Australia

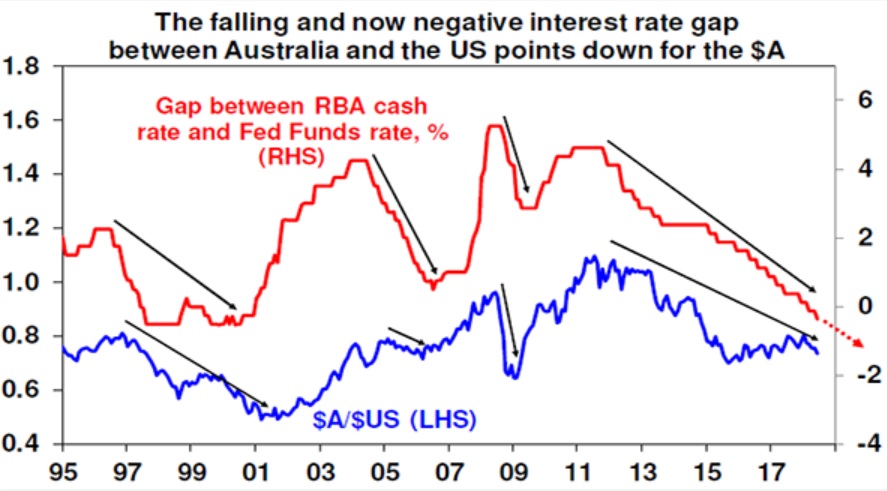

Australian dollar and yield differential RBA and US Federal Reserve

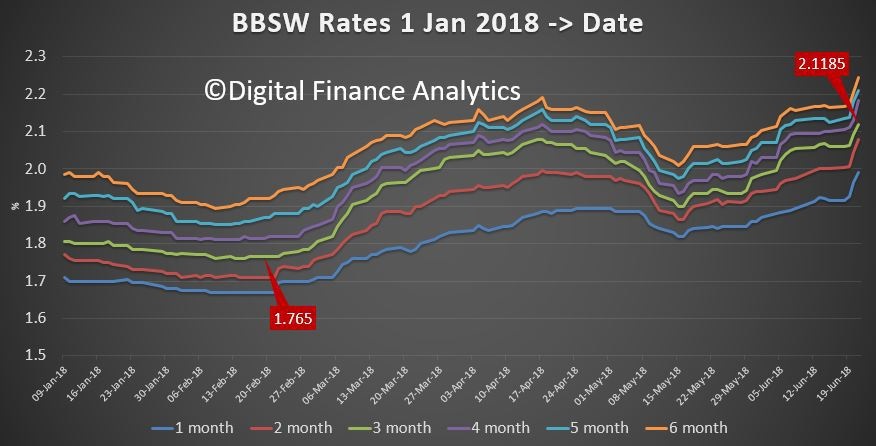

BBSW 2018

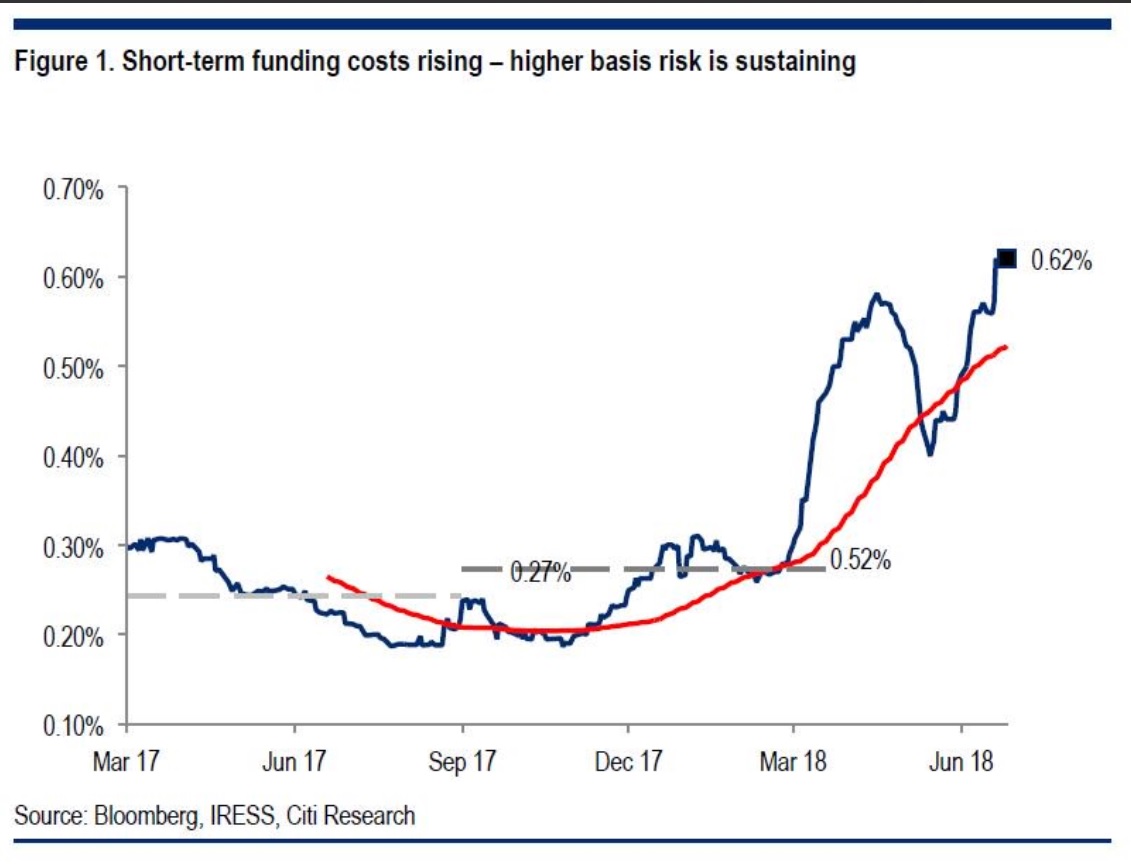

Australian Short Term Funding 2017 onwards

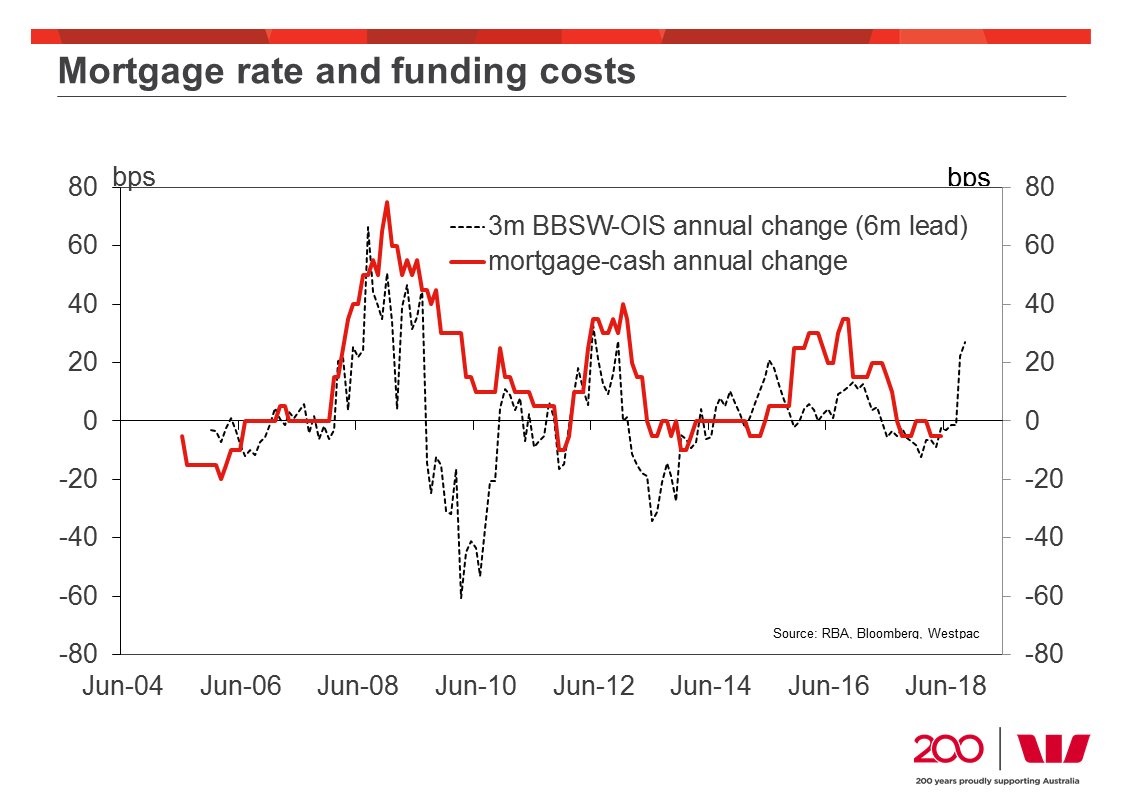

Funding Costs (BBSW) and Mortgage Rates

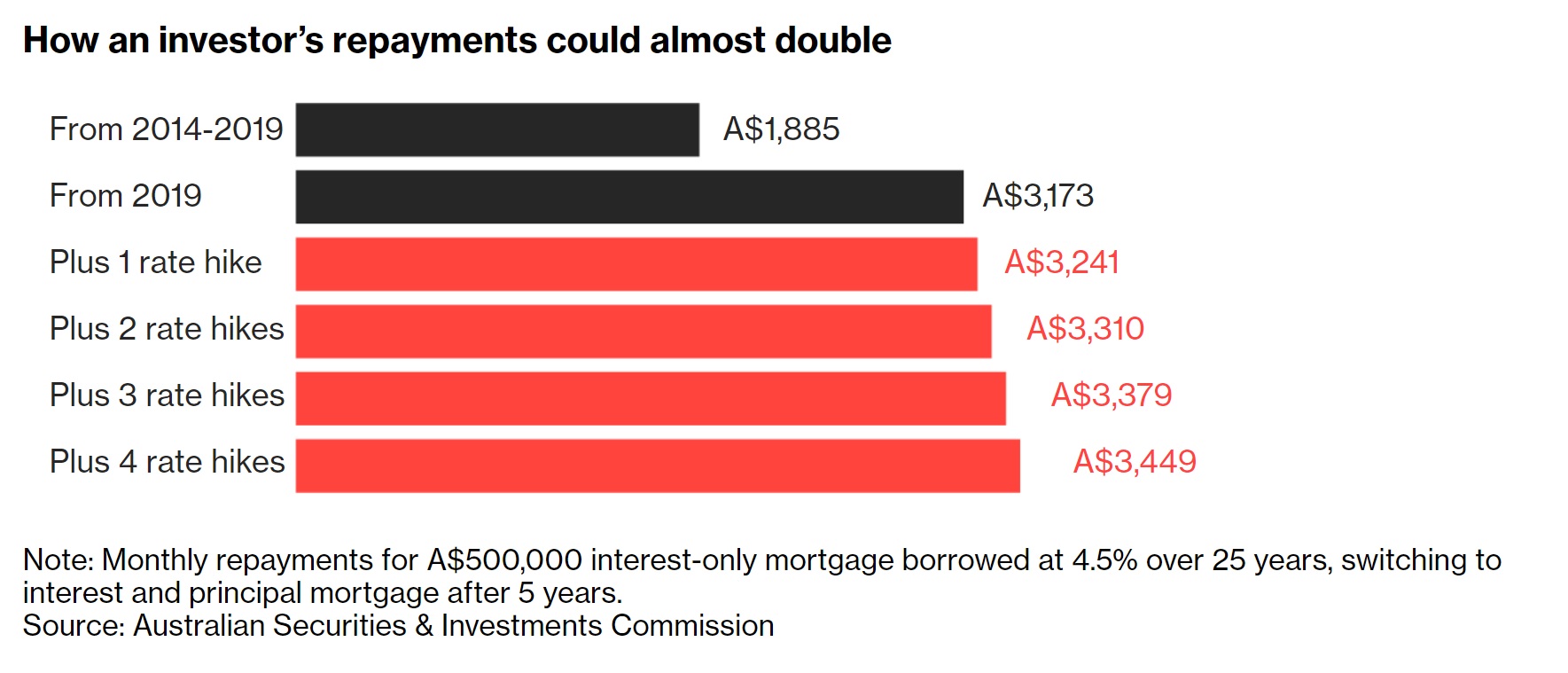

Australian interest rate hikes – potential implications for $500k mortgage

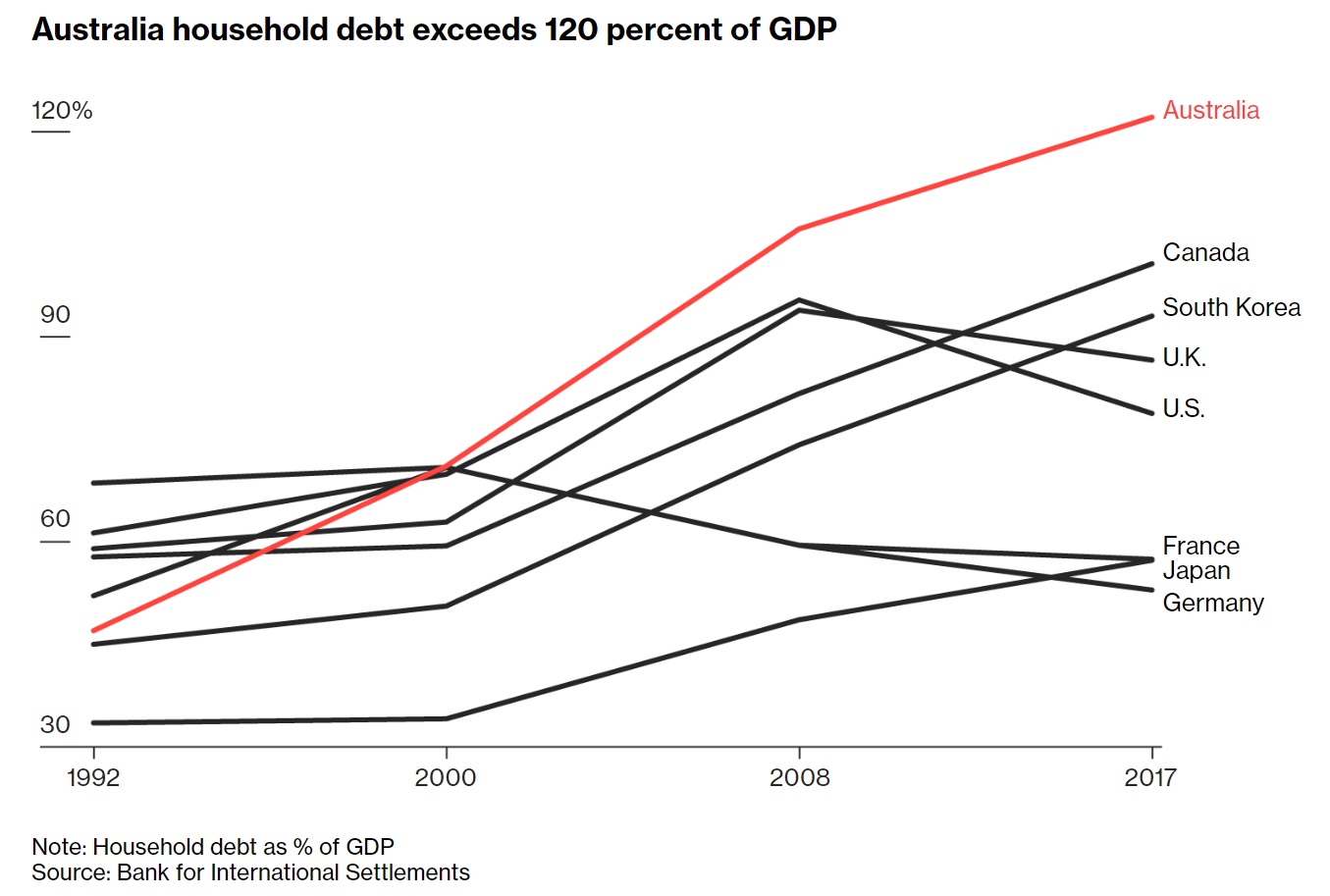

Australian Household Debt

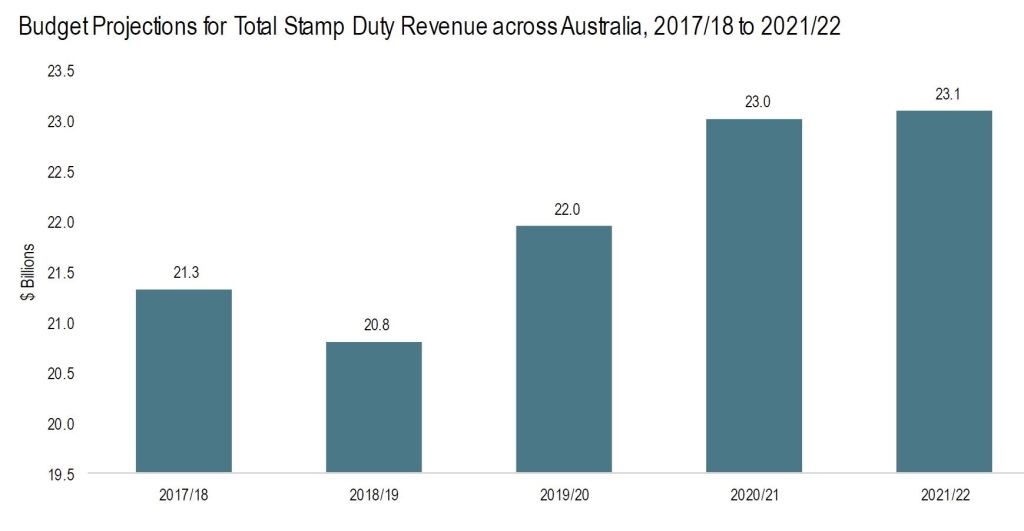

Budget projections for Stamp Duty Revenues

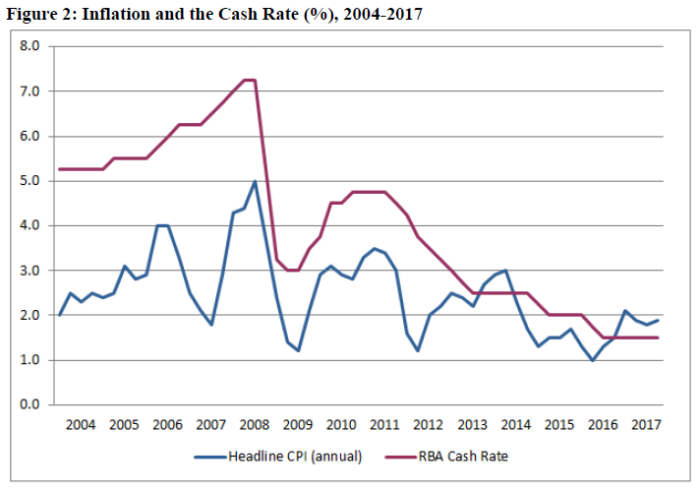

RBA Cash Rate and Australian CPI

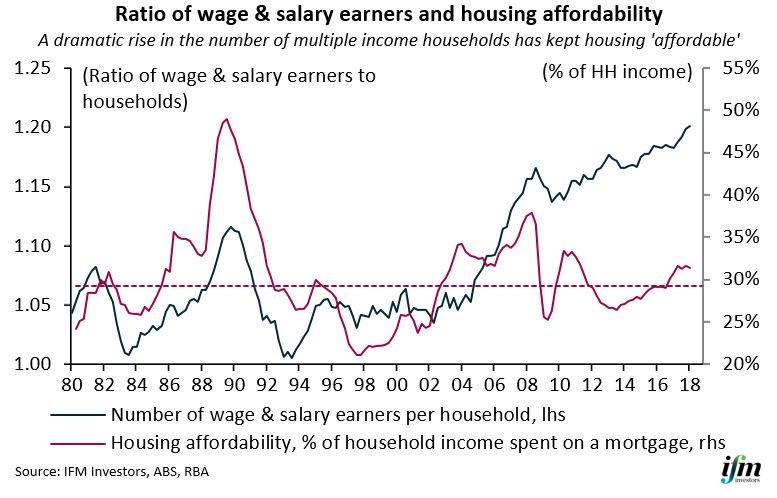

Affordability and Multiple Income Households

Housing Credit and Household Wealth

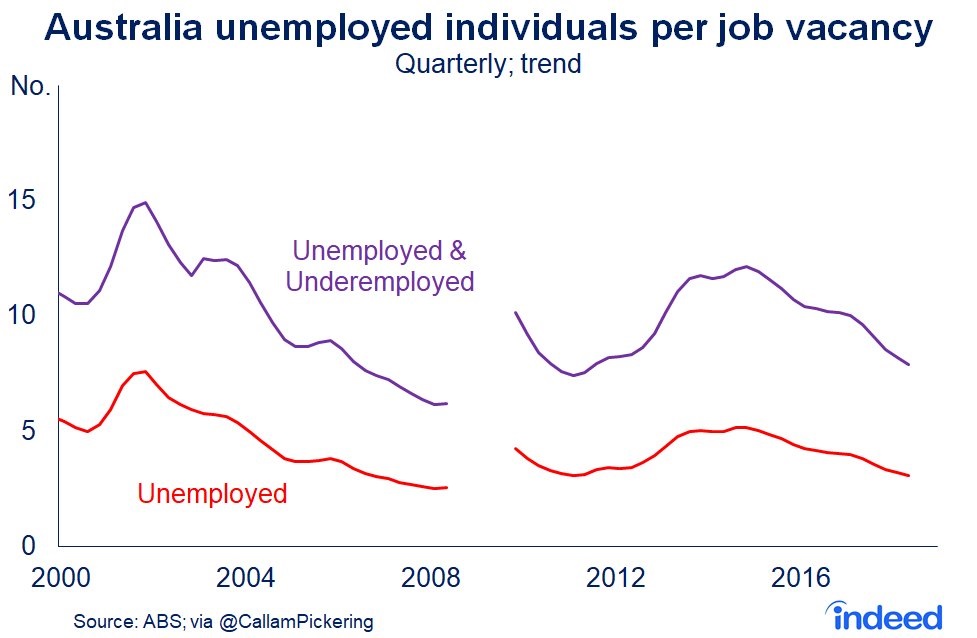

Australia – unemployed and vacant jobs

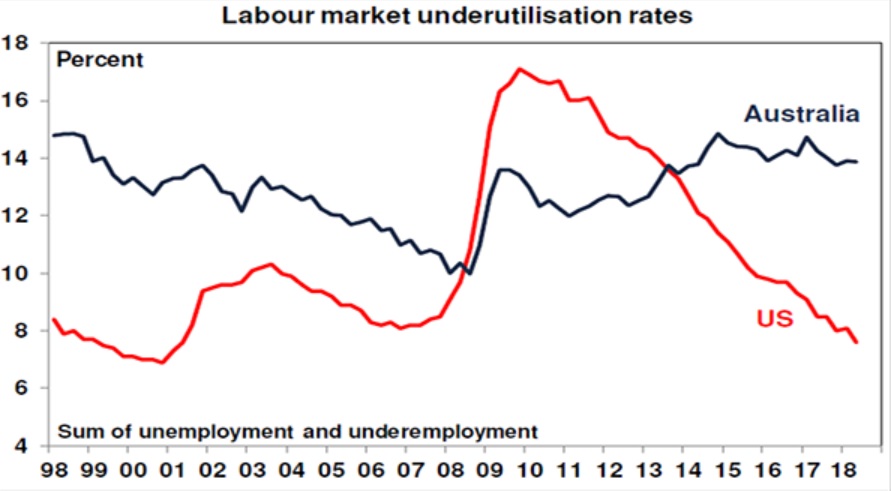

Australia and United States – labour underutilisation

