Digital Finance Analytics (DFA) has released the June 2018 mortgage stress and default analysis update.

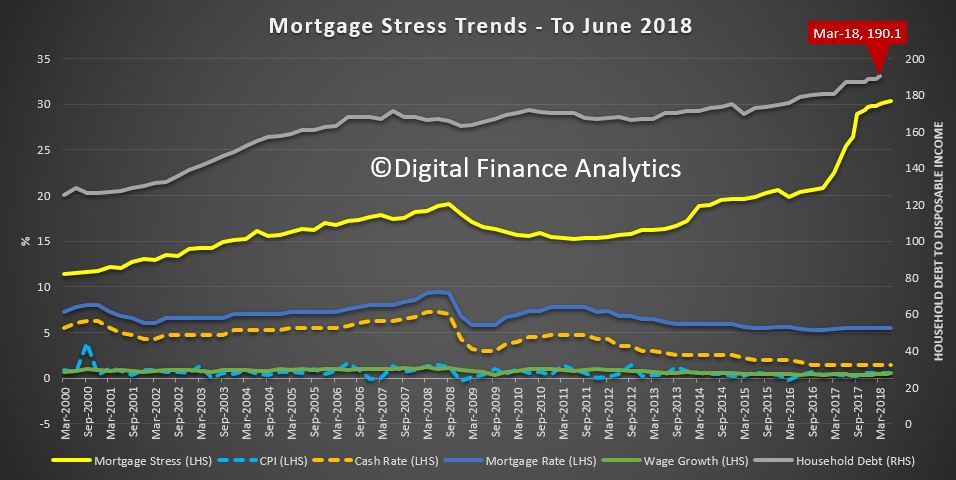

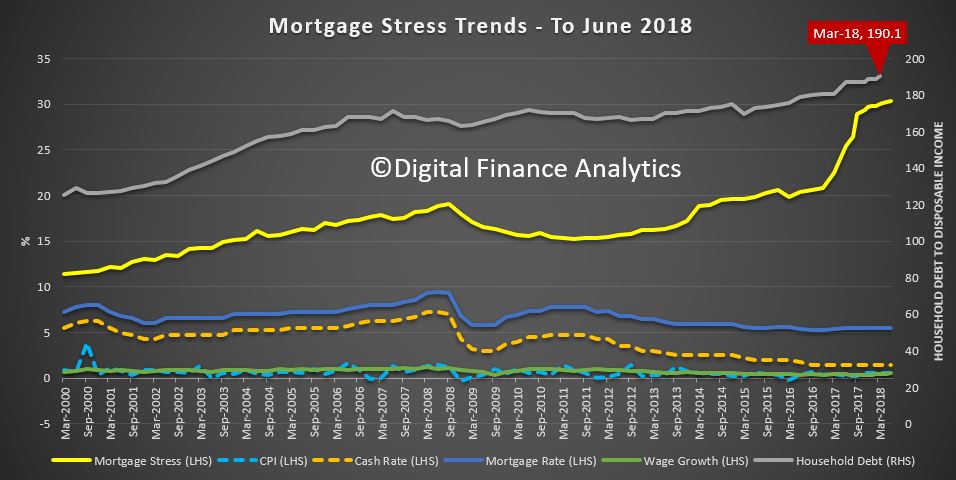

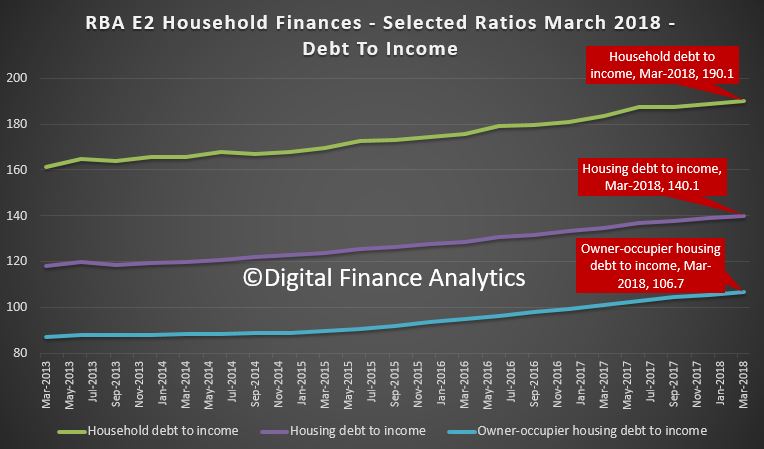

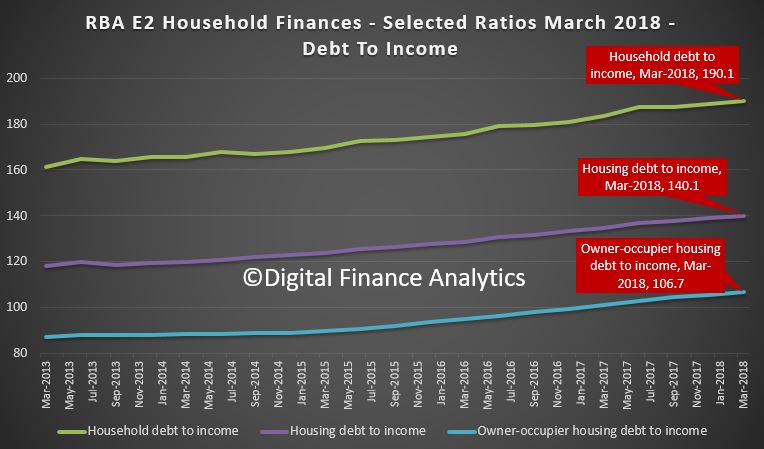

The latest RBA data on household debt to income to March reached a new high of 190.1 [1] …

… so no surprise to see mortgage stress continuing to rise. Across Australia, more than 970,000 households are estimated to be now in mortgage stress (last month 966,000). This equates to 30.3% of owner occupied borrowing households. In addition, more than 22,000 of these are in severe stress. We estimate that more than 57,100 households risk 30-day default in the next 12 months. We expect bank portfolio losses to be around 2.8 basis points, though losses in WA are higher at 5.2 basis points. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates.

