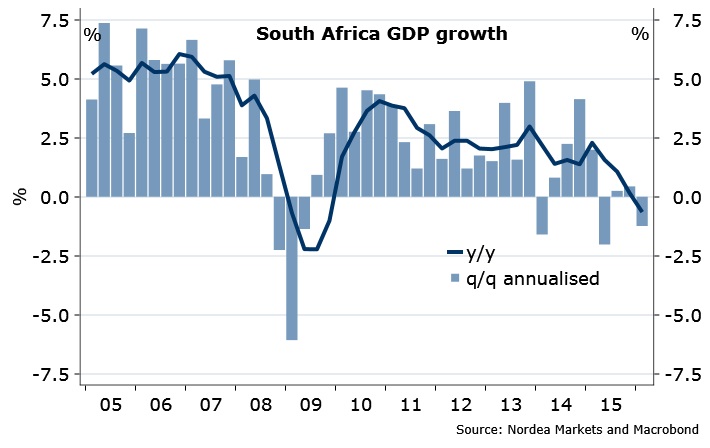

South Africa GDP

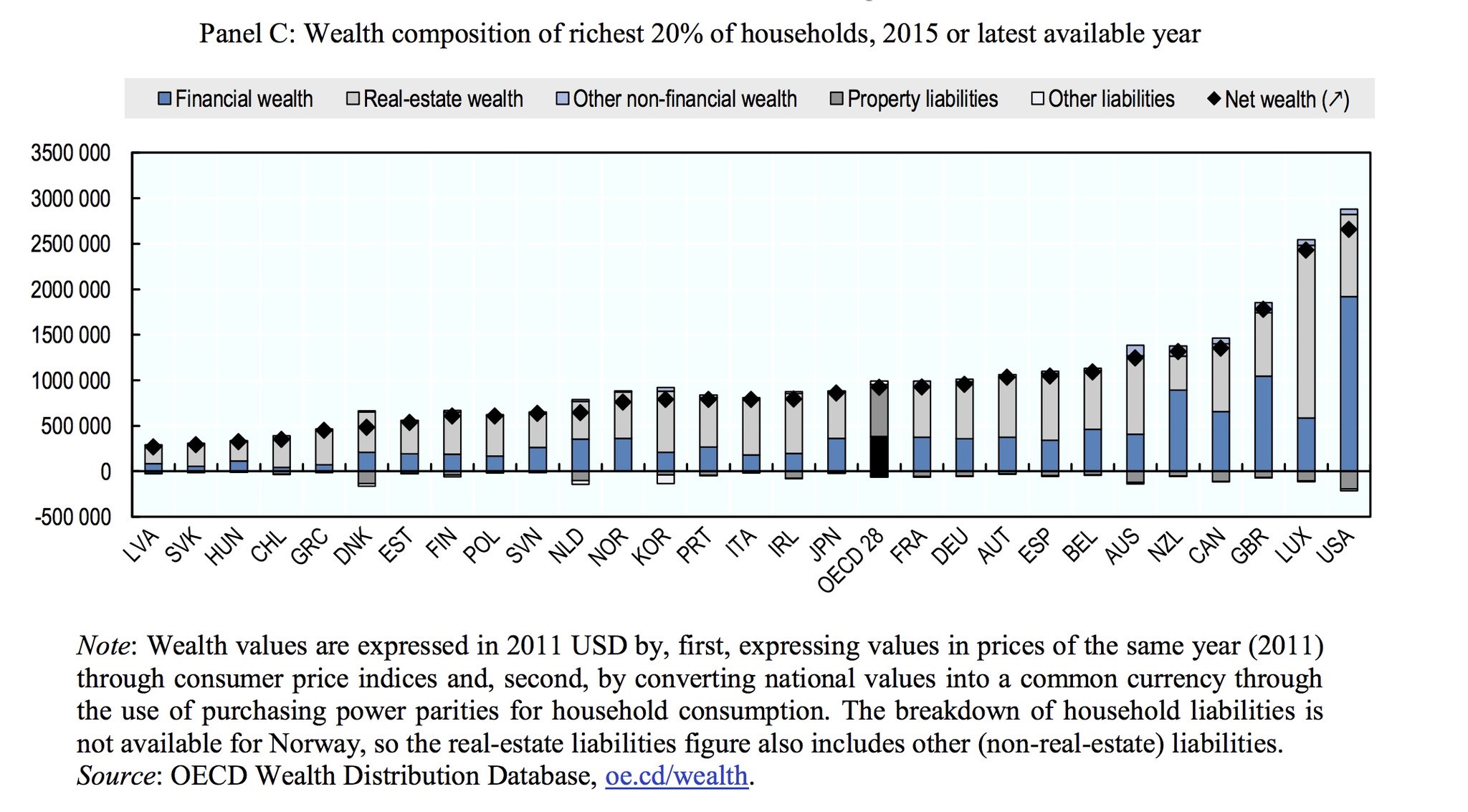