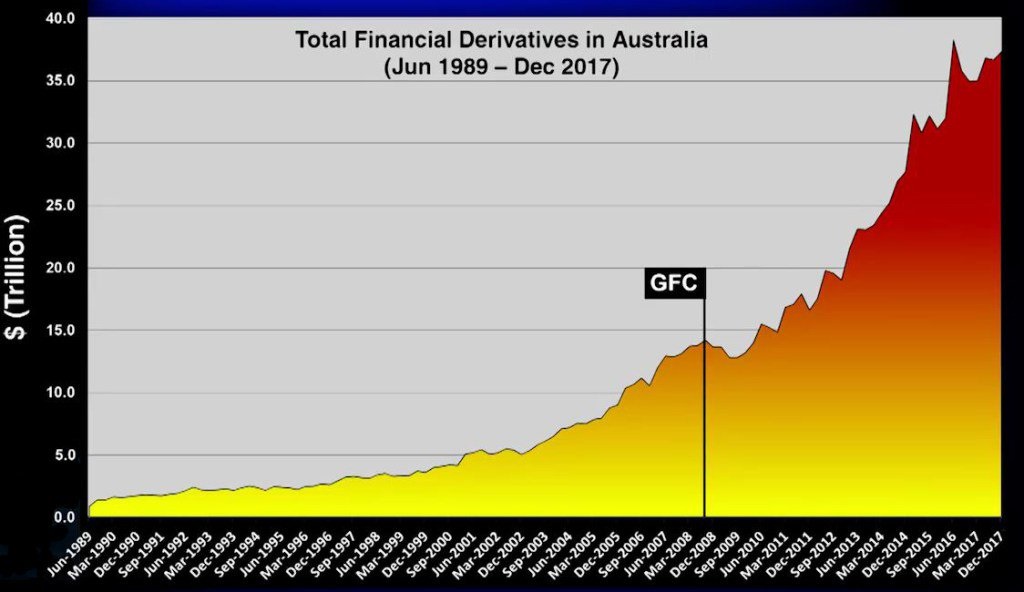

Australia – Financial Derivatives

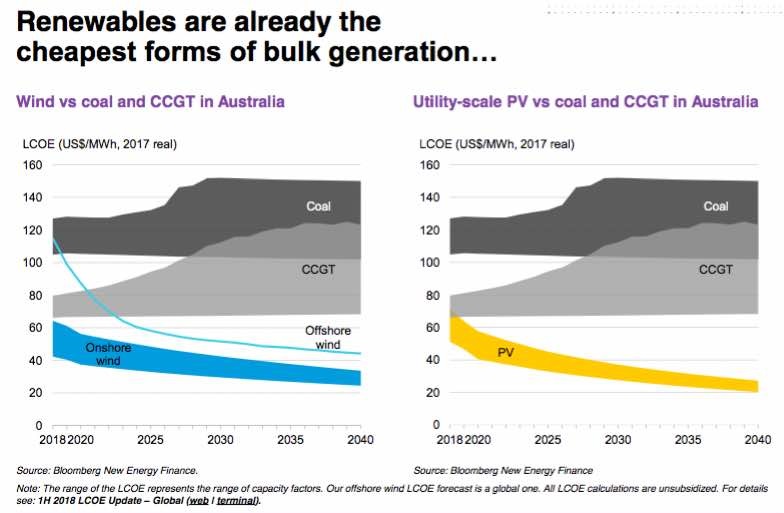

Renewables and coal costs and Australian electricity

United States & Americas

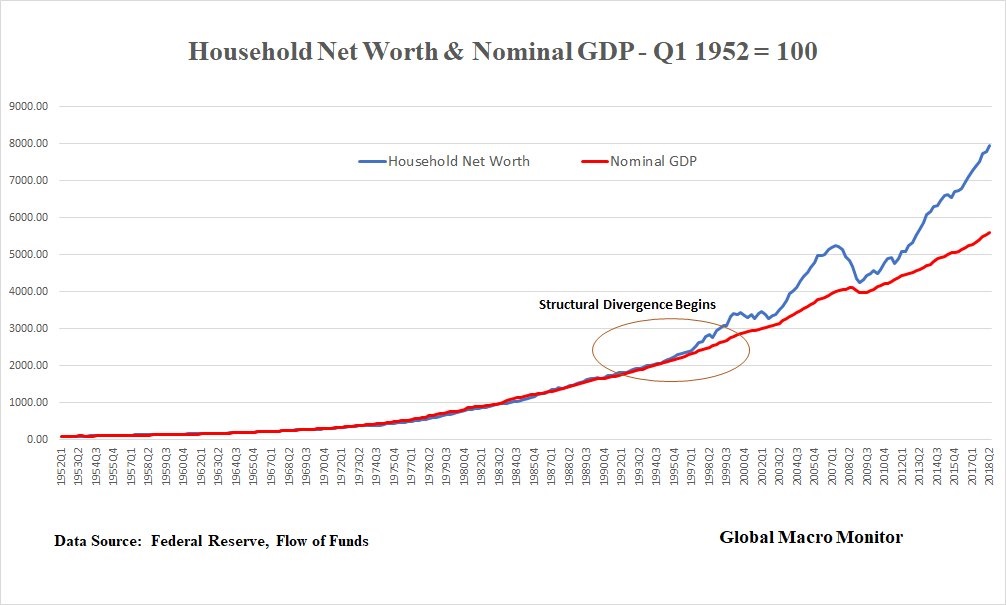

United States – Household Net Worth and Nominal GDP

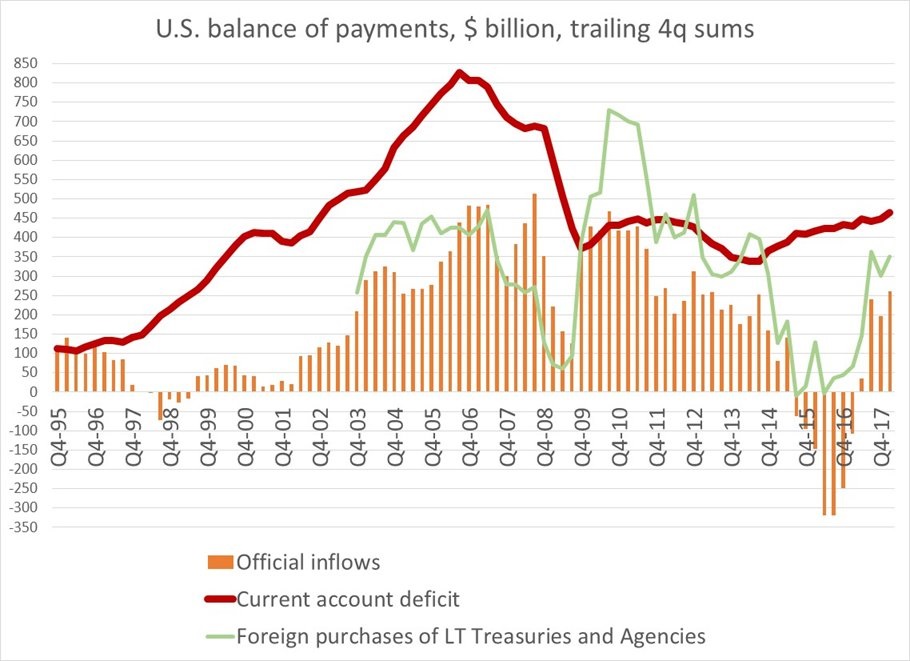

United States – Balance of Payments

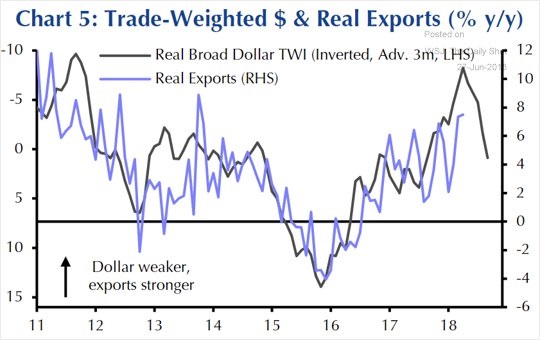

United States – Real Exports and Trade Weighted $

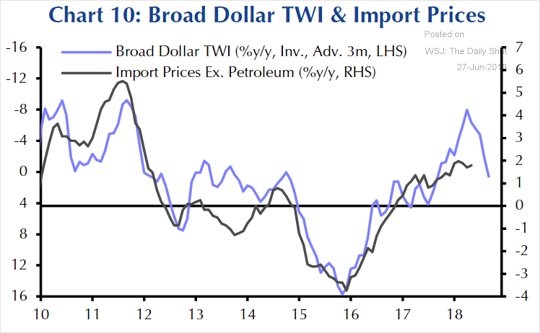

United States – Import Prices and Trade Weighted $

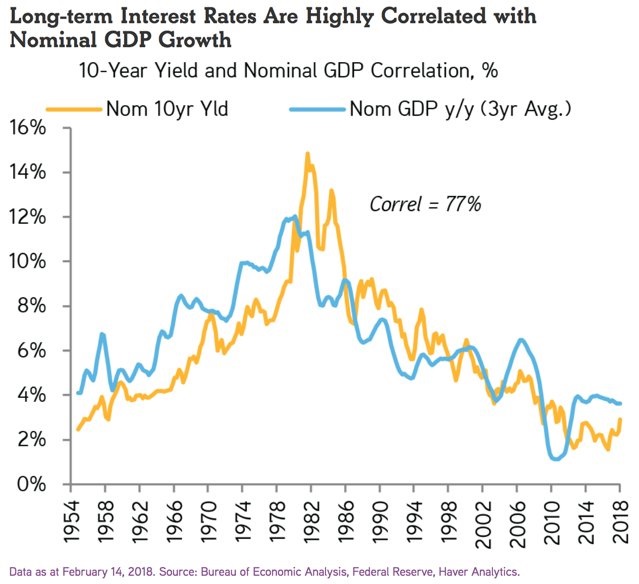

United States – Nominal GDP and Interest Rates

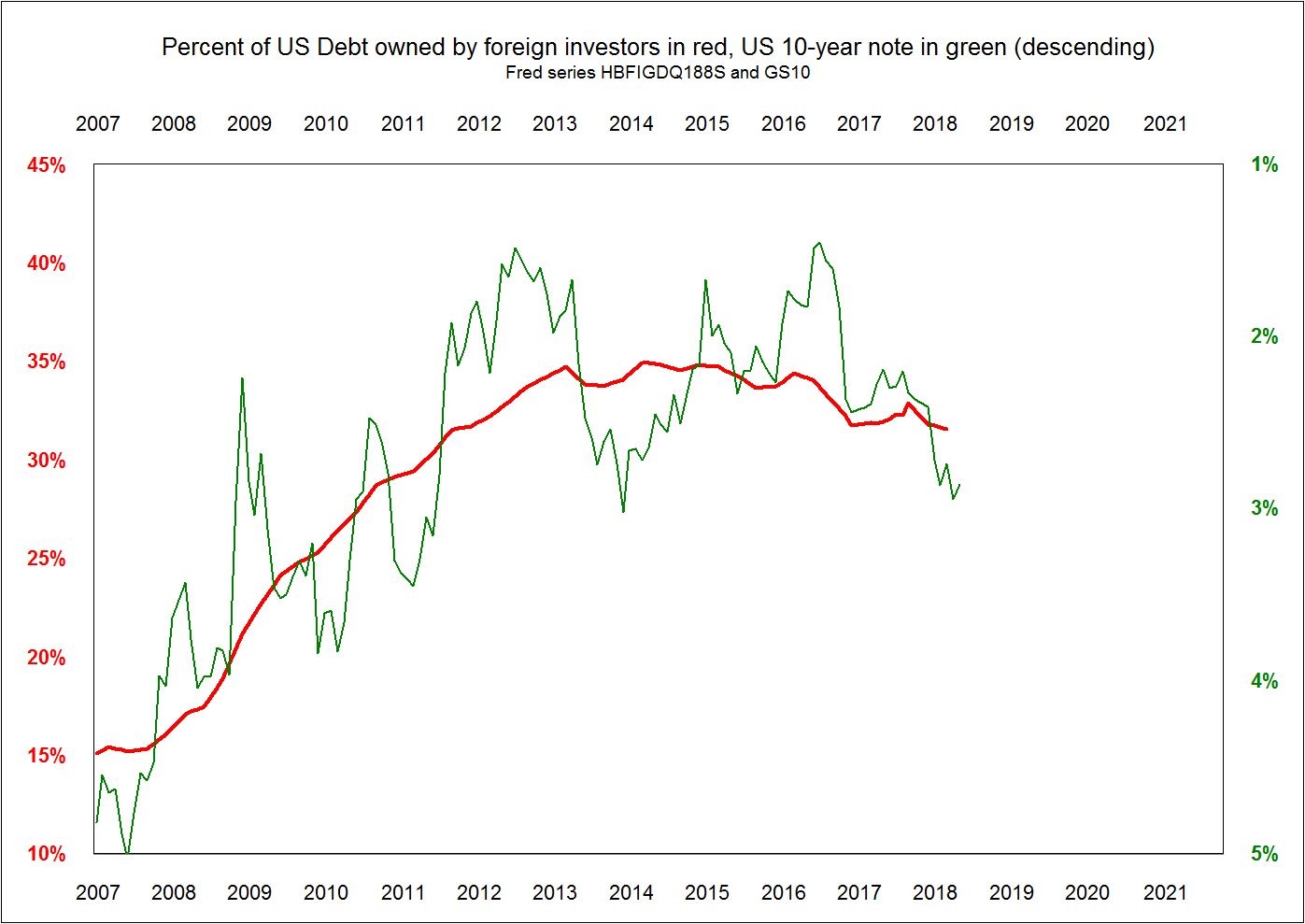

Foreign Owned US Debt and US10s

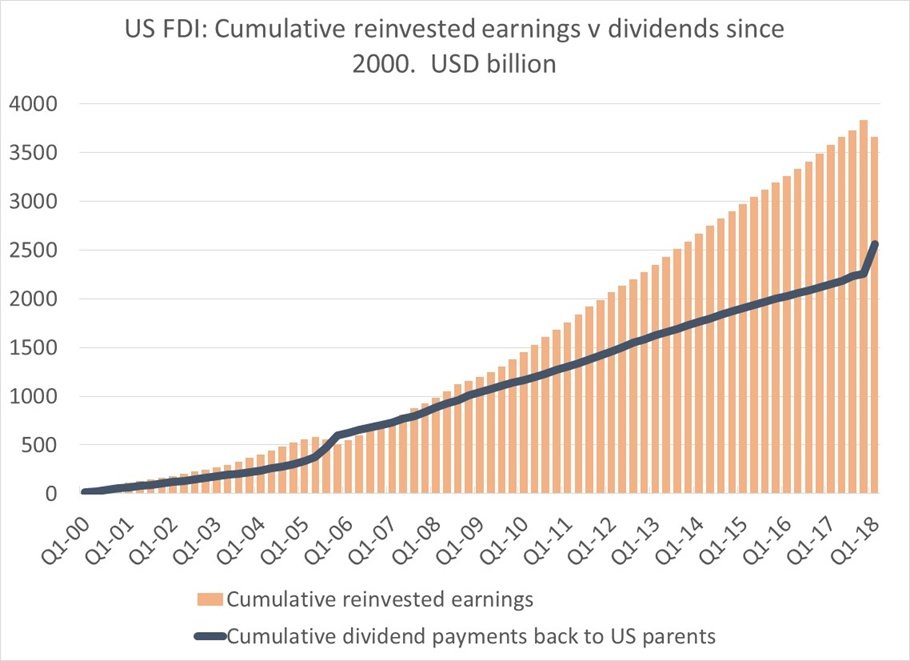

US FDI

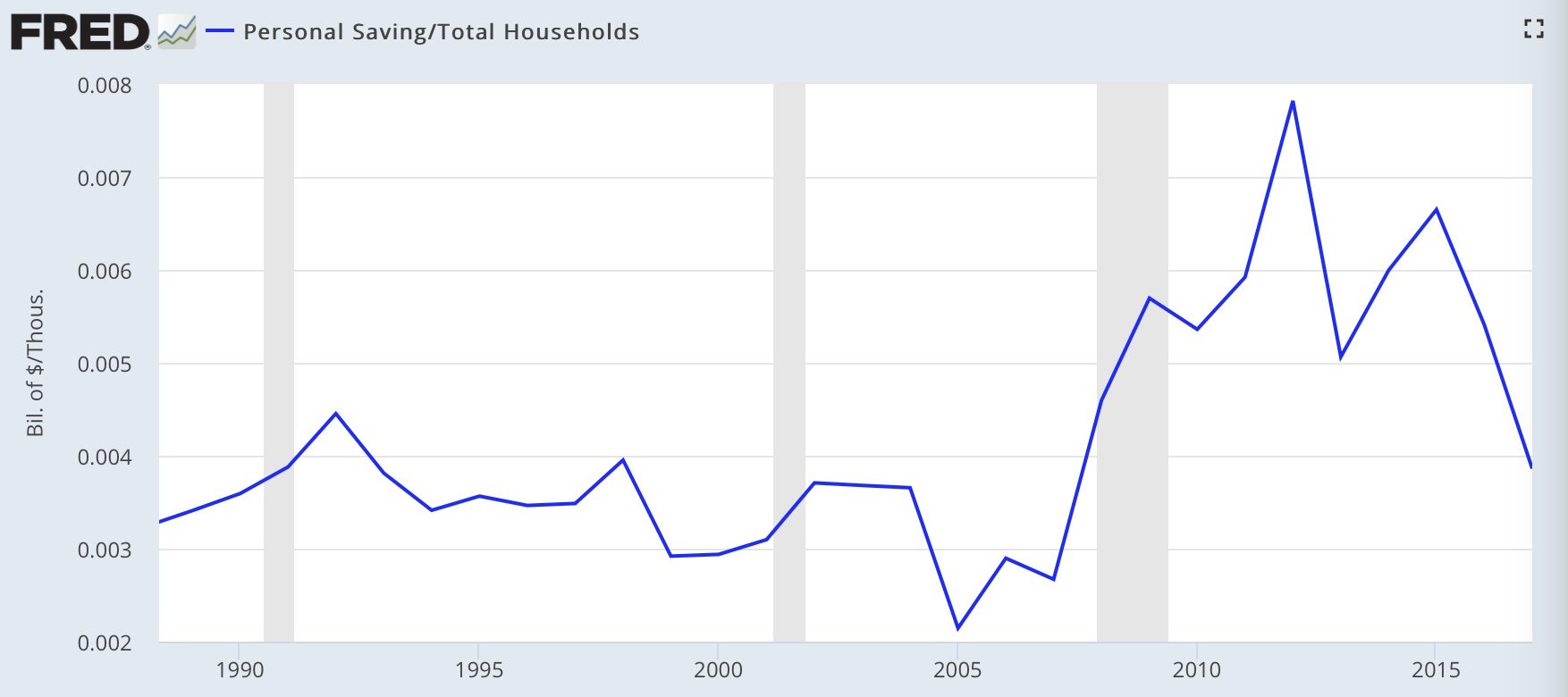

United States – savings

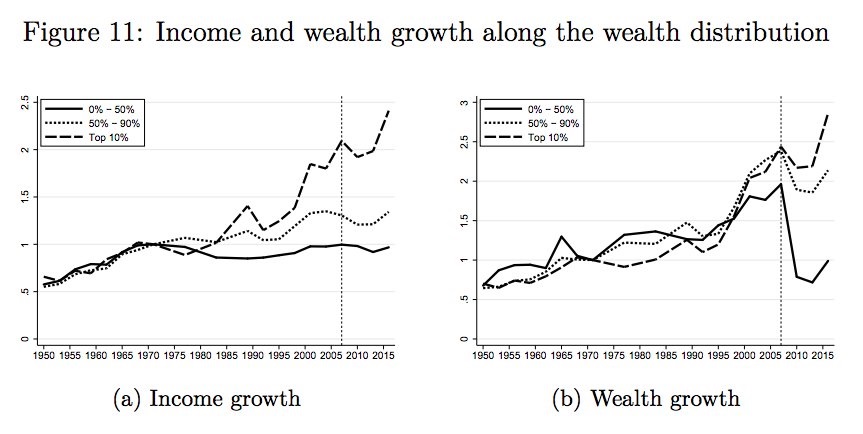

United States – Income and Wealth Growth (bottom 50% are no better off now than circa 1970…)

