It seems Michael Pascoe’s move to the New Daily, after getting dumped by Fairfax, hasn’t stopped the housing spruiking. Yesterday, Pascoe penned another article lambasting us from the “Doom & Gloom Brigade” (DGB) for being concerned about Australia’s extreme household debt:

[Here’s a] graph that tells you a lot about the real story. Unfortunately it’s a little old, as the RBA stopped including it in the bank’s monthly chart pack, replacing it with the graph of gross debt and house prices.

What counts most about debt is its serviceability, rather than its absolute size. What this graph shows is that while our gross debt has soared, what it costs us in interest (as a percentage of household disposable income) is about as low as it has been in 14 years.

One is left to speculate about why the RBA would stop issuing this graph. It would be churlish of me to suggest it was because the bank was a little embarrassed about the obvious correlation of cheap money and sharply higher gross debt.

The ‘DGB’ (Doom & Gloom Brigade) will be quick to shout a couple of things at this point.

Firstly, the debt might look cheap to service now with interest rates at record lows, but when rates rise, it will hurt like hell.

‘We’ll all be rooned’

And, secondly, all this discussion is about the average household and averages hide a lot of reality. The average household might be doing fine, but there are plenty of people who have borrowed as much as they can that leaves them little leeway if their circumstances change.

On the first point, the RBA is fully aware of the risks, which is why rates aren’t going up here until wages are rising enough to be able to handle it. And, even then, rates won’t be rising much.

The RBA has already told us that when wages growth is hunky-dory again and the economy is absolutely tickety-boo, its cash rate should only be 200 points higher. The authorities already require banks to check that a borrower could handle another couple of per cent on their home loans.

Also, as the RBA minutes allude, much of the household debt is held by people who are fairly well off and can afford the risk anyway.

The DGB’s second point is valid. There are and will always be some people close to the edge who will suffer when things change – a job loss, sickness, divorce, perhaps dropping back from two incomes to one.

There also are property investors who bite off a bit more than they can chew when they find property prices don’t always keep going up rapidly.

But that’s capitalism – borrowing to buy a home can’t be guaranteed to be a painless and sure thing.

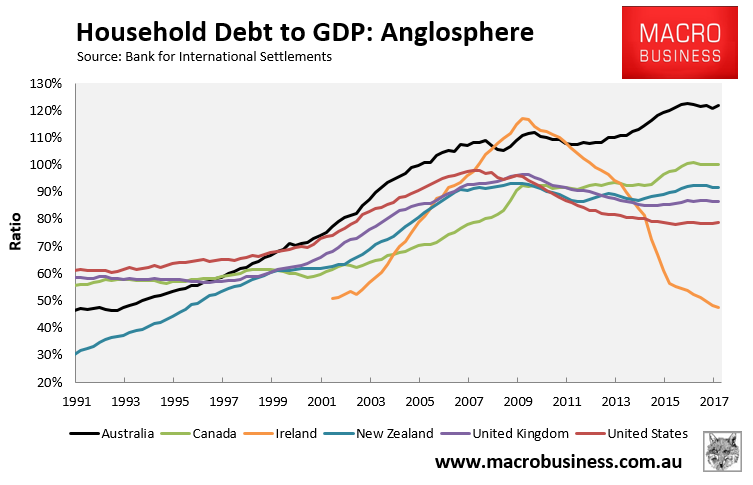

Pascoe might want to familiarise himself with the Bank for International Settlements’ (BIS) global data on household debt. Not only does it show that Australia’s household debt is the second highest in the world (behind Switzerland), and way above the other Anglosphere nations:

Advertisement

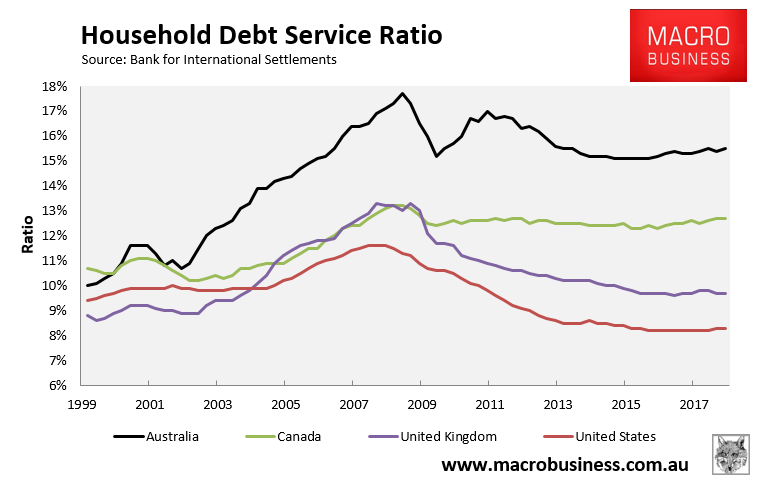

But also that that Australia’s average principal and interest repayments as a percentage of household disposable income – called the household debt servicing ratio (DSR) – is the world’s second highest, and again way above the other Anglosphere nations as well as late-1990s to early-2000s levels:

Advertisement

According to the BIS, the DSR is considered “a reliable early warning indicator for systemic banking crises”, whereby “a high DSR has a strong negative impact on consumption and investment”.

