Treasuries were flogged and curve steepened a bit:

Advertisement

Same for bunds:

US stocks are in free air and flying through record highs:

Advertisement

The proximate cause was a new US/Mexico trade deal, via NYT:

President Trump said on Monday that the countries would be entering into a new trade deal called the United States-Mexico trade agreement, and that he wanted to get rid of the name of Nafta, which he said sounded bad. Mr. Trump has frequently called the trade deal, which includes Canada, Mexico and the United States, the “worst” trade agreement in history.

The agreement with Mexico gives Mr. Trump a significant win in a trade war he has started with countries around the globe but it falls far short of actually revising Nafta. The preliminary agreement still excludes Canada, which has been absent from talks held in Washington in recent weeks.

Speaking from the Oval Office, the president, flanked by advisers including Jared Kushner and Robert E. Lighthizer, the United States trade representative, hailed the preliminary agreements as “a big day for trade” and “a big day for our country.”

Best trade deal ever! More seriously, I don’t know how Canada can stay out now. When it folds then Trump will have cleared the decks for a renewed tilt against China.

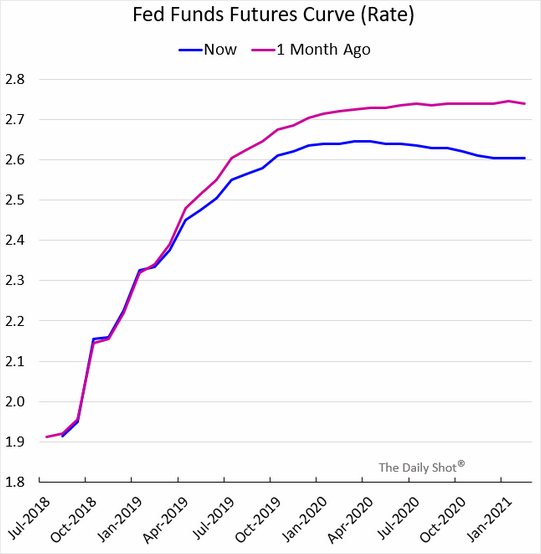

Also offering support to stocks is the dovish interpretation of the Jay Powell speech at Jackson Hole. Markets are now pricing Fed rate cuts in 2020:

FTAlphaville has some more on how far the USD will fall under these forces:

Credit Suisse’s Shahab Jalinoos and Alvise Marino tracked exactly how the dollar has moved in the aftermath of specific comments from Trump. Following his tweet on July 20 that the US was losing its competitive edge because of currency manipulators, rising interest rates and a stronger dollar, the greenback fell immediately. Its losses extended for about a week, before rebounding:

Since Trump’s most recent salvo occurred just last Monday, it’s too soon to say if the initial weakness will sustain. But Jalinoos anticipates a similarly muted reaction.

The dollar has not capitulated because the US’s mix of loose fiscal policy and tight monetary policy all but ensures it (or any currency for that matter) will strengthen. The Peterson Institute for International Economics estimates that the tax cuts enacted at the end of 2017 and February’s spending package will add $276bn in fiscal stimulus to the US economy this year. That’s about 1.4 per cent of GDP. And to keep a lid on inflation, the Fed is raising interest rates. A hike in September—despite the dovish tone of Chairman Jay Powell’s speech at the annual Fed symposium in Jackson Hole, Wyoming on Friday—appears sewn up.

Then there’s the dollar’s safety premium. As the world’s reserve currency, during periods of economic, financial or political uncertainty, investors buy greenbacks. This month, substantial volatility has rippled through emerging markets, sparked by Turkey’s currency crisis. Of course, there’s also the escalating trade war. Last week, the US imposed 25 per cent tariffs on an additional $16bn worth of Chinese goods, to which China retaliated with its own. Viraj Patel of ING sees it as a trap:

The trade war is not too risk-off for stock markets to be down massively, but equally it is not too benign to ignore. So you’re not going to put your money into risk currencies because you’re one US policy move away from markets actually selling off. You’ll default to dollars.

Were it not for this political backdrop, Patel says the dollar may have already depreciated. Various leading economic indicators (ISM, Philly Fed Index and Michigan consumer confidence) are starting to run out of steam, capping further dollar strength. Of course, neither the emerging markets rout nor the trade war appear anywhere close to a resolution, so the dollar’s safety bid appears alive and well.

That’s about right, I’d guess. As said yesterday, post-Jackson Hole the USD will come under some selling pressure. The question is how much. I expect the trade war to get worse and more Trump stimulus plus increasingly weak data Downunder so not too far for the AUD is my guess.

It does not therefore change the MB Fund allocations. Even with a goodly AUD rise, the S&P500 remains a much better bet than the ASX200:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.