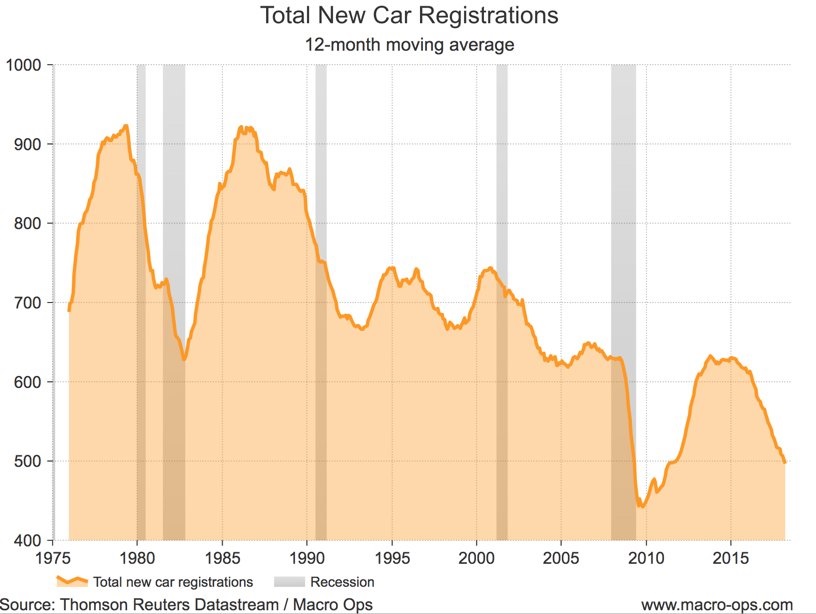

United States – New Car Registrations

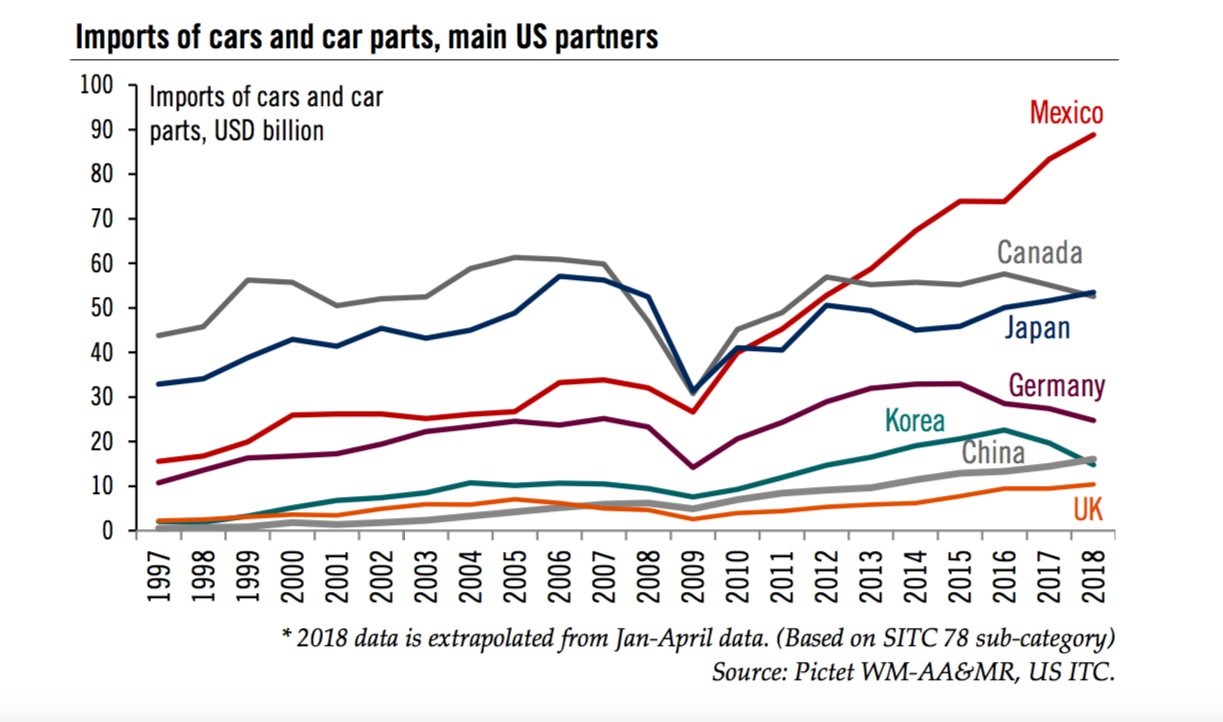

United States – Imports of Cars and Car parts, major partners

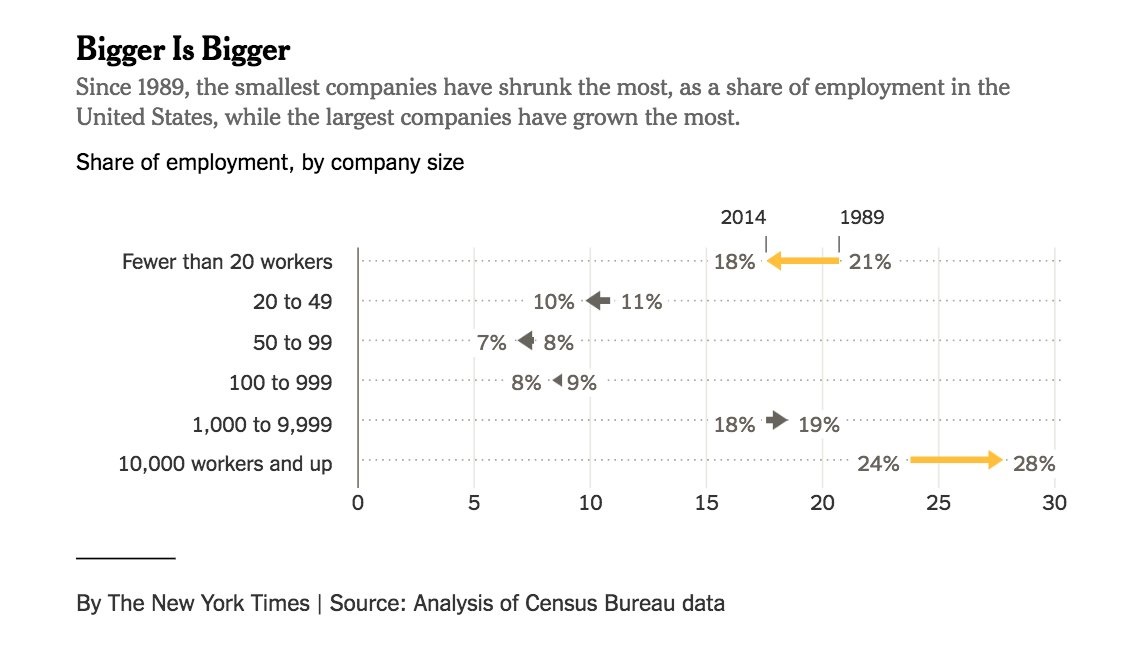

United States – company size and employment growth

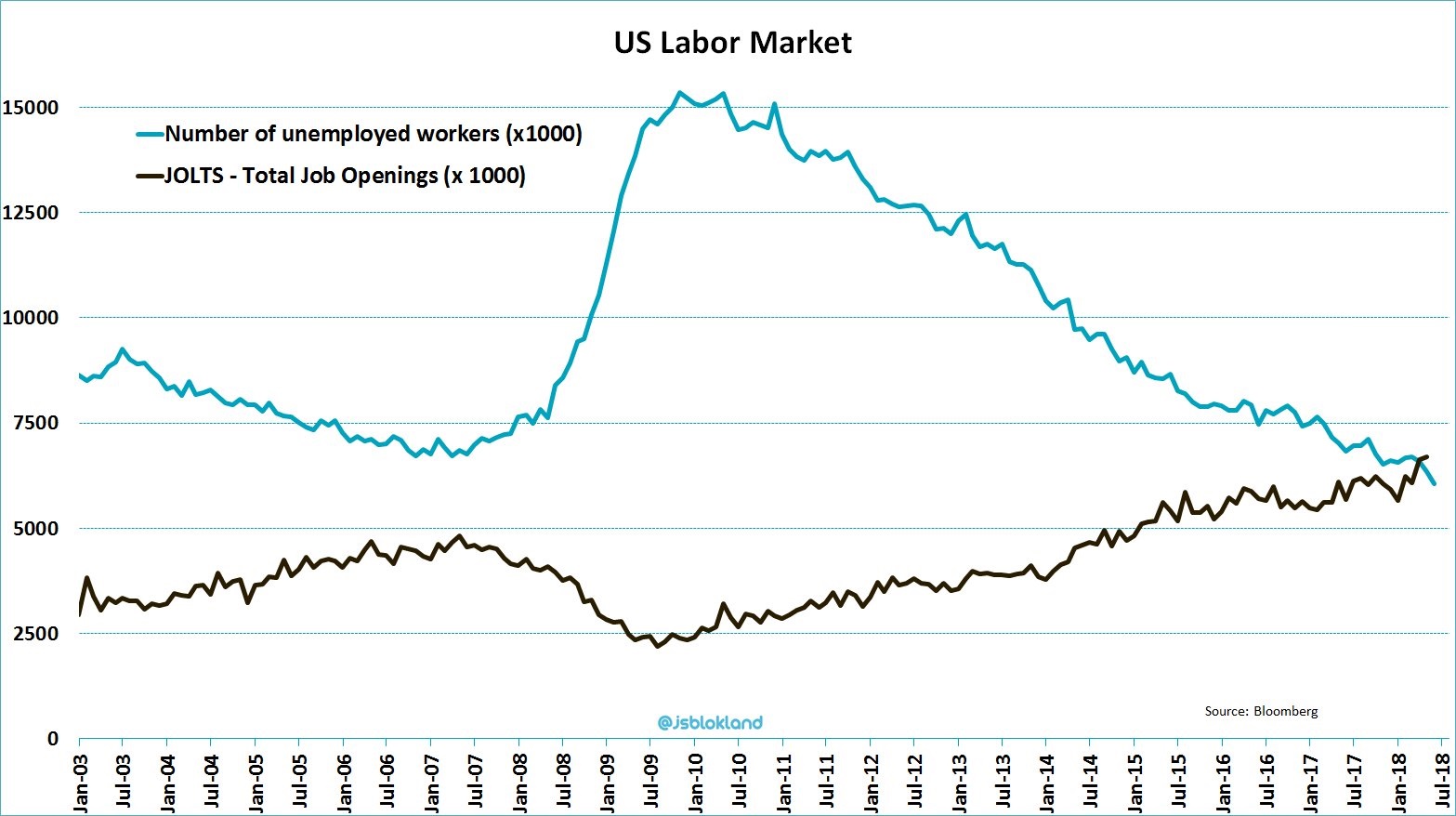

United States Labor Market

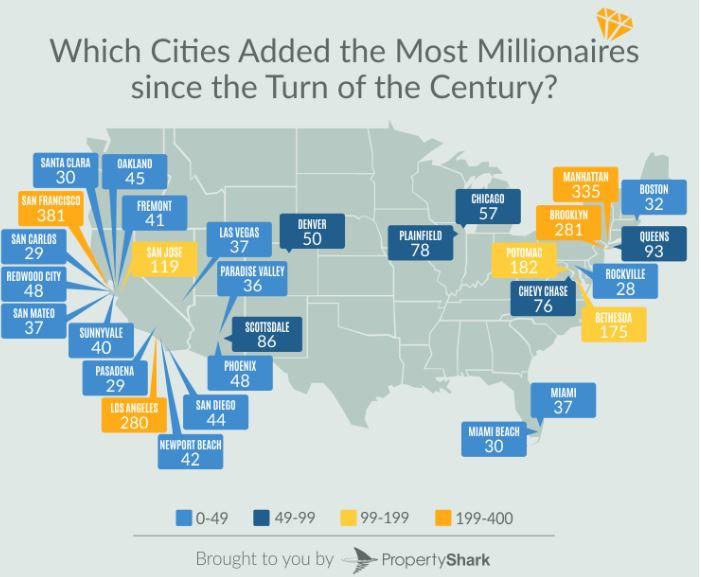

United States – New RE millionaires

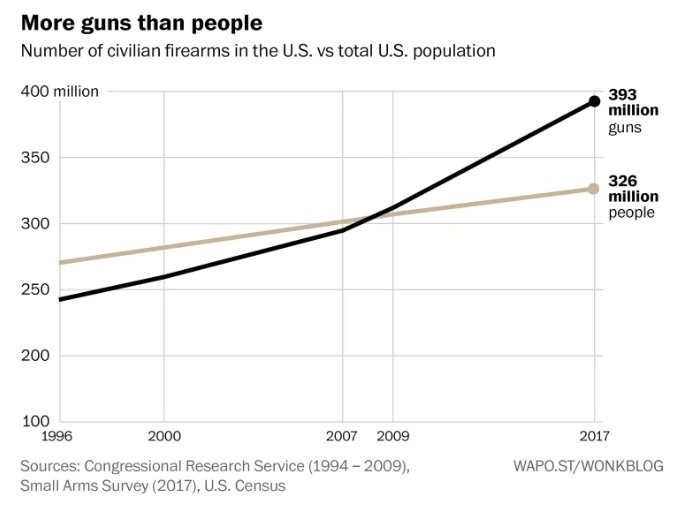

United States – Guns & People

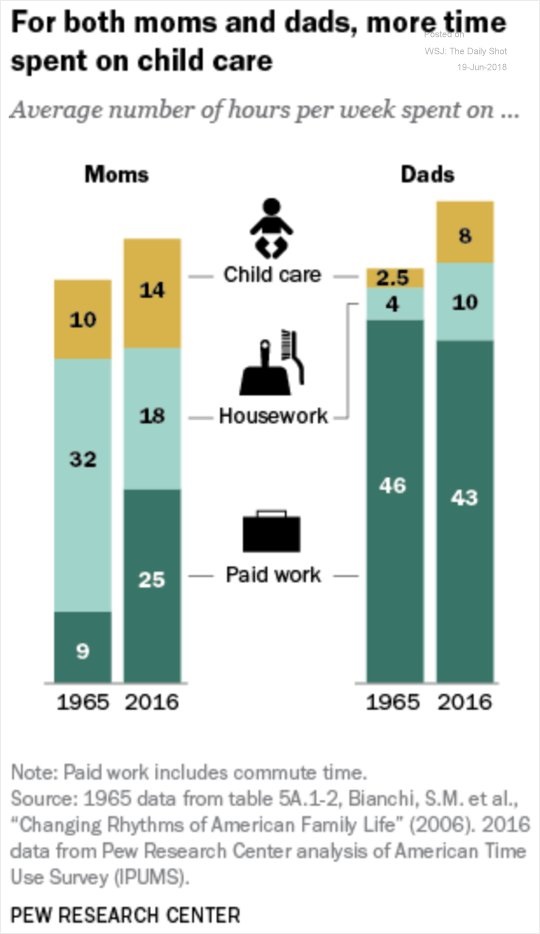

United States Parental Life Changes 1965 – 2016

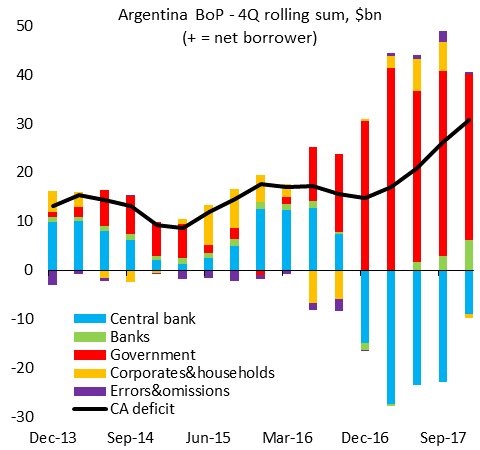

Argentina Balance of Payments

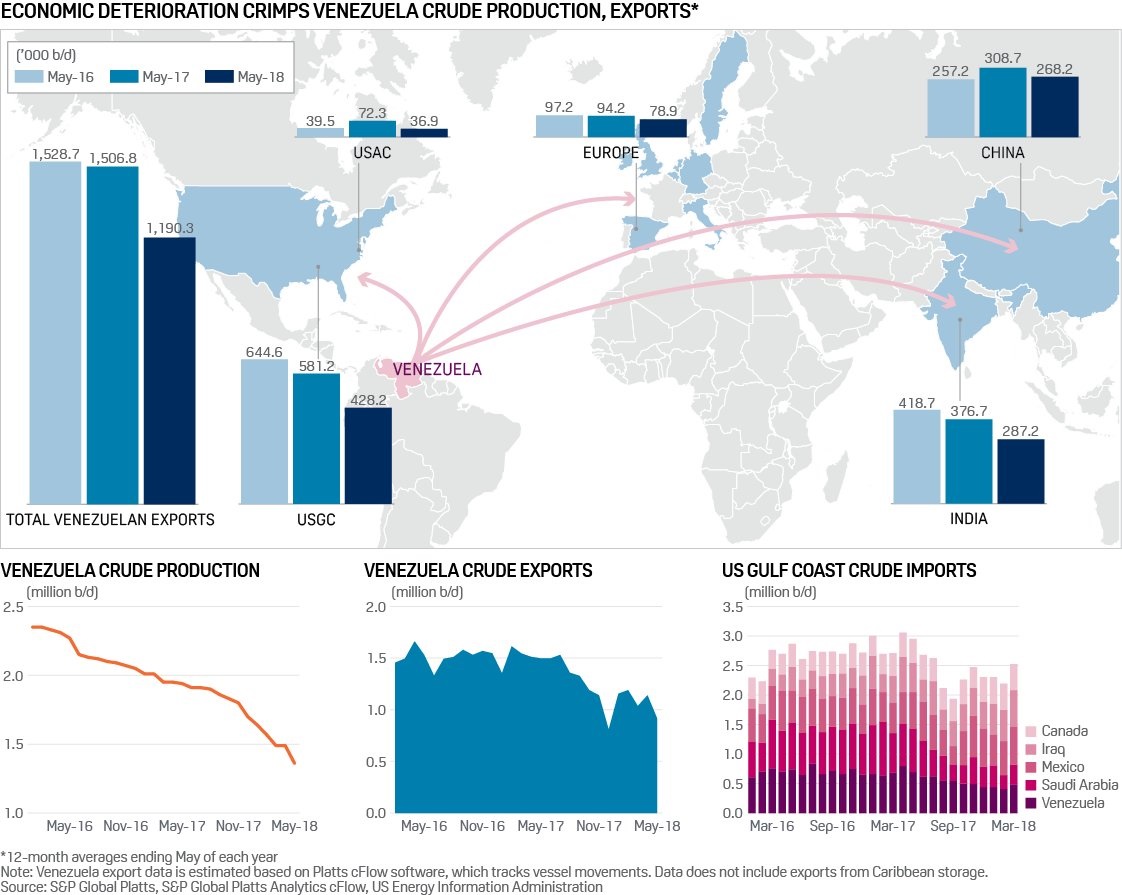

Venezuela Crude

China & Asia

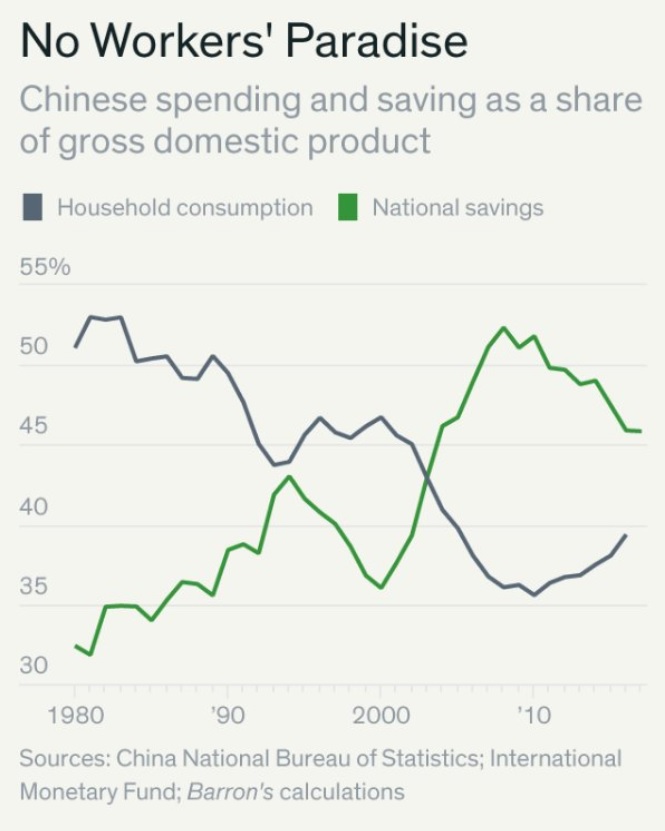

China Household Consumption & Savings

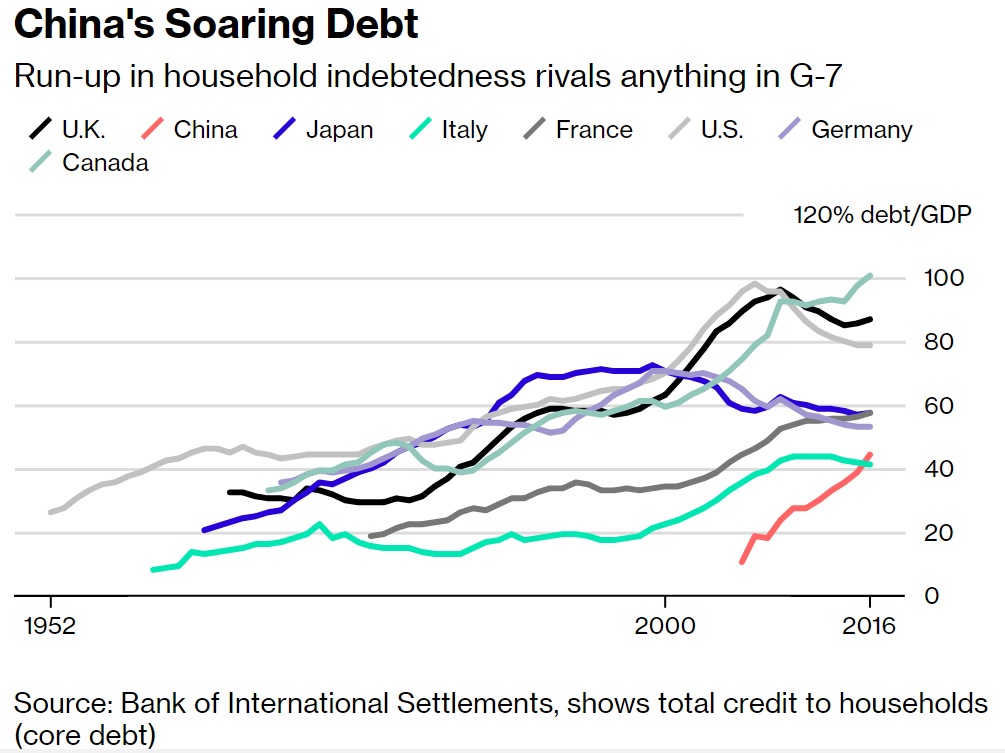

China rising Household indebtedness – comparison with G7

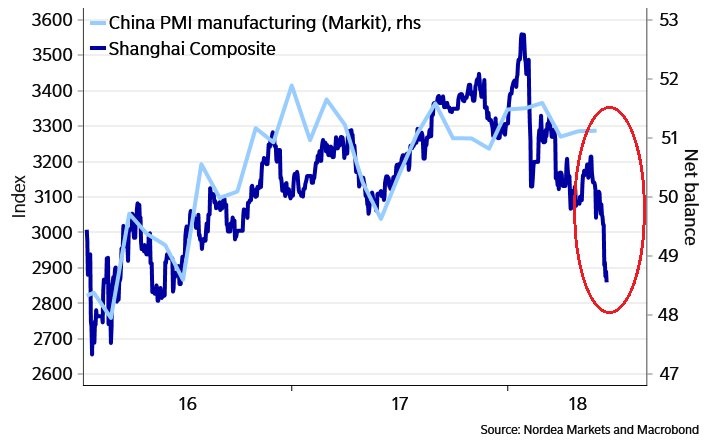

Shanghai Composite and China Manufacturing PMI

China Hang Seng – corporates at lows

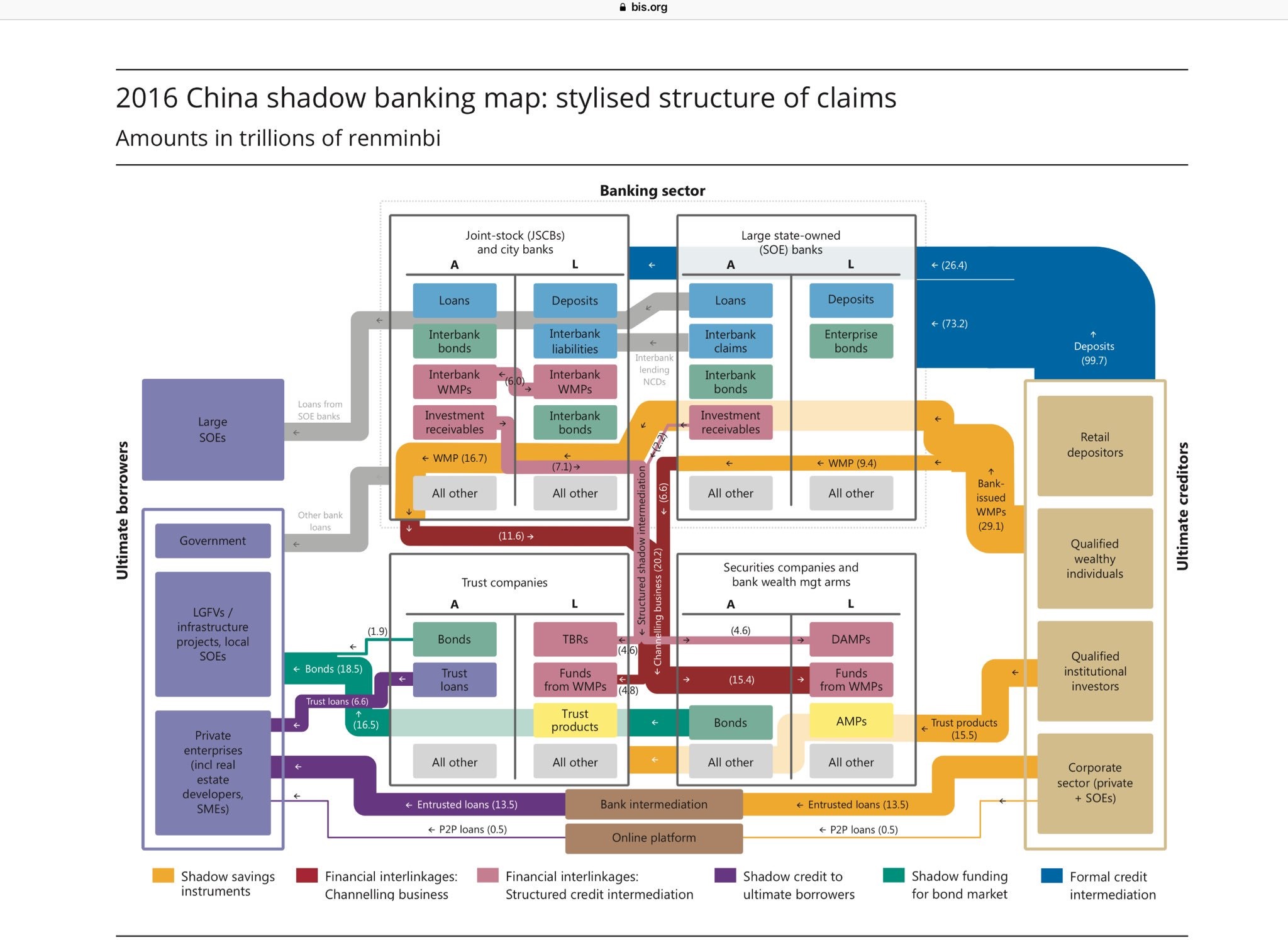

China – Shadow Banking (and how it works)

