Over the past week or so, Chinese policy makers have announced some rather extreme easing measures to combat the slowdown in train:

1. Renewed fiscal stimulus: The government will allow firms to deduct 75% of their research and development expenses from tax, which could save up to CNY 65 billion per annum. It will also accelerate disbursements of tax rebates, and CNY 1.35 trillion worth of funds for infrastructure spending.

2. Ramp up of the PBoC’s medium-term lending facility (MLF): The MLF is a facility designed to overcome collateral shortages in the interbank system. If financial institutions lack eligible collateral to repo with the PBoC in exchange for reserves, they can effectively lend first, creating collateral to be pledged with the Bank. If is a funding for lending scheme, or more appropriately, a lending for funding scheme. In recent days, the PBoC has made a record injection of liquidity into the system via the MLF.

3. Reserve requirement ratio (RRR) cuts: In June, the PBoC cut the RRR to 15.5% from 16% in an attempt to increase bank lending. Note that in China, authorities are able to use reserve rationing to control credit creation, because they do not target an official cash rate.

4. Further CNY devaluation. The USD/CNY has been managed, but allowed to rise through the technical 6.8 level.

Yesterday, markets responded favourably to the announcement of fiscal stimulus. Apparently, the change in intent was just as significant, if not more significant than details of the measures themselves (which are actually quite small). A-shares rallied strongly, while bonds and the currency sold off.

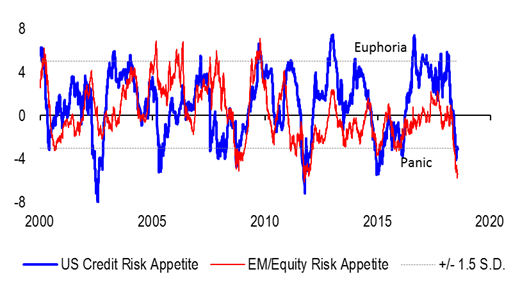

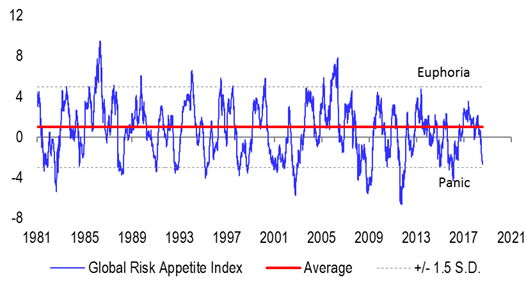

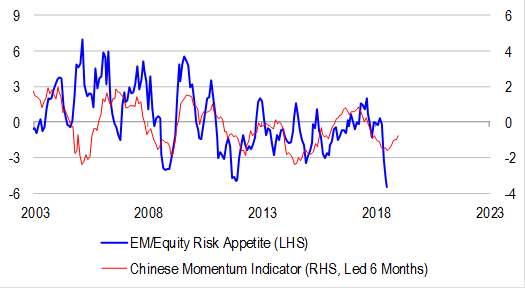

From a tactical perspective, we can understand the disproportionate sensitivity to good news. After all, emerging market (EM) or equity-only risk appetite has been in deep panic territory for some time, suggesting that EM equities have sold off too far, too quickly relative to developed market (DM) equities. They may not be cheap, but perhaps they have been oversold.

However, our analysis of asset allocation signals suggests that while there is room for risk appetite to bounce, it is unlikely to bounce very far, and is unlikely to turn outright positive. This is because:

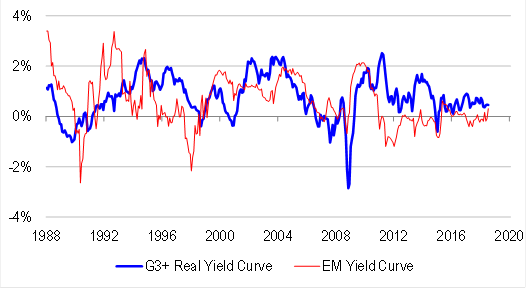

1. Even after the recent steepening of the global yield curve, the EM yield curve is less positively-sloped than the DM yield curve. In other words, bond market investors still perceive the EM growth outlook as being inferior to the DM growth outlook.

