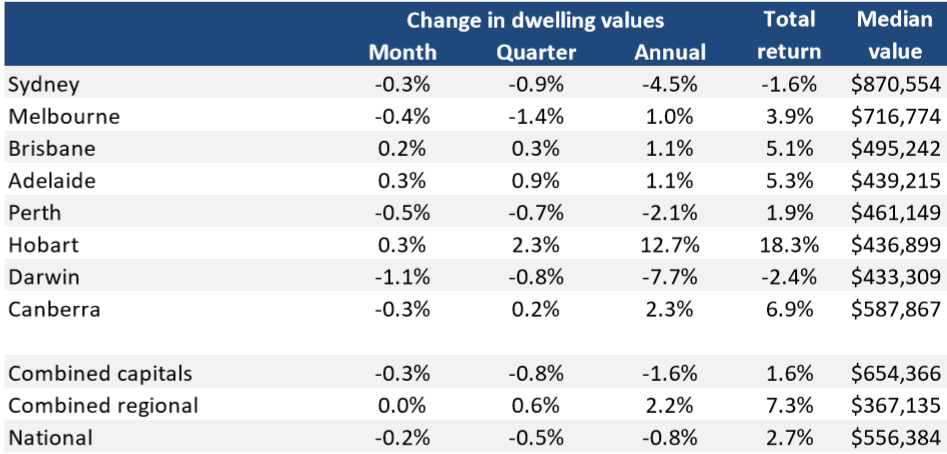

Following on from this morning’s post on CoreLogic’s daily dwelling values index results for June, CoreLogic has released its full results, which also cover the smaller capitals and regional areas (see next table).

As shown above, the smaller capitals and the regions had a mixed month, with Hobart (+0.3%) recording a rise in values, but Darwin (-1.1%) and Canberra (-0.3%) recording falls, and the combined regions flat.

