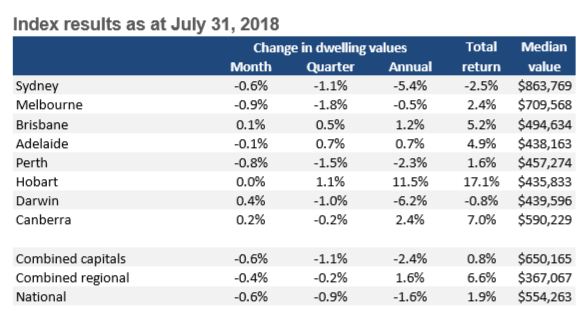

Following on from yesterday’s post on CoreLogic’s daily dwelling values index results for July, which showed that Australian dwelling values fell for the 10th consecutive month, CoreLogic has released its full results, which also cover the smaller capitals and regional areas (see next table).

As shown above, the smaller capitals and the regions had a mixed month, with Darwin (+0.4%) and Canberra (+0.2%) posting positive results, the combined regions posting falls (-0.4). and Hobart flat.

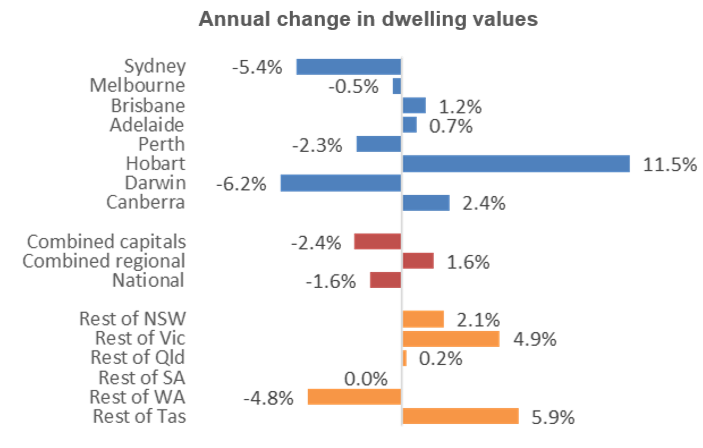

CoreLogic also shows that capital city annual growth (-2.4%) has fallen well below regional growth (+1.6%):

Advertisement

In its commentary, CoreLogic head of research, Tim Lawless, notes that the housing downturn has gathered steam, particularly at the top end of the market:

Advertisement

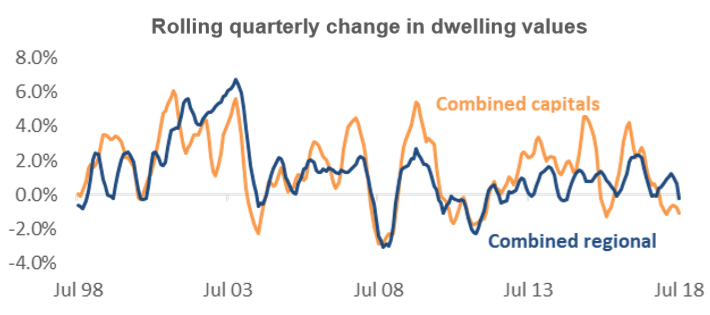

The month of July saw the housing downturn gather some momentum; on a national basis, the 0.6% month on month fall was the largest decline since September 2011 and the rolling quarterly change, at -0.9%, hasn’t been this low since January 2012…

Across the capital cities, Melbourne has been leading the downturn, with the quarterly rate of decline outpacing Sydney since May this year…

