Australia

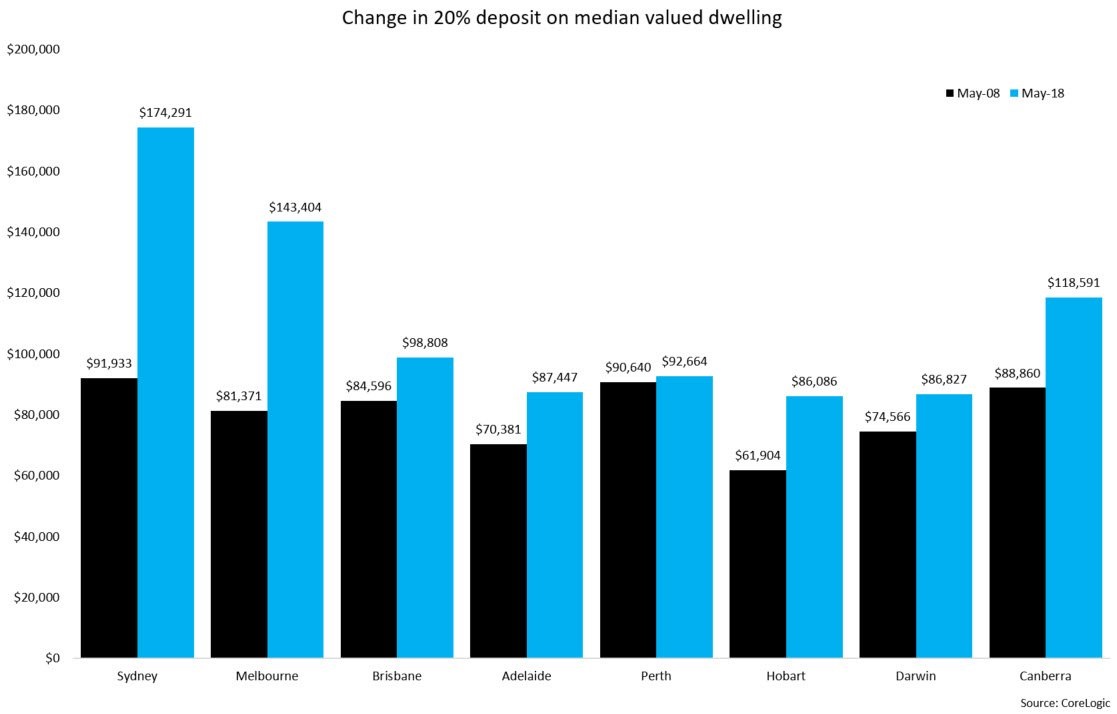

Australia – change in 20% deposit for median priced dwelling, major cities 2008-2018

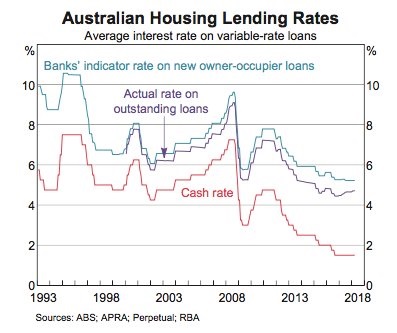

Australian mortgage rates

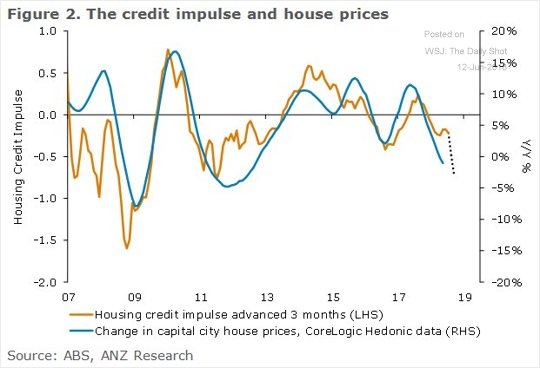

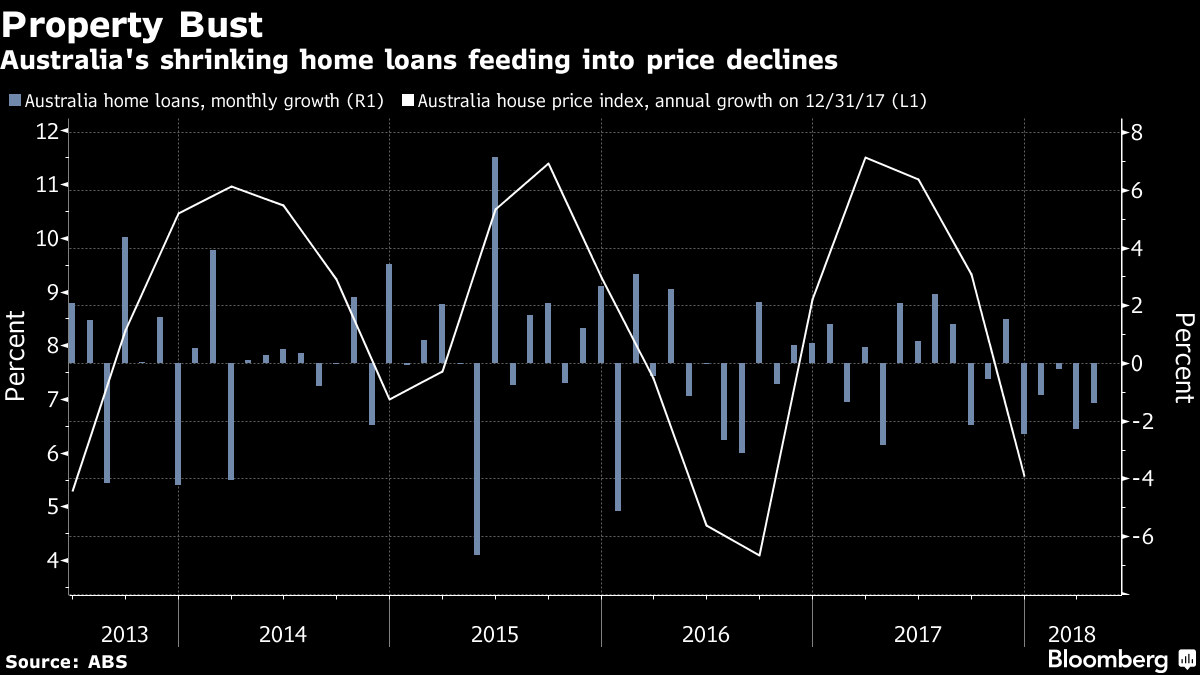

Australia – Credit impulse and house prices (1)

Australian lending growth and house prices (2)

