Could not agree more. From the always excellent Damien Boey at Credit Suisse:

CNY and US Treasuries weaken together

Over the past few days, we have seen the CNY/USD depreciate sharply, and US Treasury yields spike higher. The two developments could be correlated. A weaker CNY implies that the PBoC is having to combat more capital flight, in turn requiring it to liquidate more USD reserve holdings to defend the currency peg. Most USD reserves are invested in US Treasuries, and so the flow impact is technically negative for bonds.

All of this said, there are some other developments worth noting as well that could have contributed to the recent spike in Treasury yields.

1. US 2Q GDP growth could print ahead of 5% annualized. A sharp upswing in net exports, and inventory build ahead of Trump’s tariffs are likely to contribute significantly to quarterly growth. If GDP does print this strongly, perhaps the Fed might be emboldened to hike further. Also, growth this strong should be inflationary.

2. The BoJ is considering a “reverse operation Twist”. It plans to increase purchases at the short-end of the curve, and taper purchases at the long-end, engineering a steepening of the yield curve.

For what it is worth, we are not firm believers that Chinese selling really matters for US Treasuries in the long-run. While we acknowledge the flow impact of a large holder of Treasuries selling out of its position, we doubt there is much of a permanent valuation impact. This is because the US Treasury does not require foreign funding in any way shape of form. The US Treasury spends on “over-draft” like terms with the Fed in the first instance. This action creates both deposits and (excessive) interbank reserves. To mop up the interbank liquidity consequences of spending (but not the deposit impact), the US Treasury conducts a secondary operation of bond issuance. Bond issuance is a sterilization exercise – not a funding exercise.

Moreover, whenever foreigners choose to buy US Treasuries, they bring to the table foreign currency. Foreign currency is not useful for funding the US Treasury. Foreigners must first swap their foreign currency for USDs before buying Treasury securities. But this begs the question – where did the USDs come from in the first place? And the inevitable answer is that USDs came from bank credit creation and fiscal spending. Once again, the US Treasury does not need foreign funding. Indeed, it, and the banking sector help to fund foreign purchases of USD-denominated securities!

Therefore, there is no funding, or default risk associated with US Treasuries. We need not fear foreign funding drying up, whether from the Chinese, Japanese, Russians or OPEC.

Is CNY devaluation inflationary or deflationary?

The key issue in our view is not the technicalities of Chinese selling. Rather, what we need to grapple with is whether prevailing Chinese trade and currency dynamics are inflationary or deflationary. If inflationary, perhaps US Treasury yields should be higher. But if deflationary, we should expect the recent spike in yields to be temporary.

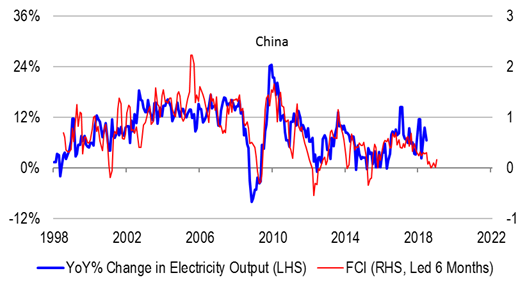

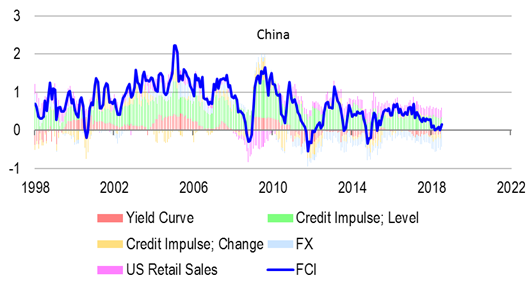

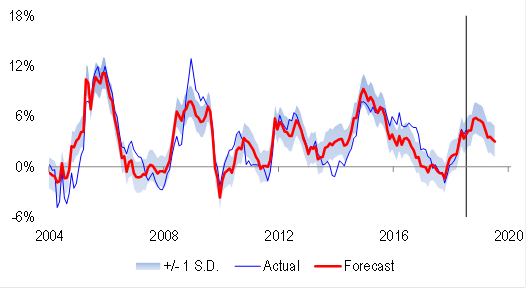

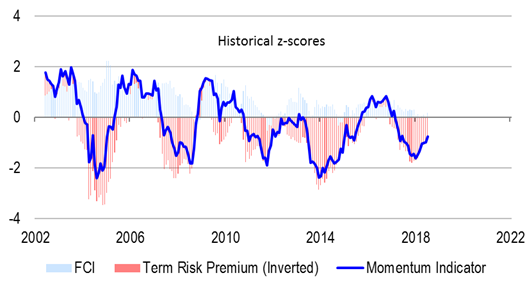

Recently, we introduced our new Chinese momentum indicator based on the difference between:

1. A forward-looking assessment of financial conditions and growth.

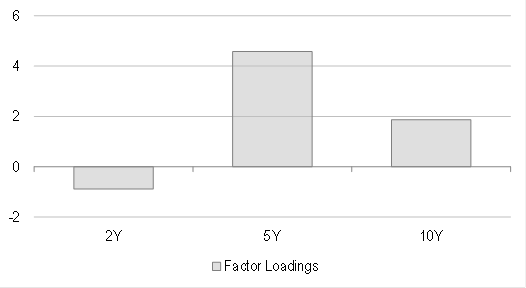

2. The term risk premium in Chinese bonds – a year-ahead predictor of bond returns, based on a non-linear combination of historical yields alone.

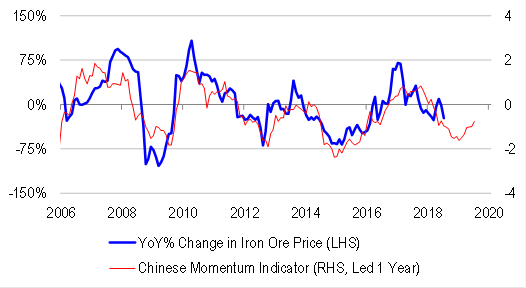

For further discussion, please see our article “Resources and emerging market weakness – tail end of panic, or tip of the iceberg” dated 18 July 2018. The momentum indicator leads commodity prices by a year. Currently, the indicator is firmly negative, consistent with commodity prices falling significantly in the period ahead. To be sure, momentum has turned less negative of late, as some adjustment has started to take place in Chinese currency and fixed income markets. But it is still negative, consistent with weakness ahead.

Therefore, China is likely to drive and export deflation in the near-term.

Arguably, US developments offset this. After all, the labour market is very strong, consistent with solid wage inflation. Labour productivity has ground to a halt, partly on the back of poor demographics, but partly also because of underinvestment. Unit labour costs (wages per unit of output) could easily rise by 3% per annum or more, driving up CPI inflation.

But labour costs are not everything. Lower commodity prices could take the edge off CPI inflation in the near-term. Also, we are wary of feedback. The US is not a closed economy. Weakness in China could eventually feedback into weakness in the US, especially if property buying slows. And we note that real private sector credit growth has been soft of late, making the economy quite susceptible to external shocks.

Investment implications

We are long quality exposures and selected bond proxies. We are underweight resources. This is because we see more deflation coming from China. Also, we are prepared to look through the noise created by short-term liquidation of Treasury holdings.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.