Moody’s Investor Services’s latest report forecast that refinancing interest-only mortgages will become more difficult, contributing to an increase in mortgage delinquencies:

Regulatory measures introduced to reduce risks in the mortgage market have curbed the origination of IO loans, making it more difficult for borrowers to refinance their loans at the end of the IO period or extend the IO period for another term with the same lender. The more difficult refinancing conditions will contribute to an increase in mortgage delinquencies as the IO period on a record number of IO loans ends over the next two to three years…

Research conducted by mortgage lender, State Custodians, has found that 15% of 1,022 surveyed homeowners have faced challenges when trying to refinance, due to falling property prices pushing them into negative mortgage equity, with 34% of young people aged under 34 unable to refinance:

“Property prices have been stagnating and falling across much of Australia for some time now – especially in the major capital markets of Sydney and Melbourne – which has made refinancing tougher for some,” State Custodian general manager Joanna Pretty said in a statement.

“Anyone who has not yet built up a substantial amount of equity in property or whose property has fallen in value is more likely to be unsuccessful in seeking refinancing,” she added.

…Pretty said that when refinancing, homeowners and investors are often overly confident that their property increased in value.

“Declines in property value are influenced by what is happening in the market and the land value of the area,” she said. She explained that valuation of homes even in good areas can still come back below expectation due to poor property maintenance and upkeep.

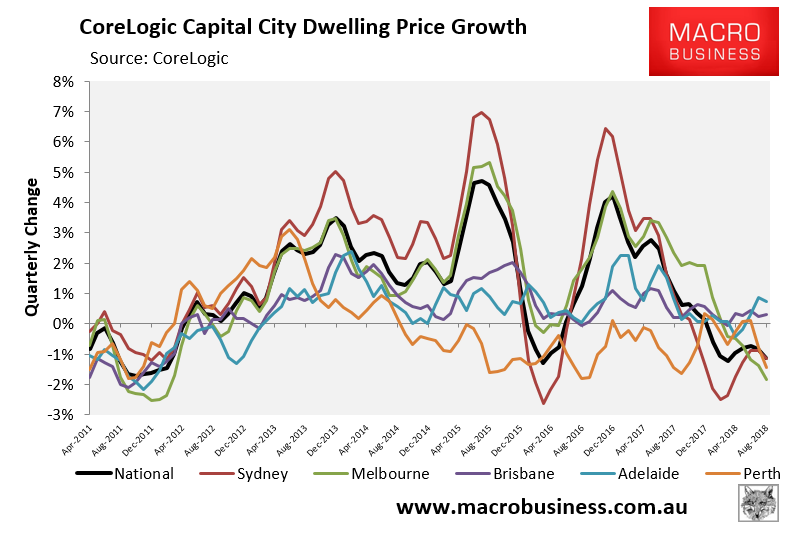

With property prices now falling across Sydney, Melbourne and Perth, more recent property purchasers are likely to face difficulty refinancing as they fall into negative equity:

The situation could get particularly unruly if the 15% to 20% property price falls predicted by some economists comes to fruition, and in light of the stiff headwinds facing the property market, including:

- The massive roll-over of interest-only mortgages into principle and interest (repayments by an average of 35%);

- Tightening lending standards arising from the banking Royal Commission;

- Rising bank funding costs; and

- Labor’s negative gearing and capital gains tax reforms should it win the next election.

The risk of forced sales will be greatest for heavily leveraged, negatively geared, investors with an interest-only mortgage.