DXY is off to the races as EUR finally breaks on the reality of clapped out European growth:

Here’s why:

AUD broke to two year lows versus DMs:

But soared against collapsing EMs:

AUD market positioning is pushing towards more rarefied bearish territory at -55k contracts:

Gold held up remarkably well. Don’t expect it to last:

Oil looks to be forming a downtrend:

Base metals were hit:

Big miners too:

Not as hard as EM stocks:

Which have a long way yet to fall if EM junk is any guide (and it is):

Treasuries were bid:

Bunds are on fire:

As Italy burns again:

Stocks took a bit of pain:

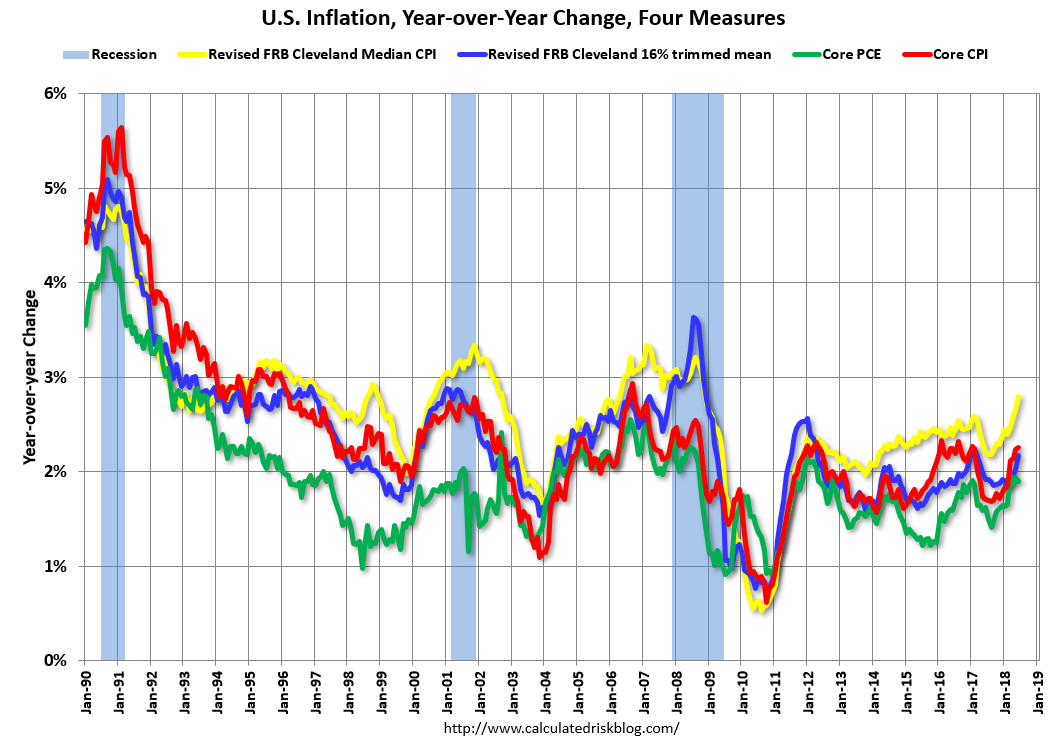

US inflation came in on the button:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% (2.7% annualized rate) in July. The 16% trimmed-mean Consumer Price Index also rose 0.2% (2.3% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report.

Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers rose 0.2% (2.1% annualized rate) in July. The CPI less food and energy rose 0.2% (3.0% annualized rate) on a seasonally adjusted basis.

Fading oil ought to prevent any kind of blow-off but there’s enough here to keep the Fed interested.

So, two weeks off and here we are with an intensifying EM shakeout. There’s further to run. EM junk debt is the leading indicator and while it falls so will EM equity, commodities and the Australian dollar.

How low do we go? I’ll leave my 72 cents year-end target in place but there is an increasing risk of overshoot. That hangs on some kind of EM contagion. Today’s flash point is Turkey which has large offshore debts (more on that in a separate post). That said, it is also on the end of some nasty Trump treatment so is under particular as well as general pressure.

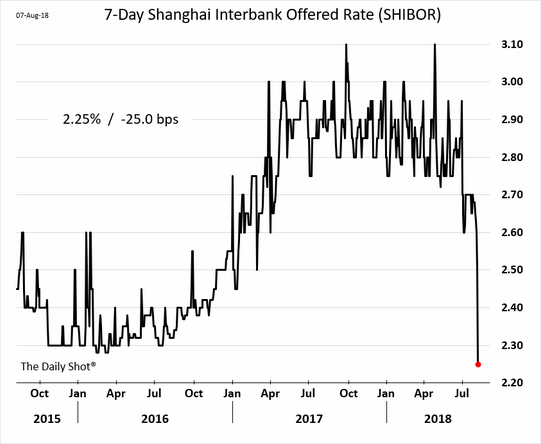

The building EM volatility and Trump trade war – which are the same thing in the sense of US inflation – is now seeing a response in China which is slashing and burning money market rates:

This will release more lending but this kind of easing is still operating within the recent mechanisms of tightening. It has not yet moved beyond them. Thus the economy will still slow for the next six months.

