So says RBA and APRA:

…the adjustment in the Sydney and Melbourne housing market was “being well managed to help create a sustainable housing market” and while global growth was growing above trend, there were three main downside risks.

Mr Frydenberg said his meeting with Mr Byres left him similarly assured over the housing market in that the adjustment in Sydney and Melbourne was “orderly”.

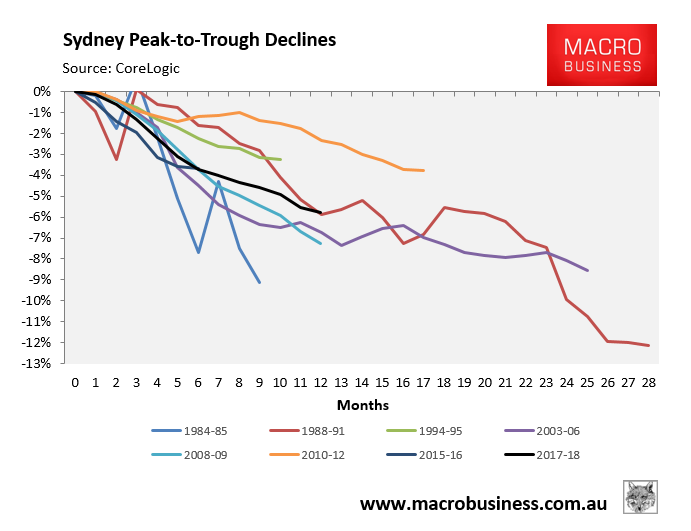

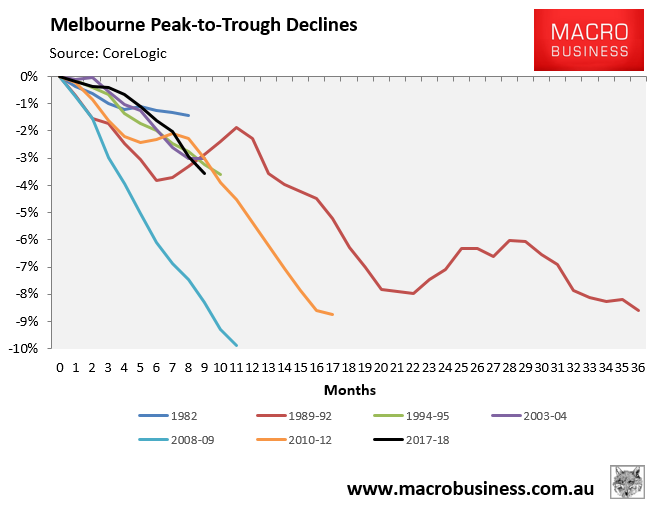

Here is the correction measured against prior versions:

I guess you could describe that as orderly so far, just so long as you don’t look under the bonnet. Why so?

Because this is the first ever property correction that we’ve had without hiking interest rates. That means that when/if the market threatens to turn disorderly, which it doesn’t do until folks get spooked that prices are going to keep falling, there wont be any monetary ammunition left to turn it around.

The RBA has already said it considers a 1% cash rate to be the absolute bottom given Australia needs to fund its external deficit. So that only leaves 50bps to cut and, as Westpac showed yesterday, at least half of that will be held back by the banks as market-based funding costs rise.

That means that during the next global shock, punters can look forward to a grand total easing on mortgages of 25bps versus 300bps during the GFC. It may even be worse because the RBA will very likely have to cut twice next year year as the economy slows and Labor reform to property taxes trigger more house price falls, well before any global shock, meaning there’ll be nothing left at all.

When the RBA cuts again I do expect to see some brief rally in support of house prices as old habits die hard but I do not expect it will last long. Wider headwinds are too great.

There is also APRA’s post-royal commission structural shift. The days of liar loans and interest-only binges are gone and are not coming back and the interest-only reset has years to peak.

Not to mention withdrawing Chinese capital, which is going to intensify with the Trump trade war.

Some form of lower immigration is headed for Sydney and Melbourne as well.

Of course there is always fiscal support such as first home buyer grants. But, again, atypically they are already in the market in Sydney and Melbourne and prices are falling anyway. That little trick is also nearly played out.

There will be lots of other desperate attempts to prop up the market as prices fall and perhaps they will be enough to keep the ongoing falls orderly.

But falls they will be and I wouldn’t bet on it not turning completely out of control.