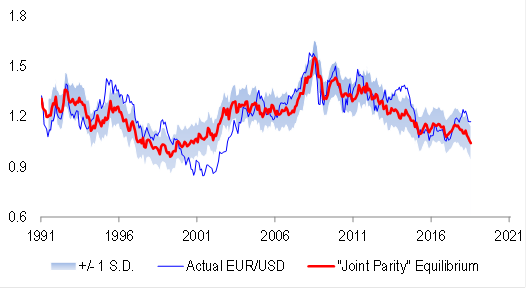

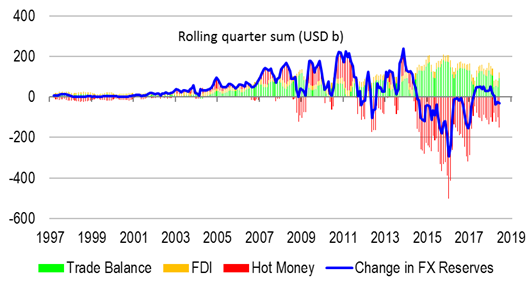

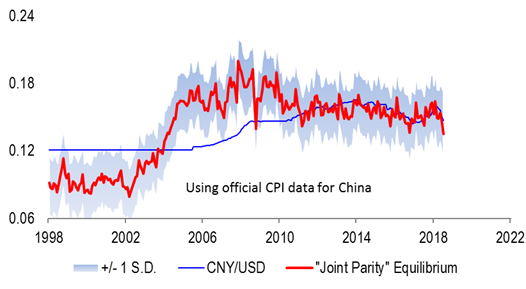

2. There is still a looming USD shortage in the world. CNY/USD and EUR/USD are materially above levels consistent with external balance, or “joint parity” equilibrium levels. The risk of further USD strength is a problem for the USD-dependent (or linked) EM complex.

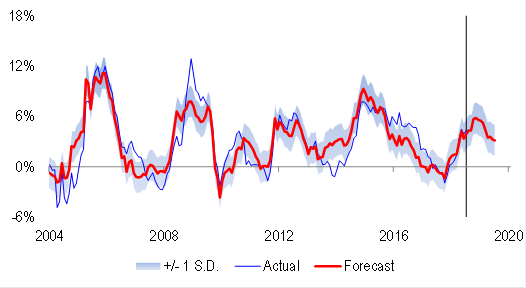

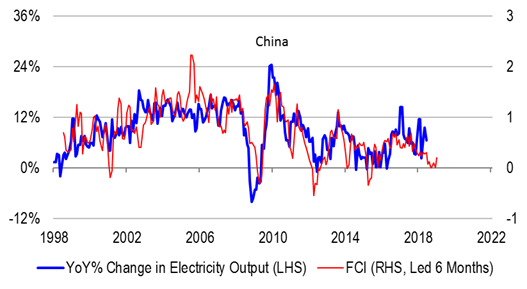

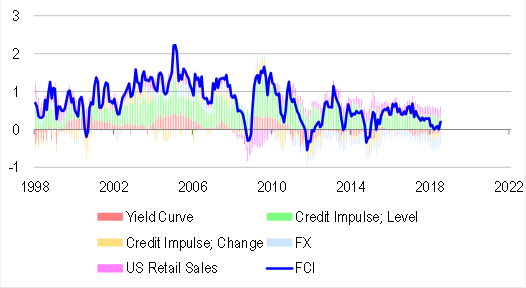

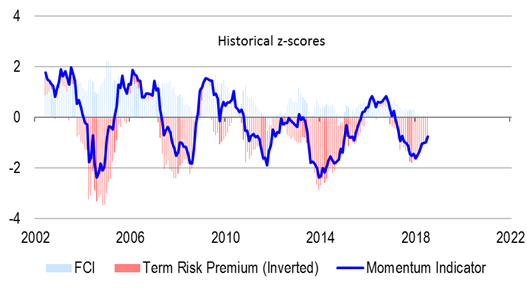

3. There is still considerable scope for Chinese bonds to rally, given that the term risk premium in bonds is meaningfully positive. There is also still a slowdown in growth ahead of us, because financial conditions are still relatively tight, even after considering the easing measures that have been announced.

US protectionism and CNY misalignment are still key risks to monitor

Abstracting from quantitative signals, we see several issues that still need to be resolved before declaring victory for Chinese policy makers. Unfortunately, we do not yet see sufficient progress on any of these fronts.

We welcome Chinese fiscal stimulus and monetary easing measures. More will be required, and probably has been signalled. Stimulus should serve to eventually stabilize financial conditions and growth. But currently, policy makers are caught in a Chinese finger trap. The binding constraint on growth is the elevated level of the CNY/USD. Any attempts to expand money supply through fiscal deficit spending or bank lending will necessarily put more downward pressure on the equilibrium level of the currency, rendering the CNY/USD even more expensive, and even more of a constraint on growth. Offsetting this dilution, or supply issue is demand. If the PBoC can somehow engineering a widening of real yield differentials with respect to the US, perhaps the improved carry trade appeal of the currency can help to stabilize it. In turn, this is a function of relative growth expectations, and what the Fed chooses to do as well.

