Endeavor Equities Strategy has released a detailed report predicting heavy price falls for both Sydney and Melbourne as the “largest regulatory credit crunch in 30 years” bites:

A crackdown on the use of measures that understated borrower expenses, and overstated their borrowing capacity, would reduce loan values by up to 30 per cent and have a profound impact on property prices… about 40 per cent of all mortgages were “non-prime”, based on the level of borrower’s income relative to debts…

“Our base case suggests expense ratios will increase sharply, serviceability ratios will decrease proportionately, and loan sizes and property prices will suffer in the order of 15 to 20 per cent in real terms”…

Meanwhile “lower house prices would reduce the ability for stressed borrowers to trade out or finance”…

“We see credit growth over the coming 12 to18 months as likely flat to negative, margins under pressure, heightened legal risks and bad debts set to increase as equity turns negative for a significant portion of leveraged home owners and investors.”

The report said a sample of 420 Westpac mortgages, made public as part of the Hayne royal commission, supported its prior view that 40 per cent of all outstanding mortgage debt was “non-prime”.

This was based on the “internationally accepted” measure of “non-prime” being a mortgage in which more than 40 per cent of income was being used to service interest payments on debt.

” ‘Non-prime’ mortgages areas have default rates three to five times higher in a downturn,” Mr Orr told The Australian Financial Review.

Paul Dales, Chief Australia and New Zealand Economist at Capital Economics, also expects Australia’s housing correction to deepen:

“Prices in Sydney fell by 0.8% in July after seasonal adjustments, and are 5.4% below their peak and falling at a three-month annualised rate of 6.6%,” he says.

“In Melbourne, prices dropped by a larger 0.9% in July and for the first time since November 2012 the annual growth rate turned negative.

“Prices in Melbourne are still only 3.0% below their peak, but they are now falling at a three-month annualised rate of 8.3%.”

So the declines are getting steeper, a trend that Dales believes will continue.

“Most worrying is that prices will soon be falling at an even faster pace,” he says.

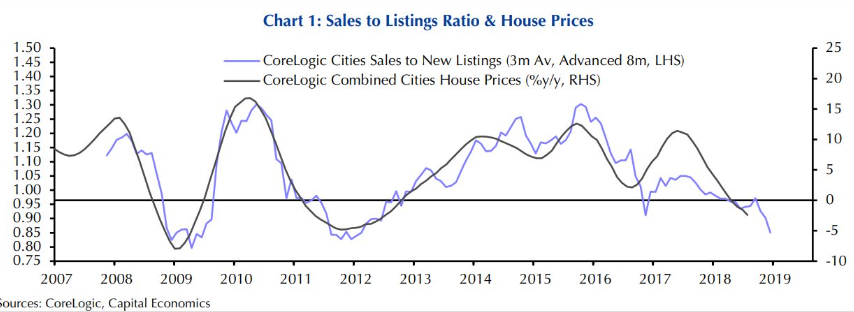

“The further decline in the number of home sales in March — the latest month of reliable data — to a seven-year low was larger than the fall in the number of new listings.

“In other words, demand is deteriorating at a faster rate than supply is improving.

“That suggests house prices in the eight capital cities will soon be falling by 5% a year”…

“There is still a big risk that the Royal Commission investigation into the banks results in a further tightening in lending standards,” he says.

Advertisement

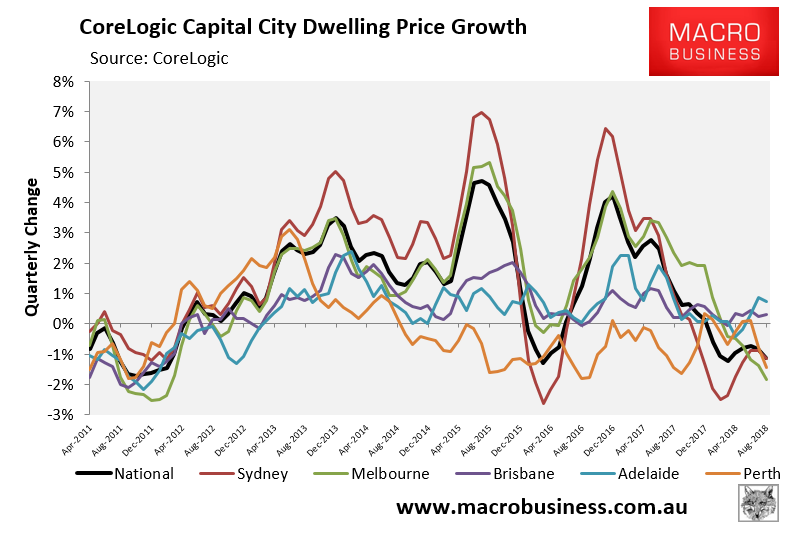

As noted by Paul Dales, quarterly price growth did weaken in the three months to July, according to CoreLogic:

So rather than recovering, the market appears to be falling at an increasing rate.

Advertisement

We also know that there are stiff headwinds facing Australia’s housing market over the next few years, including:

The massive roll-over of interest-only mortgages into principle and interest (raising repayments by 35% to 50%);

Tightening lending standards arising from the banking Royal Commission;

Rising bank funding costs; and

Labor’s negative gearing and capital gains tax reforms should it win the next election.

These factors combined will continue to weigh on housing values and make investing in property a particularly risky proposition, especially in Sydney and Melbourne, where values are most over-valued, investors are more dominant, and auction clearance rates, prices, and investor finance growth are already falling.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.