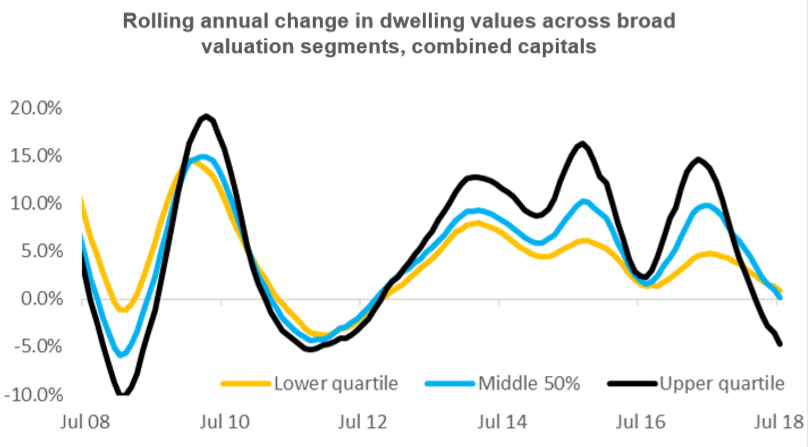

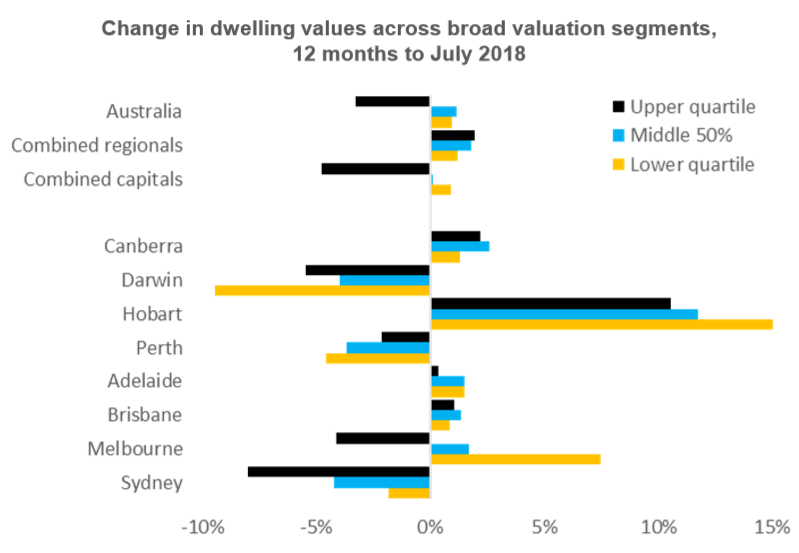

The premium end of the market has seen a more substantial decline Digging below the surface, Mr Lawless said, “the growth trends vary remarkably across the broad valuation segments of each housing market, highlighting the diversity of conditions.

“The starkest annual performance differential is in Melbourne, where the top quartile has seen values fall 4.1% over the past twelve months while property values across the lower quartile are 7.5% higher. Similarly, in Sydney, dwelling values are down 8.0% across the most expensive quarter of the market, while the most affordable quarter of the market has seen values fall by a much lower 1.8% over the past twelve months.”

“The surge in first home buyer activity evident since stamp duty concessions were introduced across New South Wales and Victoria in July last year has propped up demand across the more affordable end of the housing market, while a new focus on borrowers with a high debt to income ratio is likely to be dampening the amount of funds available for purchasing expensive dwellings.

“The focus on high debt to income ratios will intuitively impact the Sydney and Melbourne housing markets more than other cities due to demonstrably high dwelling prices relative to household incomes.” he said.

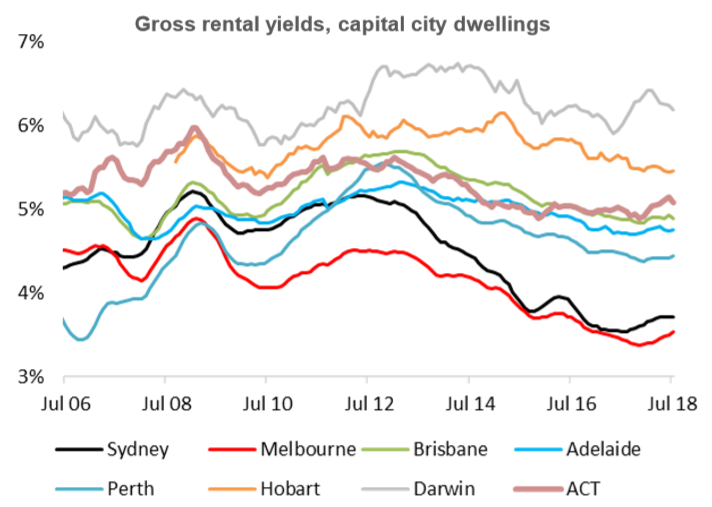

On the flipside, falling dwelling values has lifted rental yields from historical lows; albeit rents fell nationally in July and have turned negative year-on-year in Sydney:

Rental market conditions eased further in July, with national rents falling 0.2% over the month to be only 1.6% higher over the year. The weakest capital city rental markets are Darwin and Sydney where rents were 2.2% and 0.4% lower respectively over the past twelve months. At the other end of the spectrum was Hobart, where weekly rents have surged 10% higher over the year due to a severe shortage of rental stock coupled with rising migration rates. CoreLogic has tracked rents for over a decade and the 0.4% annual fall in Sydney rents is the largest decline on record. Mr Lawless said, “With rental conditions generally remaining subdued nationally, the recovery in rental yields is likely to be drawn out.”

Nationally, gross rental yields reached a record low of 3.61% in late 2017; the result of rapid value growth while rents only inched higher. With rental conditions remaining soft, the implication for rental yields, which nationally are currently only 11 basis points higher than the historic low, is that they are likely to remain well below average for the foreseeable future. Rental yields remain the lowest in Melbourne (3.04%) and Sydney (3.21%) which, along with dim prospects for capital gains and tougher credit conditions, is likely to act as a further disincentive to investors in these markets.

With the recent by-election results favouring the Labor party, the potential for changes to negative gearing and capital gains tax concessions following the next federal election would likely be playing on the minds of investors. While the outcome of Labor’s proposed changes to negative gearing and capital gains tax rules are debatable, it’s broadly accepted that these policies would have a further dampening effect on investor sentiment and overall housing market conditions.

Advertisement

CoreLogic also sees the housing correction continuing:

Overall, Mr Lawless said, “We can’t see any factors that may halt or reverse the housing markets trajectory of subtle declines over the second half of 2018..

“Although the 10% speed limit on investor credit growth has been removed for eligible lenders, we aren’t expecting a rebound in credit availability for investment purposes. Mortgage rate premiums for investment loans remain in place and the limits on interest only lending continue to disincentives investors.” Additionally, he said market factors such as low rental yields and dim prospects for short to medium term capital gains are also likely to quell investment demand.

Higher housing supply is another factor that is likely to weigh on some sectors of the market…

Despite the reduction in dwelling values in Sydney and Melbourne, housing affordability remains a pressing issue in these cities. The ratio of dwelling prices to incomes was tracking at 9.1 in Sydney and 8.1 in Melbourne at the end of June. Although these ratios are likely to improve as incomes edge higher and housing prices reduce, prices would need to fall a lot further to see this measure of affordability return to more adequate levels.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.