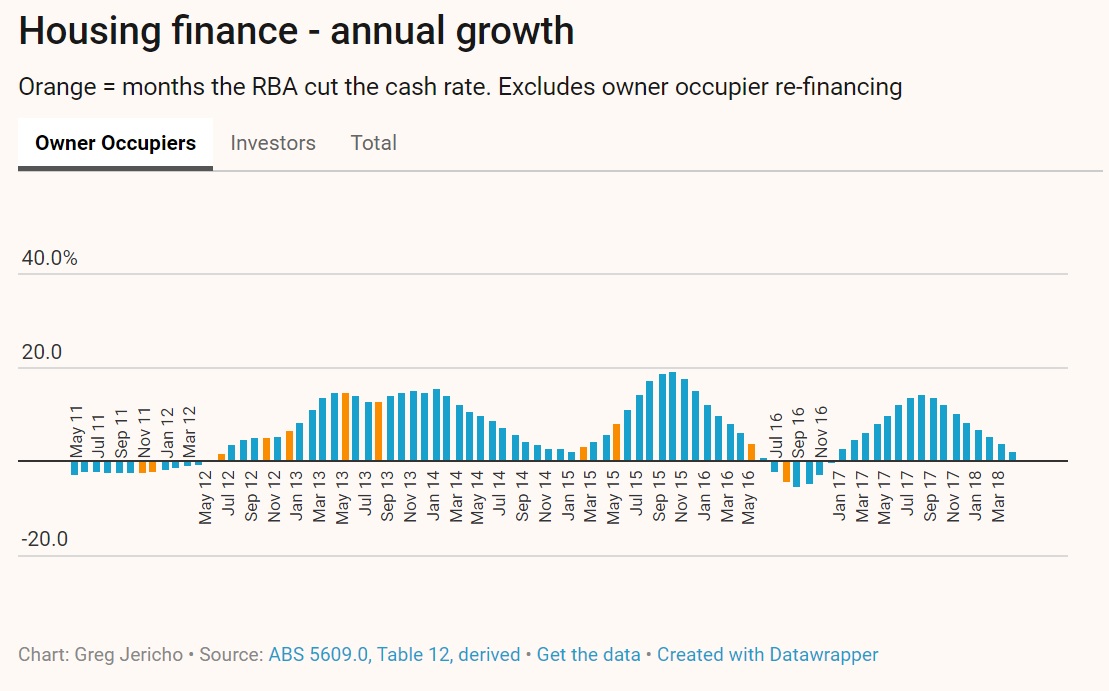

Housing Finance, Annual Growth – Owner occupiers

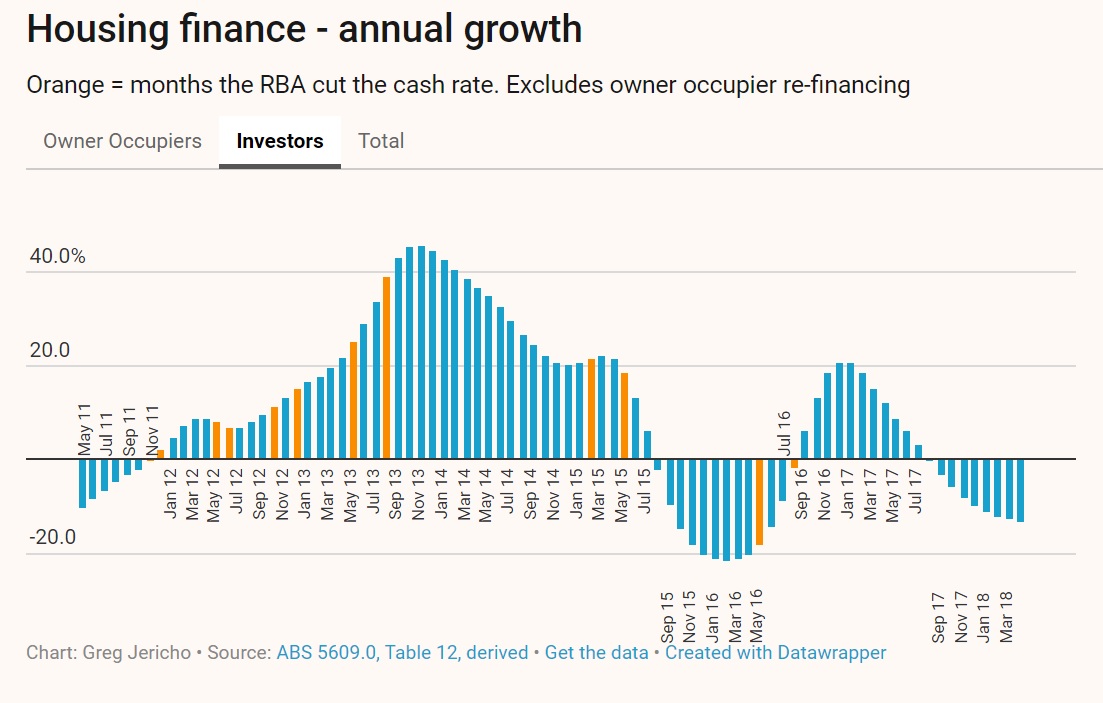

Housing Finance, Annual Growth – specufestors

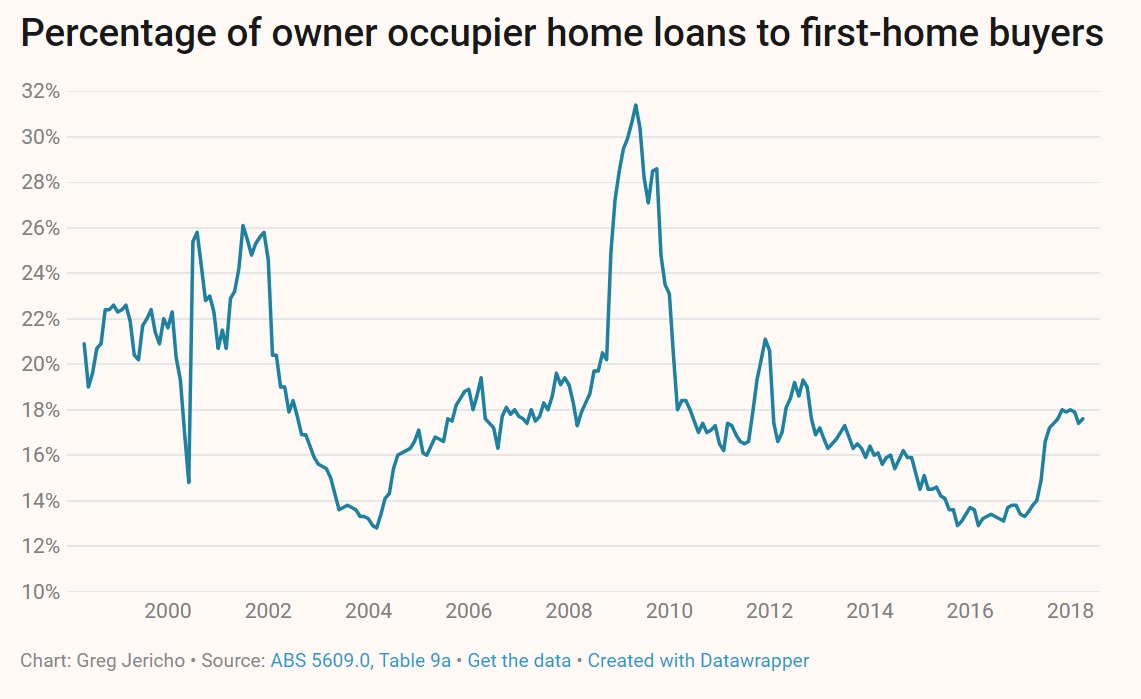

Housing Finance, First Home Buyers – Percent of lending

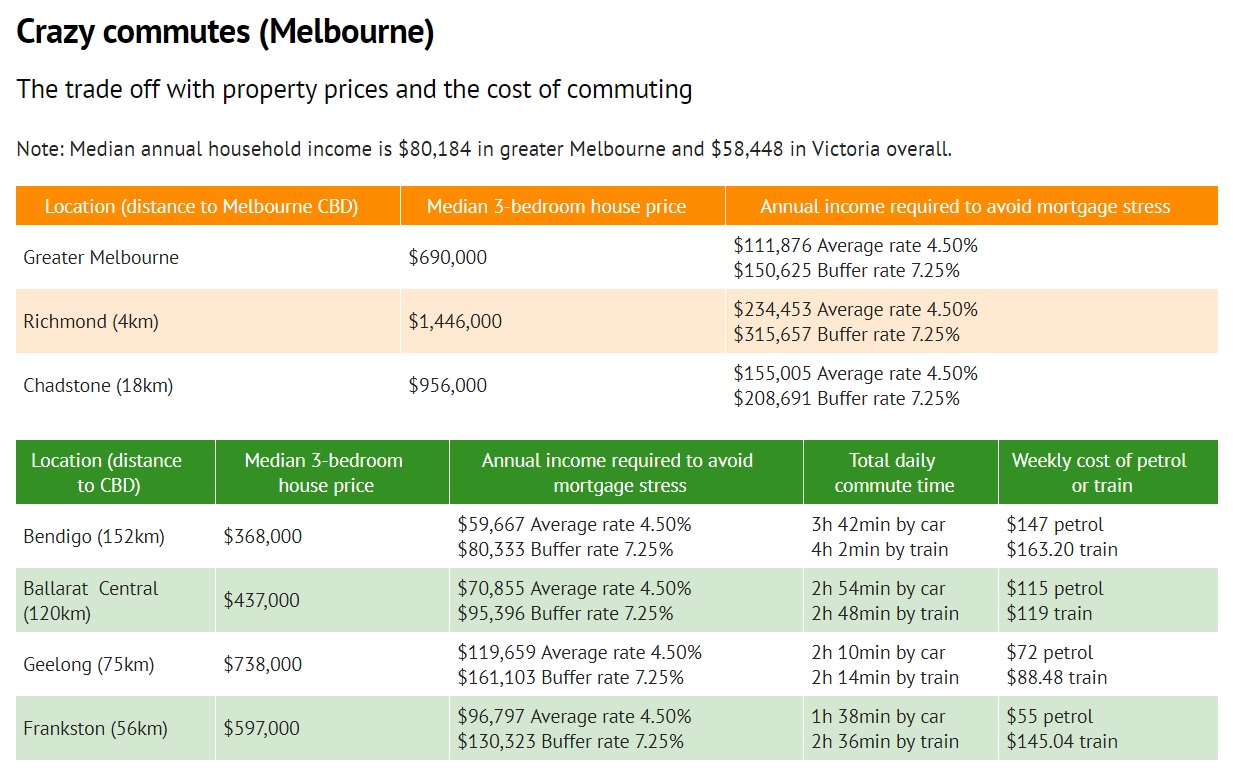

Crazy Commutes – Melbourne

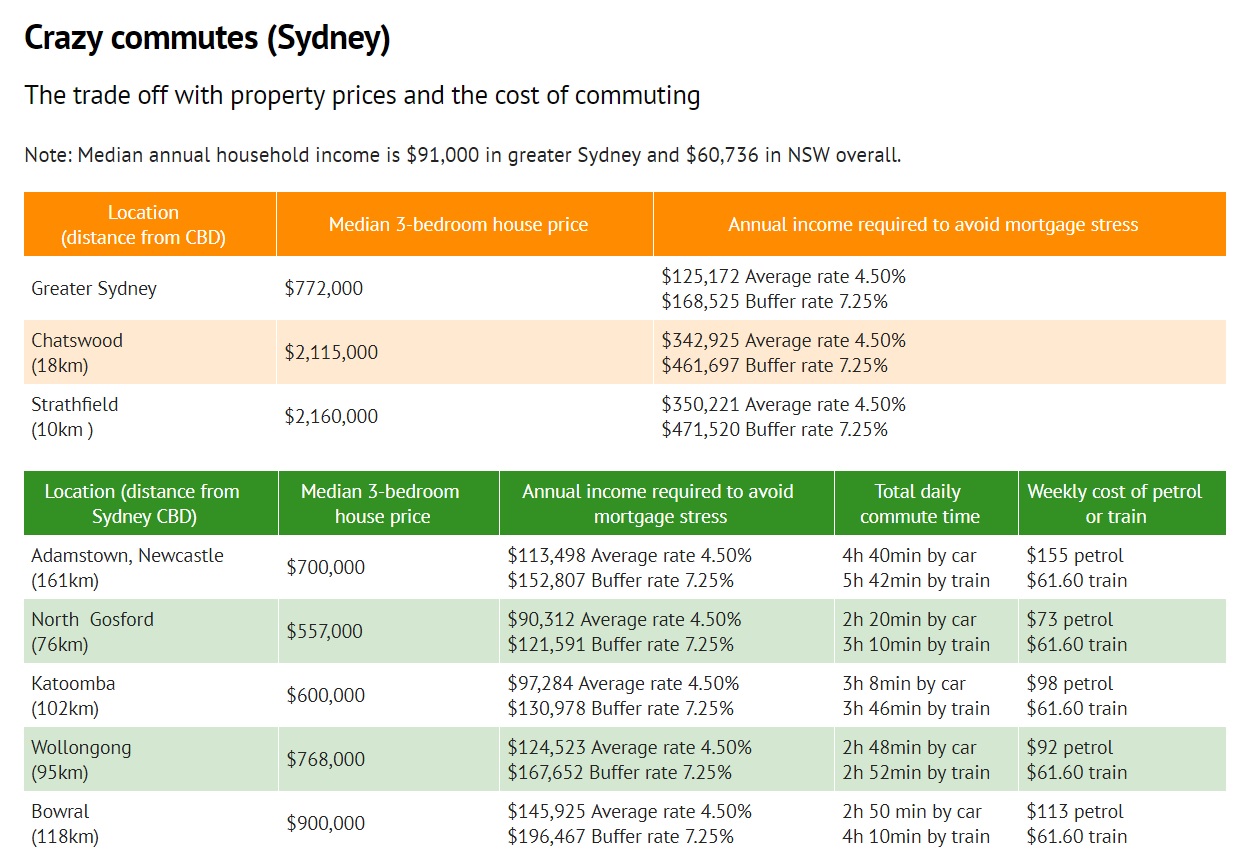

Crazy Commutes – Sydney

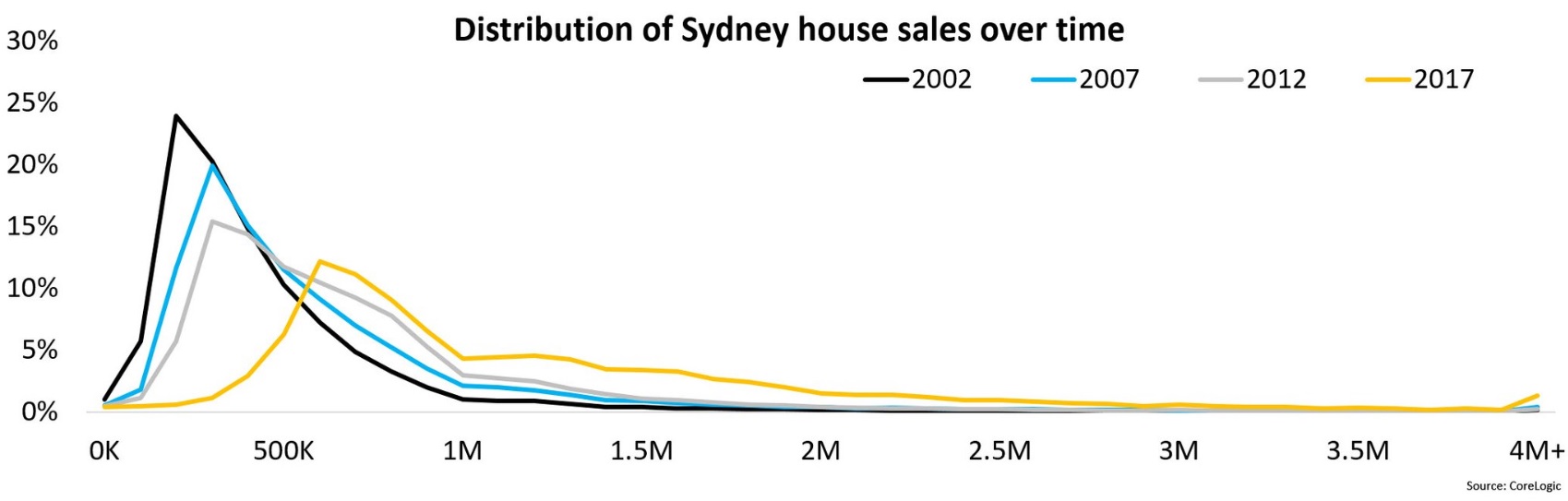

Sydney House Price sales over time

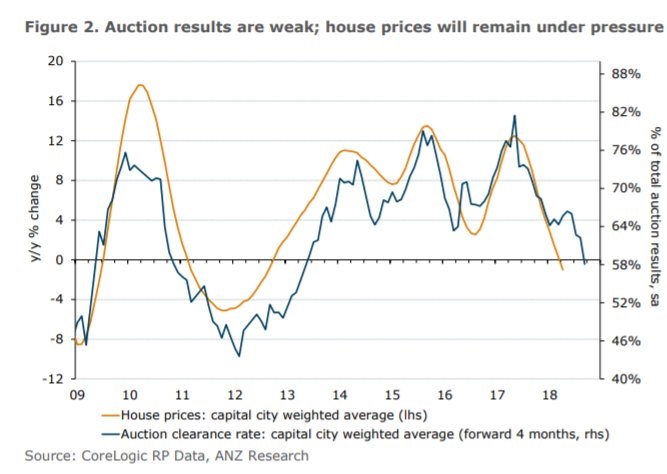

Australia – Auction Clearances and house prices

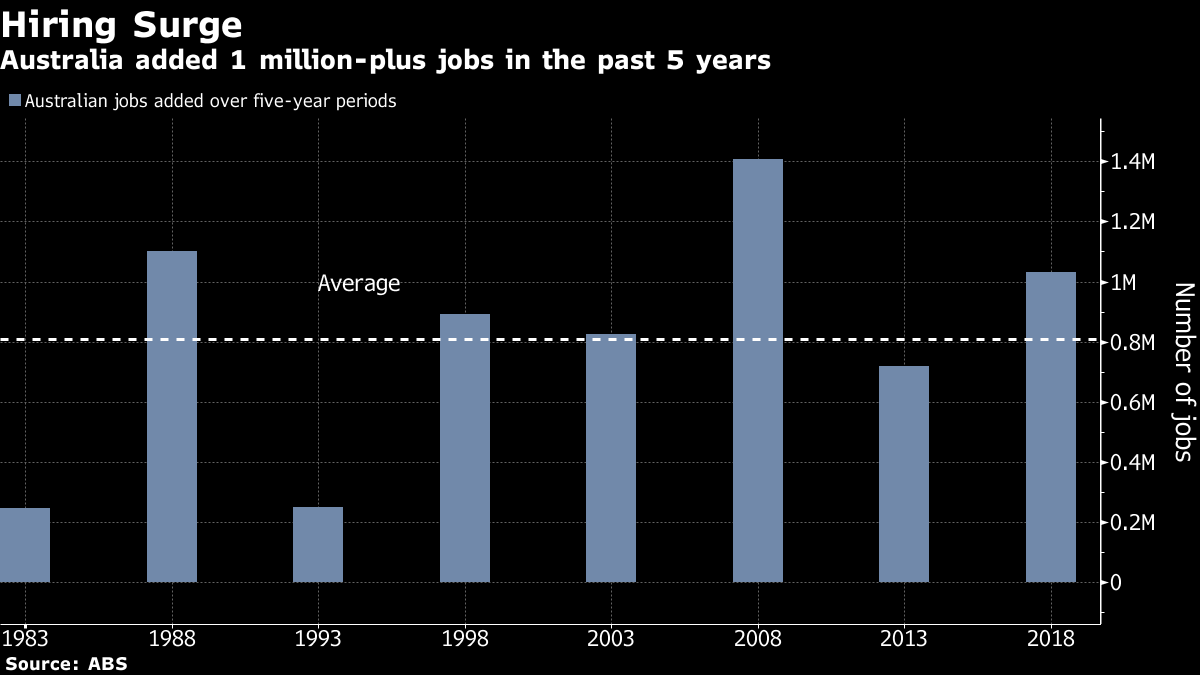