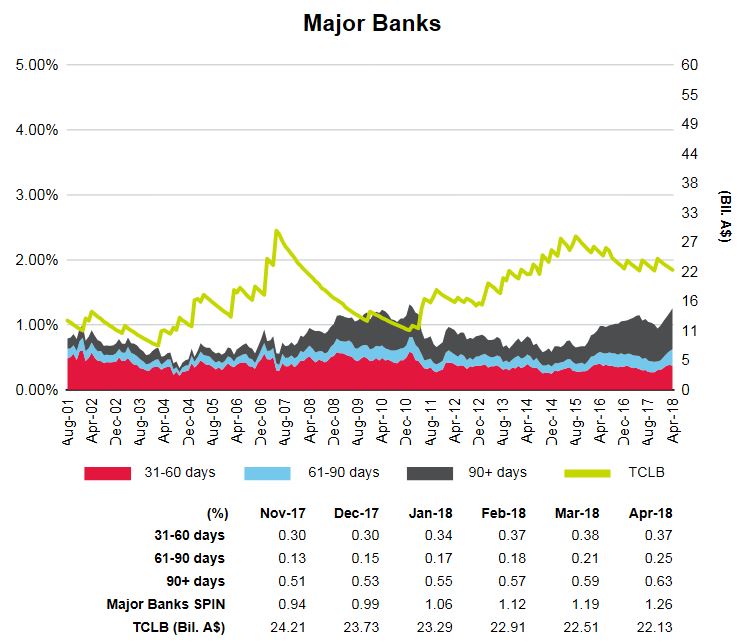

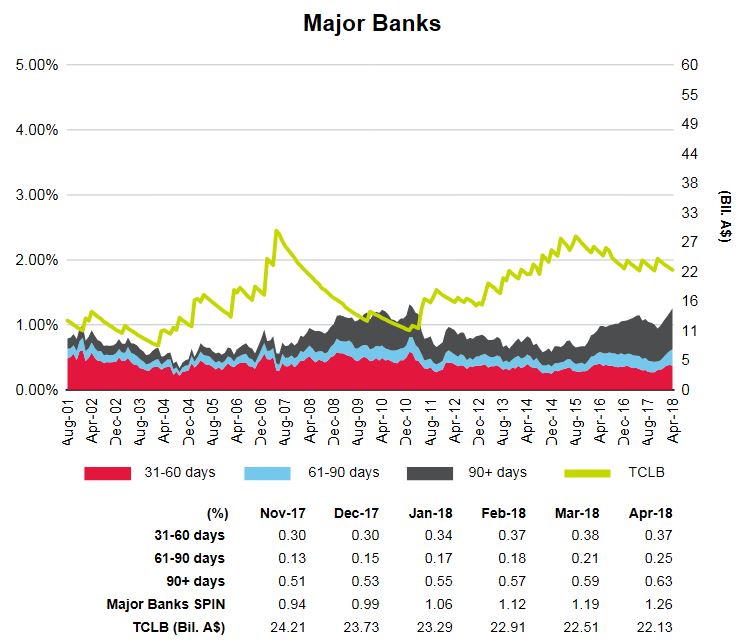

The latest S&P Ratings data shows a rise in 90 day plus delinquencies in the SPIN series for April, from the major banks. So despite the fact it only covers MBS mortgages the trend is consistent with our stress analysis!

The inevitable result of too lose lending standards and easy loans is creating an intractable problem for many households given the continued low income growth, high cost environment. This also means risks to lenders continue to rise.

Our surveys show that more households are keeping their wallets firmly in their pockets as they try to manage ever tighter cash flows. This is an economically significant issue and will be a drag anchor on future growth. The RBA’s bet on sustained household consumption looks pretty crook. Even now, household debt continues to climb to new record levels, mortgage lending is still growing at an unsustainable two to three times income. Falling home prices just adds extra picante to the problem.

