This week’s key economic data revealed another contradiction.

On Wednesday, it was revealed that Australian wages growth was stuck near record lows, growing by just 2.06% in the year to June (1.99% in the private sector):

Then yesterday, it was revealed that Australia’s unemployment rate has fallen to the lowest level since November 2012 at 5.36%:

Advertisement

For several years, economists have projected a rebound in wages growth as Australia’s unemployment falls towards the NAIRU (non-accelerating inflation rate of unemployment), which the RBA claims is around 5.0%.

Indeed, the Federal Budget explicitly forecast a sharp rise in wages growth as unemployment falls to a projected 5.25% for the next three years:

Advertisement

What the pundits often miss is that it is not the unemployment rate that is the central indicator for wages growth, but rather the underemployment rate (i.e. those wanting more work). Underemployment appears to be the best indicator of slack in the labour market and whether bargaining power favours firms or workers.

To illustrate this point, consider the following three charts.

Advertisement

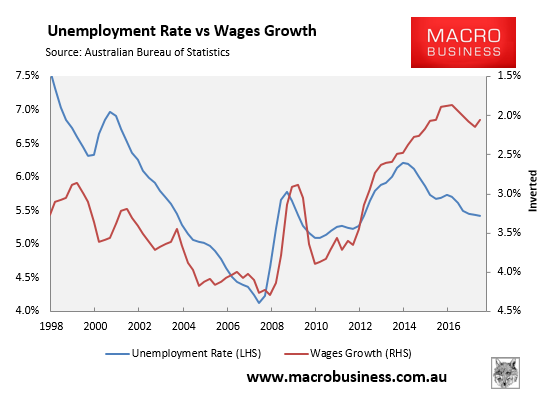

First, the unemployment rate versus wages growth (inverted):

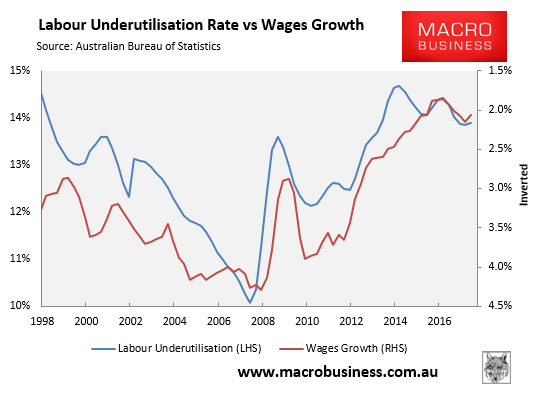

Second, the underutilisation rate (i.e. unemployment plus underemployment) versus wages growth (inverted):

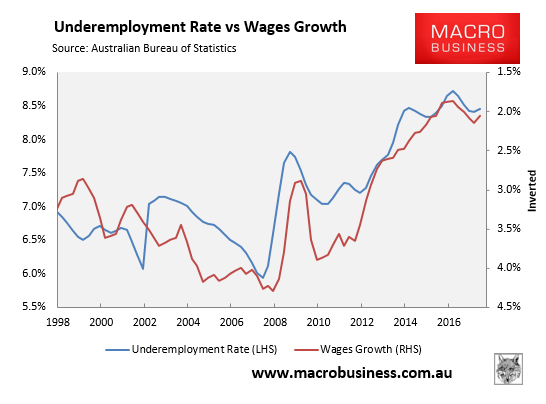

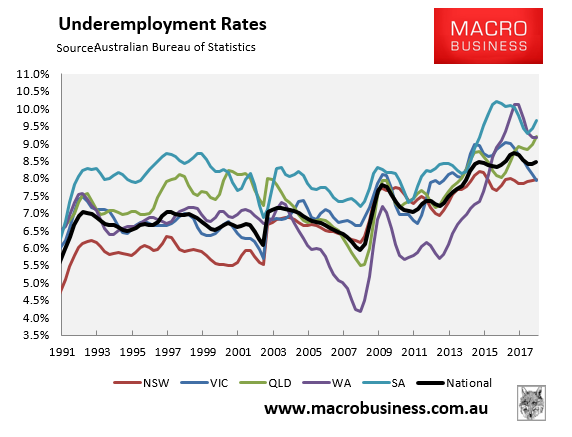

Finally, the underemployment rate versus wages growth (inverted):

Advertisement

Of the three charts, the underemployment rate (third chart) has the strongest correlation with wages growth and the unemployment rate (first chart) has the weakest.