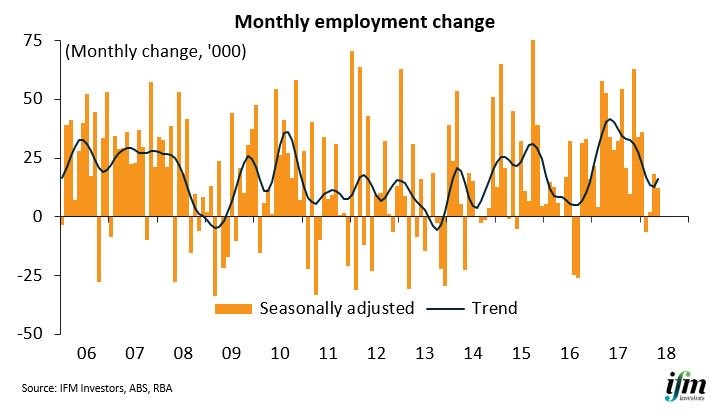

Australia – employment growth

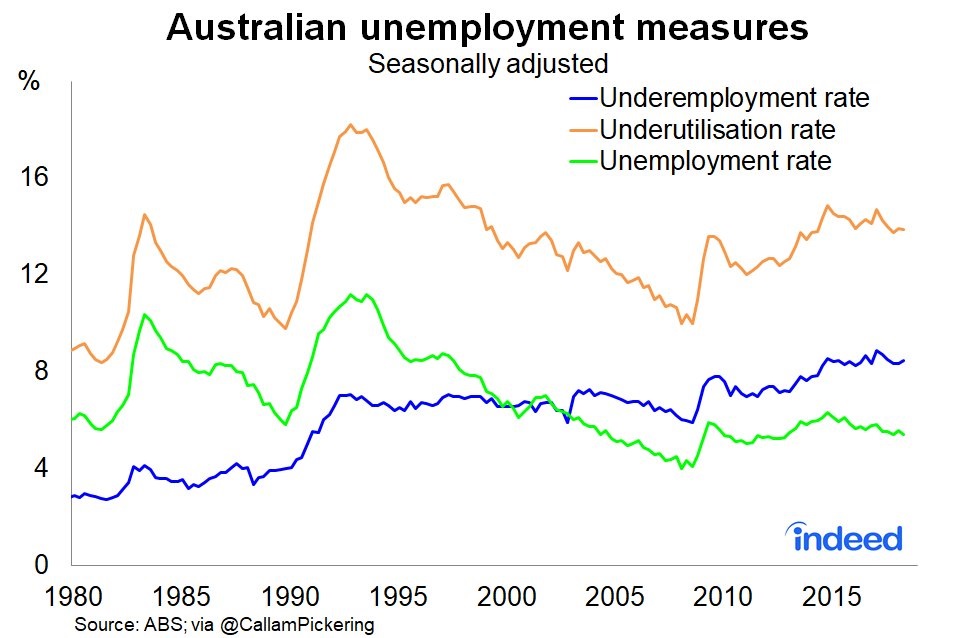

Australian Unemployment

Australian unemployment – various measures

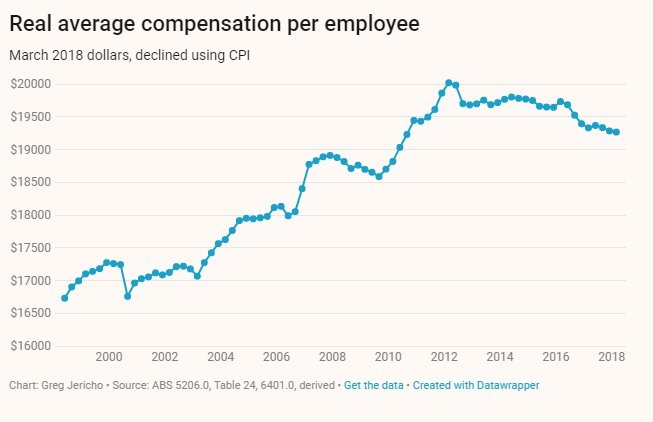

Australia – Real Average Compensation per Employee

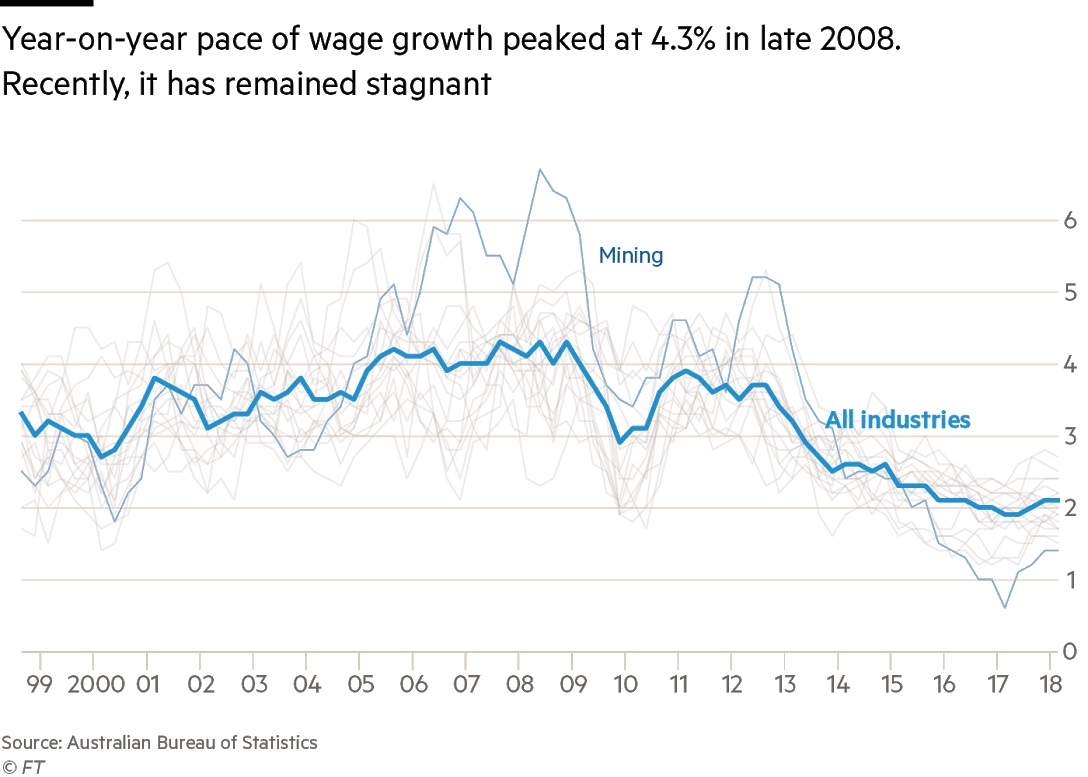

Australia – Wages growth

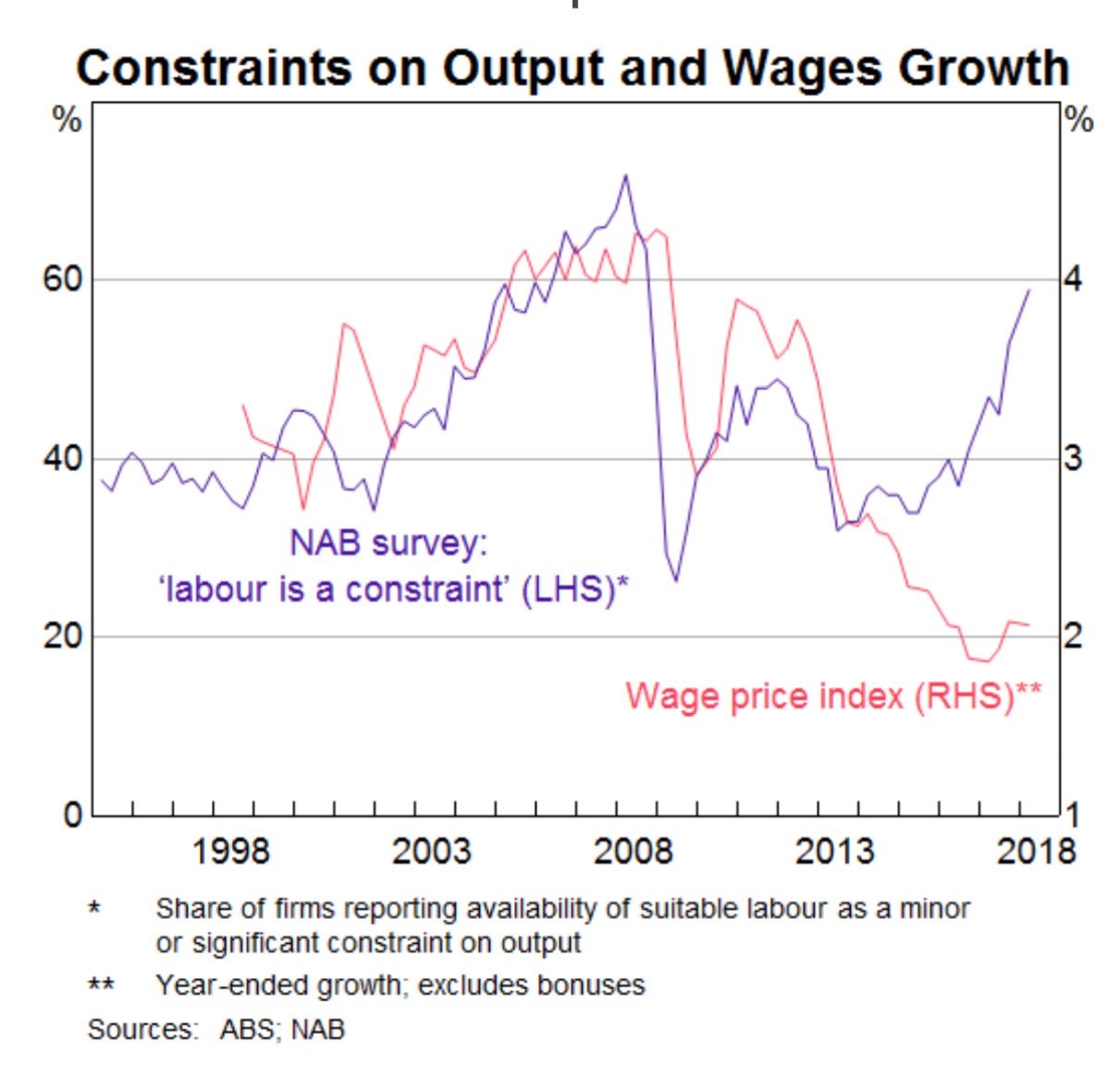

Australia – labour constraints and wages

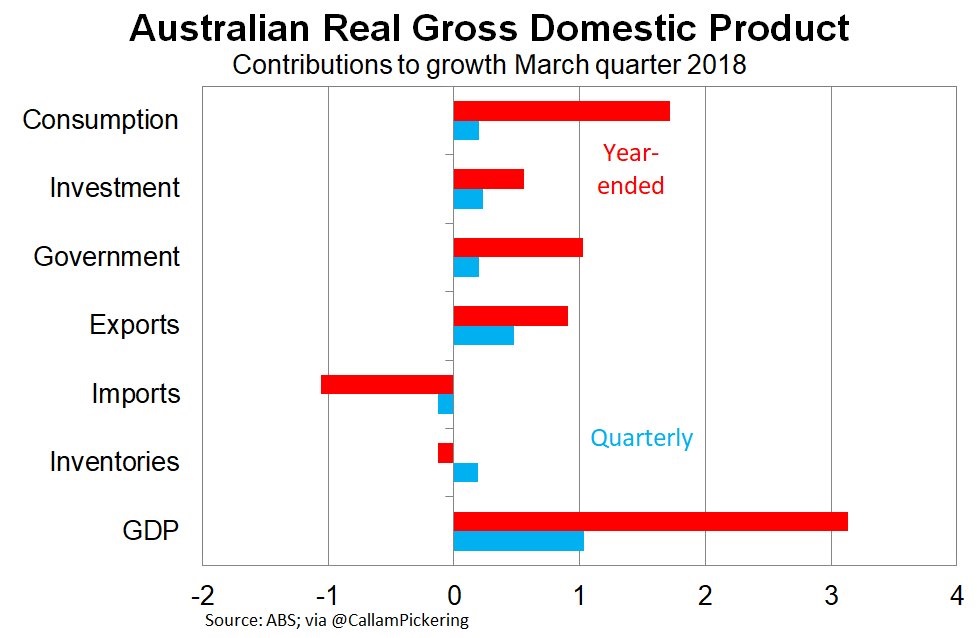

Australian Real GDP – Contributing sectors

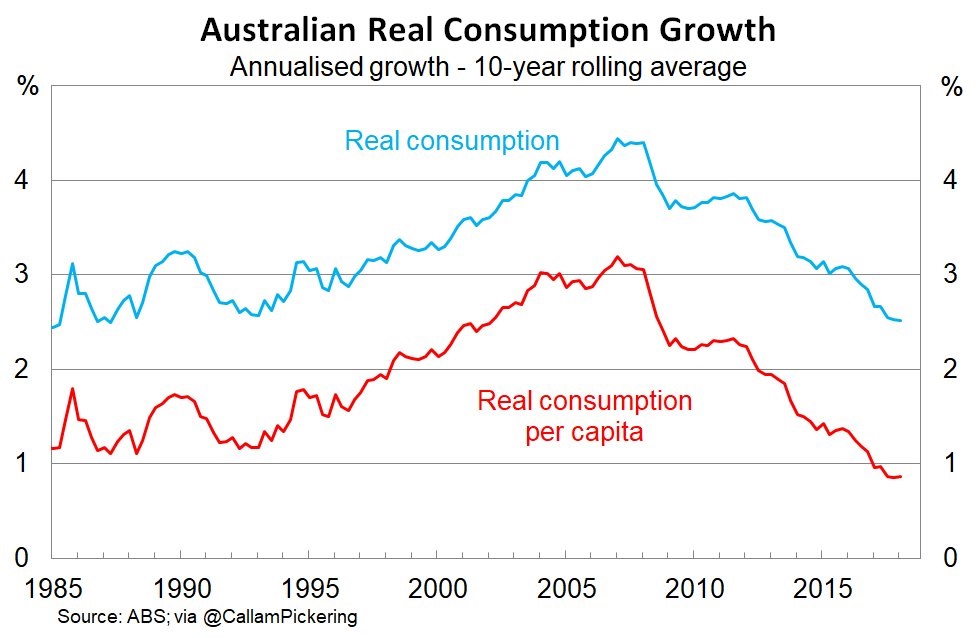

Australia – Consumption

Australia – Household Outlays

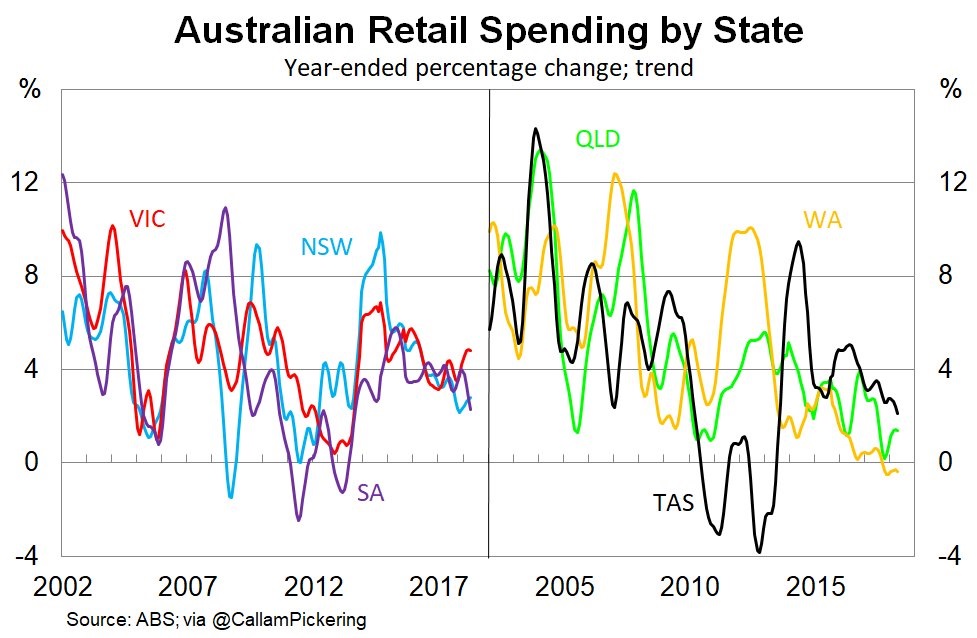