OECD – Wealth Composition of Richest 20% of Households

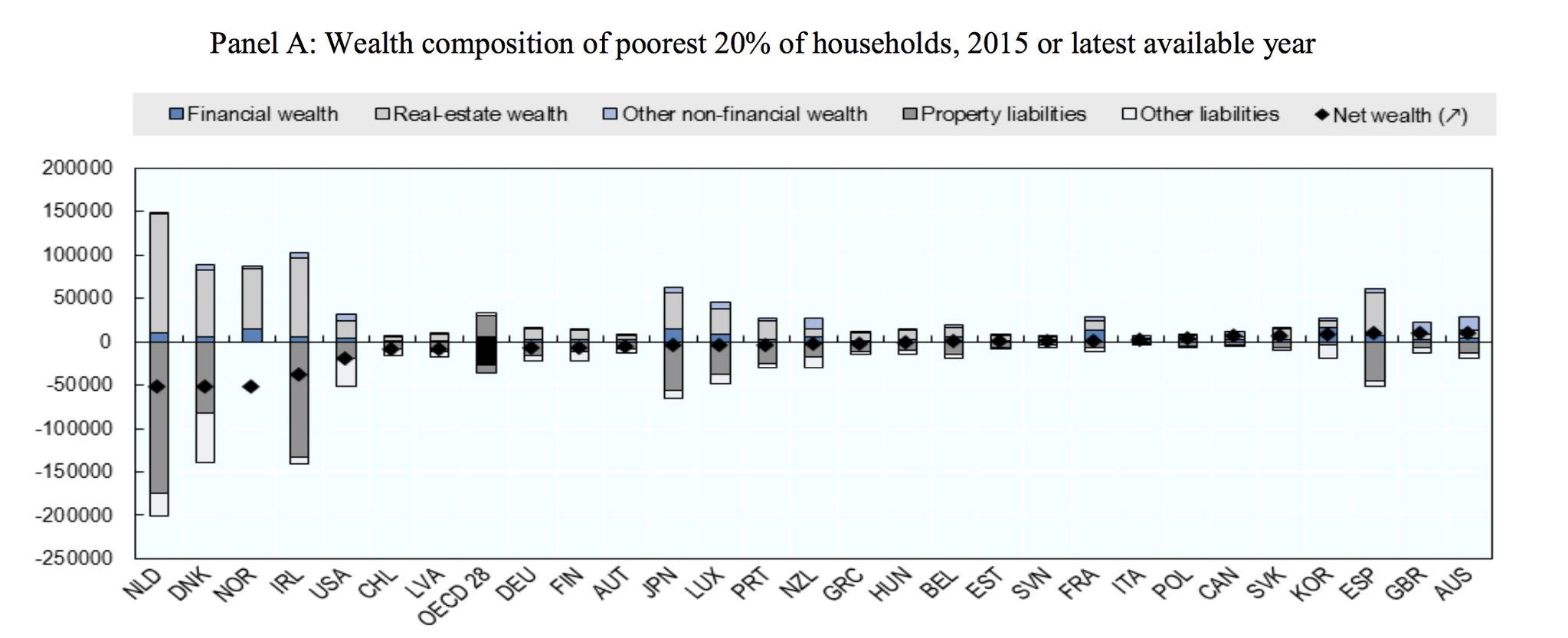