Economist Phil Soos has come up with similar conclusions in the below scatter chart:

Advertisement

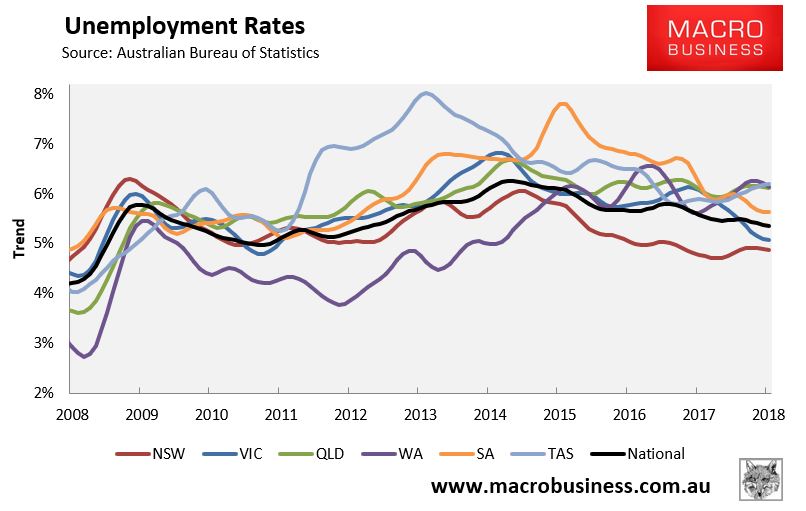

Interestingly, NSW bears this point out. Despite having by far the lowest unemployment in the nation at 4.9% (i.e. supposedly below NAIRU):

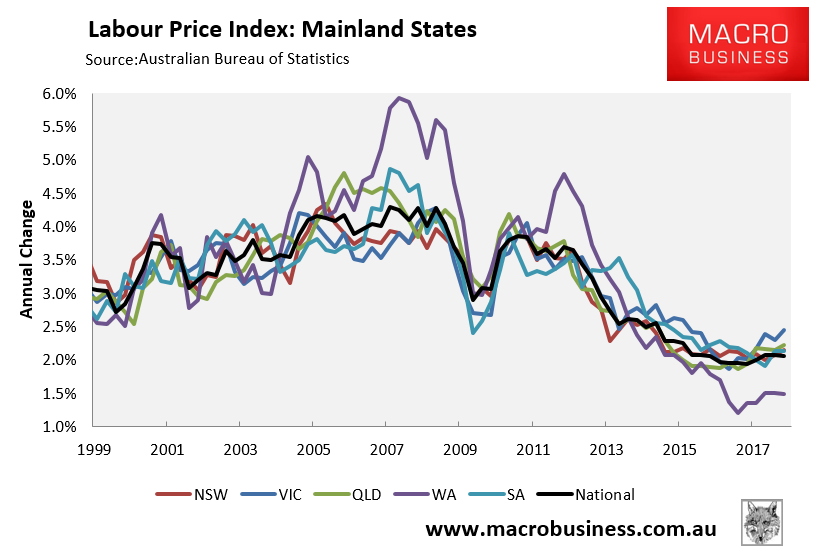

NSW wages growth is weak (2.1%):

Advertisement

Whereas underemployment remains high:

Perhaps there is some “non-accelerating inflation rate of underemployment” that economists should instead focus on?