Australian Retail Spending by state

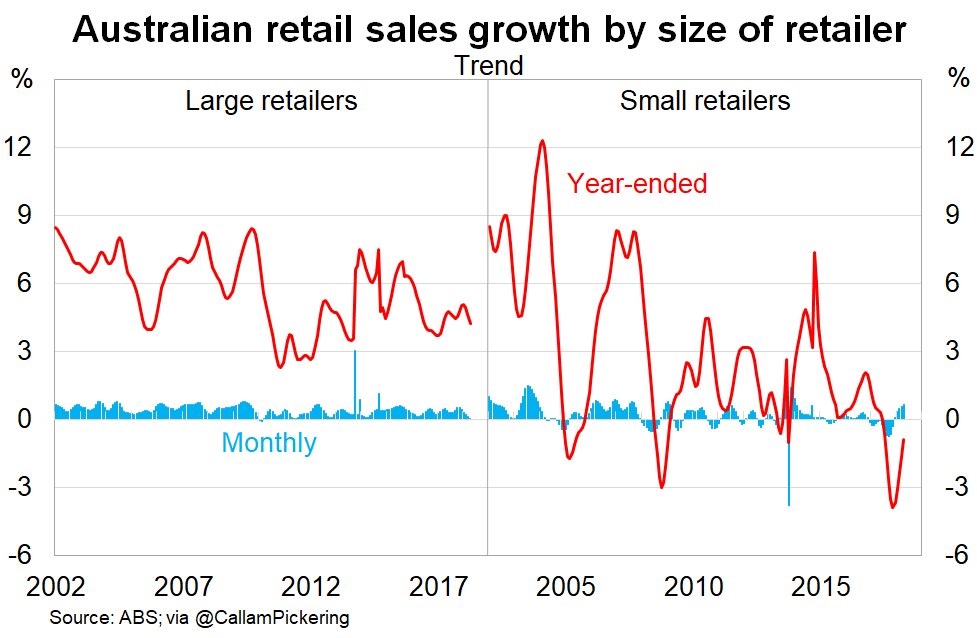

Australian Retail Sales growth and retailer size

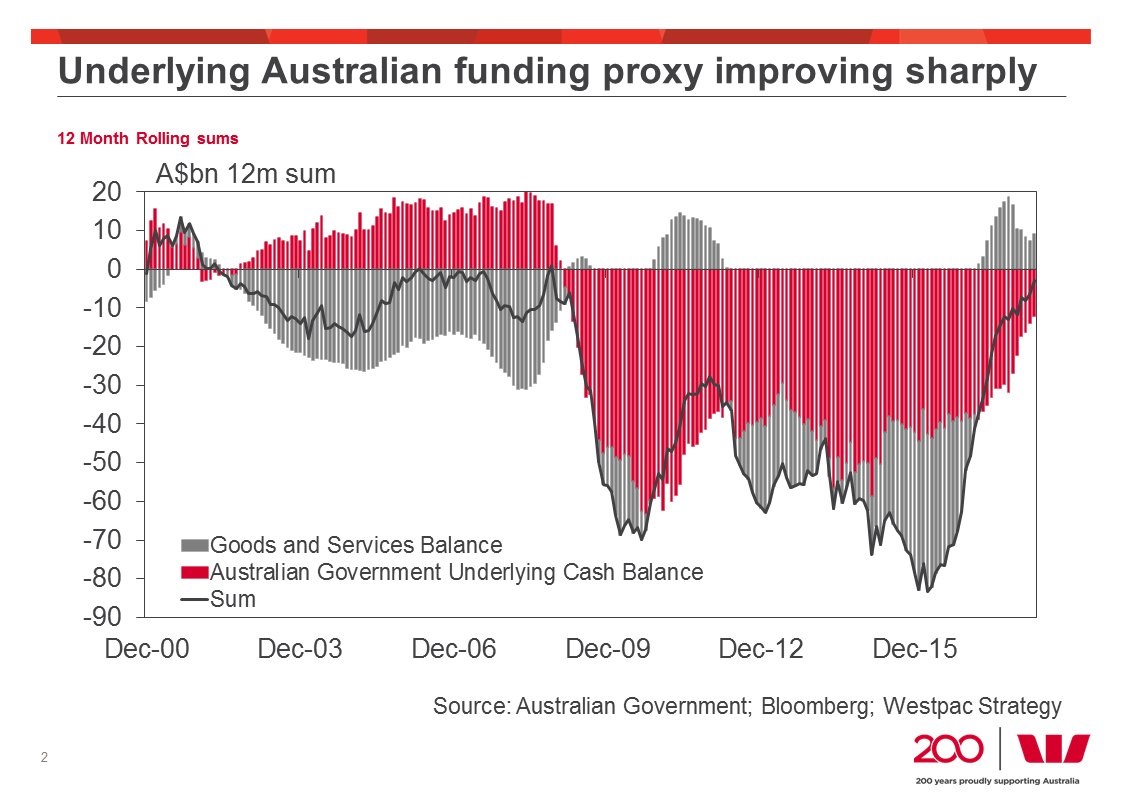

Australian Goods and Services and underlying Government cash balance

Overseas borrowing in Foreign Currency by Australian Financial Institutions

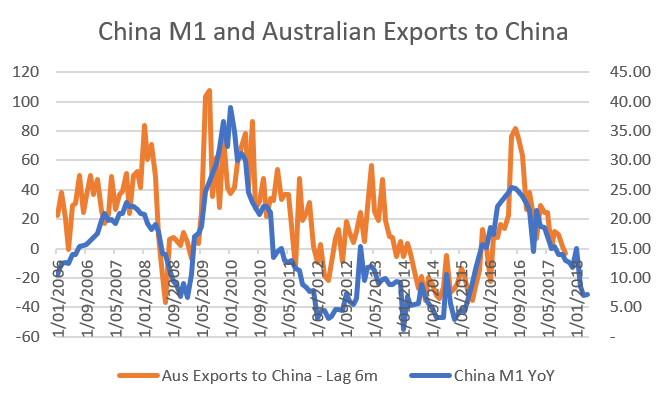

China M1 and Australian Exports to China

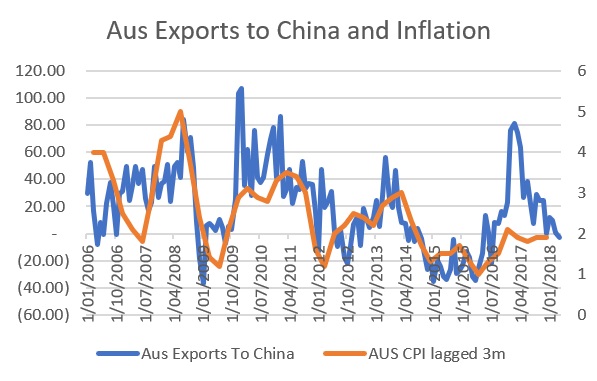

Australian exports to China and Australian Inflation

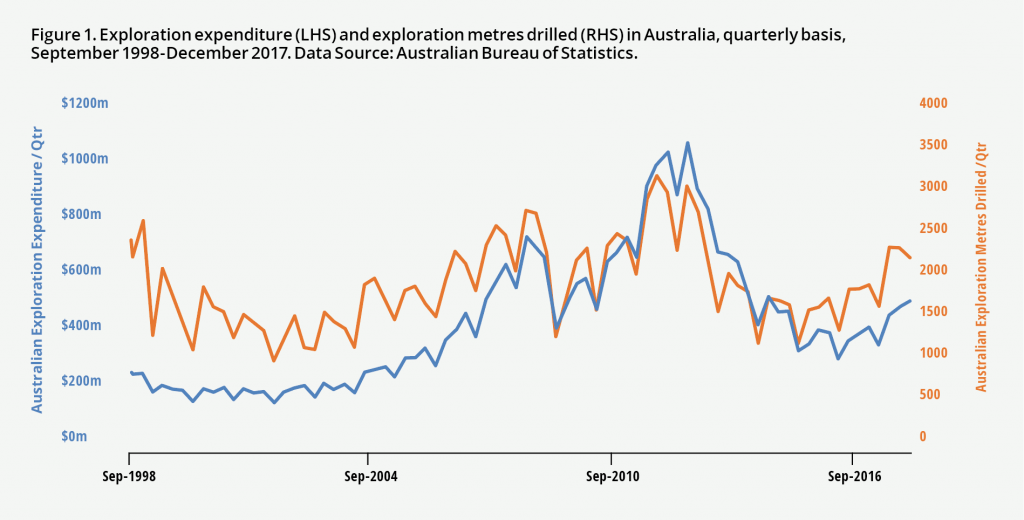

Australia – Exploration Expenditure and metres drilled

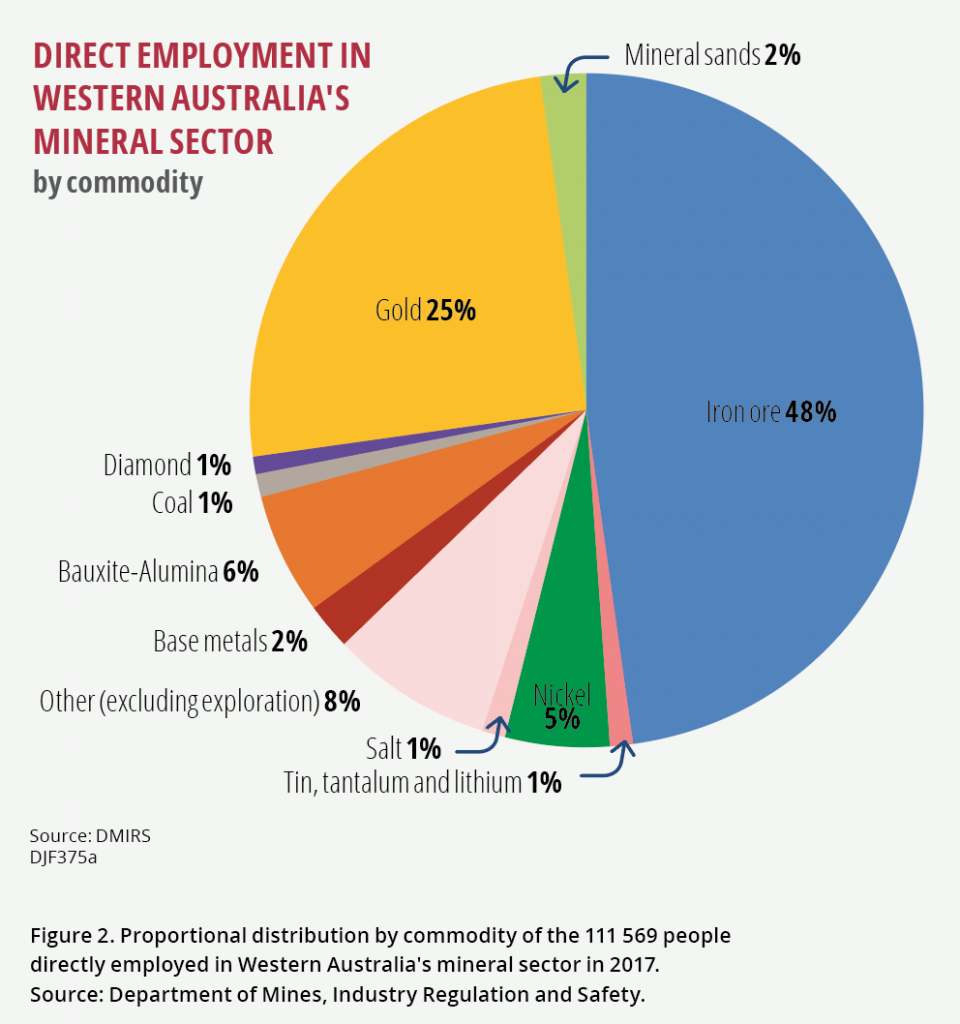

