The Australian Institute of Health & Welfare (AIHW) has produced a new report showing how the dream of home ownership is out of reach to growing numbers of Australians as the nation grapples with a chronic lack of affordable housing:

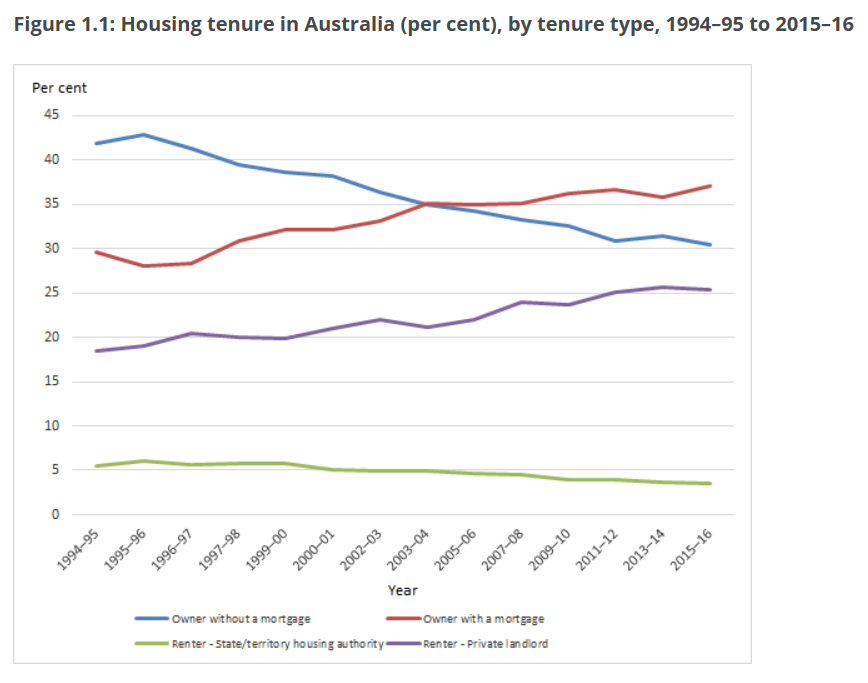

Over the last 20 or so years Australia has seen a shift from outright ownership to owning with a mortgage, and a shift from overall home ownership to private rental (SIH data: Figure 1.1). Between 1994–95 and 2015–16, the proportion of outright owner-occupied households fell from 41.8% to 30.4%. Comparatively, the proportion of households owning with a mortgage has increased, from 29.6% to 37.1%, over the same period. Overall, the proportion of households in home ownership fell from 71.4% to 67.5%. There has also been an increase in the proportion of households renting privately (from 18.4% to 25.3%), and a decline in the proportion of households renting through state and territory housing programs (from 5.5% to 3.5%)…

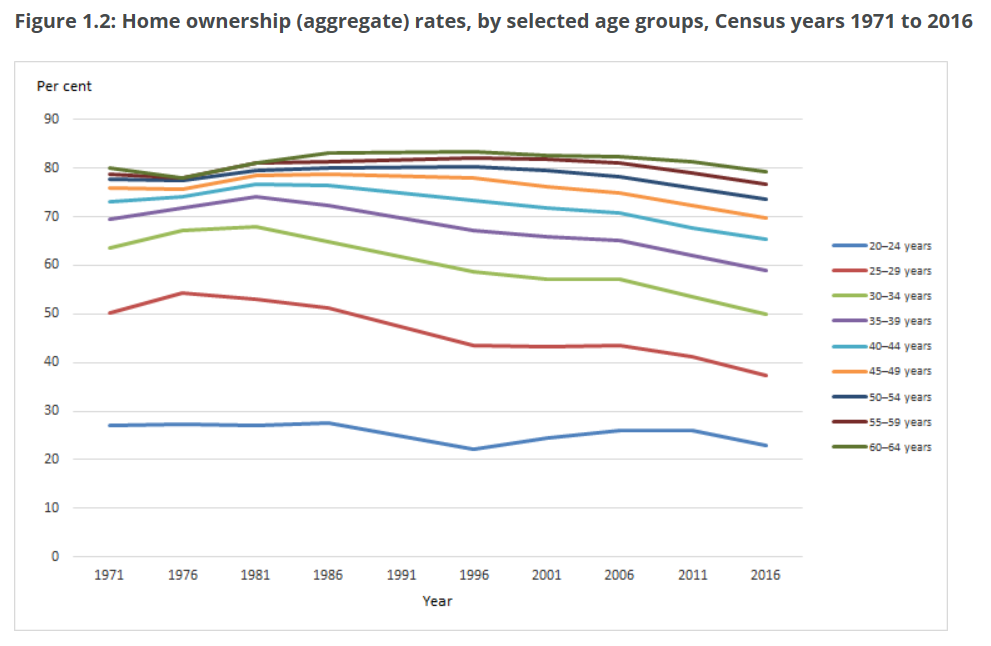

Figure 1.2 displays home ownership rates reported in Censuses in Australia between 1971 and 2016, by selected 5-year age groups. The home ownership rate of 30–34 year olds was 64%, and 50% for 25–29 year olds, in 1971. Forty-five years later these rates have decreased notably, with the home ownership rate of 30–34 year olds falling 14 percentage points to 50%. Similarly, that of 25–29 year olds fell 13 percentage points (to 37%). While declines are evident for other age groups they are much less marked.