OECD – Wealth Composition of Poorest 20% of Households

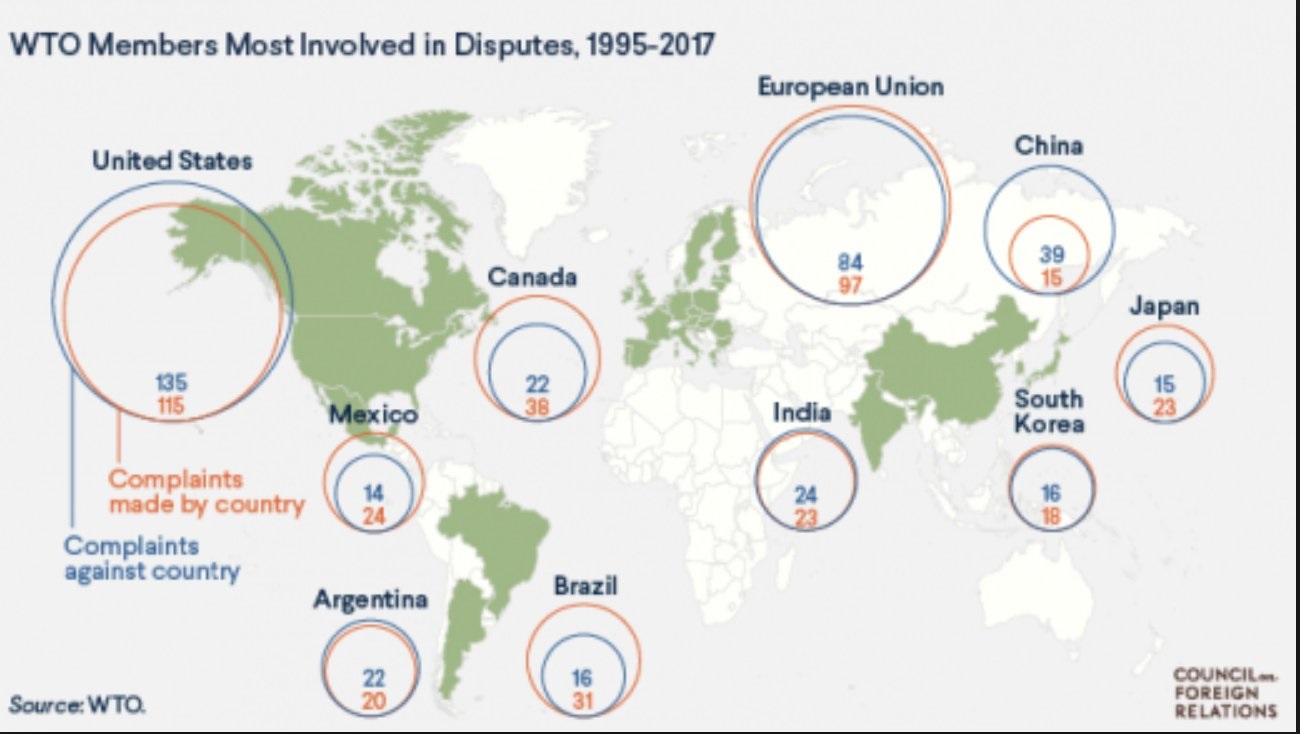