Moreover, despite Australia’s interest rates cratering to record lows, which has lowered interest repayments, the DSR remains very high, thanks to increased principal repayments. Therefore, should interest rates rise even modestly, then obviously Australia’s DSR would surge. And it wouldn’t take much to push it above the pre-GFC peak.

DFA’s Martin North has also taken Pascoe to task via YouTube:

Advertisement

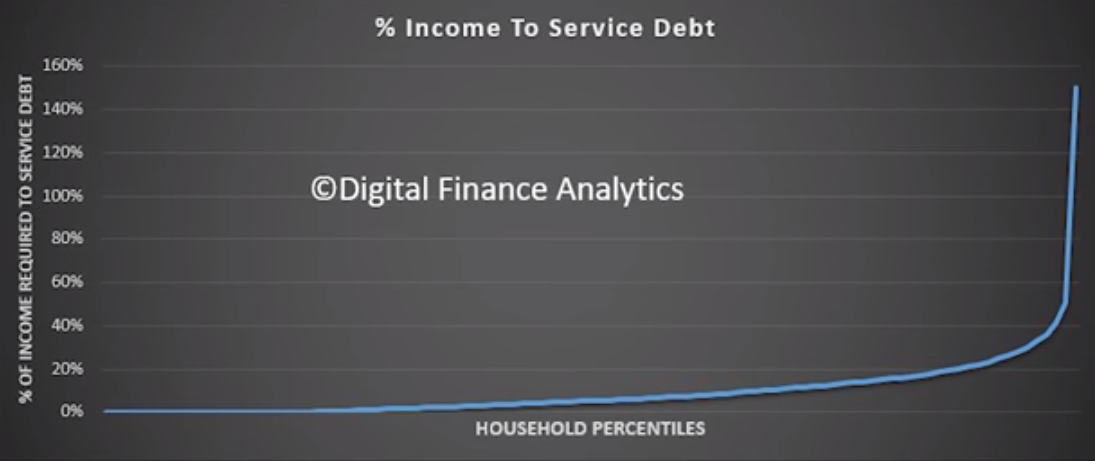

North argues that while many households carry no debt and are not at risk of defaulting, there are a significant percentage teetering on the brink:

Advertisement

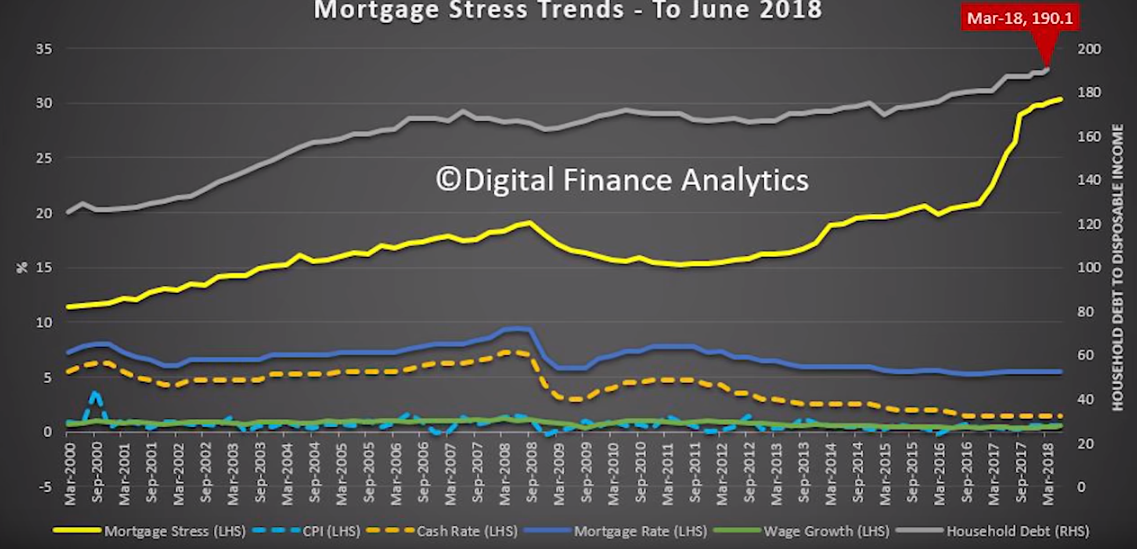

That is, some 30% of mortgage borrowers are in “stress” at current interest rates, representing around one million households:

Therefore, according to North, “it will be the marginal borrower that triggers problems down the track, as we witnessed in the US during the GFC”.

Advertisement

Michael Pascoe can spin Australia’s household debt situation all he likes. But at the end of the day, Australia’s debt explosion has left the nation – and our banks – in a precarious position if/when interest rates finally rise.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.