It’s like trying draw blood from a stone. Some charts from Westpac on the wage price index:

Anyone looking at that little lot and seeing ANY chance of reaching RBA and Treasury goals needs to take the red pill.

We’ve chronicled many times why it’s happening:

Advertisement

terms of trade falls which although paused are still effectively falling in investment terms. This is a national wage cut;

poor economic structure with limited profits, oligopolies everywhere and no productivity;

because of poor capital productivity given the great housing ponzi, energy shock and zero reform all misallocating capital like confetti;

deteriorating demographics;

peak household debt;

hollowing out of non-mining tradables.

And on it goes. Then into this mess of a work force of 12.8m you drop at least 240k cheap foreign workers per annum to create a permanent supply shock!

Why would you expect anything other than trashed wages (Greg Jericho)?

Damien Boey at Credit Suisse quite rightly sees it getting worse:

Advertisement

…our wage inflation tracker was pointing to subdued wage inflation of around 0.5% in 2Q because there remains ample slack in the labour market. Even though EBA wage inflation has picked up, slack has been an offsetting factor, as has moderation in labour cost inflation reported in business surveys.

Going forward, we there are reasons to believe that wage inflation will pick up in trend terms. After all, the recent Fair Work Commission ruling will award a 3.5% annualized wage increase to roughly a quarter of the workforce in 3Q. Also, recent labour market data has been surprisingly strong. However, we think that there is room for undershooting in wage inflation given the overshooting occurring at present.

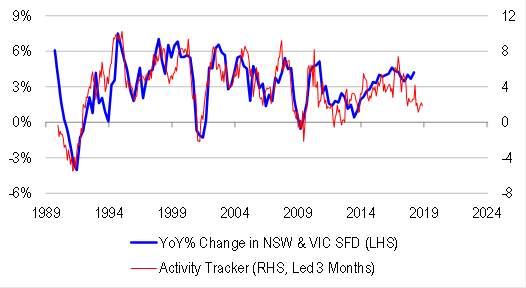

Much depends on the degree of slack in the labour market, which in turn reflects activity. Our proprietary activity tracker, based on a range of timely leading indicators, has been pointing to subdued growth of less than 1.5% annualized in the non-mining economy for some time. Sluggish retail spending, soft housing sentiment and more recently, slowing capex growth have been weighing on our activity tracker. Yet actual non-mining activity has been surprisingly strong relative to the leading indicators, consistent with the over-shooting we are seeing in employment and wages.

Unless something changes wage gains are about to stall and fall away. You can’t run mass immigration into huge economic slack and expect ANY OTHER OUTCOME:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.