WTO Member Disputes 1995 – 2017

…and Furthermore…

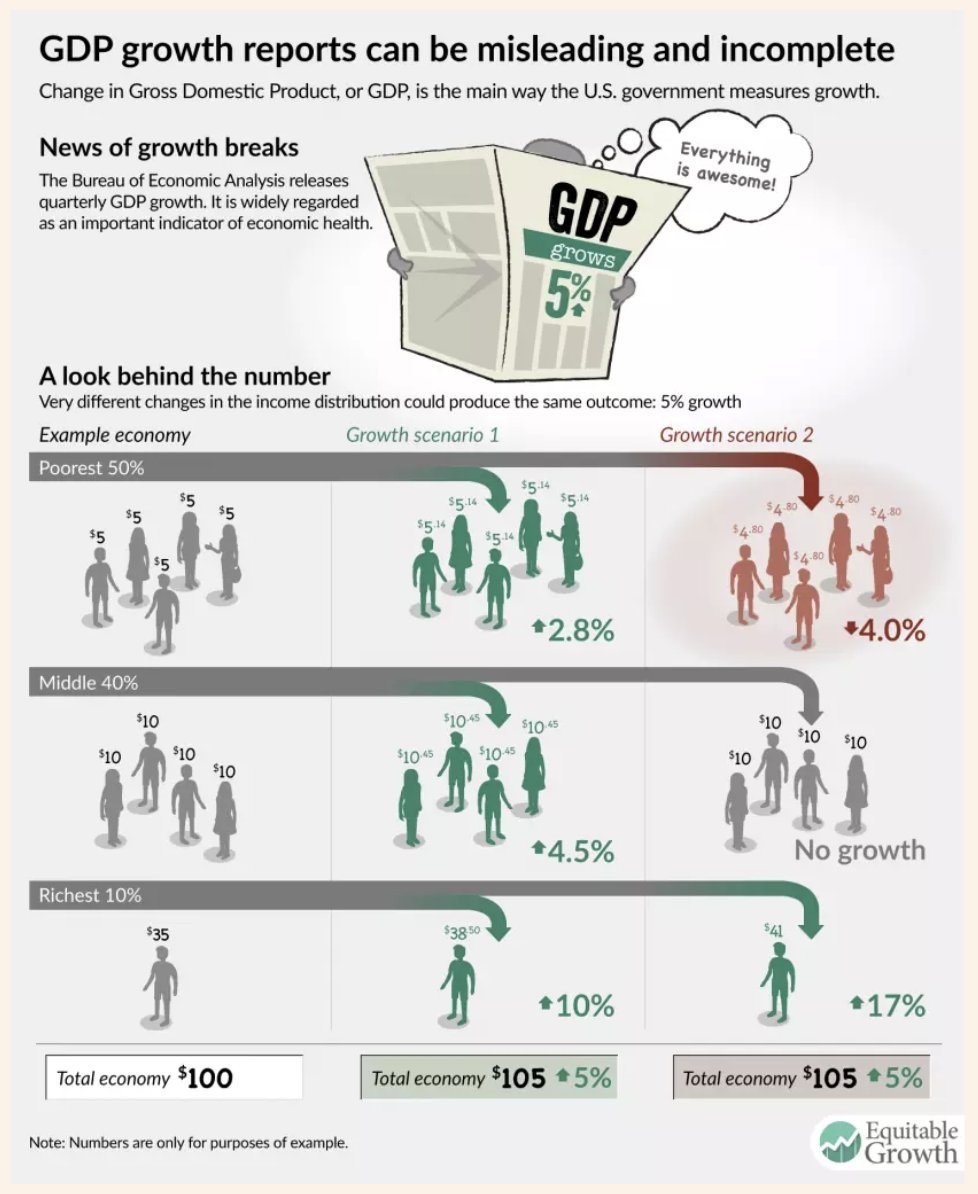

On GDP…..

