Via Gottiboff today:

Let’s assume such a major overseas event will not take place and concentrate on the events we can control which are contributing to the housing mess in Sydney and Melbourne.

We’ll start with the banks and their regulators. The banks now have a set of rules that have been imposed on them by APRA and bank staff are petrified of showing any flexibility. The most secure borrowers are held up because some minor APRA regulation has been breached, so the loan is blocked. Seeing their business decline, some banks are offering low rates for a couple of years. That enables them to get around, but not breach, the APRA rules. Once the army of ASIC corporate cops arrives into the big banks, such artificial mechanisms may be more difficult. In any event they are dangerous for banks because they could be accused of irresponsible lending and be liable for any loss.

At this stage, the Reserve Bank is happy that most dwelling markets have not fallen to levels that cause economic damage. But as long as the credit squeeze continues, prices will keep falling. The further prices fall, the harder it will be to reverse, because everyone holds back waiting for the market to fall further.

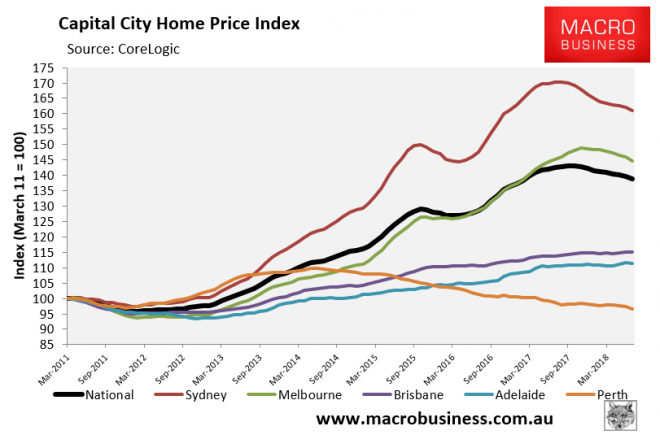

The inner city apartment markets in Sydney, Melbourne and Brisbane are down 20 per cent and it’s clearly possible falls of that size will spread to other areas of Sydney and Melbourne.

Chinese buyers, who compared Sydney and Melbourne prices to Shanghai and then declared Australia cheap, were the buyers who did most to boost apartment prices. The Chinese are honouring their off the plan purchases, but are no longer substantial buyers. Australian investors are waiting to see where the fall ends.

Chinese buyers are not going to return. If anything they will diminish further as the falling yuan is arrested by capital account tightening.

APRA seems happy to allow the fringe banks and non-banks to take market share from the majors which are still ages away from delivering the loan leverage data needed to get approval for looser lending standards. Falling prices may well cause them to tighten standards further before we ever get there.

Then we have the interest-only reset and Labor’s now inevitable negative gearing reforms (and/or a Coalition election Hail Mary immigration cut).

Supply is gushing out and more is coming. Building approvals are still very high though falling.

Plus the end of the cycle is approaching one way or another and another offshore shock is inevitable. Aussie bank funding costs are already rising in part on that basis. But it is also structural given the perception shift of Australian credit quality driven by the royal commission. Mortgage rates may be past the cheapest that they will ever be right now.

That has given us a falling price disequilibrium with no end in site:

For now the supports remain a few more possible rate cuts, perhaps two with half kept by the banks. And mass immigration. Fiscal is already deployed in FHB grants and prices are falling anyway.

History tells us that the RBA’s reaction function is triggered somewhere between 5-10% price falls, chart from UBS:

And given the slowing economy as public infrastructure investment plateaus and consumption diminishes, the RBA forced to cut sometime next year as the labour market weakens.

That’ll trigger a little bit of housing activity but not for long given the broader negative house price settings will persist.

So we might see the first leg down approach -10%. Then a pause before a second leg down of another -10%. Whether that second leg is better or worse will depend upon the global cycle and timing of a shock but Gottiboff’s -20% total seems a reasonable suggestion for the initial correction.

Beyond that we’re into truly speculative territory. The mining bust is still only half over as Chinese growth will grind lower, in fits and starts, over the next five or ten years. That means income pressures in Australia for a long time to come and deflationary pressures everywhere with no monetary and limited fiscal firepower in support.

We may see quantitative easing and will see a much lower Australian dollar. But also much lower house prices, perhaps another -20% in real terms over the subsequent decade. Taking us to a total correction of 30-40%.

But those are all just guesses. Perhaps there is another rabbit to pull out of the hat beyond paying no interest and selling your kids to corrupt Chinese.