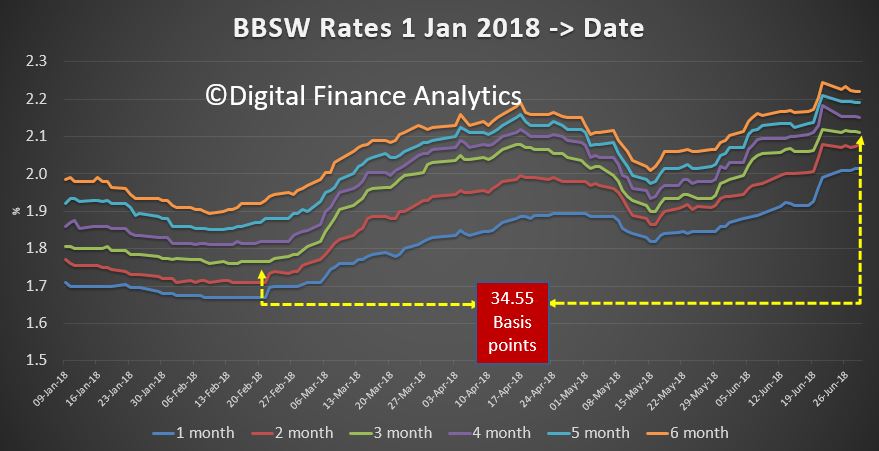

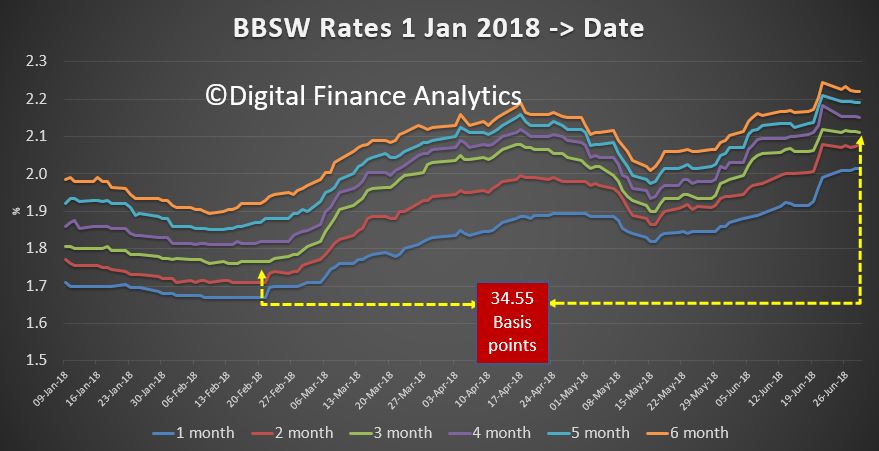

We continue to see households having to cope with rising living costs – notably child care, school fees and fuel – whilst real incomes continue to fall and underemployment remains high. Households have larger mortgages, thanks to the strong rise in home prices, especially in the main eastern state centres, and now prices are slipping. While mortgage interest rates remain quite low for owner occupied borrowers, those with interest only loans or investment loans have seen significant rises. Rate pressure will only increase as higher Bank Bill Swap Rates (BBSW) will force more lenders to lift their mortgage rates, as a number of smaller players already have done.