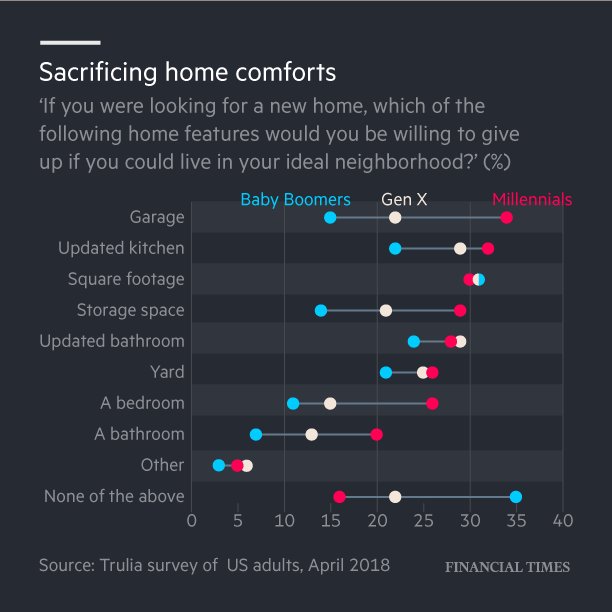

Generational Sacrifices

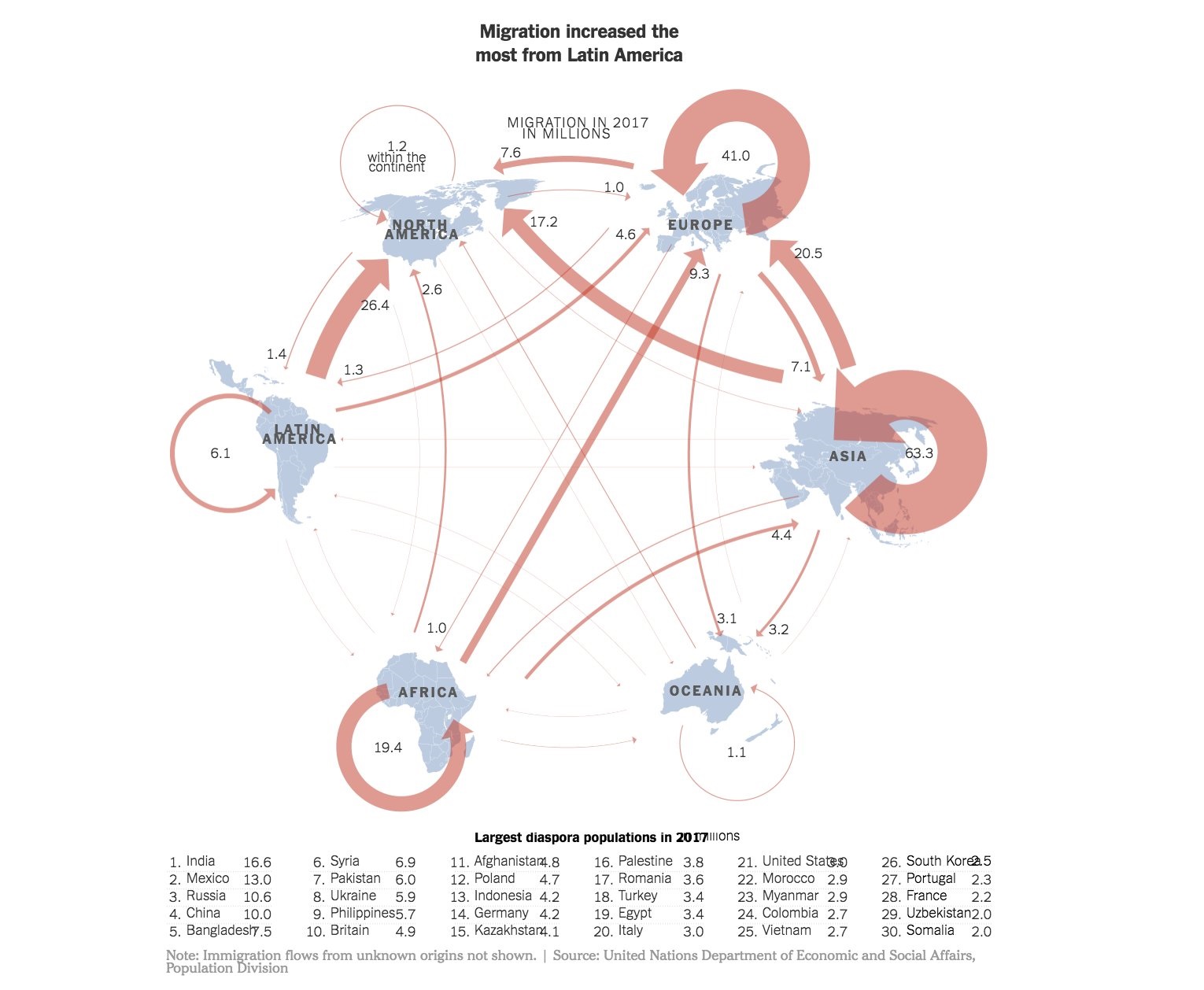

Global Migrant Flows