Direct West Australian mining employment

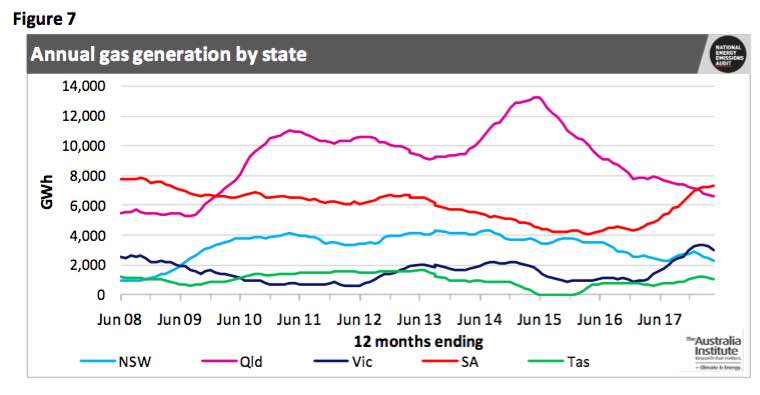

Australian gas generation by State

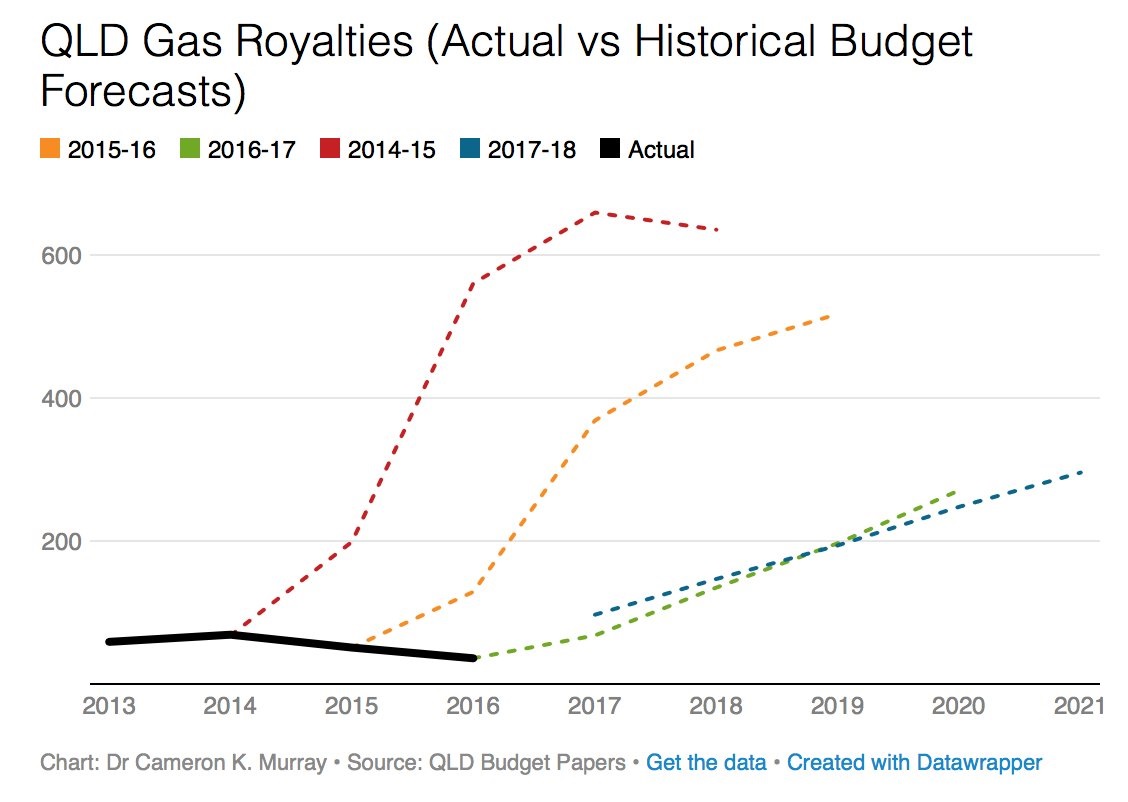

Queensland Gas Royalties

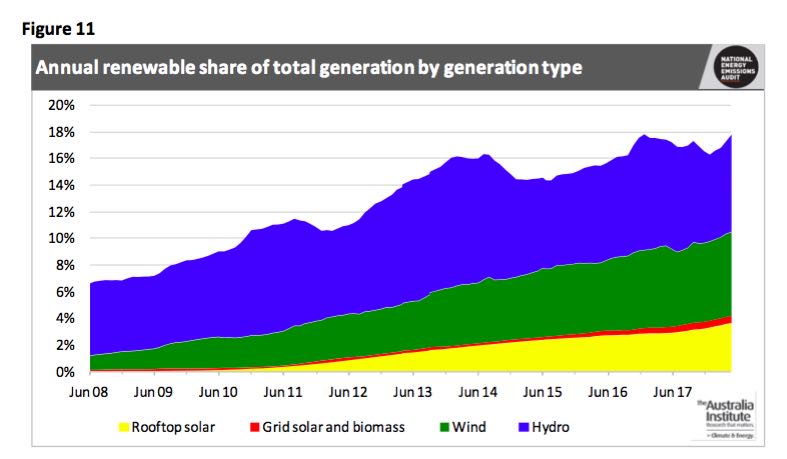

Australia – Renewable Energy

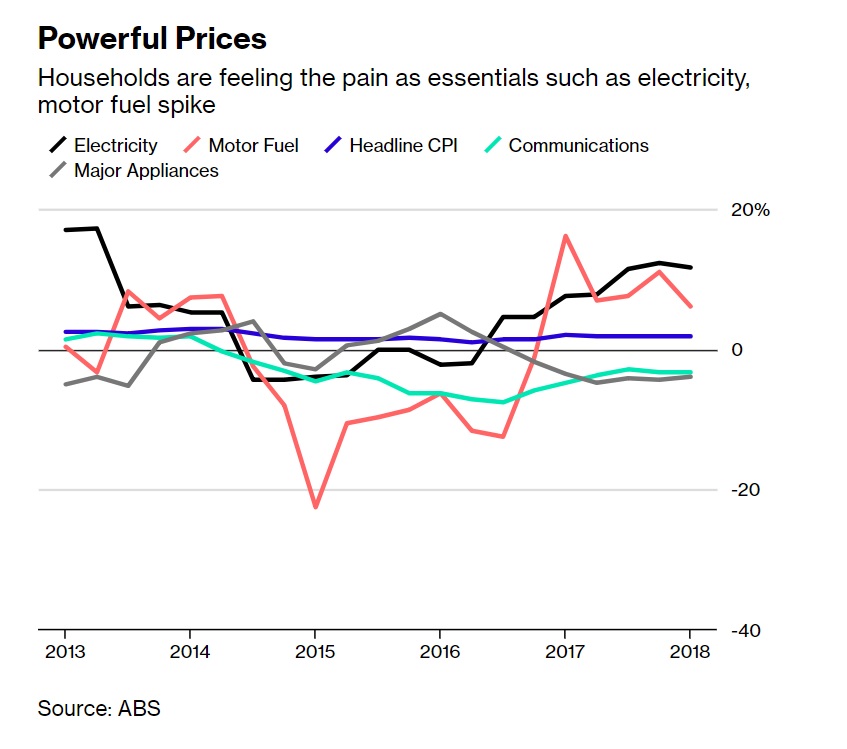

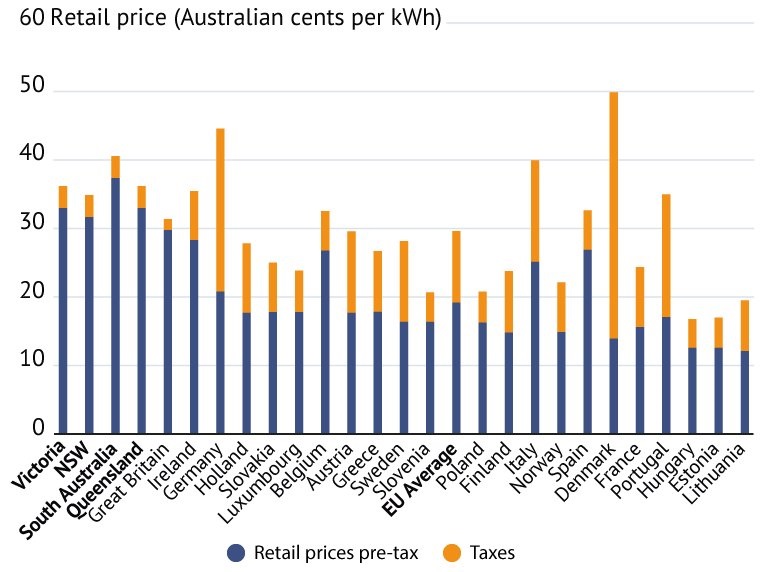

Australian electricity pricing in relation to European pricing

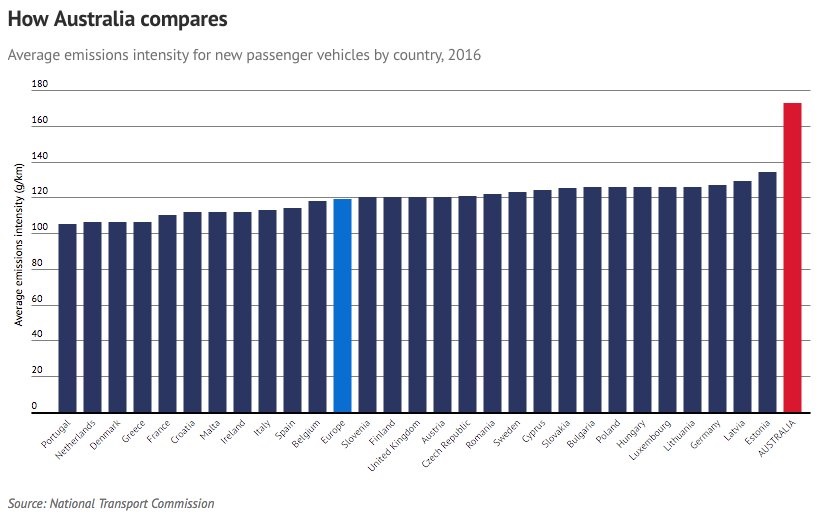

Australian emissions intensity for new vehicles in relation to Europe

United States & Americas

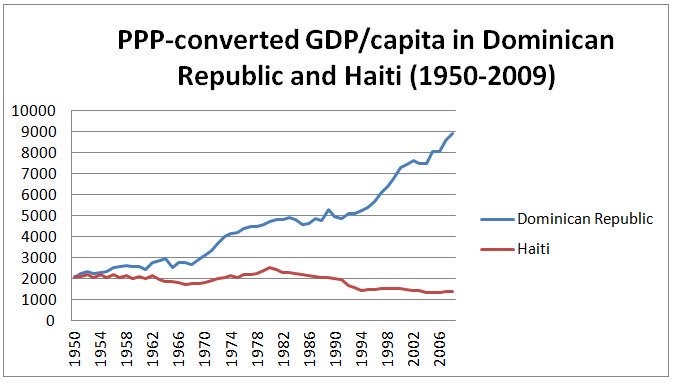

GDP Per Capita, PPP – Dominican Republic & Haiti (they share the same island)

