Via The Advisor:

Interest-only mortgagors are generally wealthier and have a higher risk appetite than other mortgagors, but they are increasingly turning to alternative sources of finance as lending criteria tighten, a Westpac economist has said.

Writing in a bulletin titled Profiling Australia’s ‘interest-only’ borrowers, Westpac senior economist Matthew Hassan and graduate William Chen looked at two data sets relating to owner-occupier loans before the introduction of APRA’s 30 per cent cap on the share of interest-only loans in 2017.

The report argued that, in many cases, the borrowers that are rolling off IO period will be facing increased repayments and may encounter difficulties refinancing against the backdrop of tightening lending criteria.

It noted that interest-only (IO) borrowers have experienced significant increase in mortgage rates between 2014 and 2016, being 46–58 basis points higher than their standard counterparts.

By using data from the Melbourne Institute’s Household, Income and Labour Dynamics in Australia Survey (HILDA), the researchers therefore sought to understand what a typical interest-only borrower looks like to “get a better idea of how some of these pressures might play out”.

The report suggested that just over 12 per cent of mortgagors had IO loan terms, accounting for 3.8 per cent of all households, down slightly on 2014 when just under 4 per cent had an IO loan. The report argues that this “likely reflects tightening lending conditions and the introduction of rate tiering measures from 2015 on”.

…Notably, the bulletin showed that less IO borrowers are ahead of repayments than other types of mortgagors (28.3 per cent compared to 56.4 per cent), which the researchers suggested could be an indication that interest-only borrowers have “less financial ‘headroom’ to make ahead of schedule repayments” and/or reflect that those with higher risk appetites may be more likely to put spare cash towards investment in yielding assets rather than service their mortgages ahead of schedule.

Those behind schedule are also higher than other types of mortgagors — 3.9 per cent versus 2.2 per cent. However, this marked an improvement from 2014 when 7.7 per cent of IO borrowers reported being behind schedule.

“This likely reflects the wider improvement in borrower quality seen in the income, employment and LVR profile of interest-only borrowers. An increased reliance on ‘alternate’ funding sources may also relate to tightening credit criteria and affordability pressures,” the report read.

Further, more IO borrowers are borrowing from others (friends, relatives, solicitors or community organisations) in order to help finance their home purchase, up from 5.4 per cent in 2014 to 7.9 per cent in 2016. This compares to a small decrease among non-interest-only borrowers over the same period.

“It is evident that some are having to resort to alternate sources of finance as lenders apply tighter lending criteria. Some would-be borrowers that have been unable to raise alternate funds have likely been squeezed out of the interest-only market.”

And there will be more.

This is the interest-only refinancing cliff that MacroBusiness has warned about for months.

In a nutshell, Australia’s banks can only issue 30% of new loans as interest-only now. That’s roughly $40 billion per quarter, which would mean that the reset dwarfs the banks’ entire front book interest-only capacity.

Therefore, some large portion will have to transpire in the back book. Our best guess for how much that will be is based upon the history of what the banks have managed previously. We’ve guessed the banks will be able to manage some $25 billion per quarter in the back book as the great reset builds. That means we’ll see the following total resets to principle and interest:

At the peak, that’s 3-4% of the loan book being shocked by 40% repayment hikes. It’s big.

It may also be appearing in the major banks mortgage arrears which have a big jump recently in 90-day buckets (though overall levels remain low):

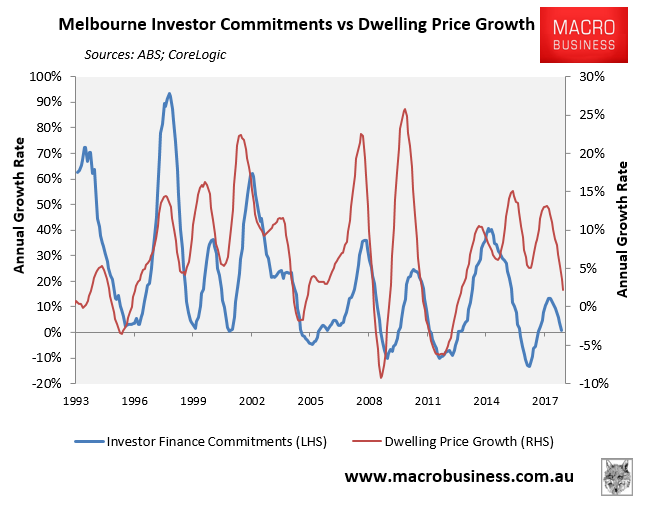

It also matters because the flow of investor mortgages is a key determinant of house prices growth, especially in the investor hotspots of Sydney and Melbourne, as illustrated clearly by the next charts:

Basically, falling investor demand means falling dwelling prices. And this is before Labor’s negative gearing and capital gains tax reforms are implemented, assuming it wins the next election, which will also smash the investor market.