Fewer Australians are tending to own their home at retirement. For Australians nearing retirement, for example, age groups 50–54, 55–59, and 60–64, home ownership rates peaked in 1996 at 80%, 82% and 83%, respectively (Figure 1.2). Since 1996 however, there has been a gradual decline in home ownership rates, most notably in the 50–54 age group which has seen a 6.6 percentage point fall over these 20 years (from 80.3% to 73.7%)…

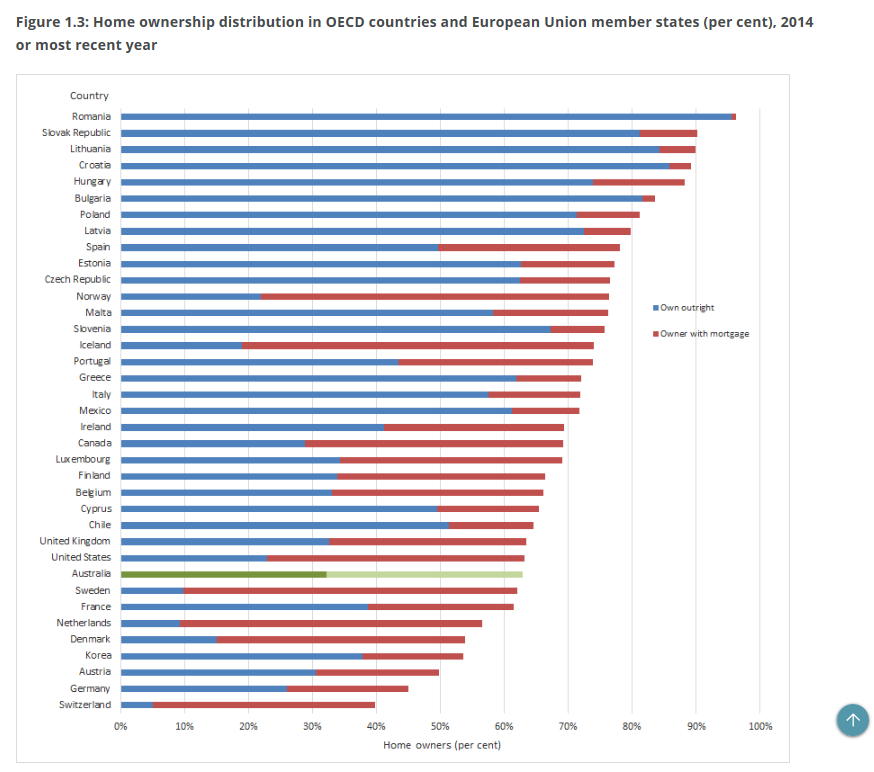

Despite changes in housing tenure over time, home ownership is still the most common tenure type in Australia, as it is in many other Organisation for Economic Co-operation and Development (OECD) countries and European Union (EU) member states [9] (Figure 1.3)…

While Australia ranks in the lowest quarter in terms of aggregate home ownership rates (twenty-ninth out of thirty-seven countries), it ranks in the top third for home owners with a mortgage (twelfth) (Figure 1.3)…