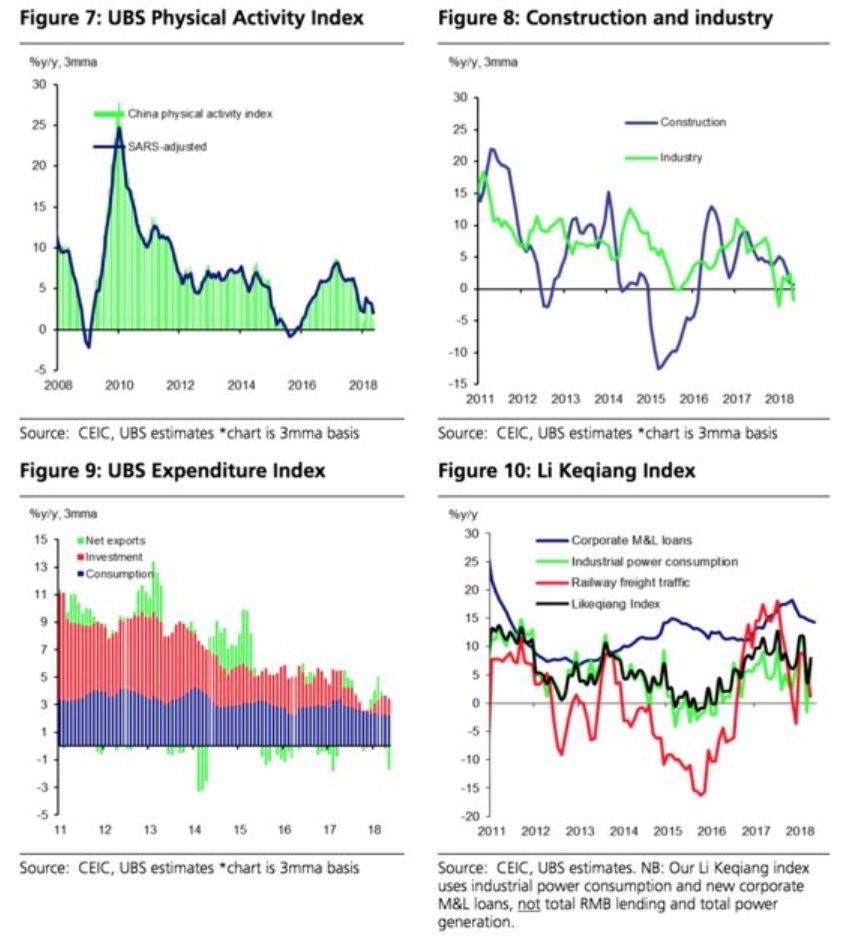

China easing – 4 different metrics

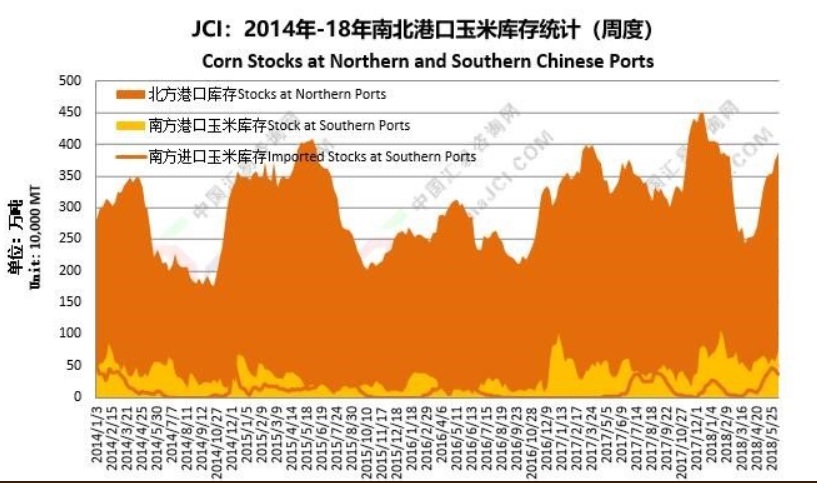

China – Corn Stocks

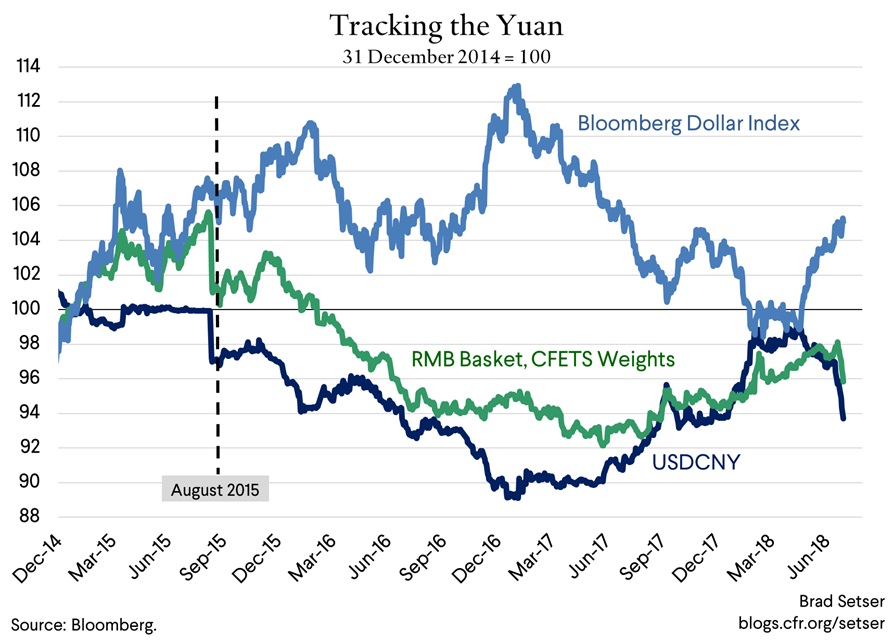

China – CNY

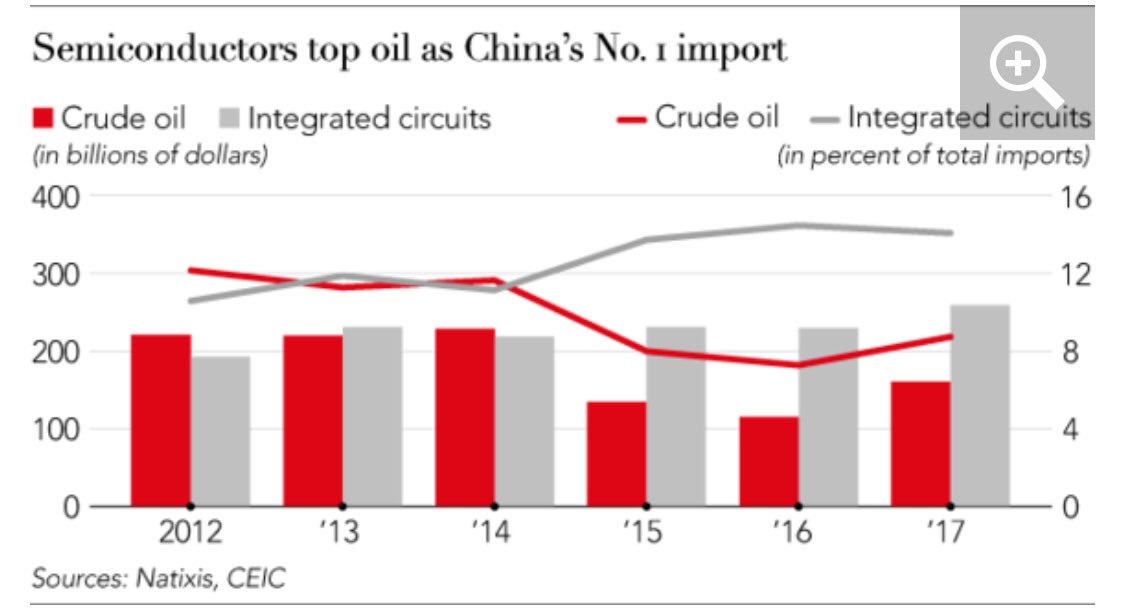

China Imports – Semiconductors and oil

Japan Unemployment

Europe & United Kingdom

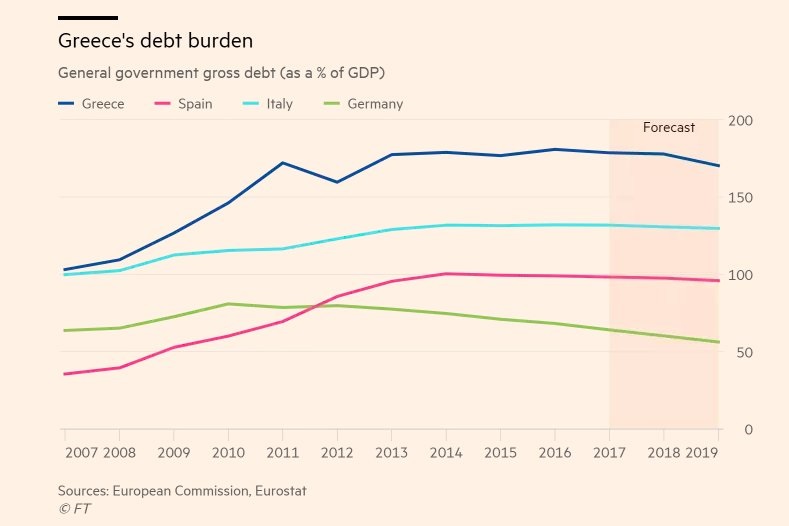

Government debt to GDP – Germany Greece Spain Italy

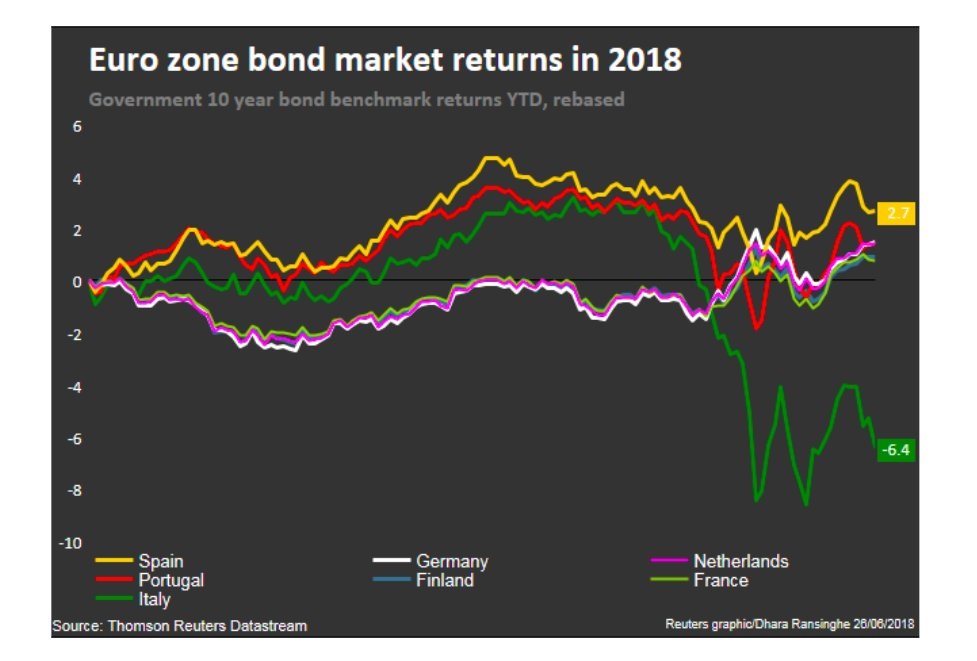

Eurozone 10yr Sovereigns YTD

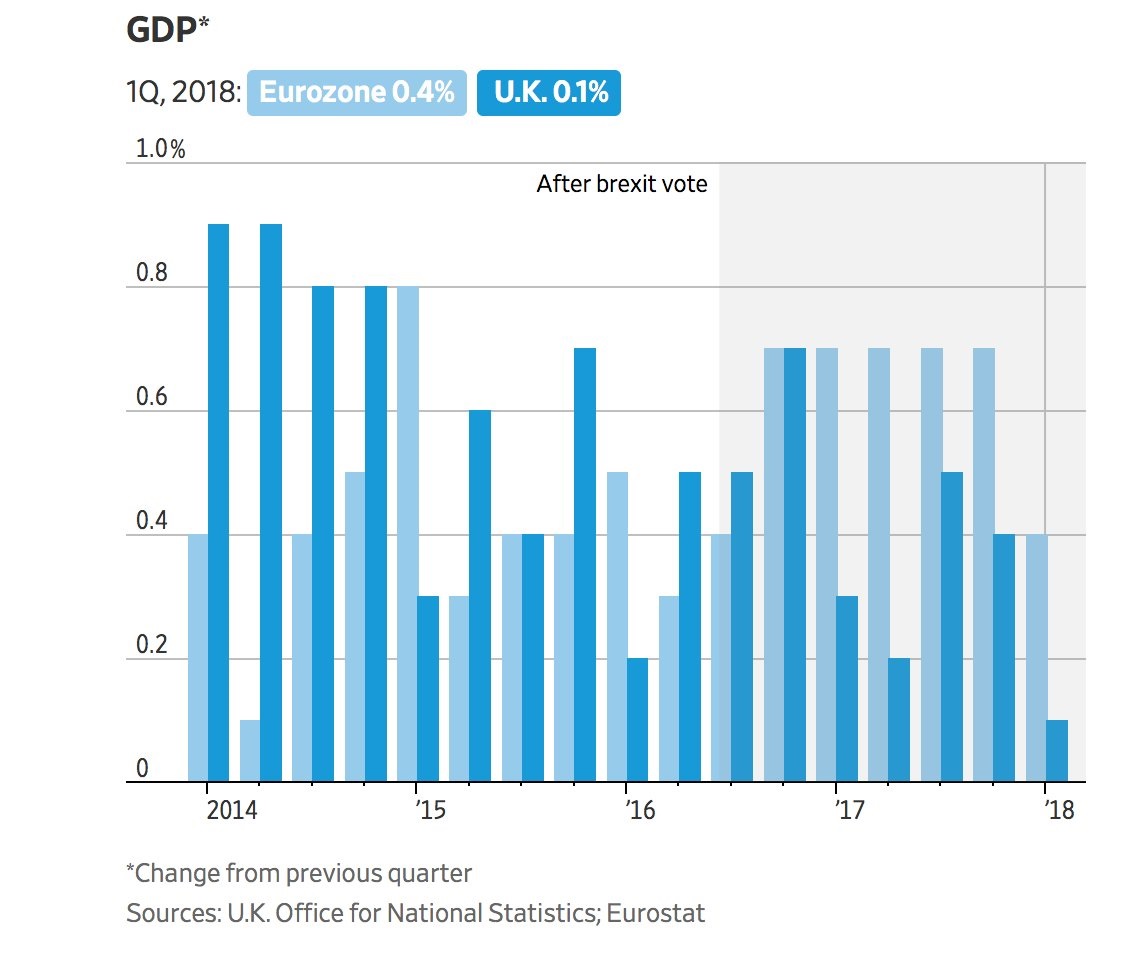

United Kingdom and Eurozone GDP

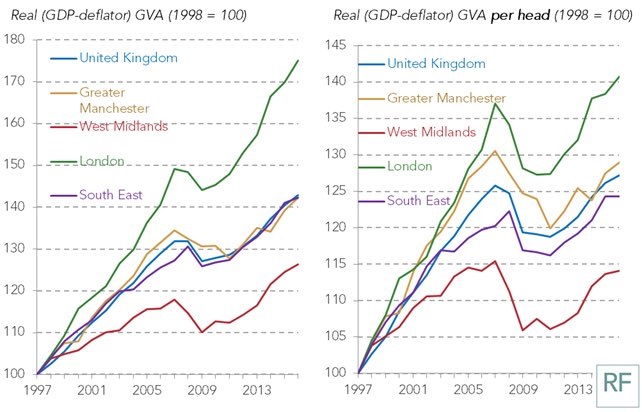

United Kingdom regional economies GDP per Head and GVA

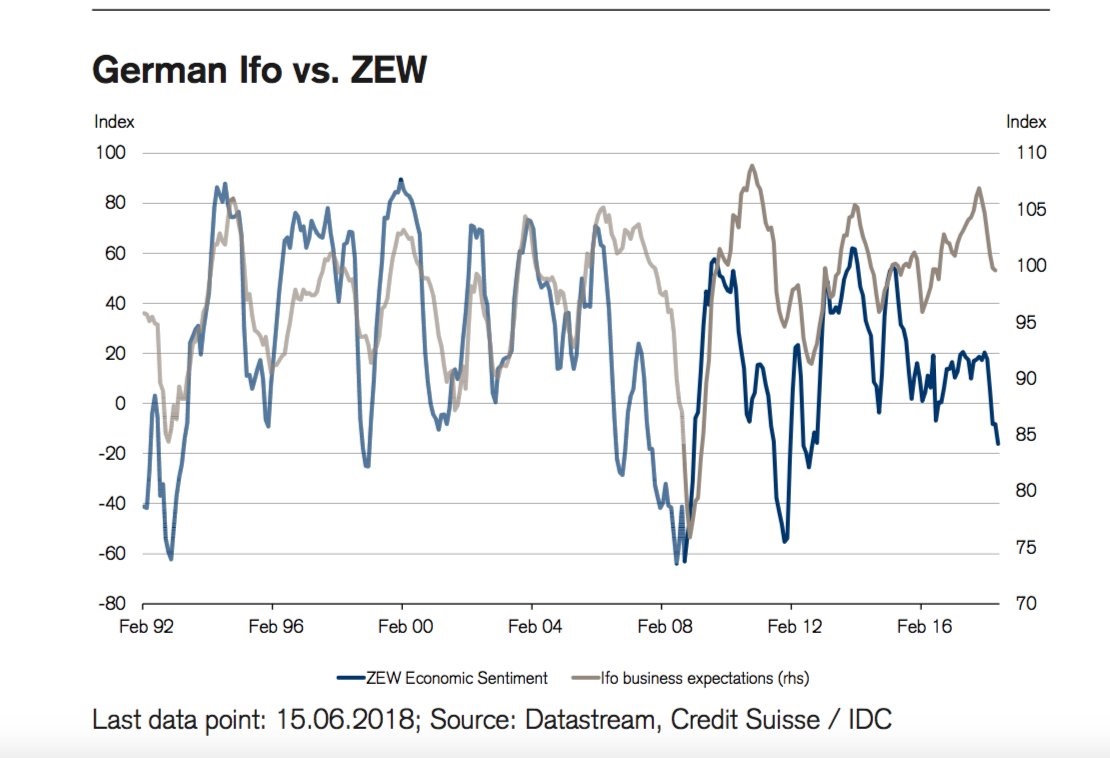

German Sentiment and Expectations

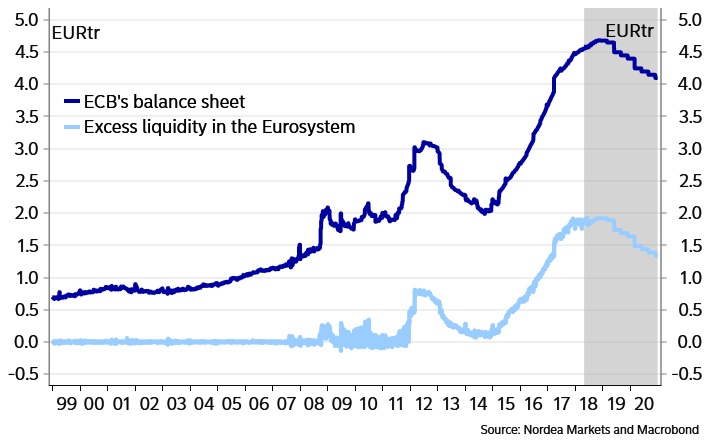

Eurozone TLTRO

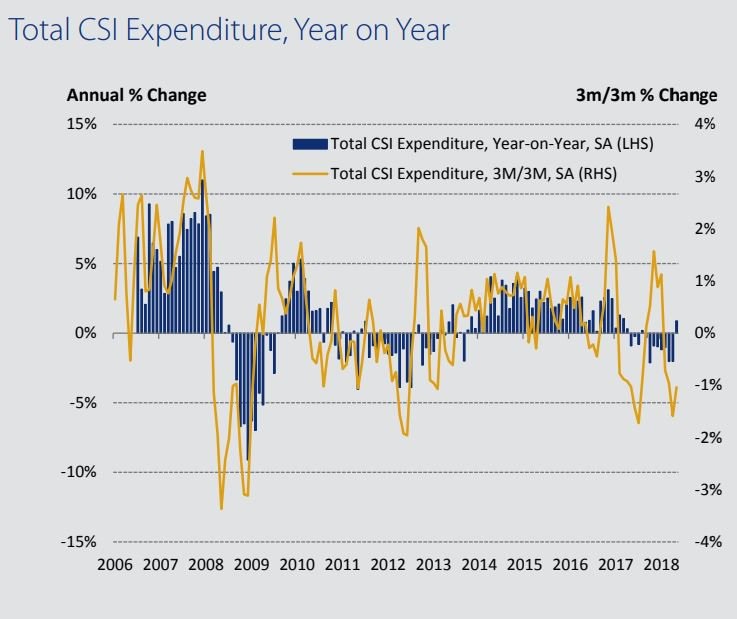

United Kingdom – Consumer Spending

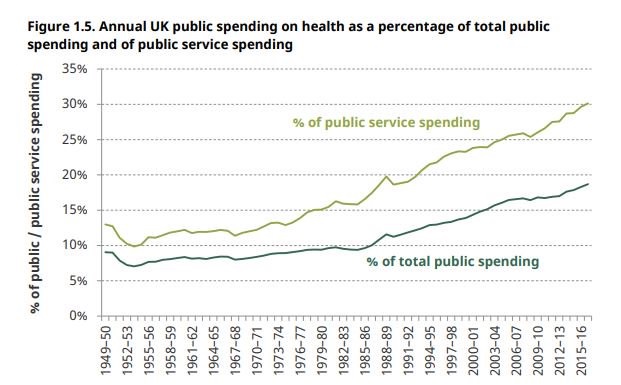