It also raises the question of whether wages can be stimulated when the supply of labour is continually augmented via immigration. As noted recently by CBA senior economist, Gareth Aird:

Advertisement

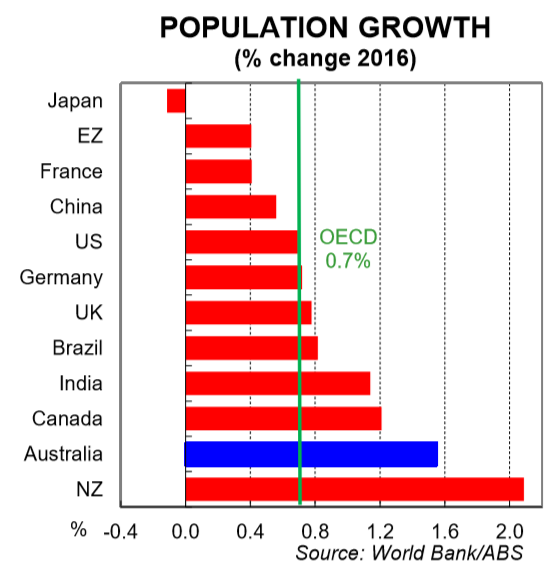

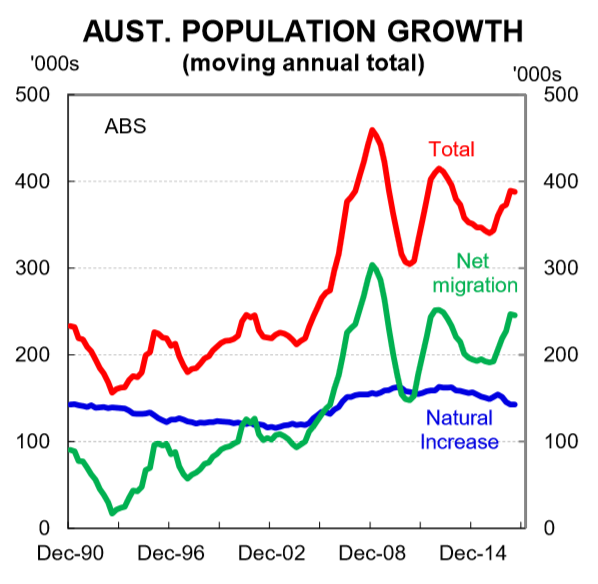

Australia has adopted a policy decision to run a very high immigration program by OECD standards (charts 6 and 7). It has continued down this policy path despite several years where labour market slack has been elevated (that is, there has been plenty of Australian’s looking for work in some capacity). From a wages perspective, immigration augments the supply of labour beyond what would have naturally occurred. That intensifies the competition for existing jobs while of course also adding to the demand for labour. The bigger the supply side shock, the more that the competition for existing jobs intensifies. This puts downward pressure on wages initially, but its effect should only be temporary. However, if the supply side shock continues when slack is elevated the temporary impact may not prove to be so short lived.

In many ways, this is the result of running a high immigration program when there is plenty of slack in the labour market based on the notion of skills shortages. In 2016/17, the “Skill Stream” accounted for 67% of the total migration programme outcome. From the perspective of an employee, working in an industry that has a skills shortage means that the labour market in that profession should be tight. In industries with skills shortages, bargaining power between the employee and employer should move more favourably in the direction of the employee and higher wages should be forthcoming. But in Australia’s case at the moment there is no evidence of widespread skills shortages based on the broad-based weakness in wages growth. The relatively high intake of skilled workers looks to be a pre-emptive strike on the expectation that there will be skills shortages in the future. It does not appear to be a policy response to the evidence of skills shortages. This has implications for wages and the NAIRU.

If “skills shortages” are not able to manifest themselves because employees are consistently able to hire from abroad, then employees have had a reduction in their bargaining power that is independent of the level of slack in the local labour market. Essentially talent is not scarce because firms can hire from a global pool of labour. The downward pressure that this applies on wages growth is amplified if a worker from abroad is able and willing to work at a lower rate of pay than local residents. Given the attractiveness of Australia as a destination to live and work relative to so many other places it is reasonable to assume that this occurs to some extent. The upshot means that employee bargaining power is lowered at the margin which therefore puts downward pressure on the NAIRU, all else equal.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.