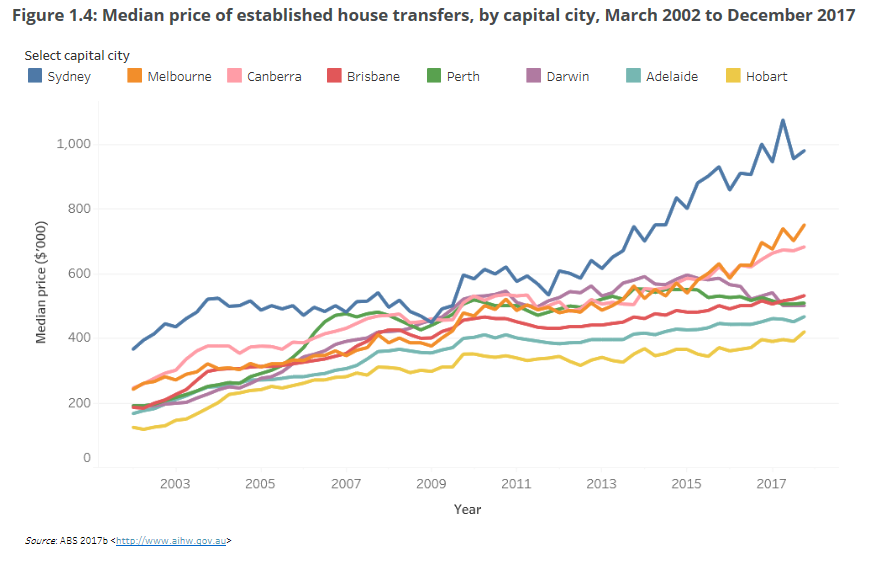

Based on the OECD’s price to income ratio index, housing affordability in Australia has broadly declined since the early 1980s, and the demand for sustainable, affordable housing continues to grow [11]. This demand puts pressure on dwelling prices, with a particularly adverse effect for low-income households. A number of factors influence house prices, such as interest rates, population growth, availability and release of land, and building approvals; therefore affecting housing affordability. House prices in Australia have increased substantially in recent decades…

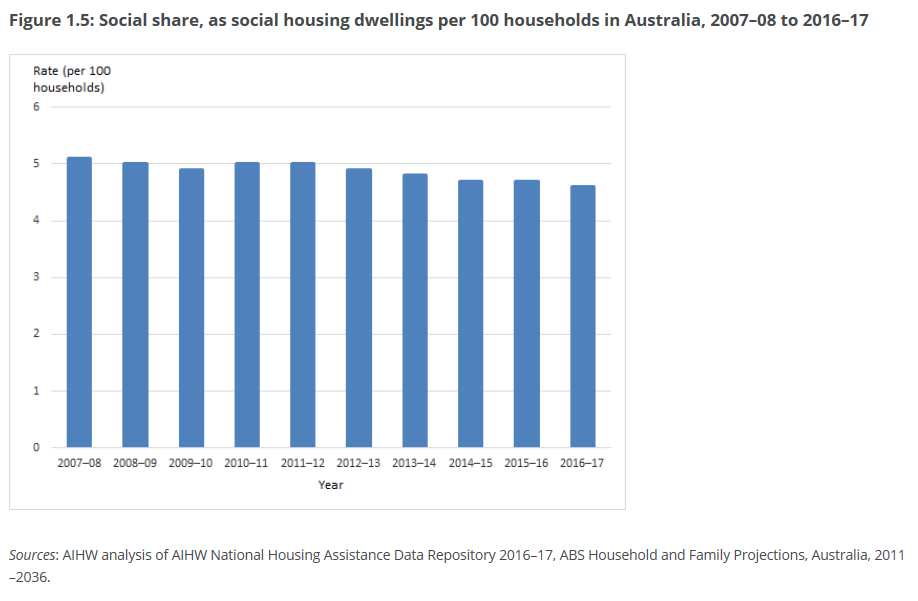

In recent years across Australia, the stock of social housing, which includes both public rental housing and community housing, has not kept pace with growth in either the overall national dwelling stock or the number of households.

The share of all dwellings in Australia accounted for by public rental housing (this does not include community housing) rose from 1981 to 1996 but has fallen since 1996… The number of social housing dwellings per 100 Australian households has declined from 5.1 per 100 households in 2007–08 to 4.6 in 2016–17 (Figure 1.5)…

What strikes me about the above is that Australia’s rate of home ownership is actually low by developed country standards. Other than that, there’s nothing in this report that we don’t already know.

Advertisement

If Australia’s policy makers genuinely wanted to ‘fix’ the housing affordability issue, they would tackle the following demand and supply-side distortions:

Normalising Australia’s immigration program by returning the permanent intake back to the level that existed before John Howard ramped-up it up in the early-2000s – i.e. below 100,000 from 210,000 currently [reduces demand];

Undertaking tax reforms like unwinding negative gearing and the CGT discount [reduces speculative demand];

Tightening rules and enforcement on foreign ownership [reduces foreign demand];

Extending anti-money laundering rules to real estate gatekeepers [reduces foreign demand];

Banning borrowing into property by SMSFs [reduces speculative demand]; and

Providing the states with incentive payments to:

undertake land-use and planning reforms, as well as provide housing-related infrastructure [boosts supply];

swap stamp duties for land taxes [boosts effective supply];

reform rental tenancy laws to give greater security of tenure [reduces demand for home ownership and reduces rental turnover]; and

force developers to supply housing for lower income earners via inclusionary zoning [boosts supply of affordable rentals].

Sadly, policy makers have no intention of actually fixing the problem and instead resort to policy band aids, like first home buyer subsidies, which make the situation worse and are designed as a new profit centre for the property industry.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.