United Kingdom – Health Spending

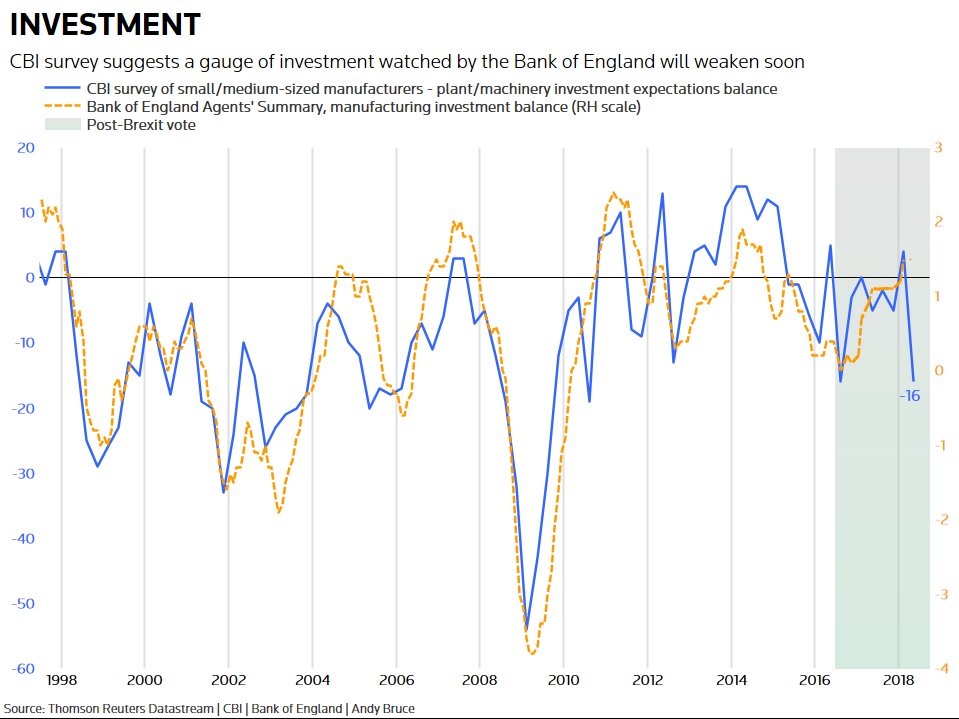

United Kingdom – Investment Sentiment

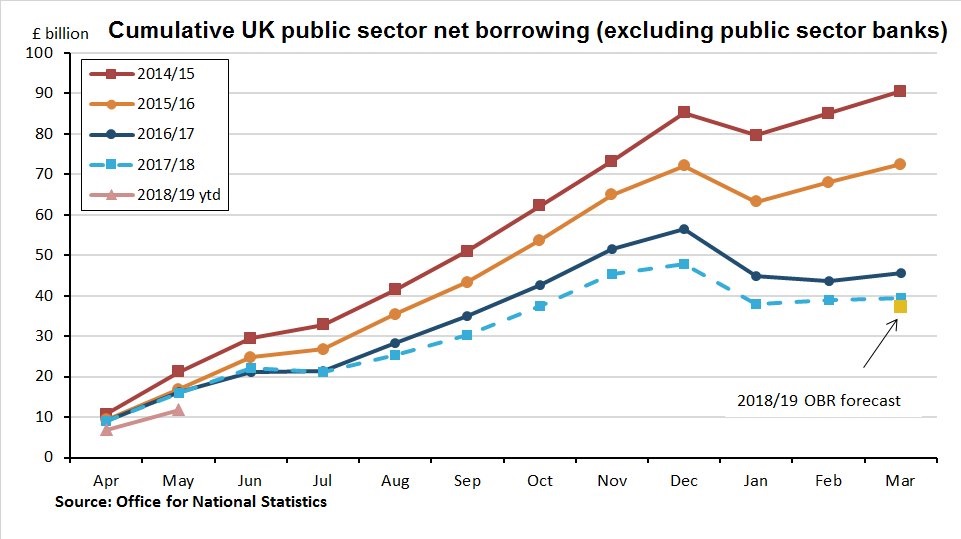

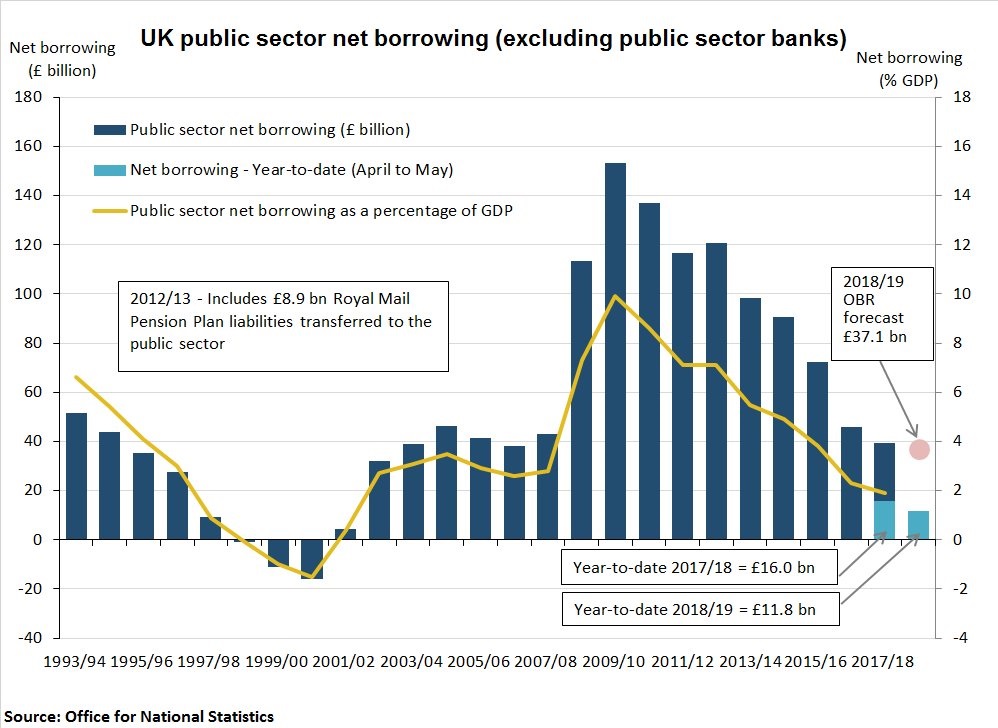

United Kingdom – Public Sector Borrowing 1

United Kingdom – Public Sector Borrowing 2

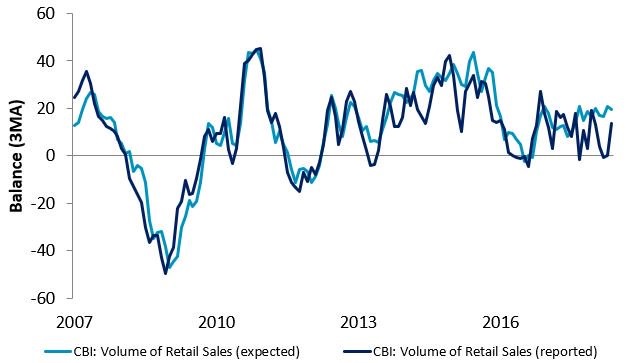

United Kingdom – Retail

Commodities

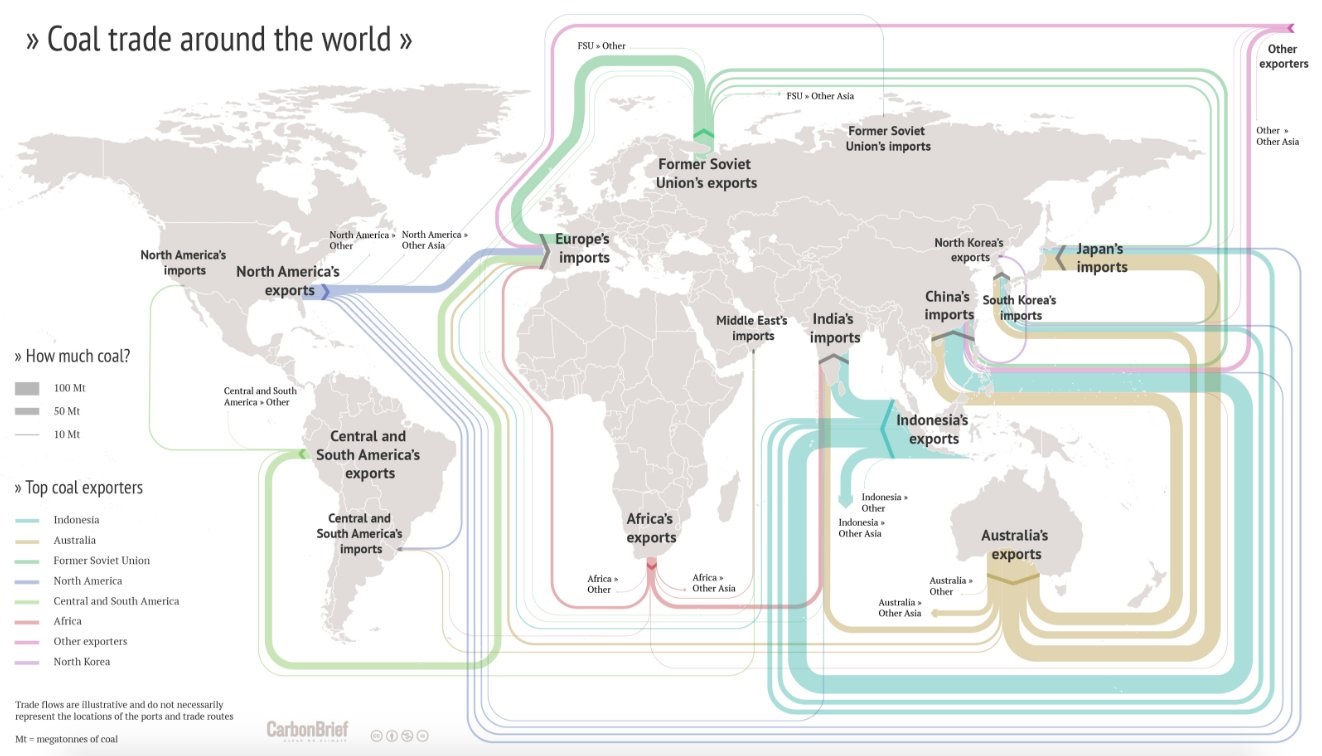

The Global Coal Trade

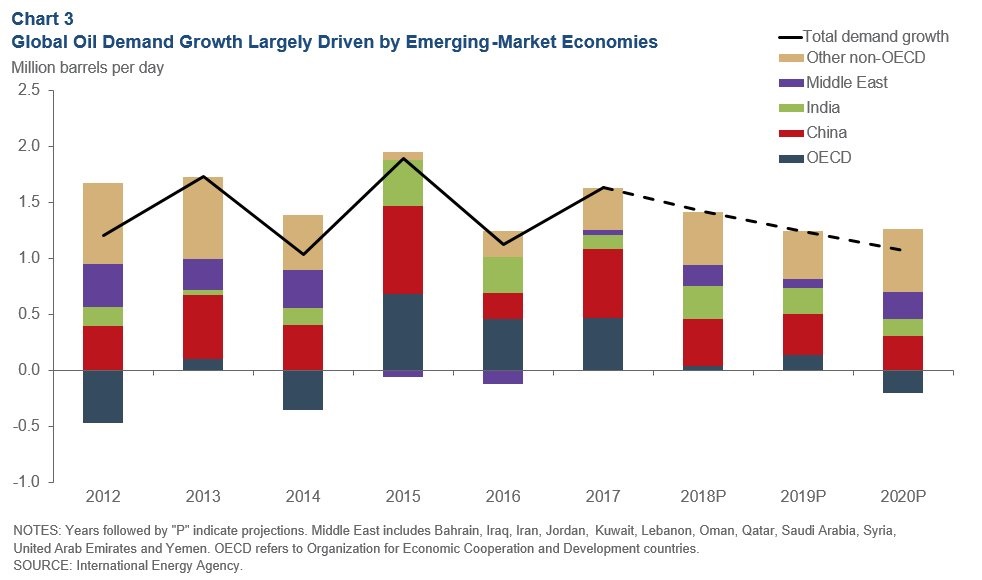

Global Crude – Demand drivers

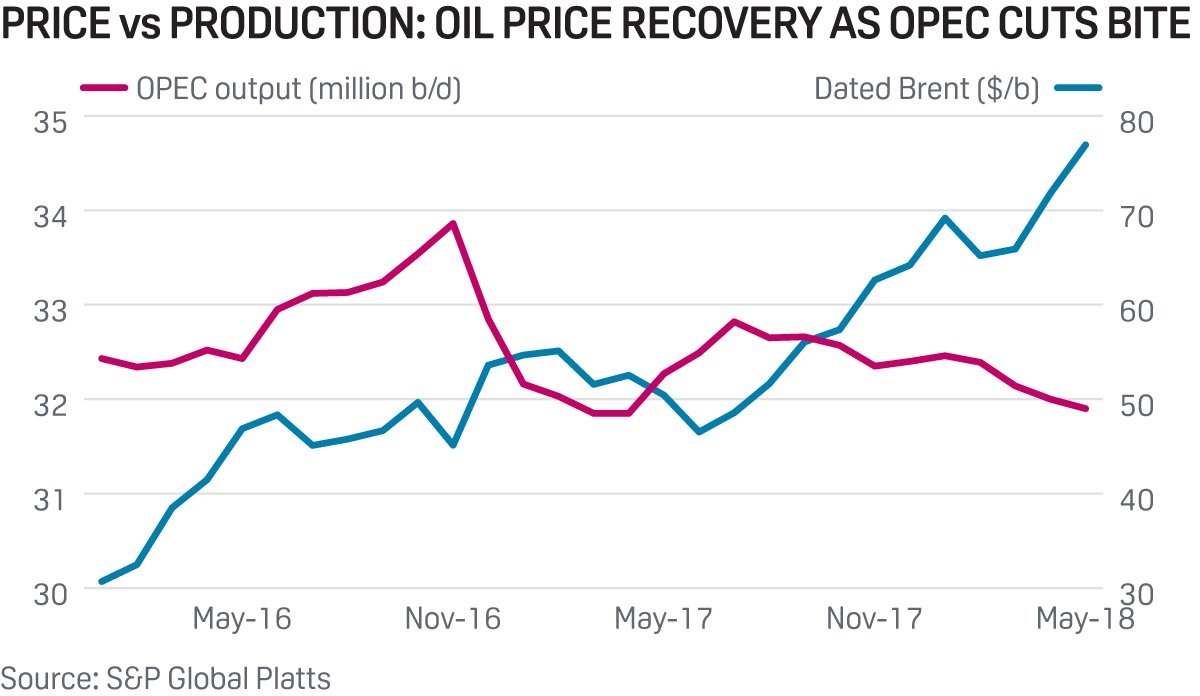

Crude Oil – Price and Production

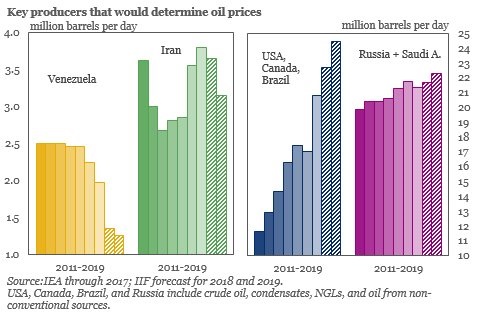

Crude – sources of suply

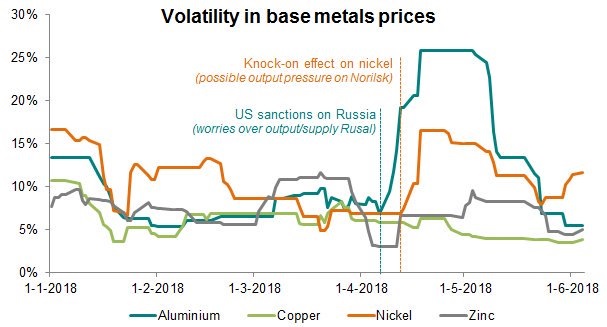

Base Metals – 2018 volatility

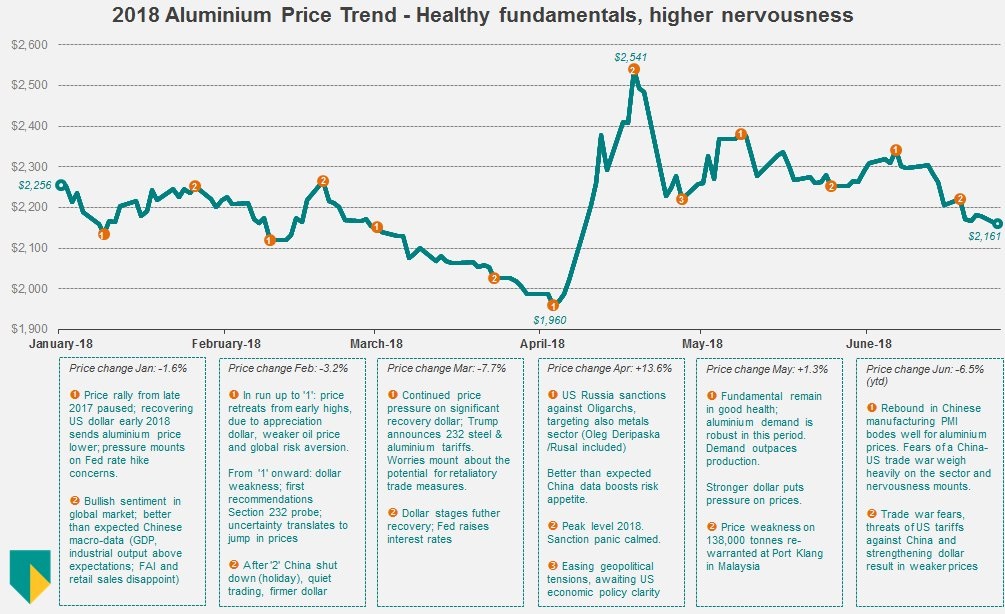

Aluminium 2018

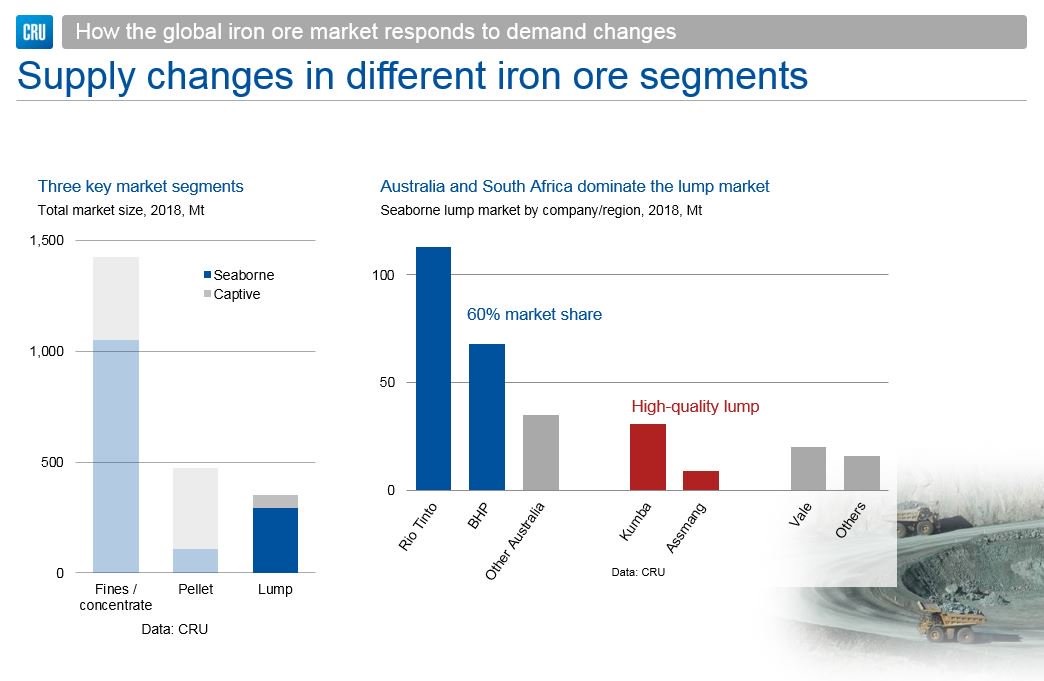

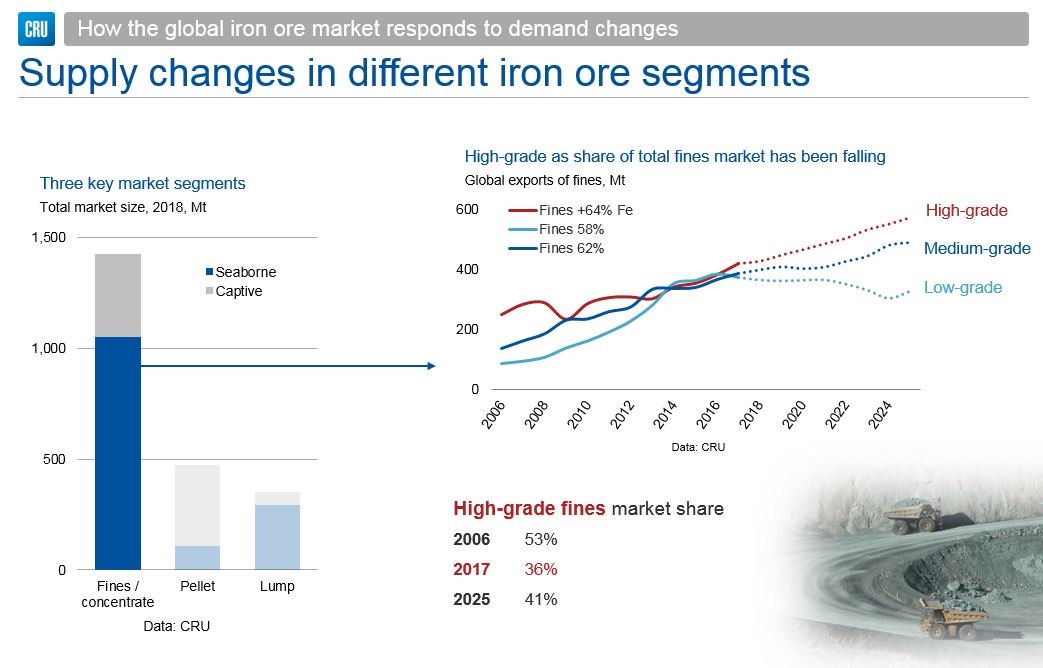

Iron Ore Supply 1