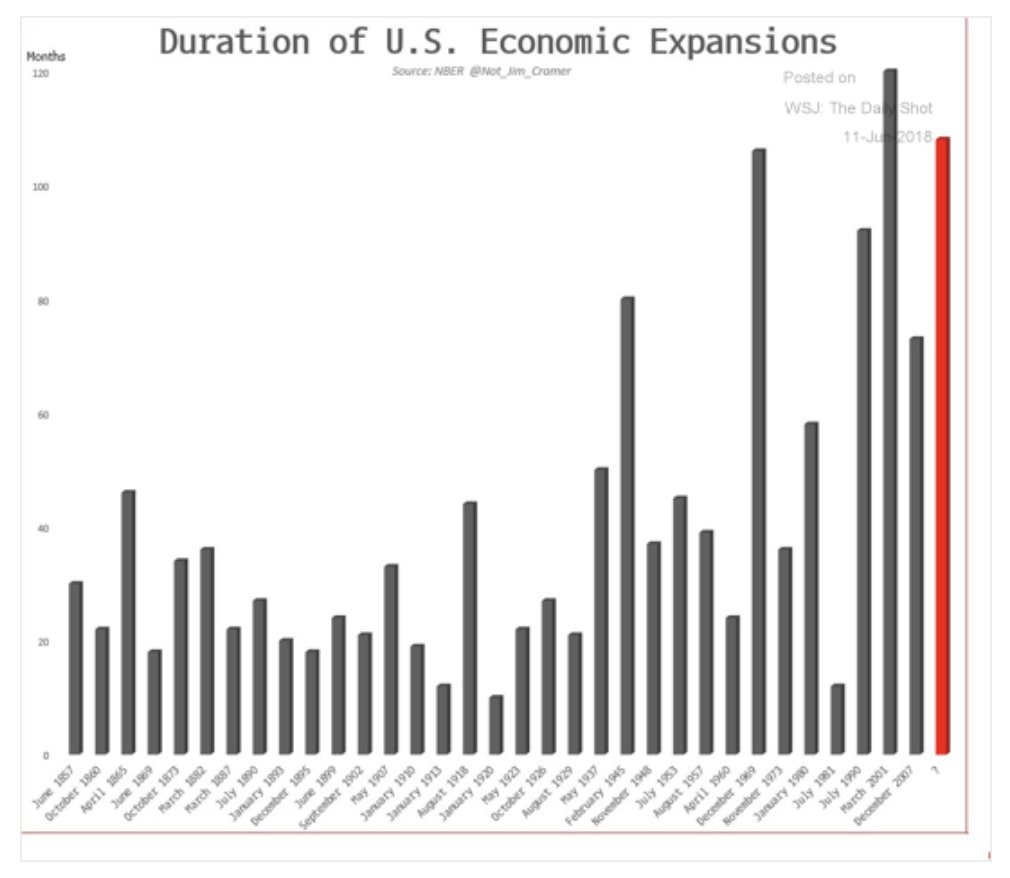

US Economic Expansions – Historical durations

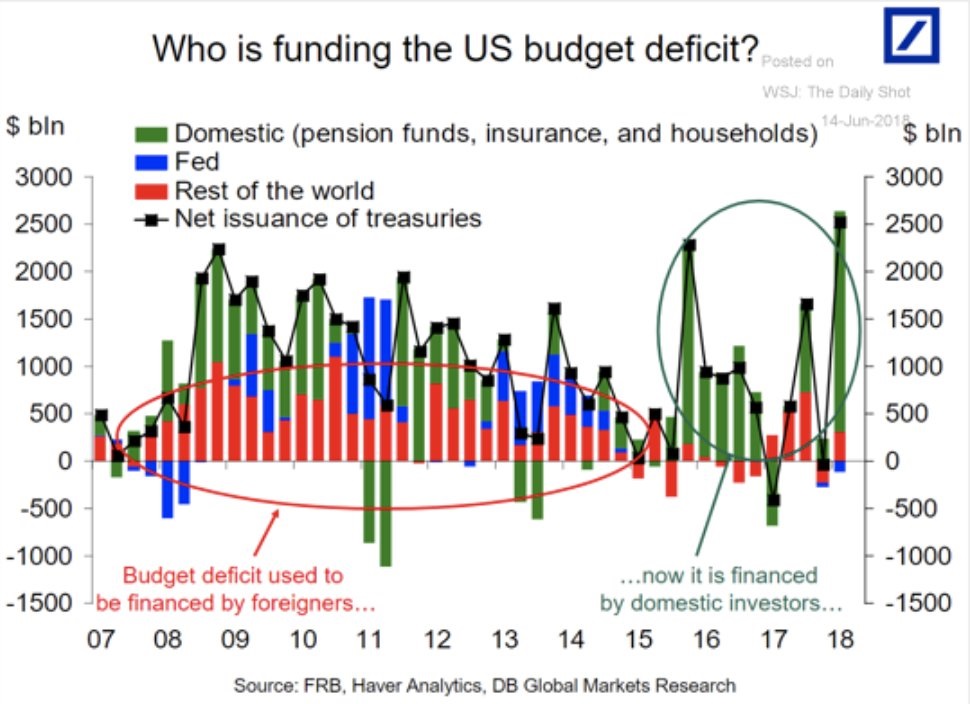

US Budget Deficit – funding sources

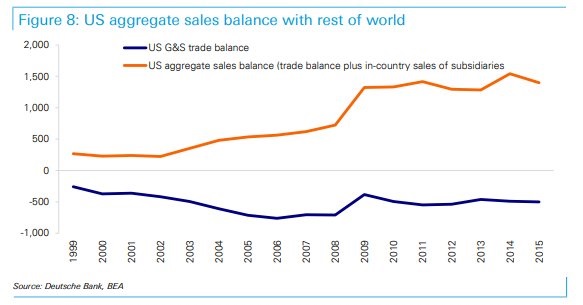

United States – aggregate sales balance with the rest of the world

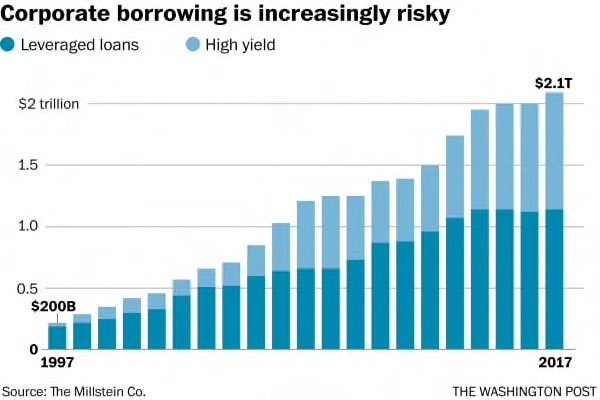

US Corporate Borrowing

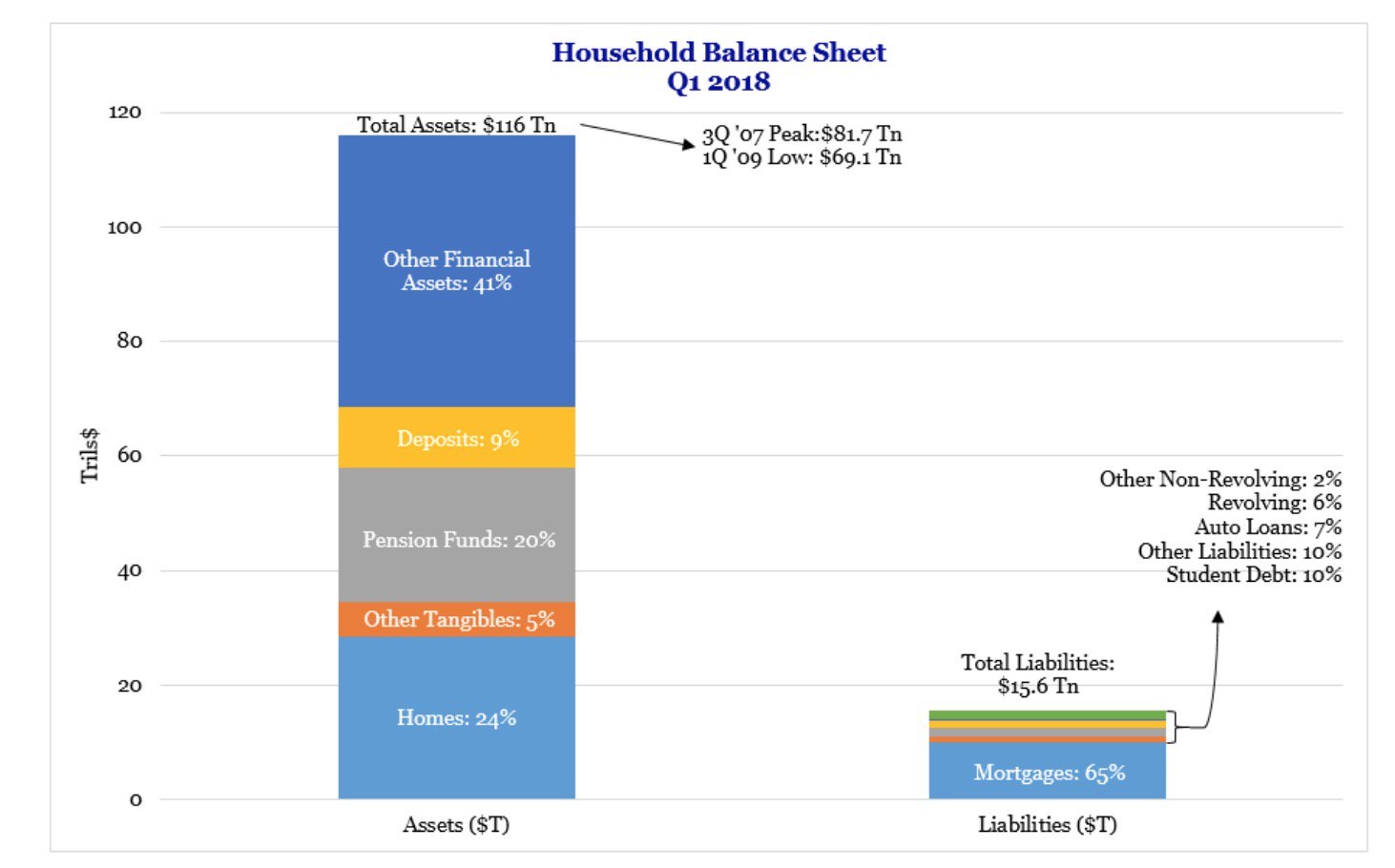

US Household Balance

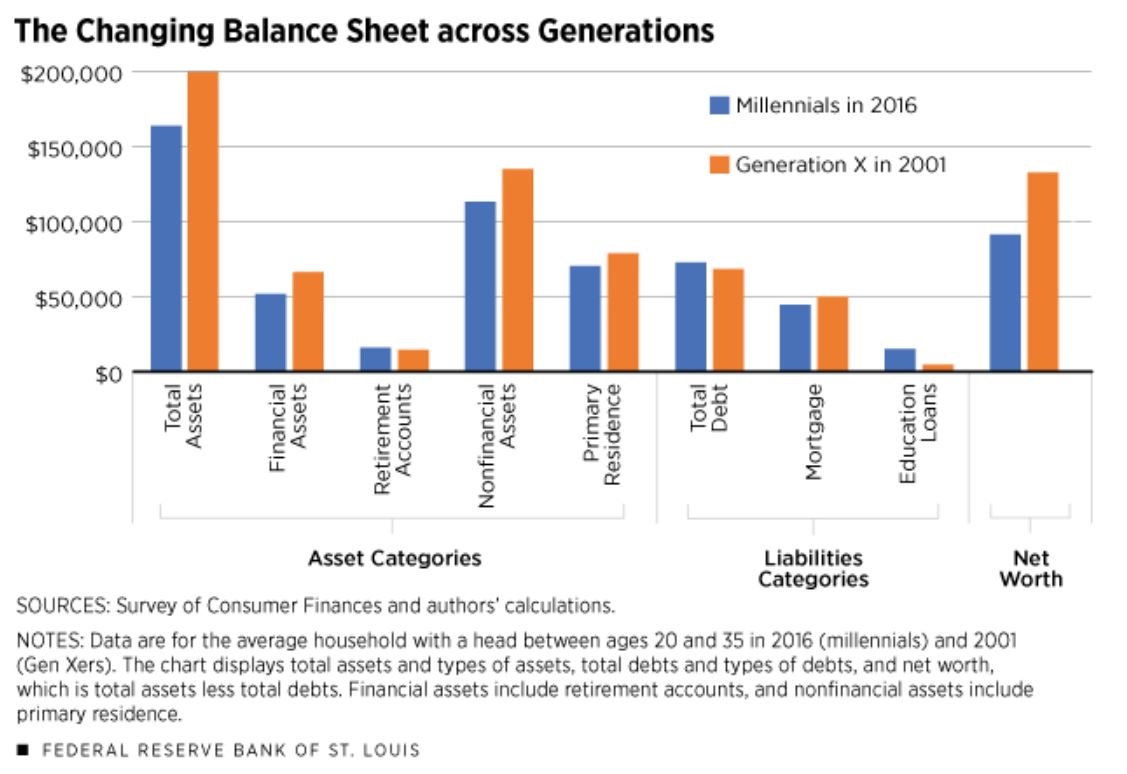

United States – Assets of Generations X & Y