Suffice to say, in the interim, the risk is that the Chinese will have to wait out a period of uncertainty, as the currency falls back to equilibrium, and stimulus is ramped up. Chinese authorities need to, and are, easing on all fronts as well as allowing the currency to fall. These easing efforts will not be immediately effective. As the currency falls, speculators may be emboldened to further run on the CNY. Hot money outflows could make domestic liquidity management much more difficult for the PBoC, as it ponders whether to let prices or quantities adjust in the system. But at some point, when the currency gets closer to equilibrium, these outflows should stabilize, and even return to inflows.

Again, we reiterate that the binding constraint on Chinese growth is the currency.

On the US side of the equation, the growth arithmetic is such that protectionism is too attractive a short-term win to pass up. Therefore, we expect more pressure to be exerted on China and its currency through foreign policy changes.

By definition, the sum of saving across all in an economy sectors (households, corporates, government and foreigners) must be zero. This is a national accounting identity. Re-arranging this identity, private sector saving must be equal to the trade balance plus fiscal deficits. Therefore to ease financial conditions for the private sector, or boost private sector saving, policy makers must engineer either larger fiscal deficits, larger trade surpluses, or at least, smaller trade deficits. And to boost equities specifically, corporate saving has to benefit disproportionately from this easing. In turn, this requires the household saving rate to flatten out or fall.

Viewed in this context, there may be some “method in the madness” of US President Trump’s policies. He has already tried large scale fiscal stimulus to ease financial conditions. With the impact of fiscal stimulus soon to peak, he is now trying protectionism to achieve the same effect, albeit at the expense of other nations. He is even making thinly-veiled criticisms of the Fed for raising rates too aggressively, because there is a risk that rate hikes will hurt asset prices and boost household saving, therefore putting a dent in the corporate sector and equities.

One possibility is that Trump may try even more fiscal stimulus. But this might embolden the Fed to raise rates even more aggressively. In the interim, the most “rational” lever to pull is trade protectionism, especially if the CNY devalues further. We suspect that this lever is ultimately not-so-rational, given that there is likely to be feedback from China back into the US, but these consequences are unlikely to take the limelight in the short-term.

For most countries, capital flows trump trade flows. For this reason, our global money markets expert Zoltan Pozsar has been more concerned about the re-plumbing of the Fed funds system, and balance sheet reduction than trade relations per se. But in the context of China, there is a strong case that trade flows matter just as much as capital flows. And if the US is going to become a smaller net importer of goods from China, the flipside is that it is also going to become a much smaller net exporter of USDs to pay for them. Herein lies the risk for the Chinese currency – a much greater USD shortage, bringing the elevated level of the CNY/USD back into focus.

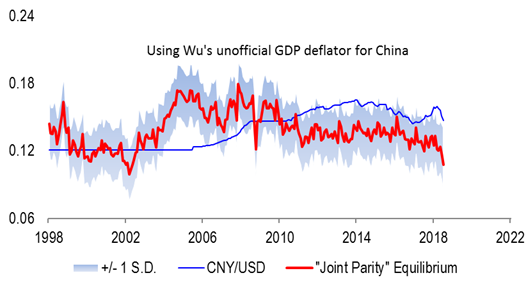

In our recent article, we constructed several different measures of the CNY/USD premium relative to equilibrium levels. If we believe the official CPI numbers from China, the premium is roughly 9%. But Chinese CPI and GDP deflators are well-known to be understated through time, and this artificially boosts purchasing power parity equilibrium. Using unofficial estimates of prices from academics (such as Harry Wu), it is possible that the premium could be as large as 30%. Either way, there is significant adjustment ahead for the currency. This adjustment process started in 2015, but did not finish there. There were interruptions over the past few years, because of Brexit (lowering the DM growth outlook relative to the EM growth outlook) and US fiscal stimulus (diluting the USD). But now, the interruptions have passed, and we are firmly in the end game.

Investment implications

Resource and EM stocks have received a boost from the announcement of Chinese fiscal stimulus. But we do not expect the boost to last. We are both encouraged and dismayed by the extreme force being used by the PBoC. On the one hand, it is a positive development that authorities are willing to use any and all measures to combat the slowdown and de-leveraging process in train. On the other hand, the extreme measures being used, and the dramatic about-face in policy stance suggests that the times are indeed dire, and that many of the constraints on growth in previous years have not gone away. Indeed, they may have become even more pressing, as the gravity of the situation is being revealed.

In our recent notes, we have explained our reasons for being underweight resources and banks relative to high quality industrials, and selected bond proxies.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.