Readers and investors will know that the MB Fund’s prevailing narrative for 2018 was “reverse decoupling”. That is, that global synchronised growth would slump quickly into US leadership and a growing EM crisis around a rising USD and slowing China. This, in turn, would club commodities lower and contain US inflation and bond yields boosting US stocks even further. For Aussie investors long US stocks this held out the prospect of unusually good late cycle returns as US stocks rose but the AUD fell. The thesis was given extra piquancy by the sudden introduction of a trade war.

So far so good. But what happens next? How does the reverse decoupling end? Does the US come back to the pack or do EMs reboot and rally? JPM has a go at that question today:

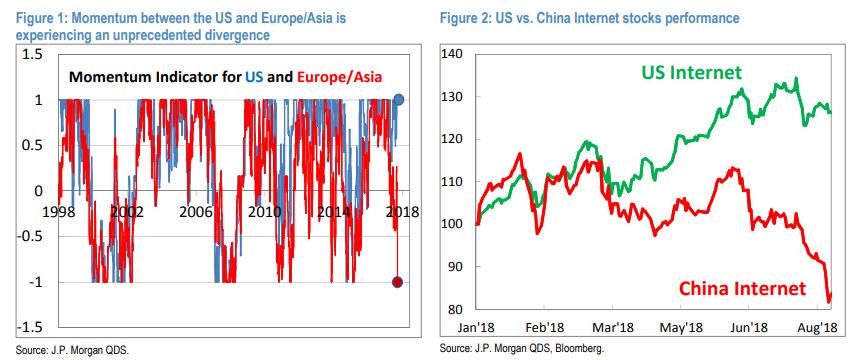

…the recent divergence in the performance of US Equities vs. the rest of the world is unprecedented in history. [Momentum] is positive for US stocks and negative for Europe and Emerging markets across all relevant lookback windows. This has never happened before.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

positive for US stocks and negative for Europe and Emerging markets across all relevant lookback windows. This has never happened before.