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end June 2018. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Households are defined as “stressed” when net income (or cash flow) does not cover ongoing costs. They may or may not have access to other available assets, and some have paid ahead, but households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell.

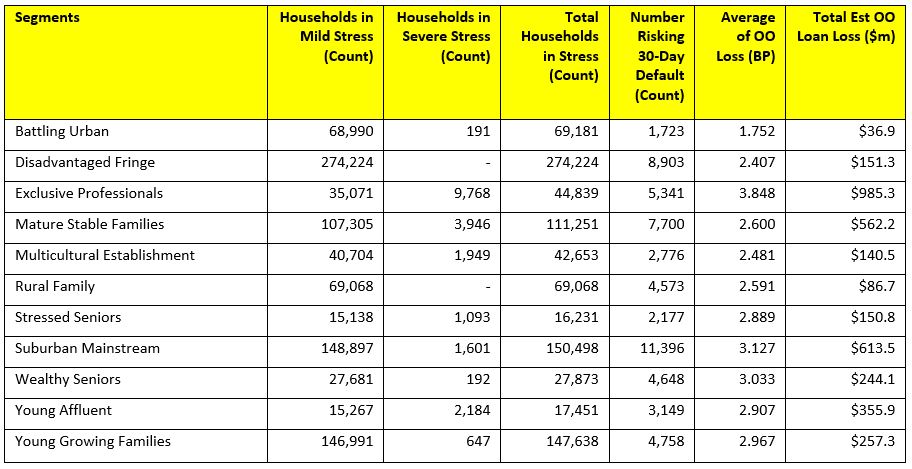

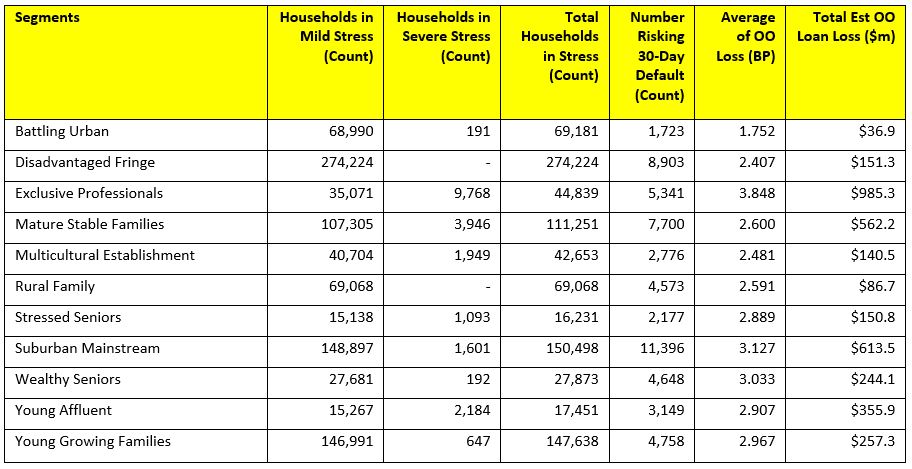

Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes. Our Core Market Model also examines the potential of portfolio risk of loss in basis point and value terms. Losses are likely to be higher among more affluent households, contrary to the popular belief that affluent households are well protected.

Stress by The Numbers.