Iron Ore Supply 2

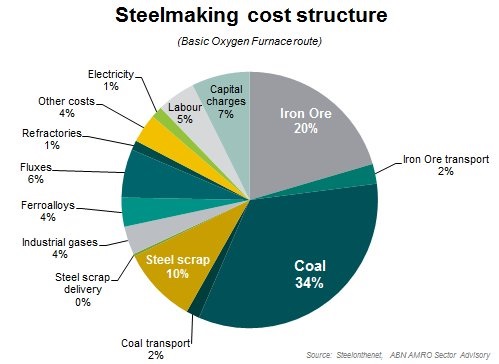

Steelmaking Costs

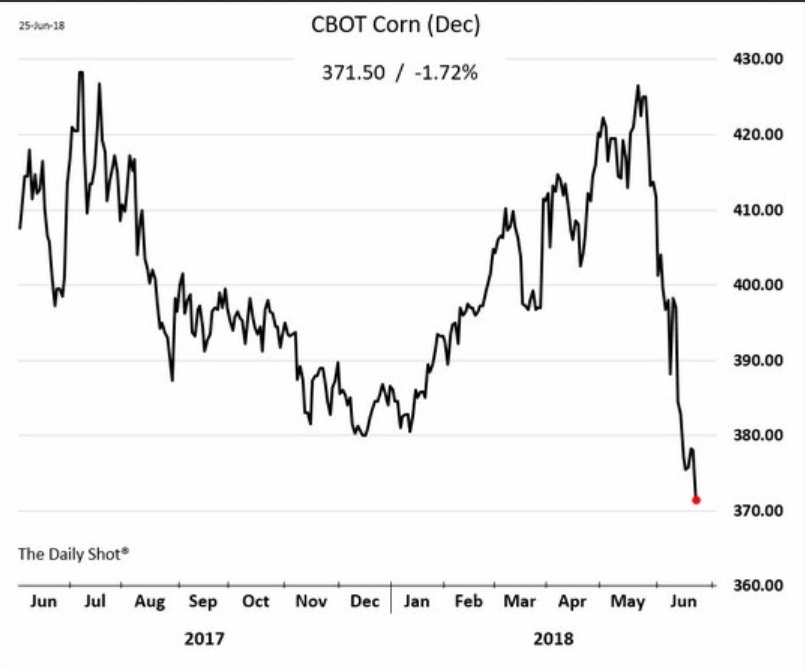

CBOT Corn …look out below

CBOT Soybeans

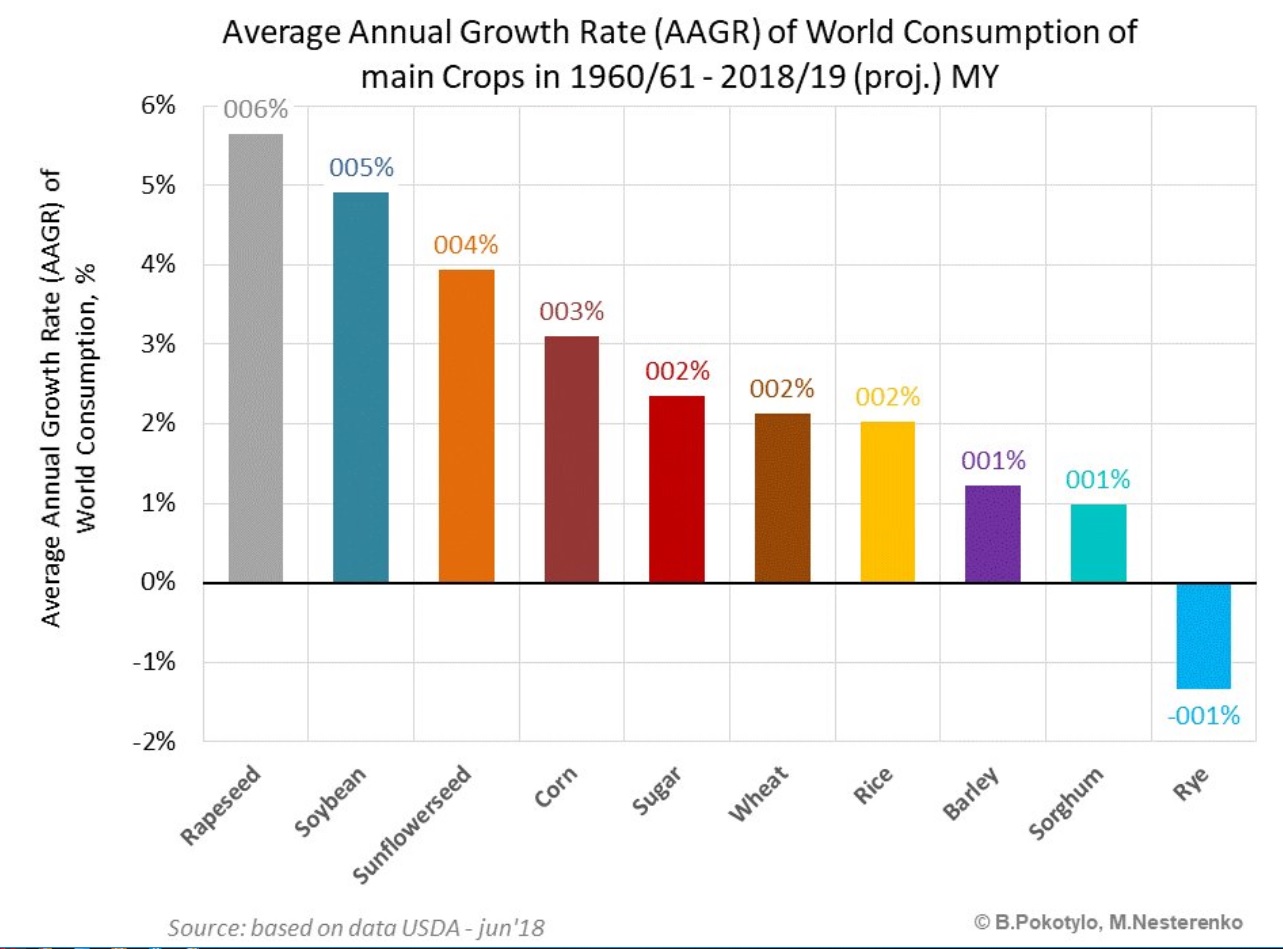

Major Crops – Average Annual growth rates since 1960

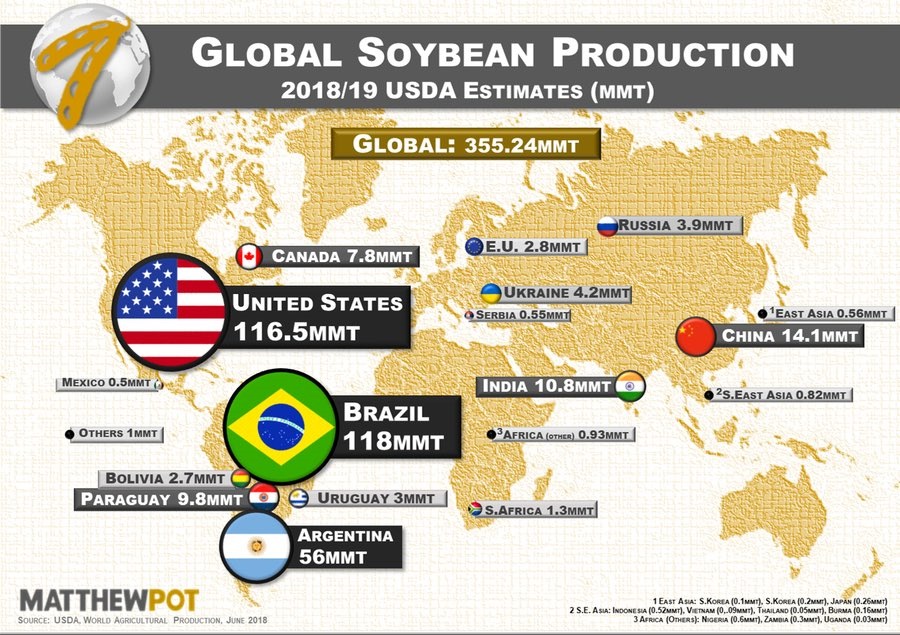

Soybeans

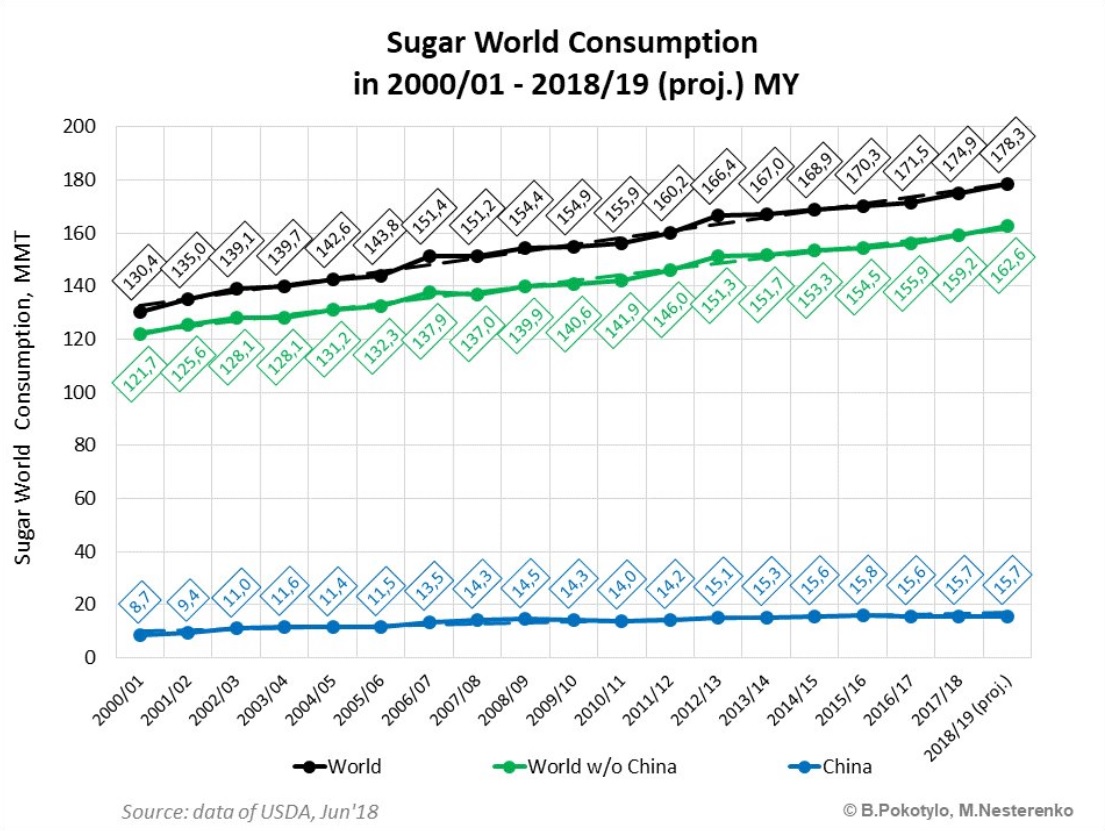

Global Sugar Consumption

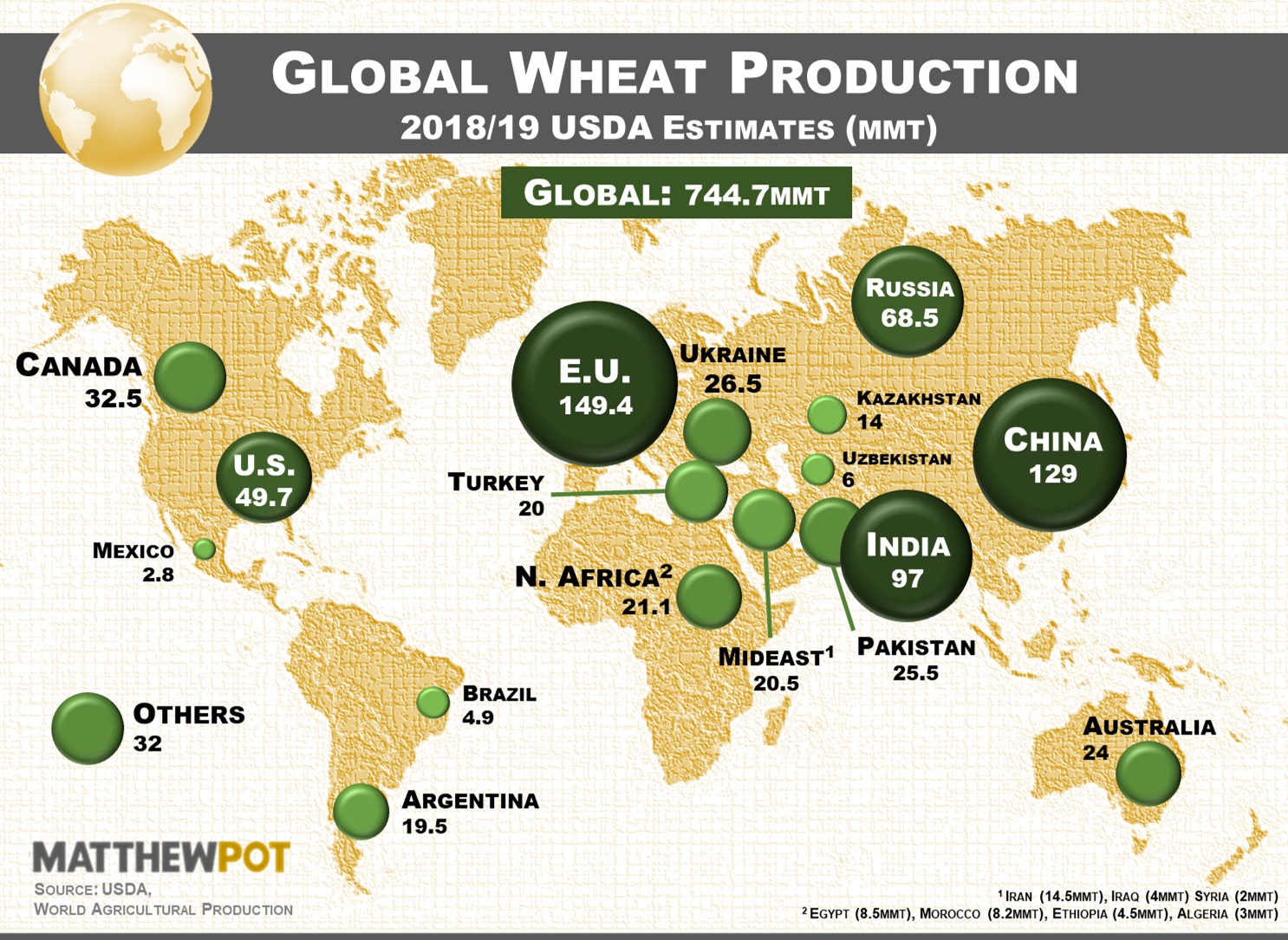

Global Wheat Production

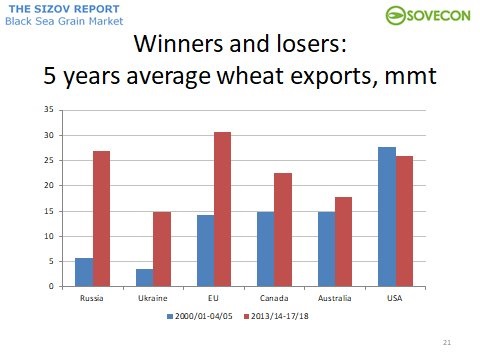

Wheat exporters

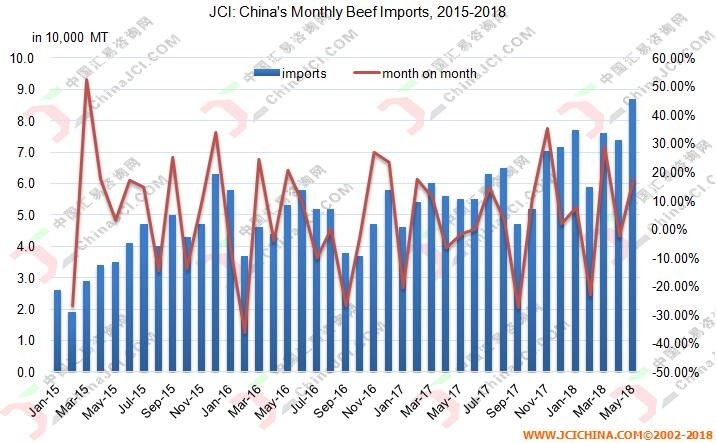

China Beef Imports

Gold – spot and future

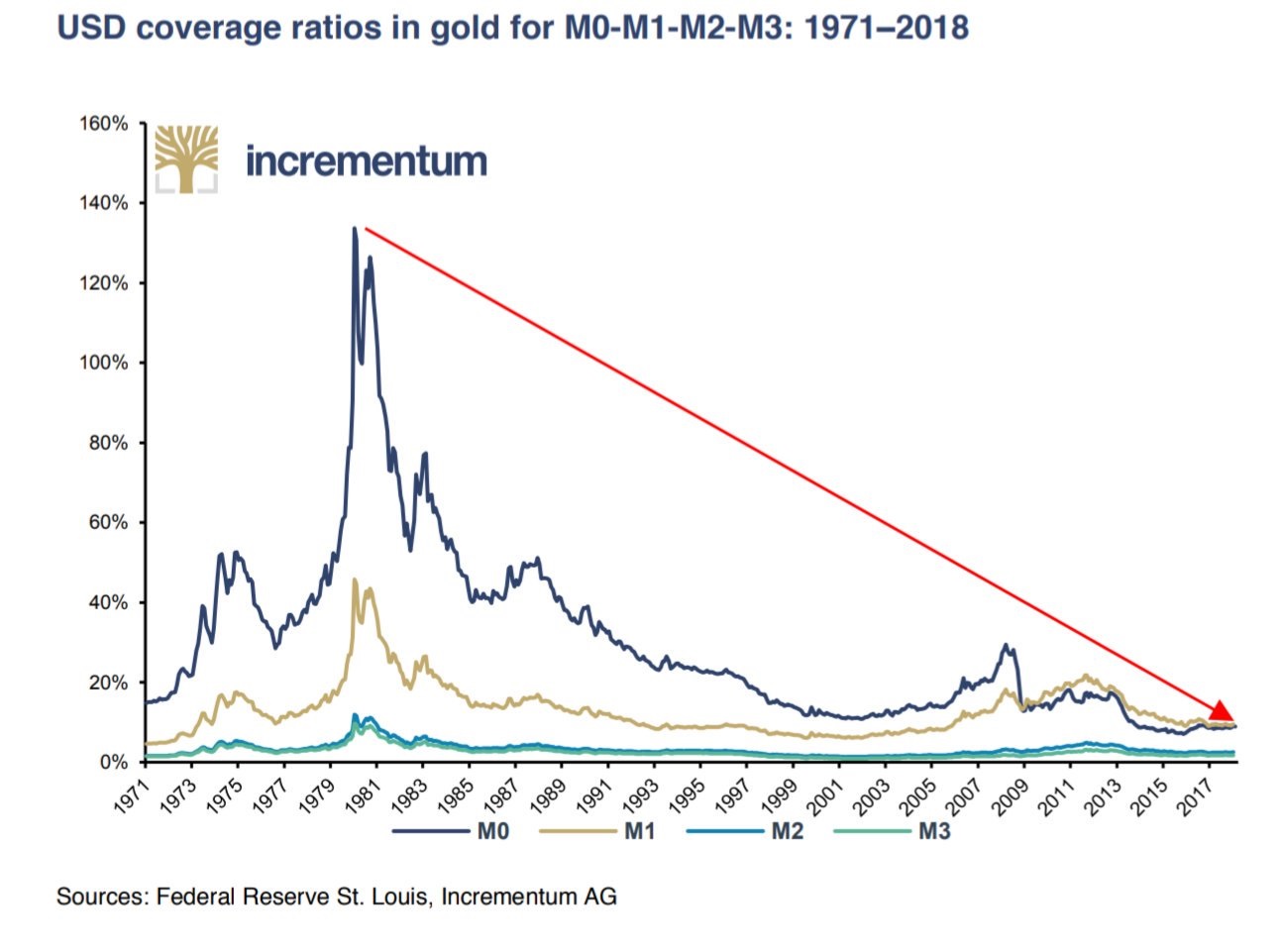

Gold Coverage

Capital Markets

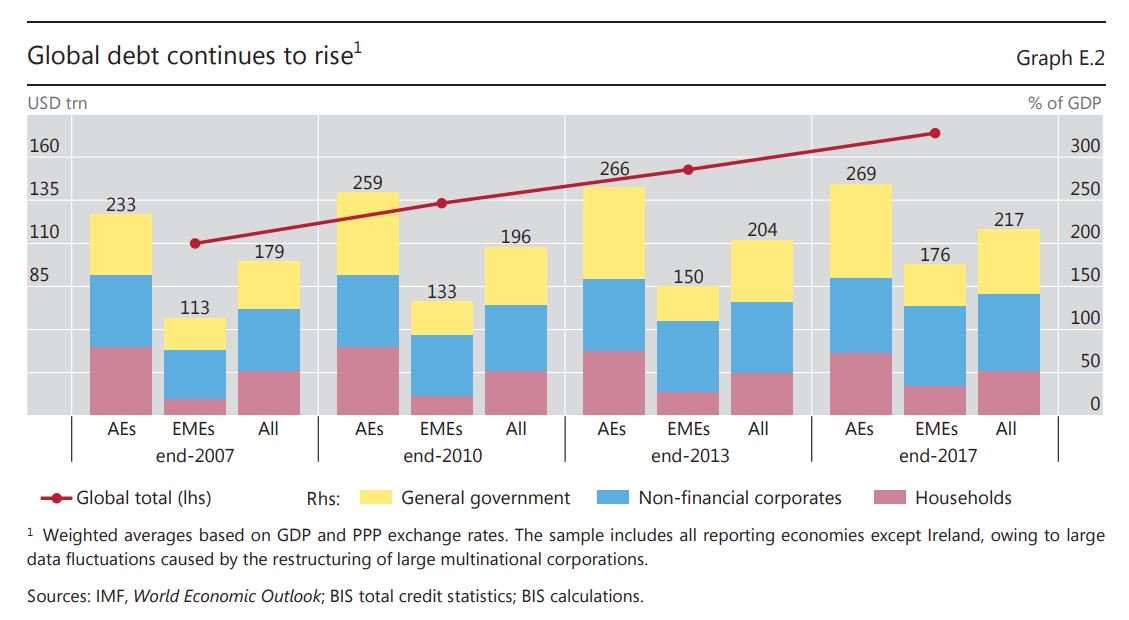

Global Debt

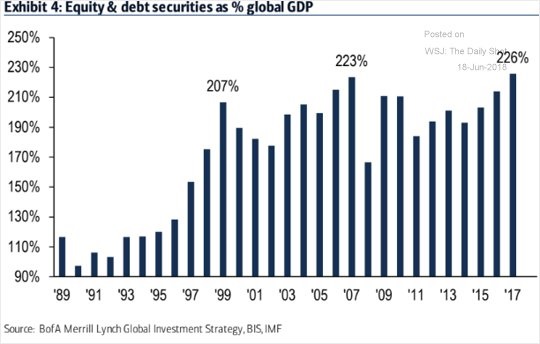

Equity and Debt to Global GDP

Global Yields

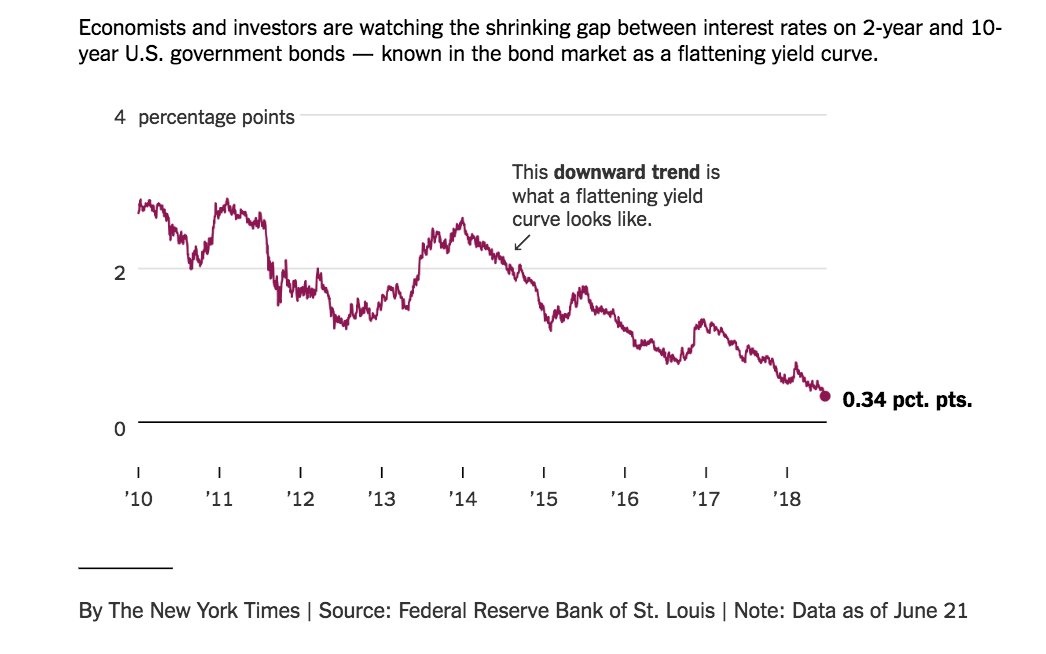

What is a flattening Yield Curve you ask?