That slowing plus the trajectory of Chinese response speaks to more stimulus coming, such as the NDRC unleashing a new torrent of infrastructure projects. If the panic really sets in we’ll see the lifting of some housing controls and possibly even cutting interest rates directly (again, more here). China has rather stupidly backed itself into a corner on the US trade war and as a result has to turn back once again to the very dying economic model it was trying to escape.

One wonders as well what the next US response will be. Trump is moving towards a quick trade deal on NAFTA. That suggests we can now expect huge new tariffs to be applied to China before year end. That won’t be enough growth for the US as the tax cuts diminish next year so Trump will need to revive the $1tr infrastructure pledge. If he can get such a package away before or after the mid-terms then it could add 0.5-1% to the US for five years. This would give it a growth outlook steady at 2.5-3%. I can’t see why Democrats wouldn’t agree.

Before going on holiday I wrote that:

There are two schools of thought on this. The first is that Donald Trump has in mind a simple trade war. This notion is supported by the progressive lifting of tariffs on Chinese goods and White House rhetoric to date. It is also supported by Trump’s wider tariff agenda and his jawboning for a lower US dollar.

The second school of thought is that the US is pursuing an economic war. This was captured recently by Steven Bannon:

If this is the objective then the US will drive tariffs and the USD upwards to break both the Chinese trade and capital accounts. China will see both falling trade to the US and major capital flight driving a domestic credit crunch. The US will need to keep stimulating to achieve this end, just as Ronald Reagan did versus the USSR.

There is a third possible outcome which is probably the highest risk. That is that the US begins with a trade war and stumbles into a economic war. This could easily happen because China cannot meet the US demands or it mishandles its response. From here it is frighteningly easy to see how the US applies its tariffs right up to $500bn, China responds with an aggressive internal anti-US goods boycott. The US responds in kind and global recession is upon us, with Australia at its epicentre.

The fourth scenario is more benign. Both leaders are under pressure over the issue at home. Either or both leaders could be forced to sue for peace, triggering a big risk-on rally for global markets.

A fifth scenario is now also firming. It is that China and the US will enter an intensifying trade and economic war but also that both governments spend like drunken sailors to mitigate fallout for their domestic constituents. This is more akin to the Ronald Reagan approach to breaking a strategic competitor by outspending them than it is a breaking of China with tariffs.

For the Aussie investor this would be significant. It means another round of commodity-intensive stimulus in China and, moreover, the same in the US. The outstanding investment beneficiary will be commodities, especially steel, which is already moving in advance though it will have to pull back sharply as conditions get worse first through H2 this year.

Assuming the combined US/China stimulus arrives then it would support a steeper US bond curve for a while. Or, at least, mitigate flattening as the long end sells with the short. US equities should remain bullish as aggregate demand is supported and the resonating effects of tax cuts drive good EPS growth. US wage rises still look of the Goldilocks variety too, firming but not too fast given the disruptions of the trade war. The US dollar should remain strong as the Fed keeps tightening and Europe sinks back into its perpetual stagnation.

This all means a material further widening in US/Australian yield spreads as falling house prices kill RBA tightening and thus a weak Australian dollar. Though once China gets some traction with stimulus that will give the currency some support next year.

In sum, the world is caught between the ongoing EM shakeout and the need for MOAR stimulus to offset it. Given the risks, the MB Fund remains conservatively positioned with large cash and bond holdings, very underweight Aussie equities and overweight US equities.

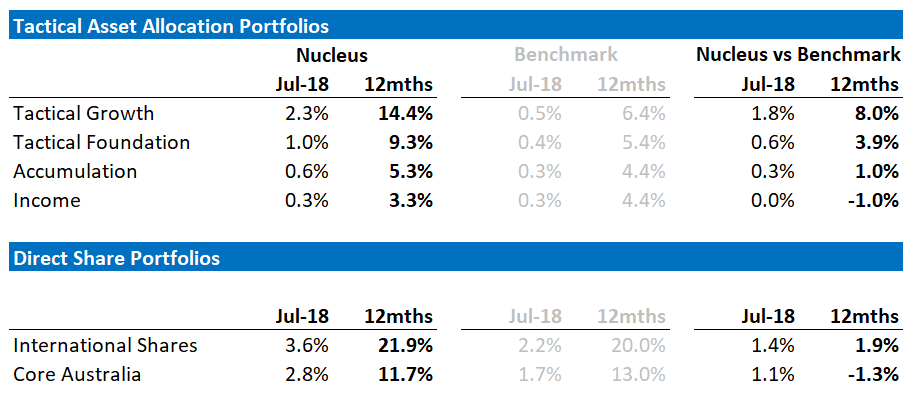

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.