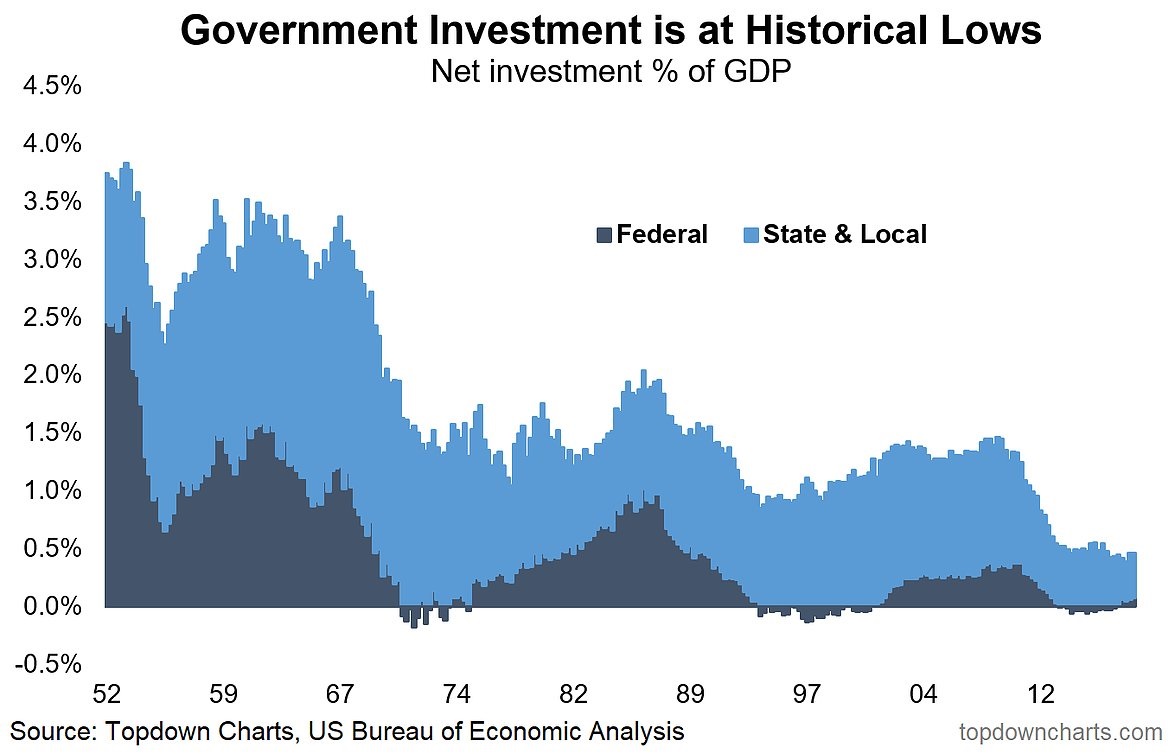

United States – Government Investment

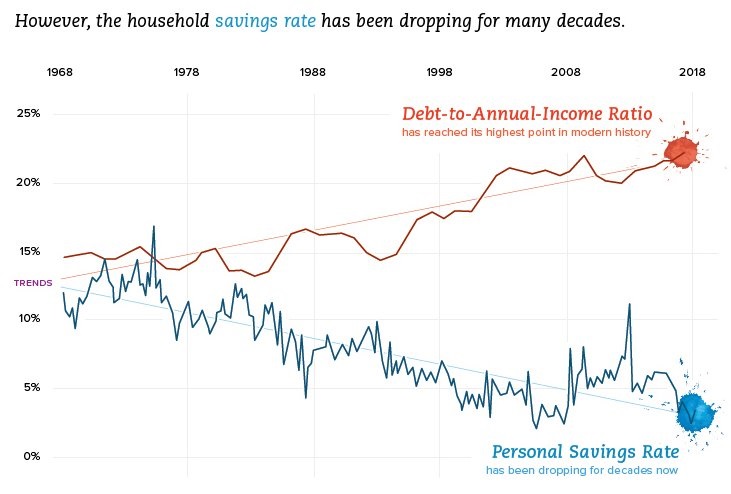

United States – debt to income & savings

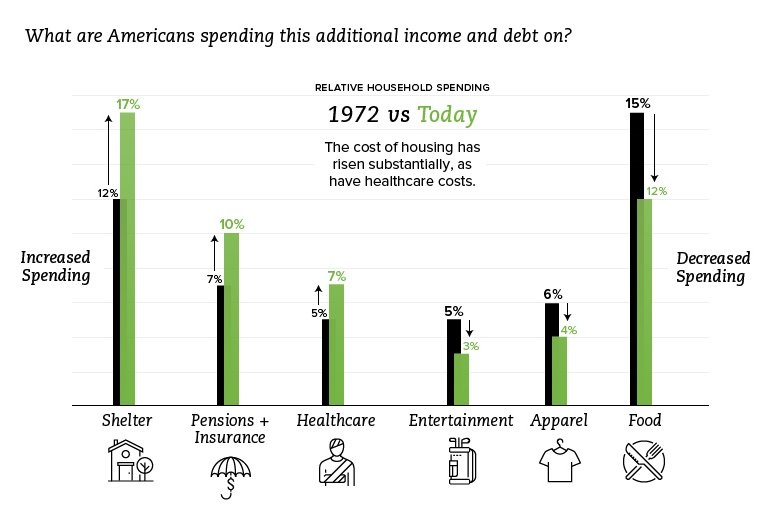

United States – Spending selected categories, 1972 and now

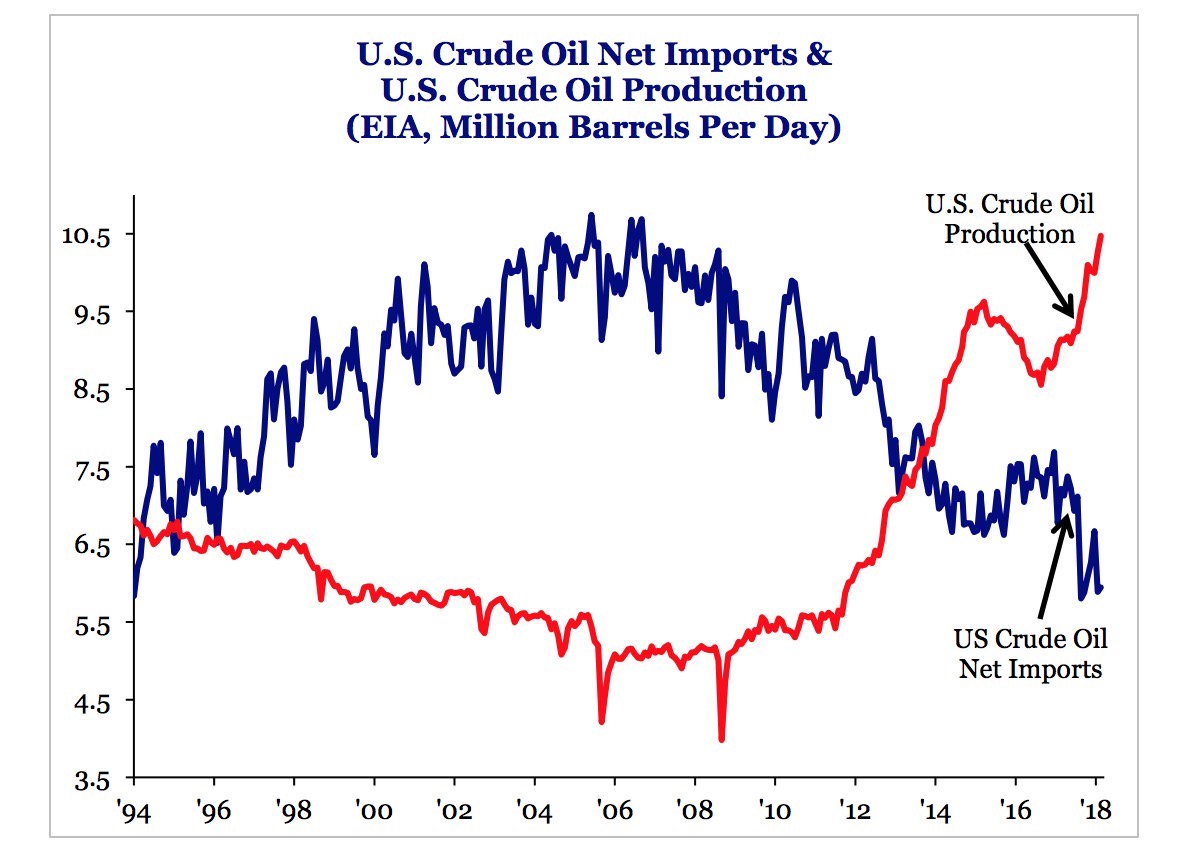

US Crude Oil Net Imports & US Production

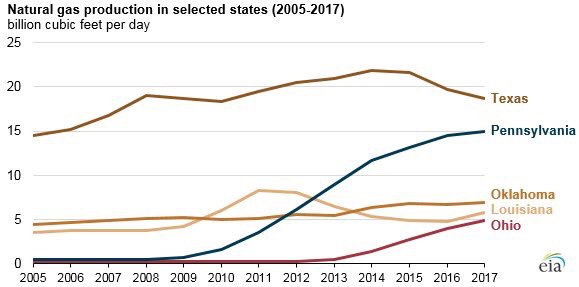

United States – Gas production, selected States

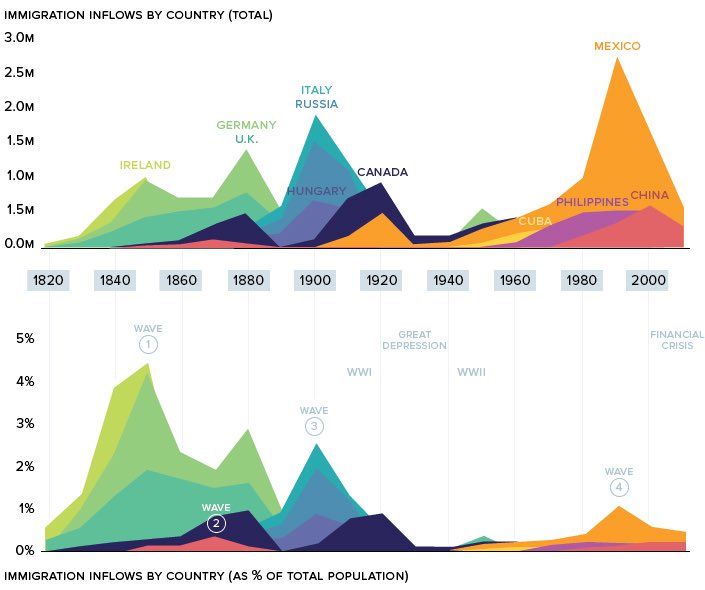

