Via the AFR:

Magellan boss and Rich Lister Hamish Douglass is preparing for the possibility that the US 10-year Treasury yield breaks through 4 per cent in 12 to 18 months’ time, sparking a 30 per cent sell-off in global equities, should the US Federal Reserve find itself surprised by resurgent inflation.

While that sounds dramatic, it’s just as likely in the fund manager’s view that the Fed keeps tightening methodically and bond yields rise to 4 per cent, but in an orderly fashion and without an inflationary scare.

Even so, Mr Douglass believes there is a strong case for being more tactical. He has increased his cash weighting in the Magellan Global Fund to 18 per cent, the highest since 2009.

“Only conservative investors sleep well,” he says.

Mr Douglass’ strategy returned 16.9 per cent over 2017-18 after fees in Australian dollar terms, according to his annual investor letter released on Wednesday. Since inception, his $10 billion strategy has delivered average yearly returns of 11.6 per cent after fees.

“Markets and economies don’t always correlate,” Mr Douglass told The Australian Financial Review, but interest rates are the most important factor right now, “and the stronger the economic growth, the more uncertainty there is around interest rates”.

…”I would say this coming together of all-time-record asset prices, central banks withdrawing liquidity and a very large and late cycle fiscal stimulus is really throwing a very uncertain picture here of what could happen.”

I more or less agree with this. Though I am less bearish on bond rates, we’ve been taking profits in the MB Fund throughout the year given the Trump boom is based upon a temporary fiscal tailwind.

We retain decent exposure to the US given its late cycle earnings boom which combines with a weakening China and falling AUD to deliver the prospect of good late cycle returns.

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book.

Magellan has a few differences in philosophy to the MB Funds:

- Magellan runs 20-40 stocks in its global portfolio – with 5 major regions and 11 sectors Magellan is always going to be underweight a number of sectors and countries. It’s not a bad feature, Magellan are effectively stock-pickers with a broad universe. The MB fund has a different mandate – we invest in a broader universe of 60-80 stocks to give investors a more diversified exposure to world markets.

- Magellan charges a lot more, 1.35% + a 10% performance fee. Our fees are closer to 1% (depending upon the size of investment), with no performance fee.

- Magellan mix some asset allocation into their international fund by sometimes holding cash. Our view is different: we have an international share fund that is always fully invested, and then we have tactical funds that switch in and out of equities, bonds and cash. We figure that you are either tactically allocating across a diversified portfolio or you are buying direct shares – not half/half.

- Magellan is a unit trust structure with all of the usual opacity that that brings. MB funds are separately managed accounts with 100% transparency on all holdings and the underpinning research.

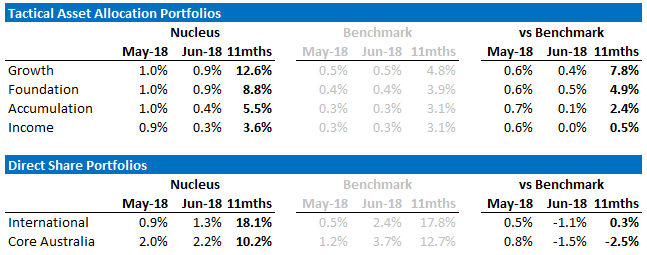

Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.