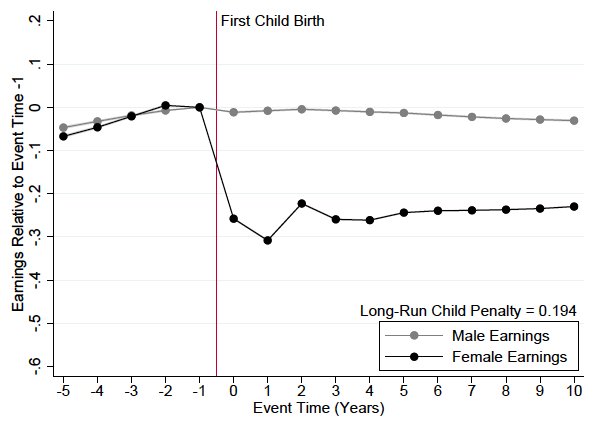

Male & female earnings Post the First Child

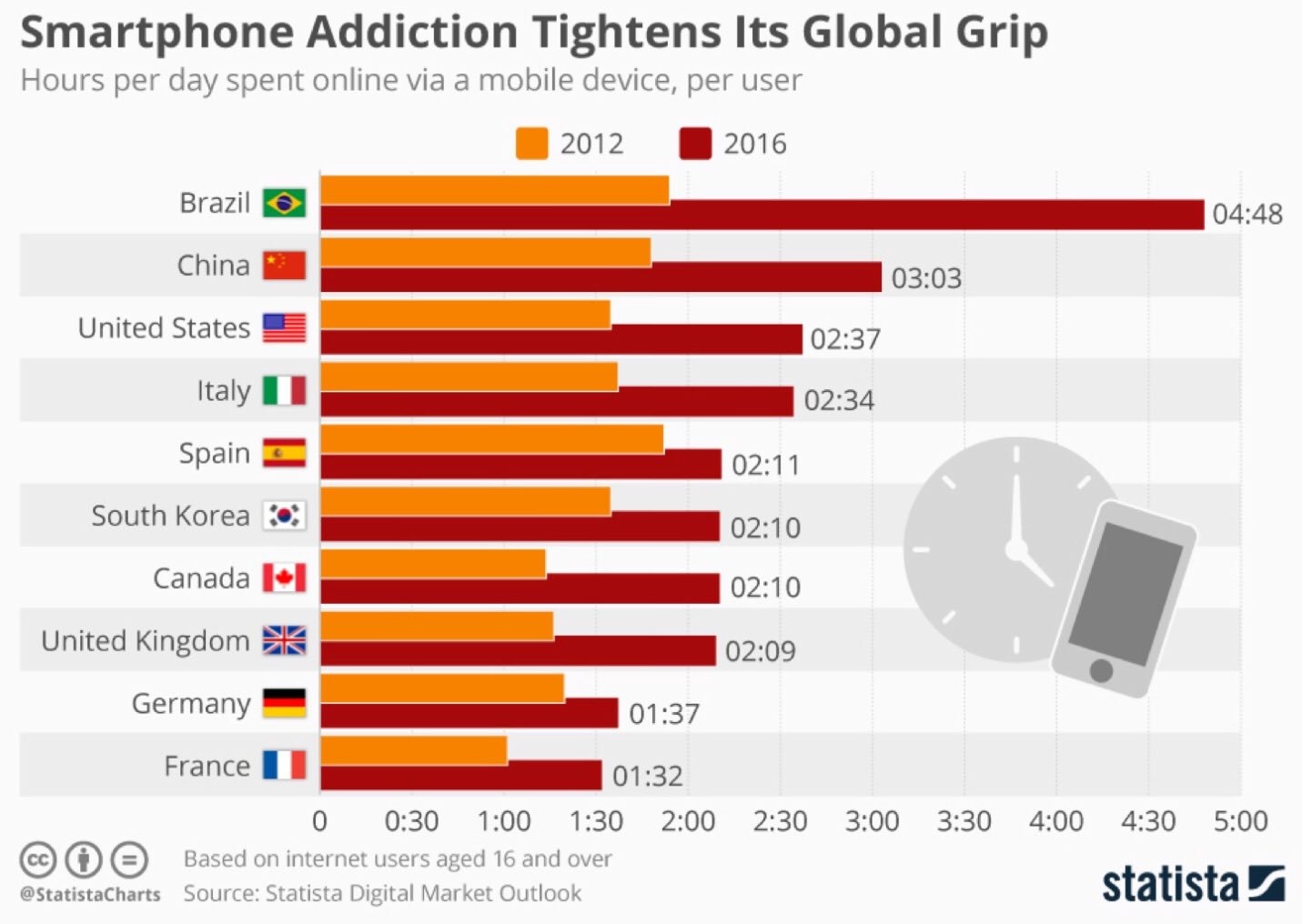

SmartPhone Addiction