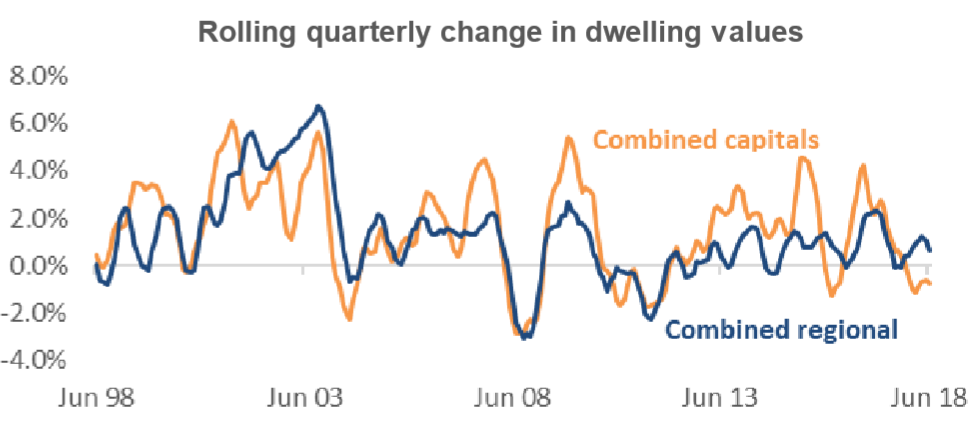

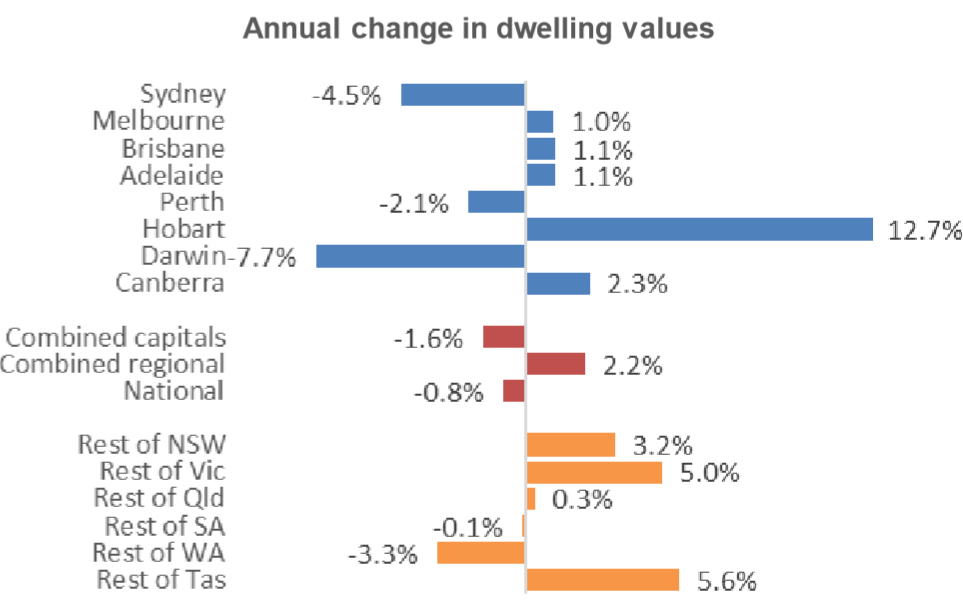

CoreLogic also shows that capital city annual growth (-1.6%) has fallen well below regional growth (+2.2%):

Advertisement

In its commentary, CoreLogic head of research, Tim Lawless, notes that recent home buyers in Sydney could be facing negative equity, especially at the premium end of the market:

Advertisement

According to CoreLogic research director Tim Lawless, despite recent and consistent monthly falls, national dwelling values remain 32.4% higher than five years ago. He said, “This highlights the wealth creation that many home owners have experienced over the recent growth phase, but also the fact that recent home buyers could be facing negative equity.”

“Tighter finance conditions and less investment activity have been the primary drivers of weaker housing market conditions and we don’t see either of these factors relaxing over the second half of 2018, despite APRA’s 10 per cent investment speed limit being lifted this month”…

Based on the CoreLogic stratified hedonic index, values across the most expensive quartile of capital city properties were down 1.5% over the past three months while the least expensive quartile saw values hold firm. Similarly, over the past twelve months, the most expensive end of the market recorded a decline of 3.6%, while the least expensive end of the market recorded a 1.4% gain.

Declines across the most expensive sector of the capital city market is largely attributable to the declines in Sydney and Melbourne, where the upper quartile of property values fell by 7.3% and 2.5% respectively over the past twelve months. Mr Lawless said, “A surge in first home buyer activity has helped support demand across the more affordable price points in these cities”.

… the cities with the highest concentration of investment activity, Sydney and Melbourne, are experiencing the most substantial decline in housing demand. To some extent, Mr Lawless noted that this reduction in demand has been counterbalanced by a surge in first home buyer activity across New South Wales and Victoria, as first time buyers take advantage of stamp duty concessions. However, activity from this segment peaked in November last year, and has continued to wane.

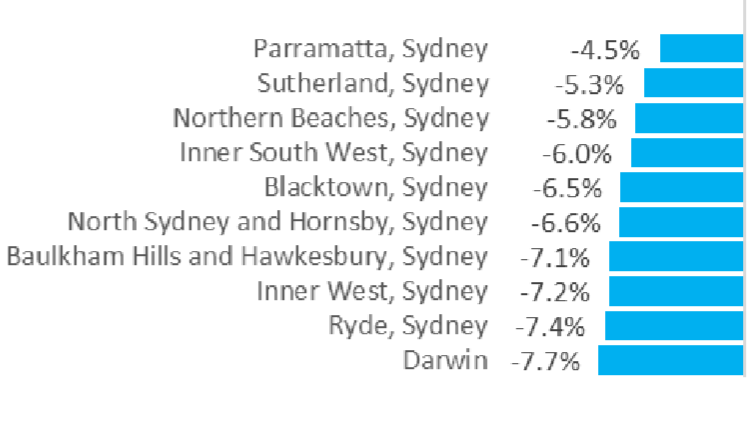

Meanwhile, some of the value falls across Sydney have been been pronounced:

Advertisement

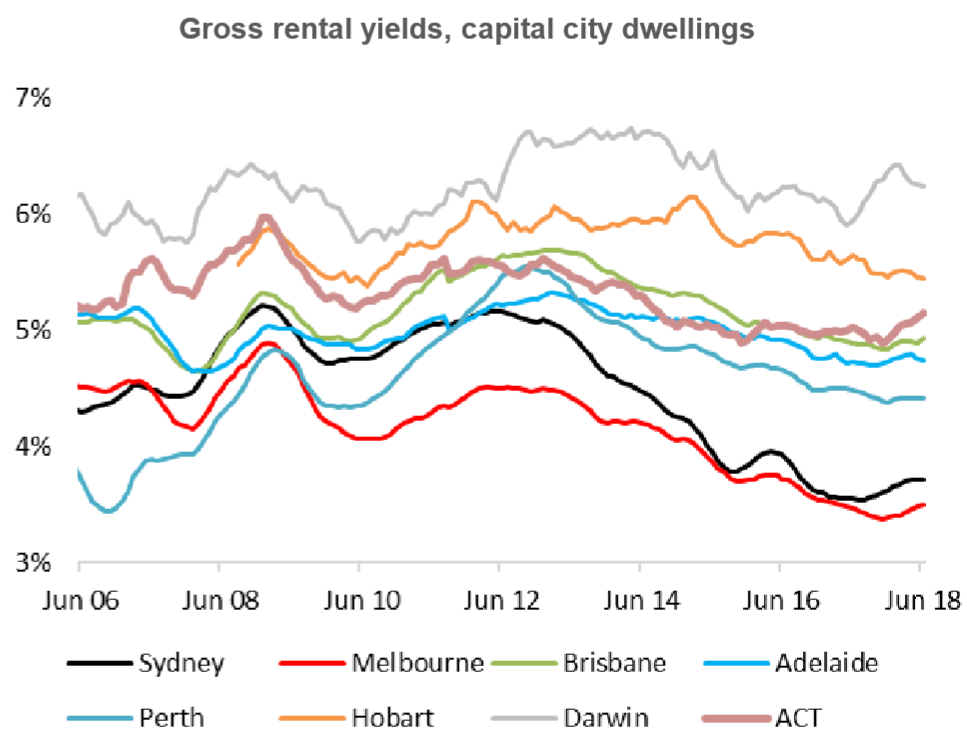

On the flipside, falling dwelling values has lifted rental yields from historical lows; albeit investors are still relying on negative gearing to offset rental losses:

While capital city dwelling values have fallen by 1.6% over the financial year, rental rates have risen by 1.4%. Although rental growth is generally mild, with rents rising and dwelling values falling, gross rental yields are consistently trending higher; albeit from record lows in some cities.

The lowest yields have consistently been in Sydney and Melbourne, where high capital gains relative to sluggish rises in rents had previously compressed rental yields to all-time lows. Melbourne yields bottomed out at 2.88% in November last year and have since risen to 3.0%; the highest reading since April 2017. Similarly, in Sydney, gross dwelling yields bottomed out at 3.04% in August last year and have since trended higher to reach 3.21%.

Despite the improvement, gross yields remain historically low, implying that most investors would be offsetting their cash flow losses against their taxable income. Mr Lawless said, “With the prospects for capital gains being muted, at least over the short to medium term, this negative gearing strategy is likely to beless appealingtomany investors.”

A big fly-in-the-ointment not mentioned by CoreLogic is Labor’s negative gearing and capital gains tax reforms, should it win the upcoming federal election, as well as the epic interest-only mortgage reset. Both will act as lead weights for the housing market.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.