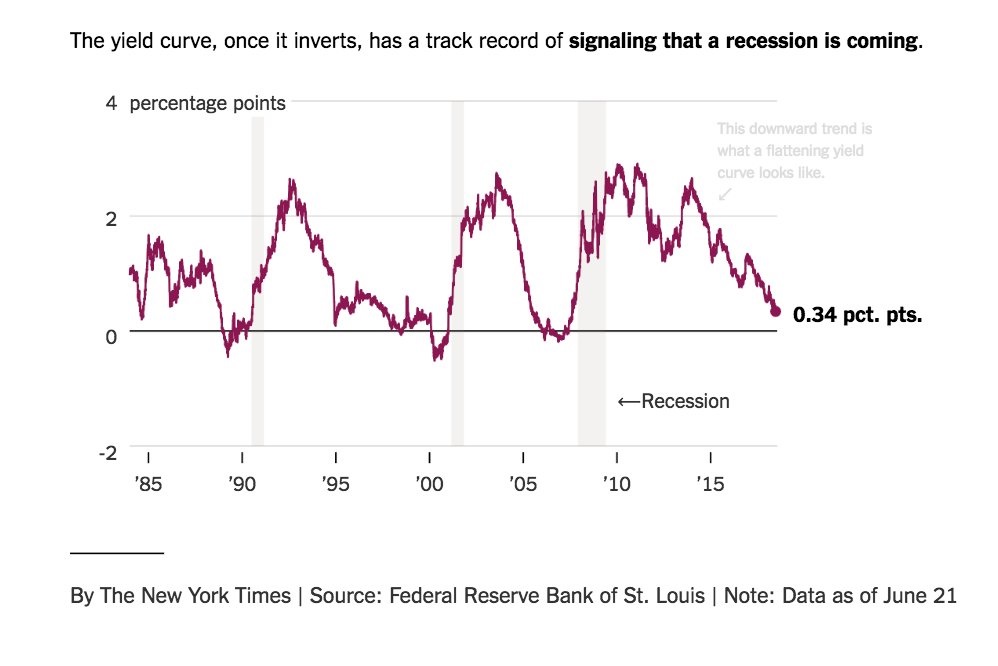

Yield Curve Inversions and Recessions

Developed Market Yield Curves

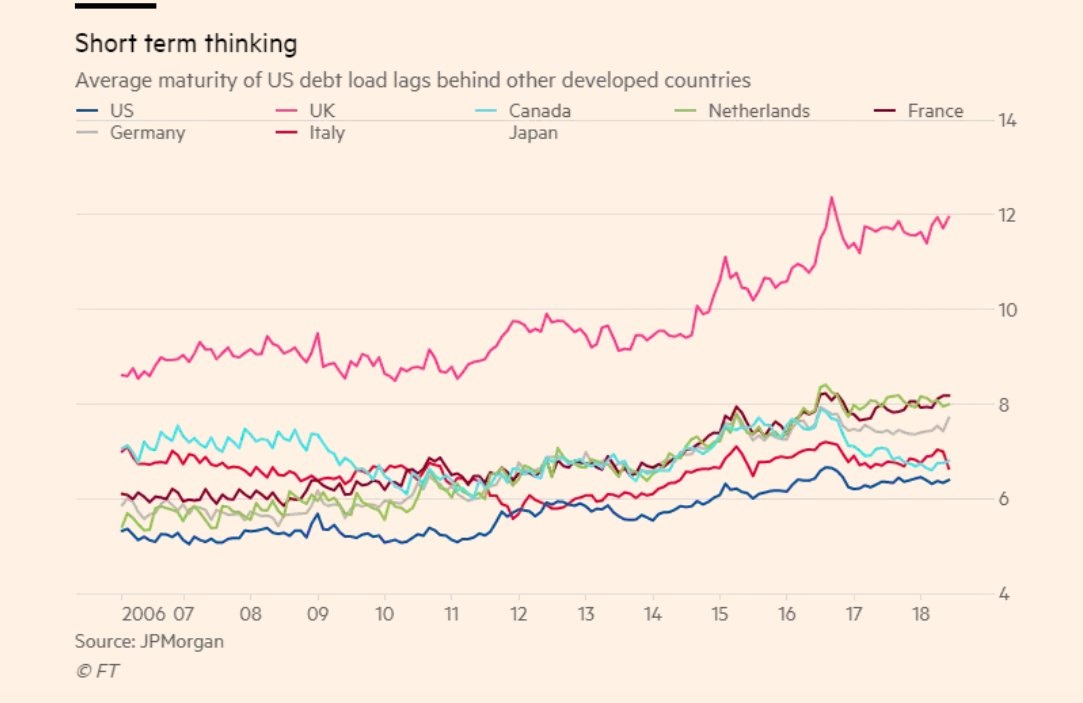

DM Maturities

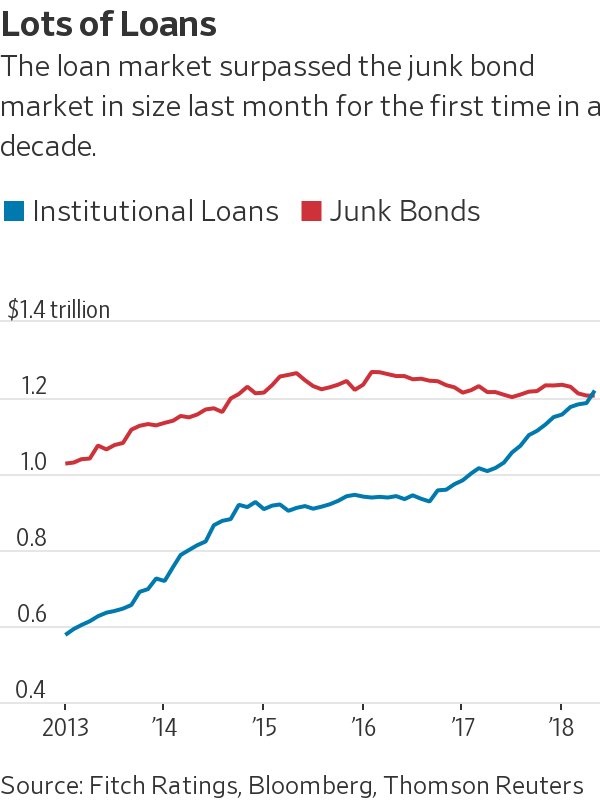

Loans and Junk Bonds

Debt Servicing – Various Developed Nations

Debt – Emerging Markets or China?

Bahrain CDS ….ice on the back of the neck

Moody’s corporate bonds – Grades since late 1990s

China International Reserves – China/Japan UST holdings

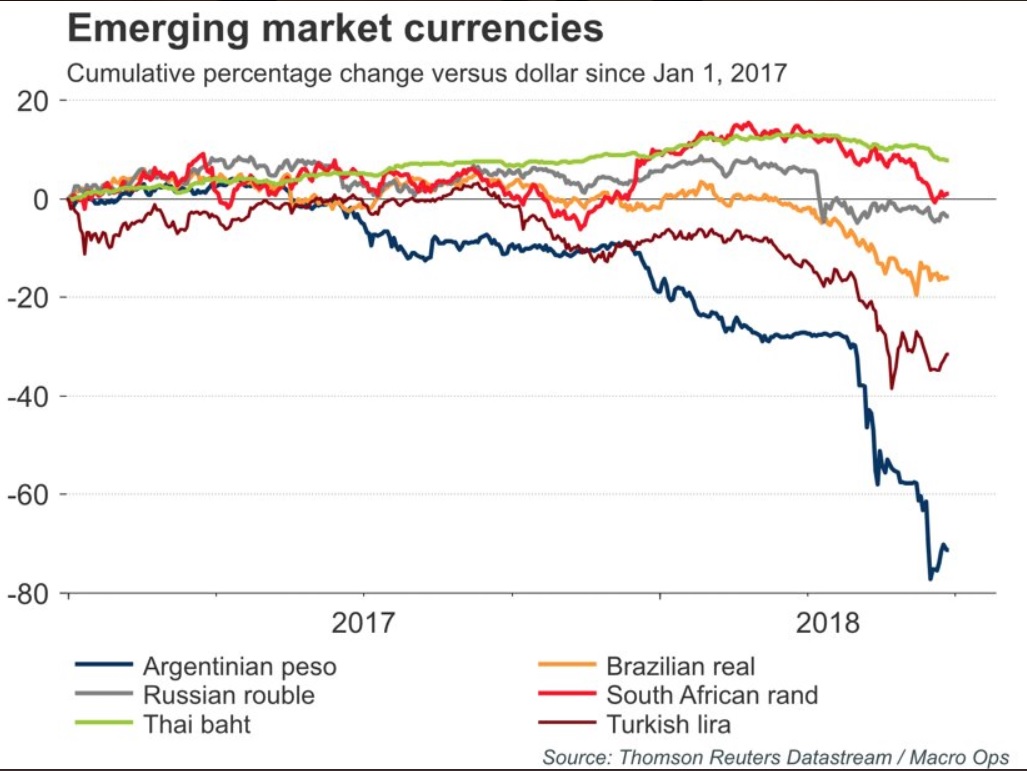

EM Currencies v USD since start 2017

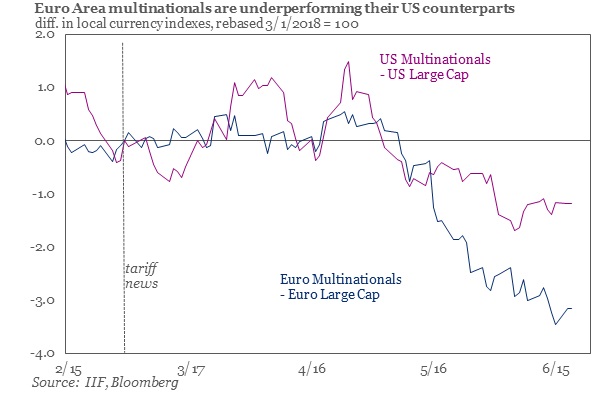

US and Euro Large Caps

CNY – USD

INR – USD

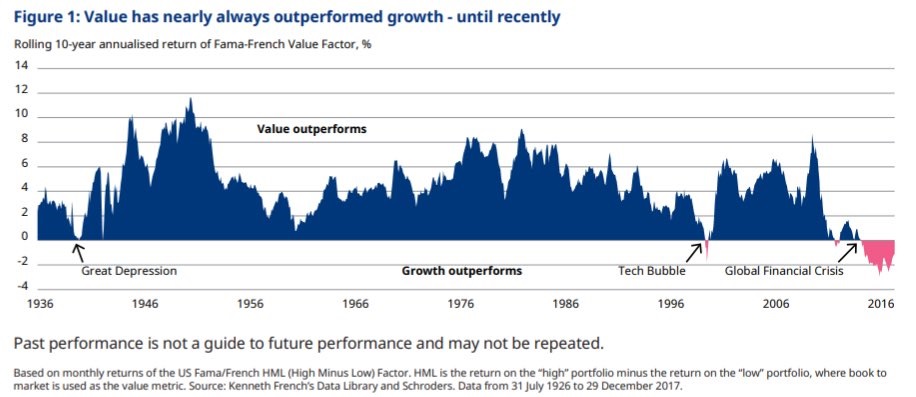

Value and Growth – What is now telling us?

