Trade tensions and deleveraging take a toll on performance

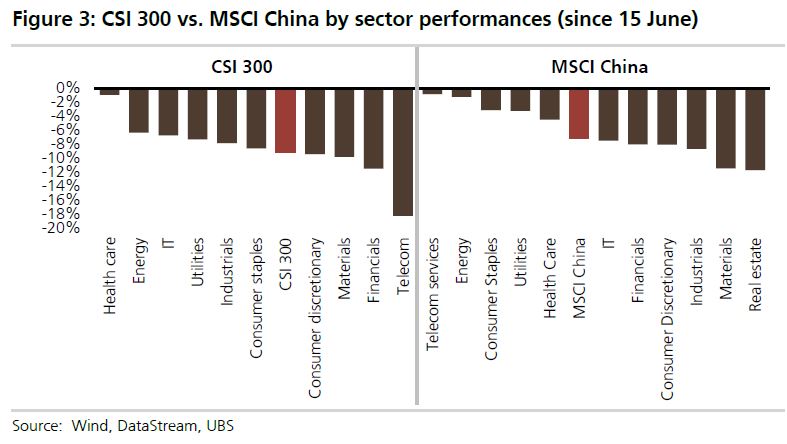

Since the 15 June announcement of tariffs between the US and China, MSCI China and CSI 300 indexes lost 7% and 9%, respectively. The selloff is broad-based and reflects market concern about the longer term impact at the macro level. Prior to this, MSCI China had gained 5% from the start of the year while CSI 300 was down 7%, indicating more cautious sentiment among onshore investors. Investors have turned overall defensive this year. Among MSCI China constituents (aside from the better performance of energy bolstered by rising oil prices), healthcare, consumer staples and utilities fared better; in the A-share market, performance is skewed to the healthcare and consumer sectors with some cyclical sectors (real estate, materials, industrials) down by over 15%.

De-rating in both markets; A-shares seemingly pricing in a hard-landing

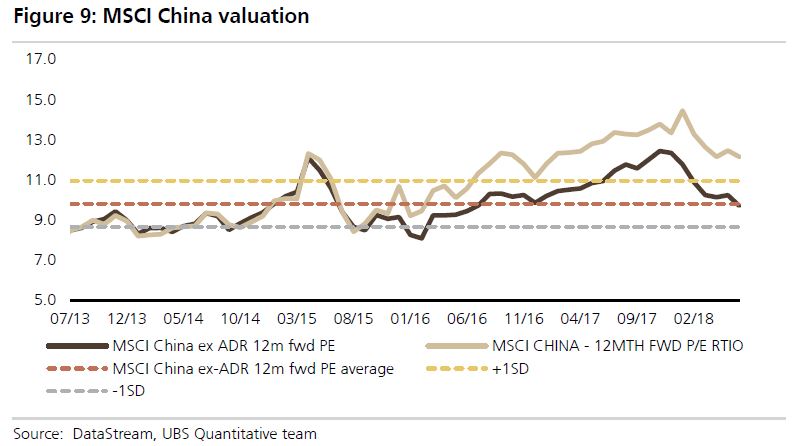

MSCI China is trading at 13x this year’s earnings, 10% below the start of the year and trailing PE of CSI 300 at 11.5x is not far above the levels of late 2015 and early 2016, when a deep stock market correction, weak external demand, currency depreciation and capital outflows weighed heavily on market sentiment. However, current economic and corporate fundamentals are on a much sounder footing compared with two-and half- years ago, in our view, with stronger export growth, better corporate profitability and stable FX reserves.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.