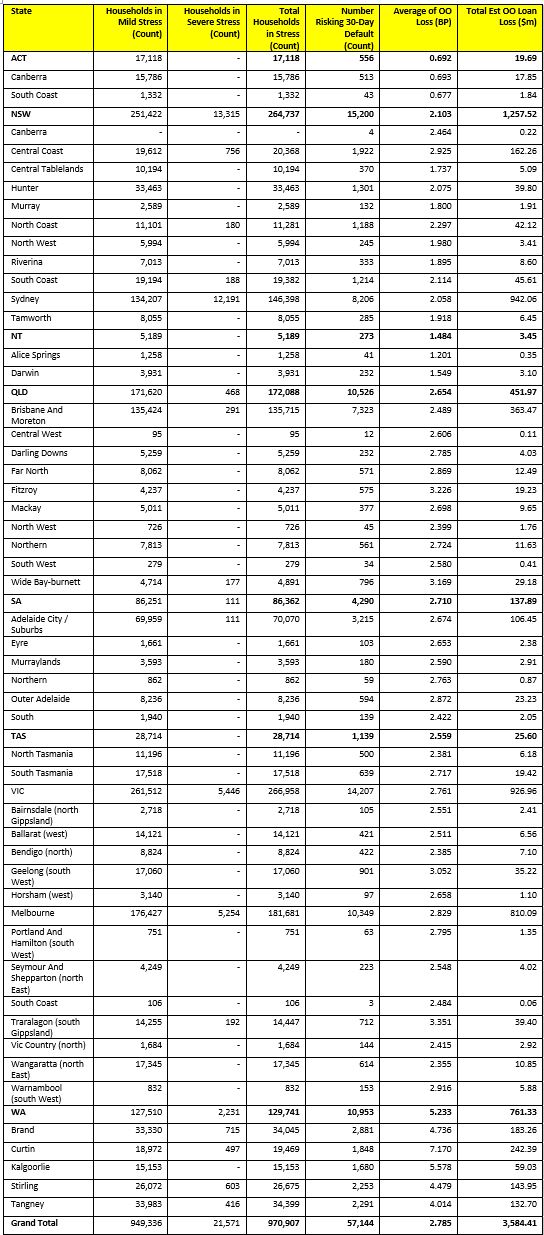

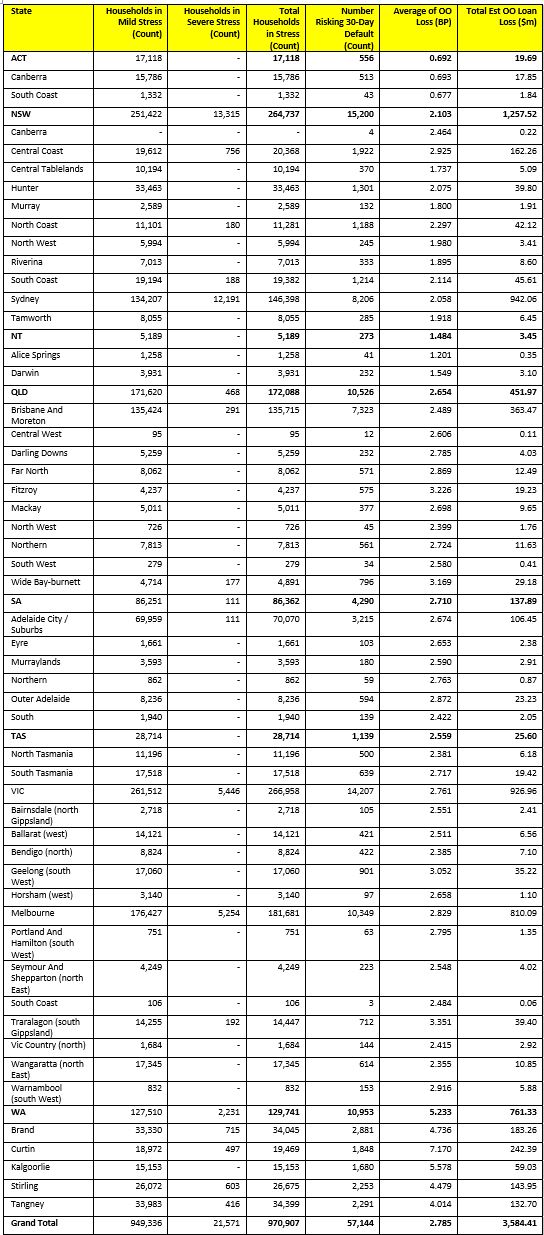

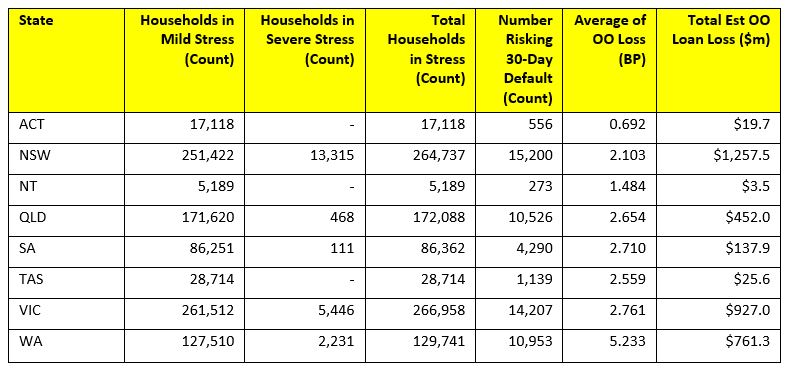

Regional analysis shows that NSW has 264,737 households in stress (264,344 last month), VIC 266,958 (271,744 last month), QLD 172,088 (164,795 last month) and WA has 129,741. The probability of default over the next 12 months rose, with around 10,953 in WA, around 10,526 in QLD, 14,207 in VIC and 15,200 in NSW.

The largest financial losses relating to bank write-offs reside in NSW ($1.3 billion) from Owner Occupied borrowers) and VIC ($927 million) from Owner Occupied Borrowers, which equates to 2.10 and 2.76 basis points respectively. Losses are likely to be highest in WA at 5.2 basis points, which equates to $761 million from Owner Occupied borrowers.

A fuller regional breakdown is set out below.