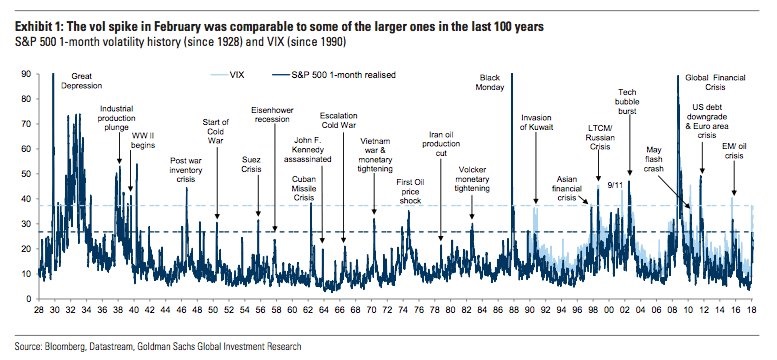

S&P 500 and VIX

Global Macro

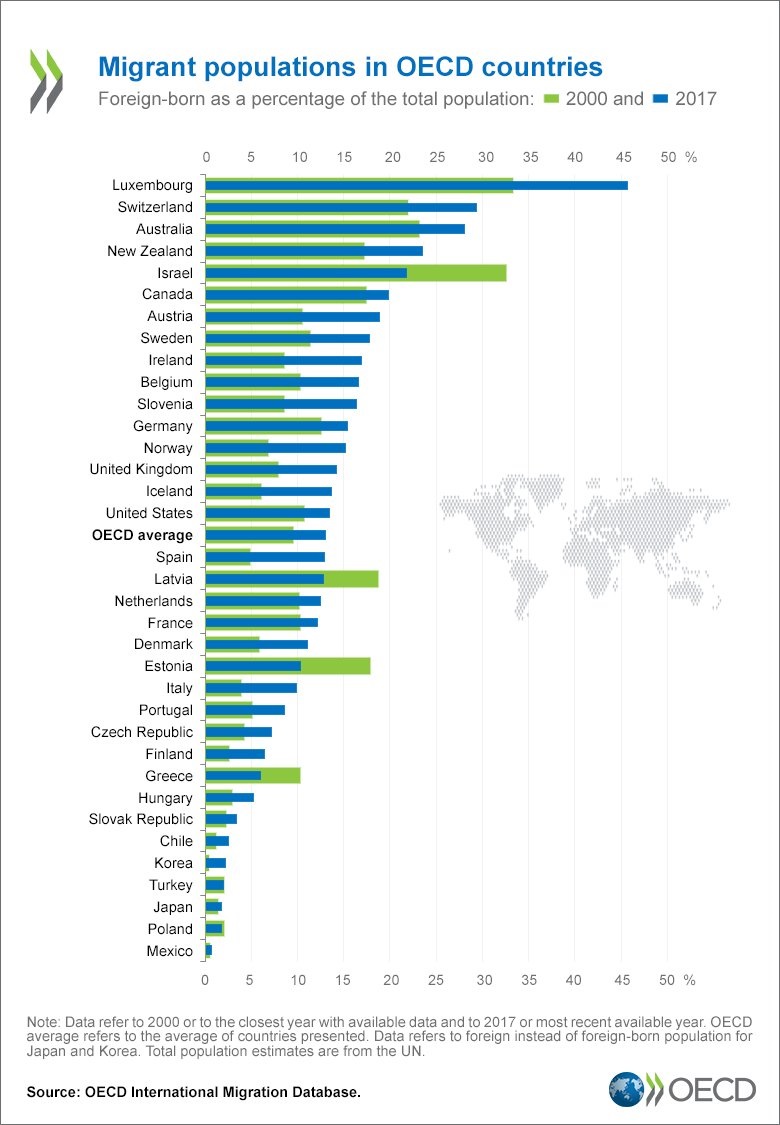

Foreign Born Percentage of Population – OECD

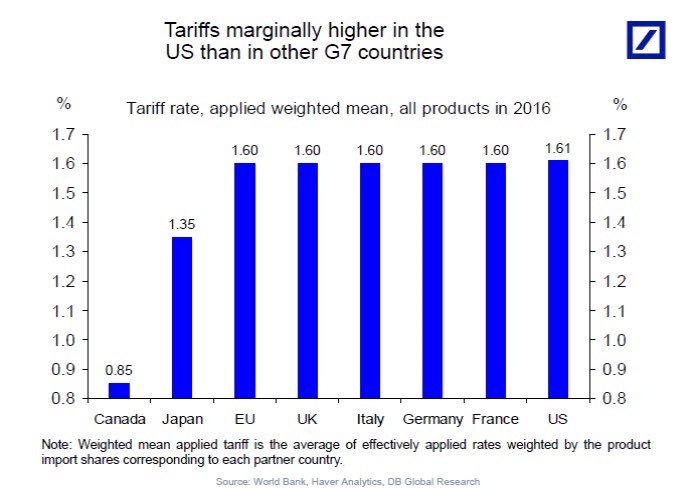

United States and G7 Tariffs

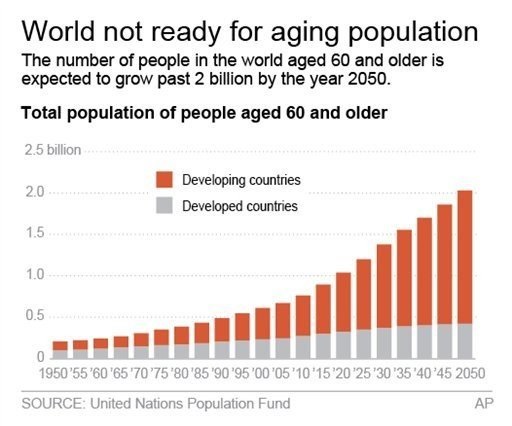

Global over 60s

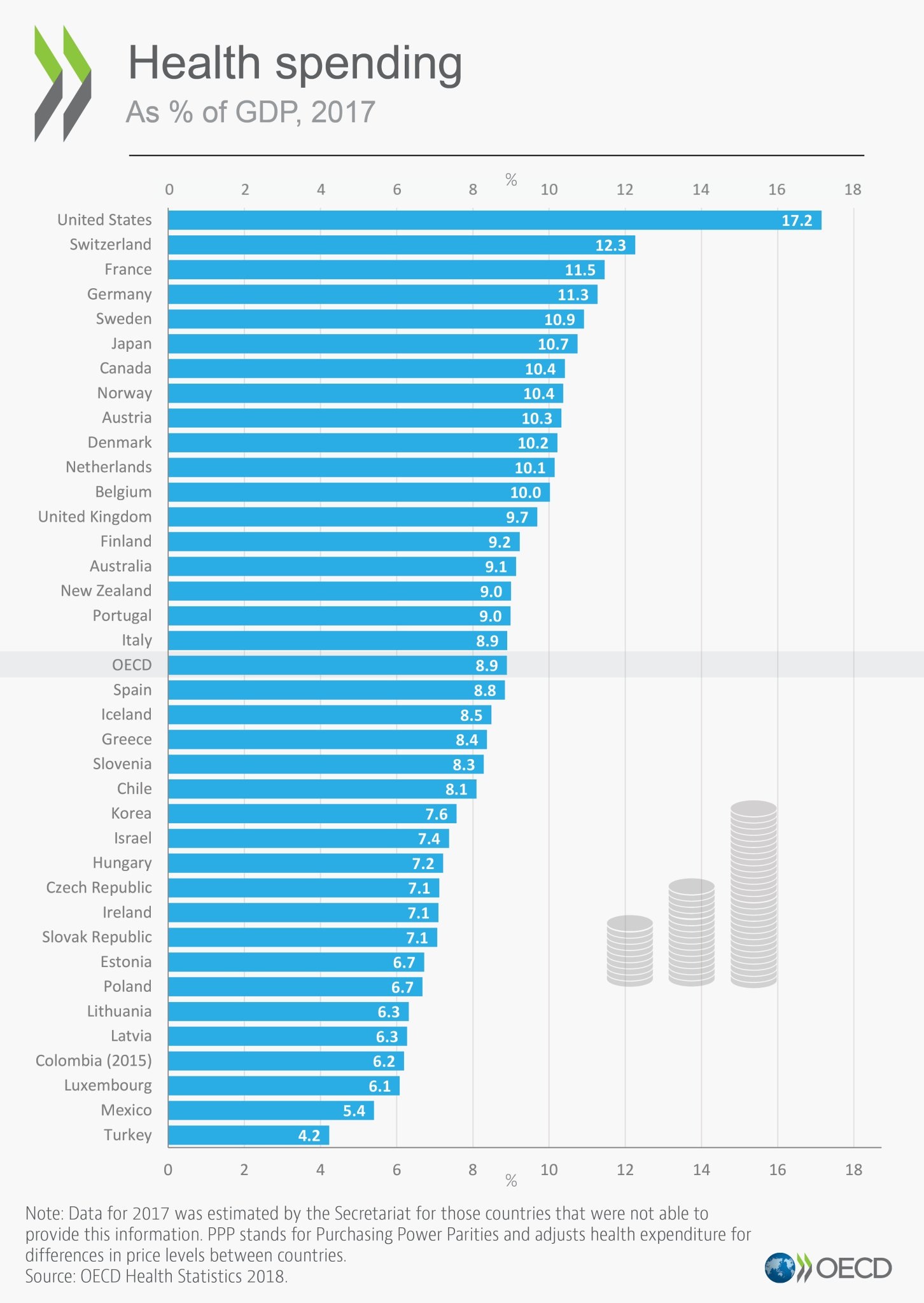

Health Spending

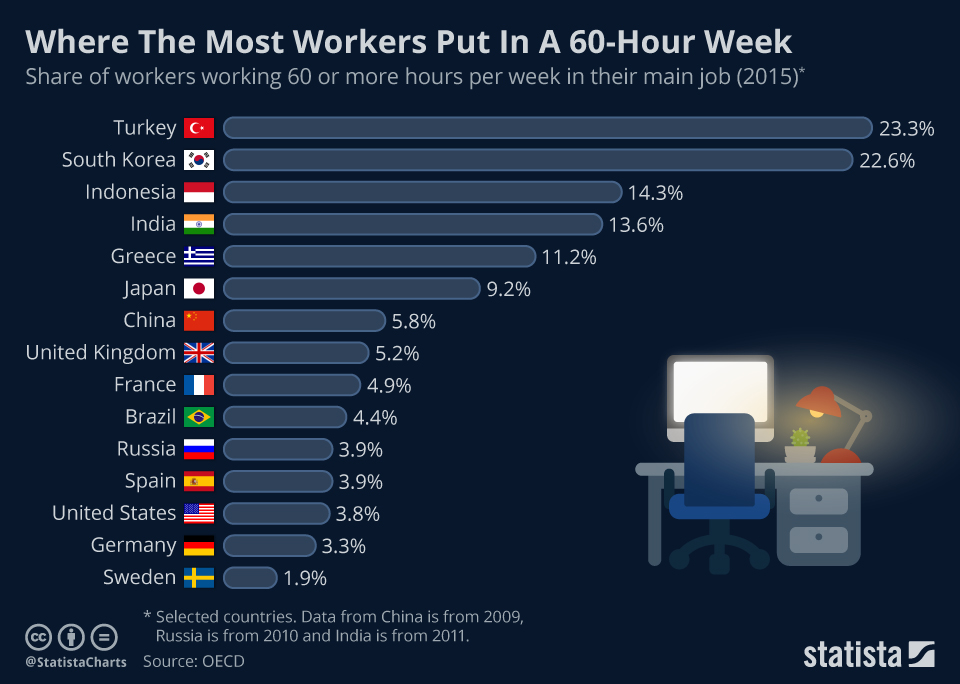

Workers doing 60 hour weeks

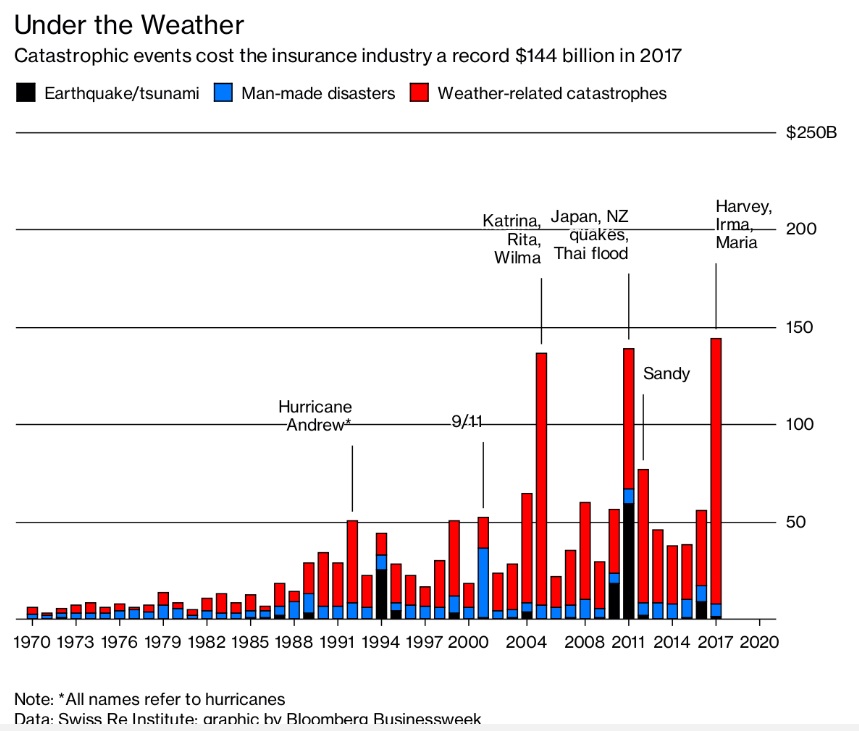

Catastrophes and Insurance

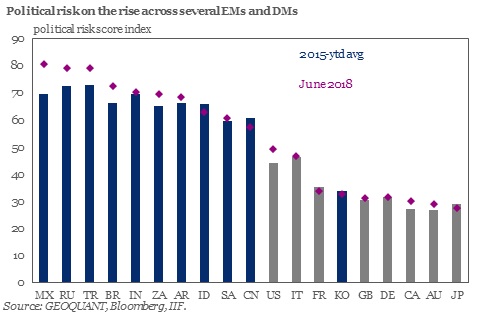

Political Risks – Selected EM & DMs

Major Global Cities – Purchasing Power

US Based remittances

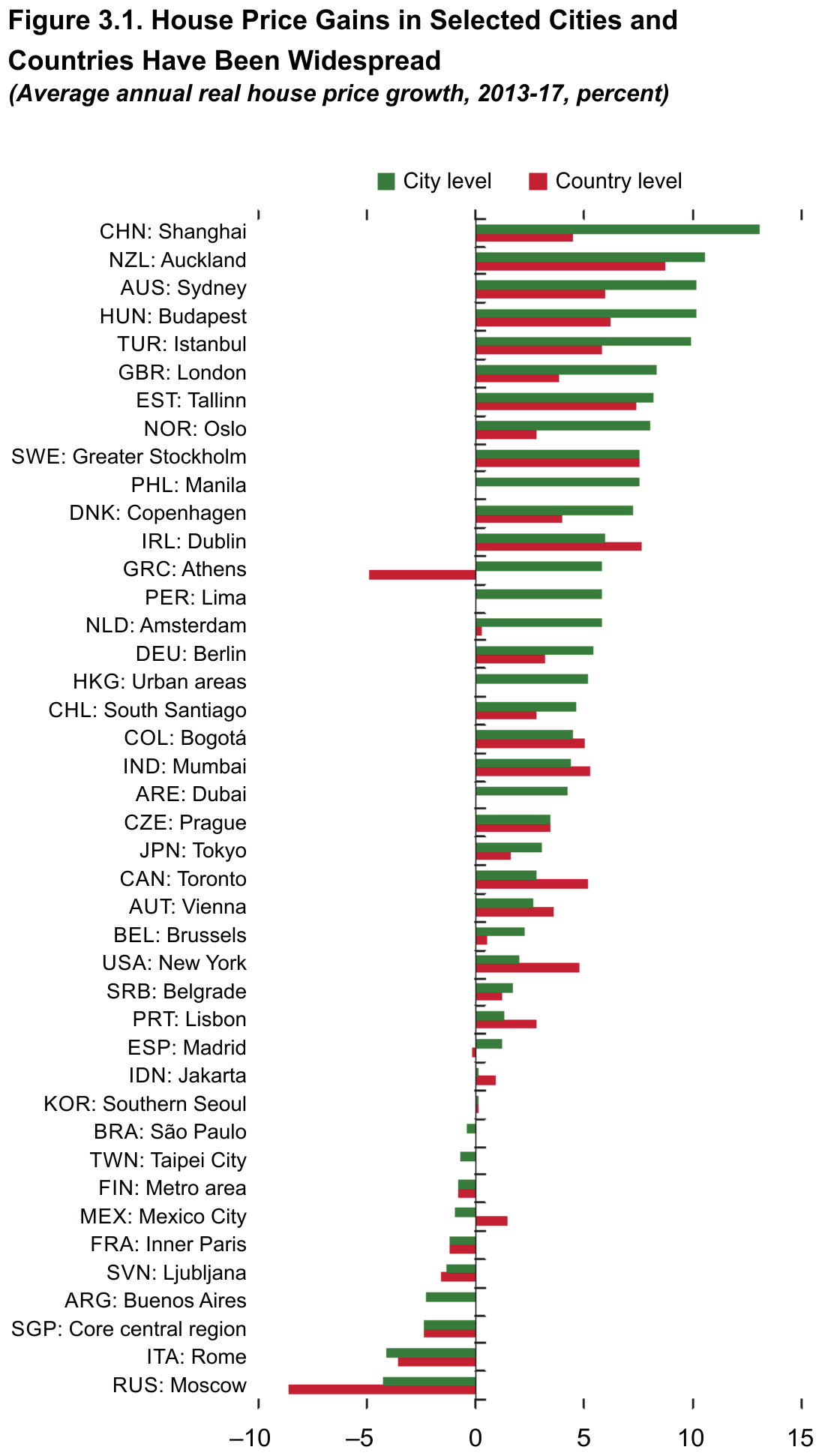

House Price Gains 2013 – 2017 – various global cities

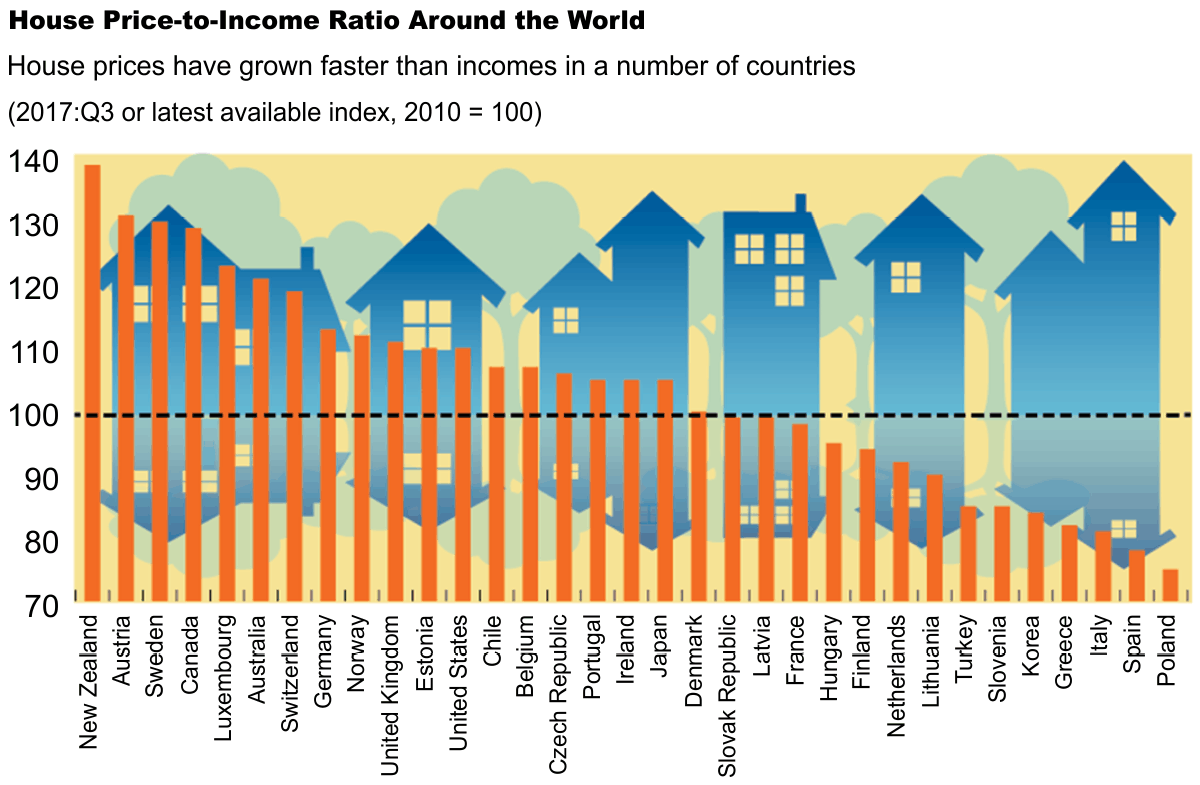

Major Global House Prices to Income

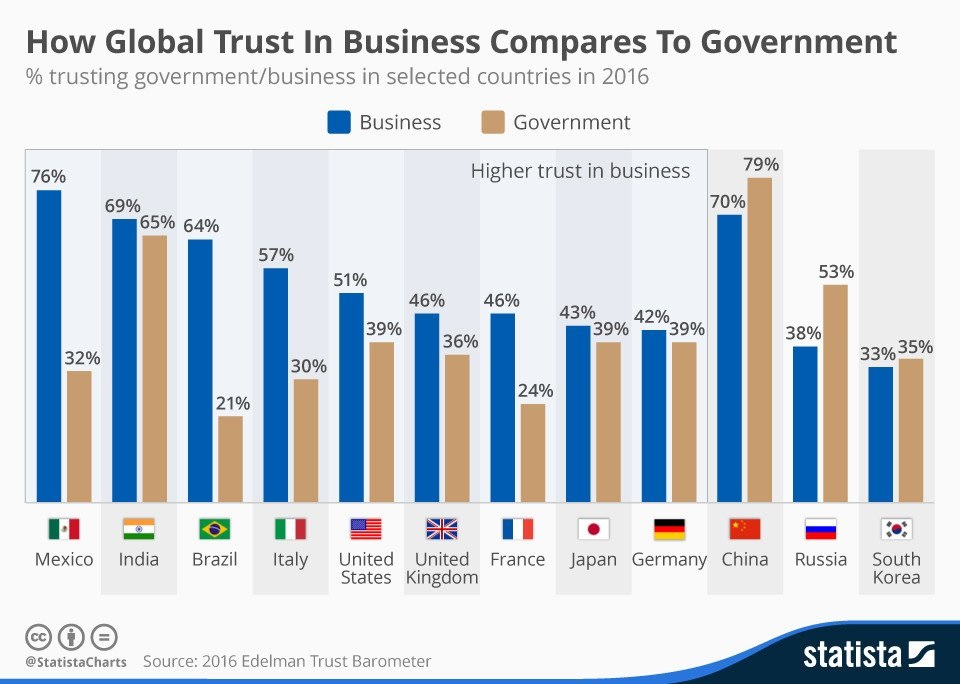

Global Trust in Business and Government

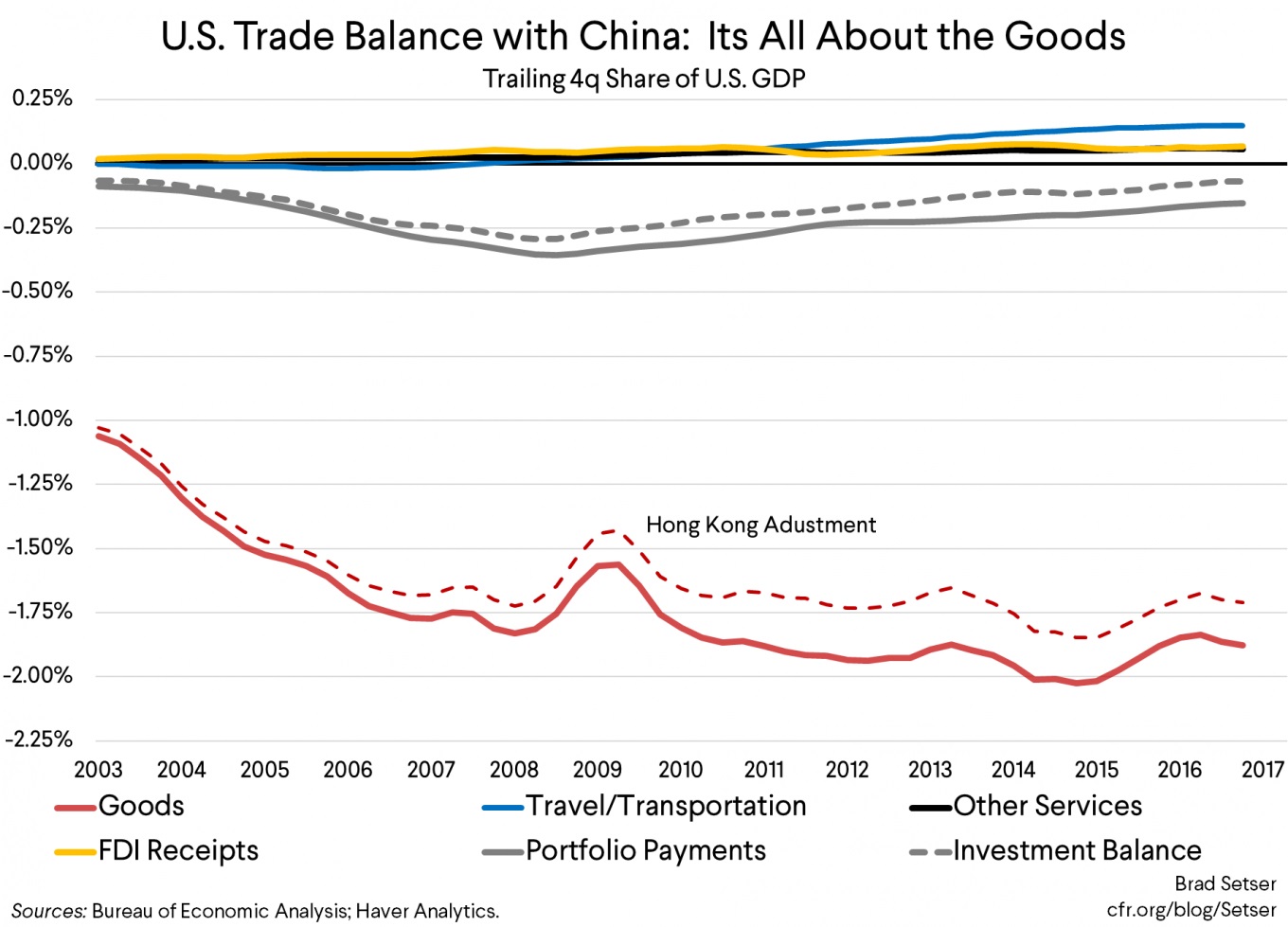

US China Trade Imbalance

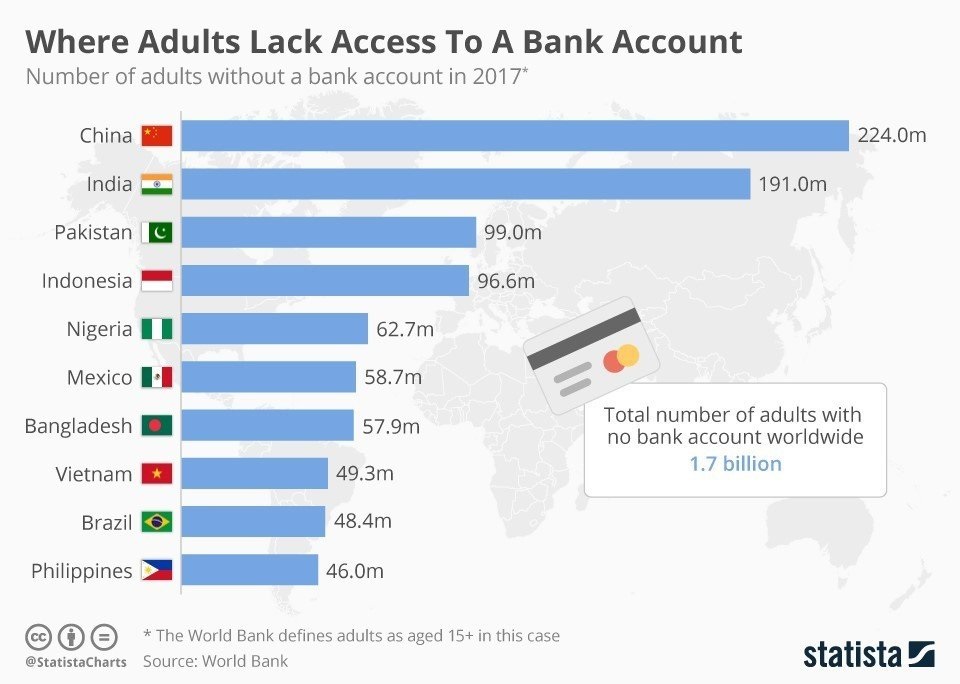

People without access to bank accounts

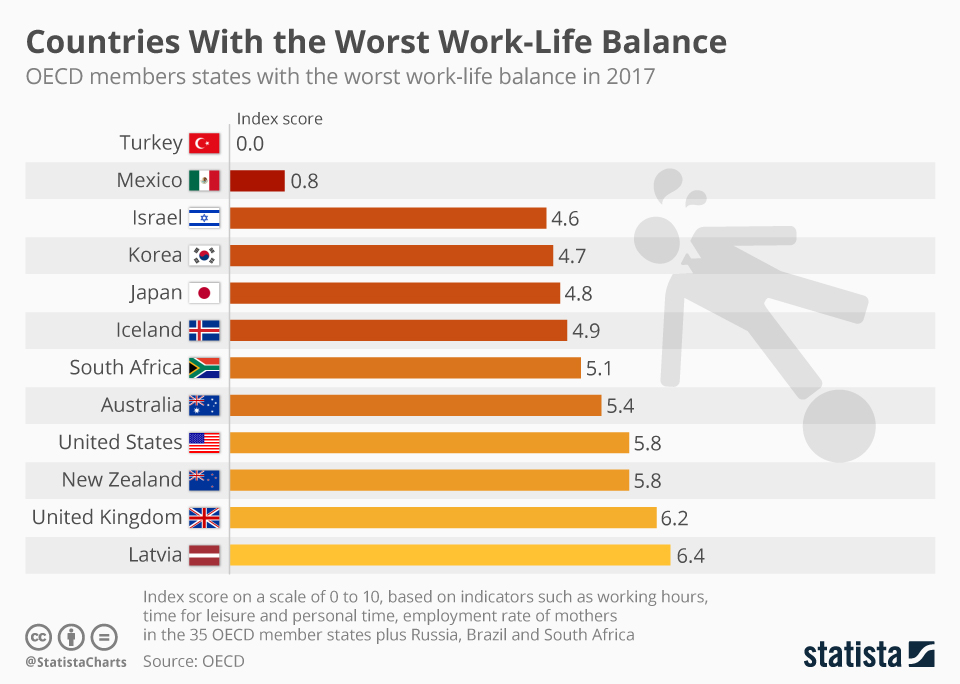

OECD – Work – Life Balances

…and furthermore…

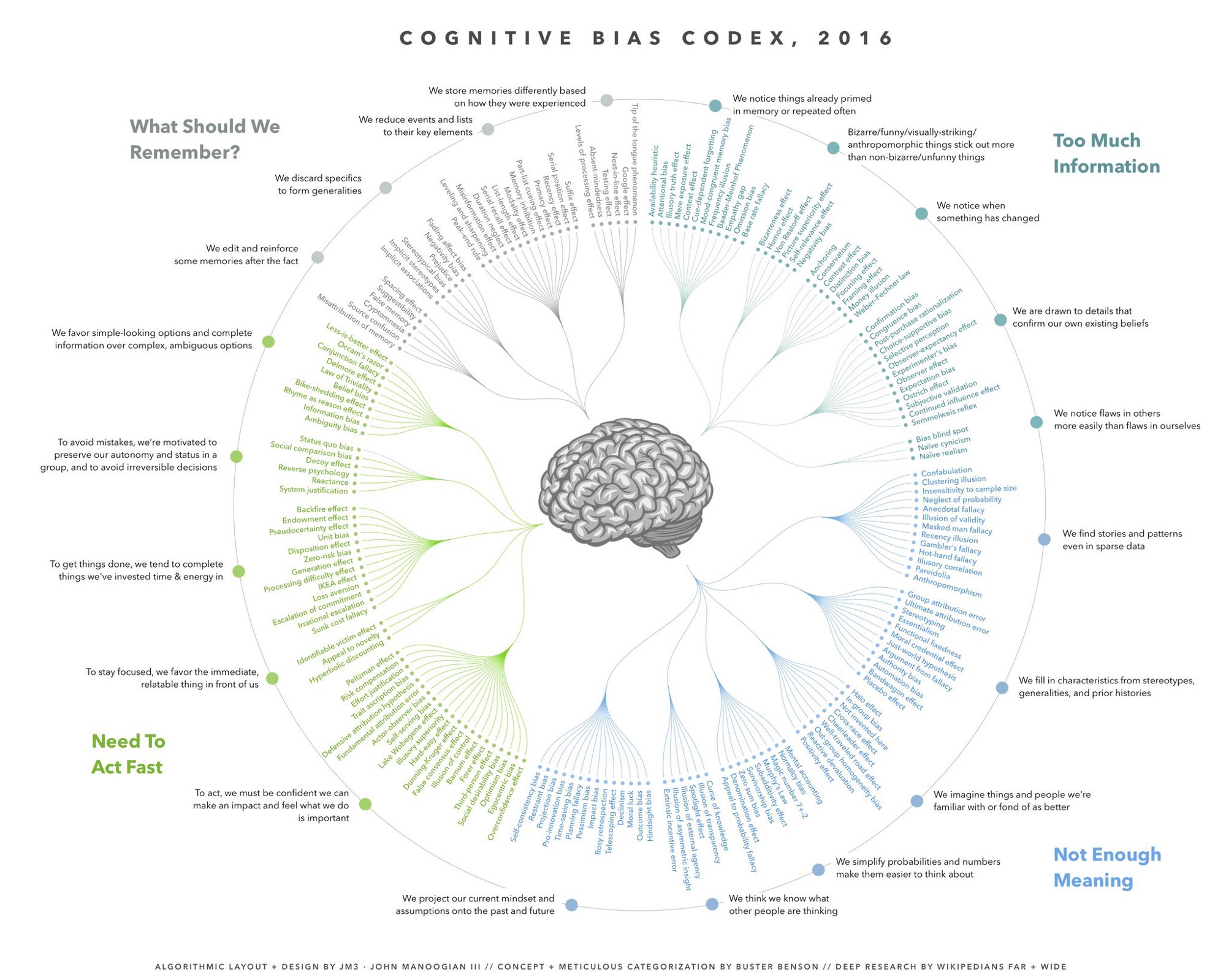

Cognitive Bias

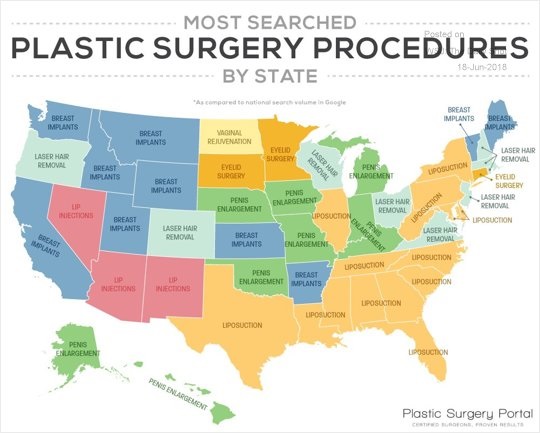

Plastic Surgery searches – US States

The World’s Major Brands

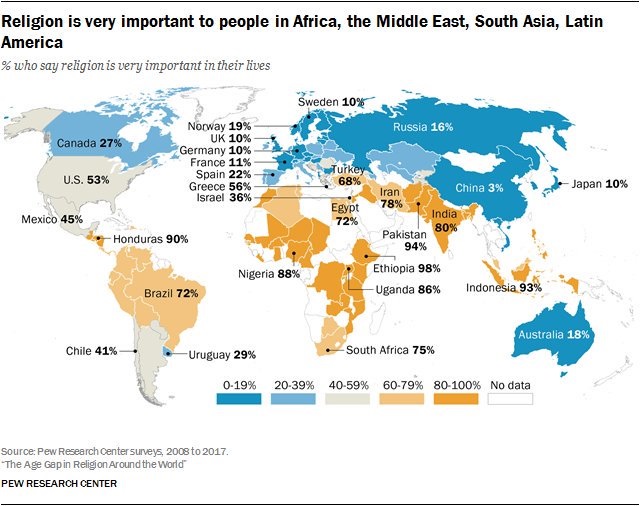

The World’s Major Religions

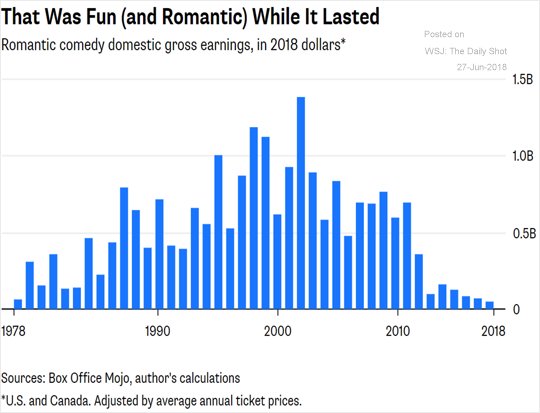

The Demise of the RomCom

Spend an Extra Hour in Bed