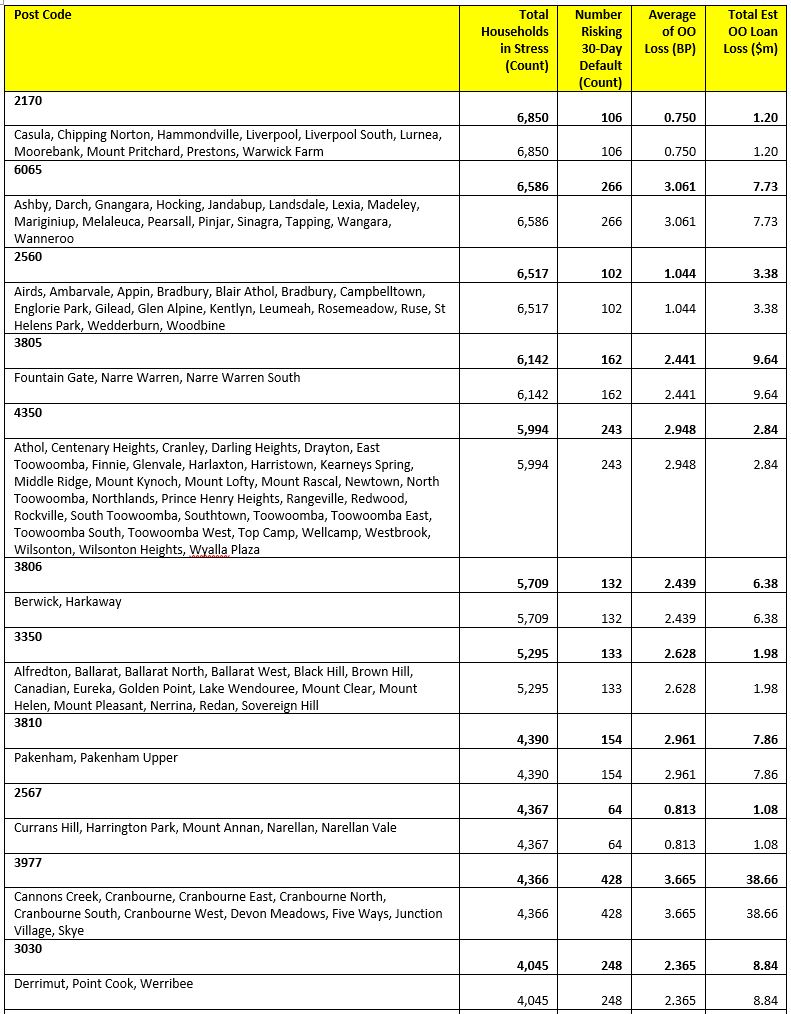

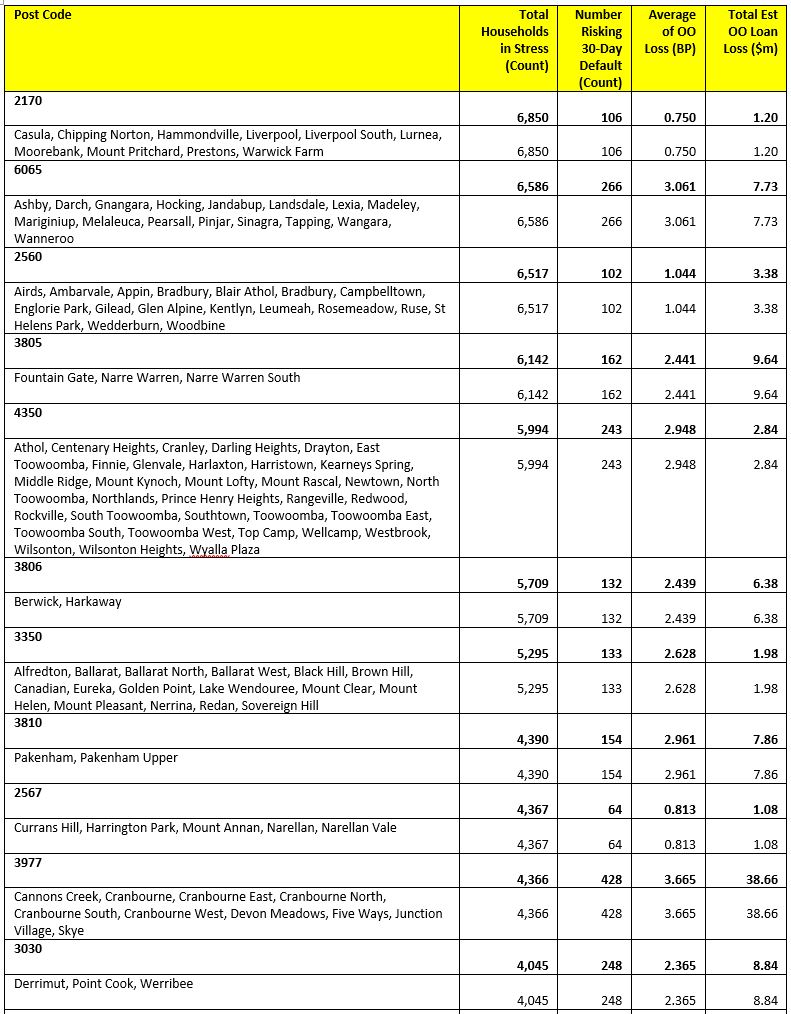

Here are the top 20 postcodes sorted by number of households in mortgage stress.

That recent spike in 90 day arrears at the major banks looks like refi failure as interest-only resets.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

The latest RBA data on household debt to income to March reached a new high of 190.1 [1] …

… so no surprise to see mortgage stress continuing to rise. Across Australia, more than 970,000 households are estimated to be now in mortgage stress (last month 966,000). This equates to 30.3% of owner occupied borrowing households. In addition, more than 22,000 of these are in severe stress. We estimate that more than 57,100 households risk 30-day default in the next 12 months. We expect bank portfolio losses to be around 2.8 basis points, though losses in WA are higher at 5.2 basis points. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates.

The inevitable result of too lose lending standards and easy loans is creating an intractable problem for many households given the continued low income growth, high cost environment. This also means risks to lenders continue to rise.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end June 2018. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Stress by The Numbers.

The largest financial losses relating to bank write-offs reside in NSW ($1.3 billion) from Owner Occupied borrowers) and VIC ($927 million) from Owner Occupied Borrowers, which equates to 2.10 and 2.76 basis points respectively. Losses are likely to be highest in WA at 5.2 basis points, which equates to $761 million from Owner Occupied borrowers.

Here are the top 20 postcodes sorted by number of households in mortgage stress.