United States Immigration sources over time

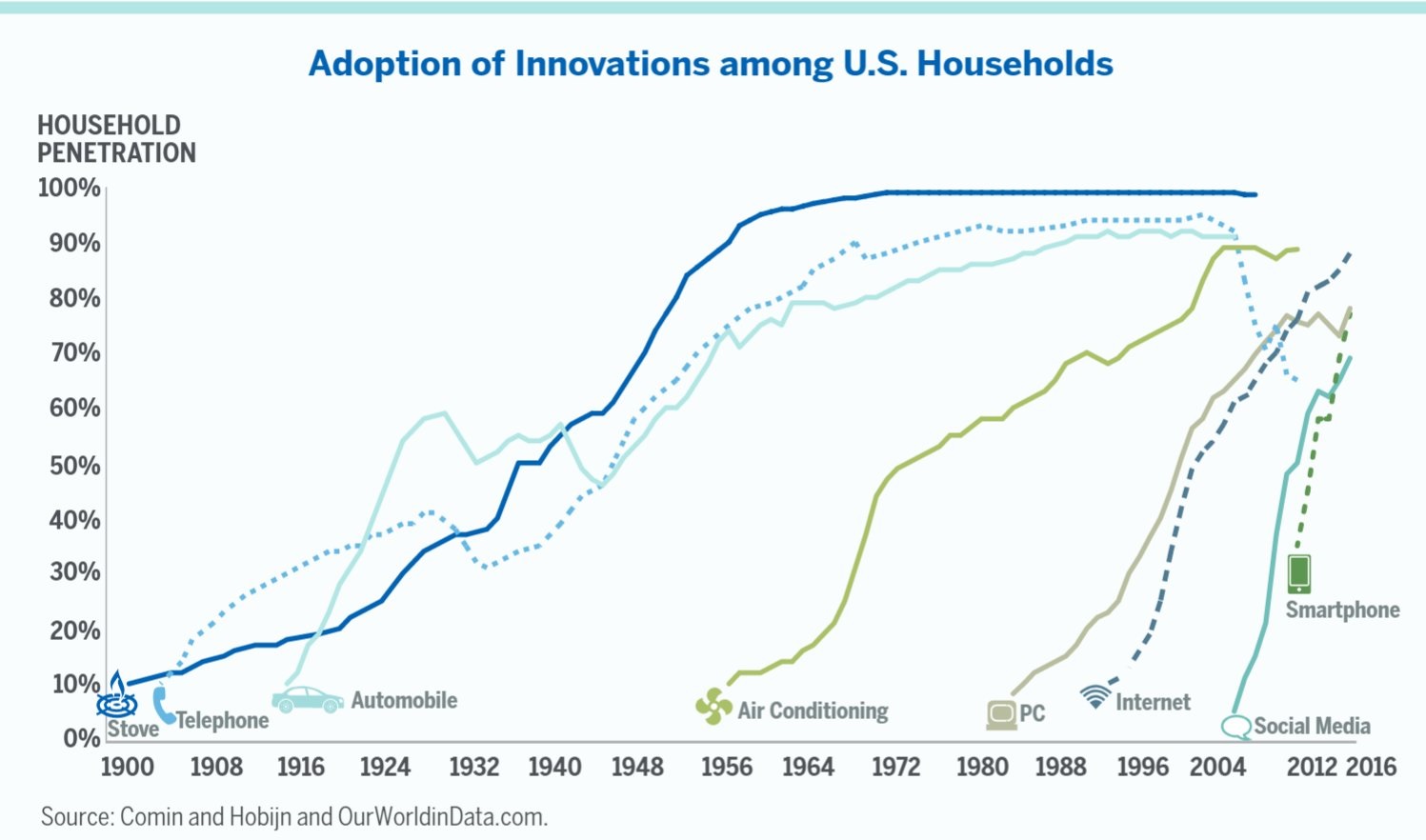

Innovation Adoption by US Households

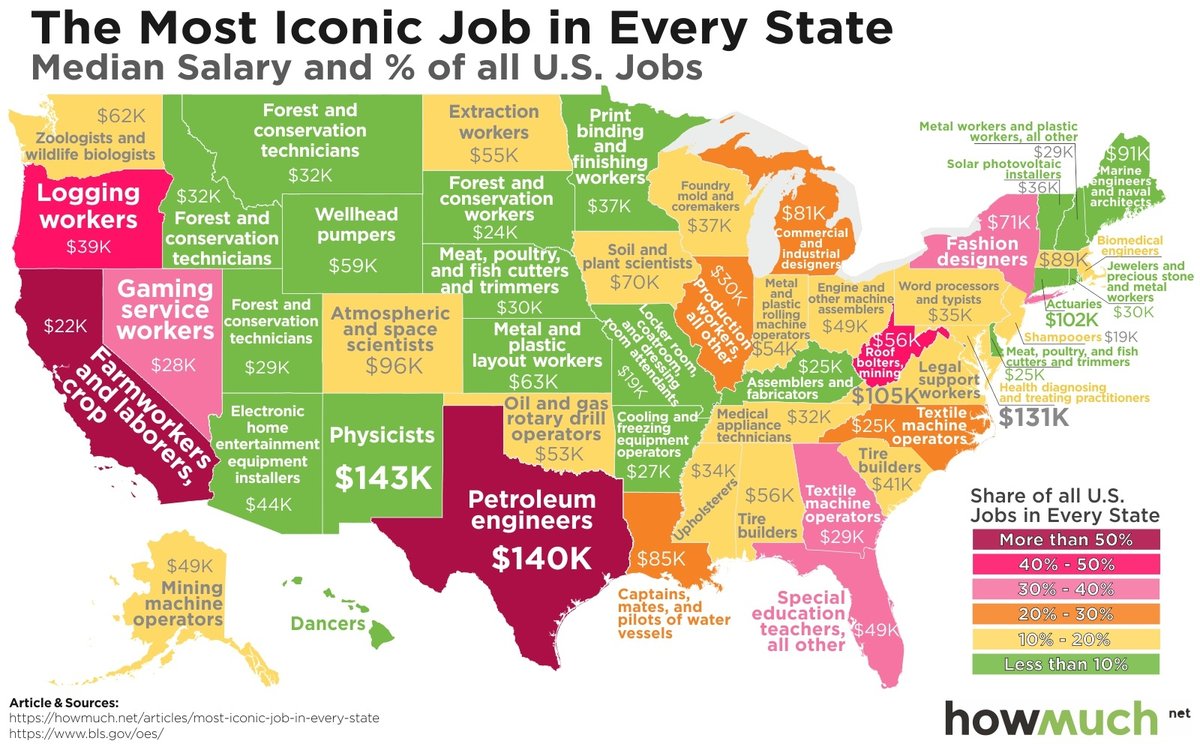

United States – Iconic Jobs & salaries by State

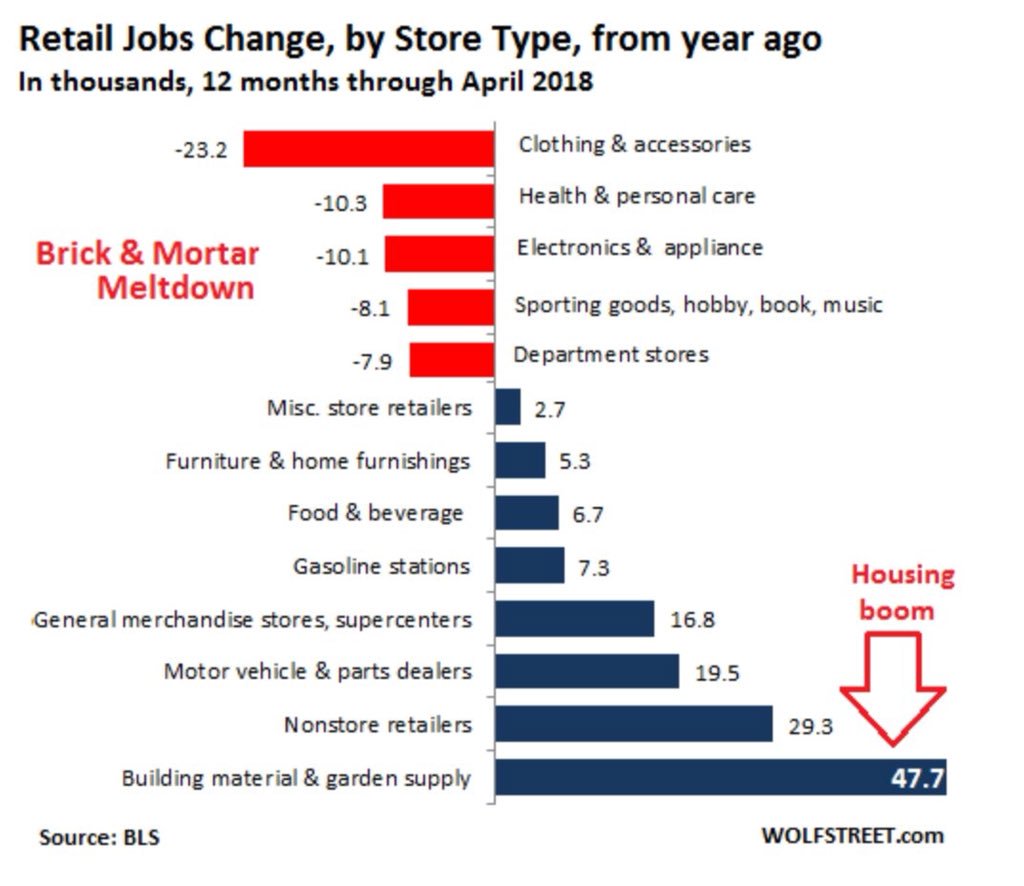

United States – Retail jobs

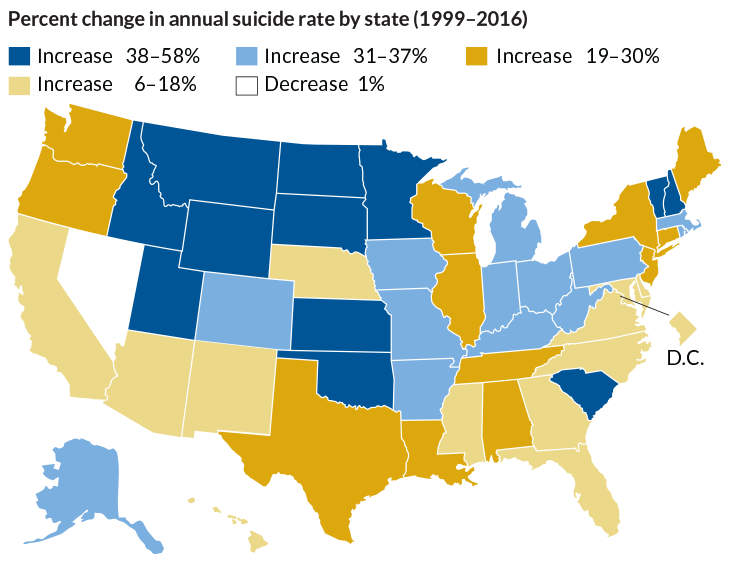

United States – Suicide rate changes 1999-2016

China & Asia

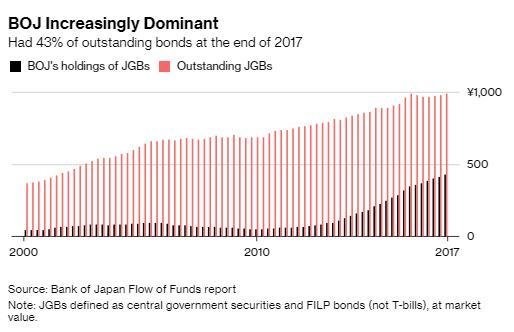

Japan – Bank of Japan and Japan Government Bonds

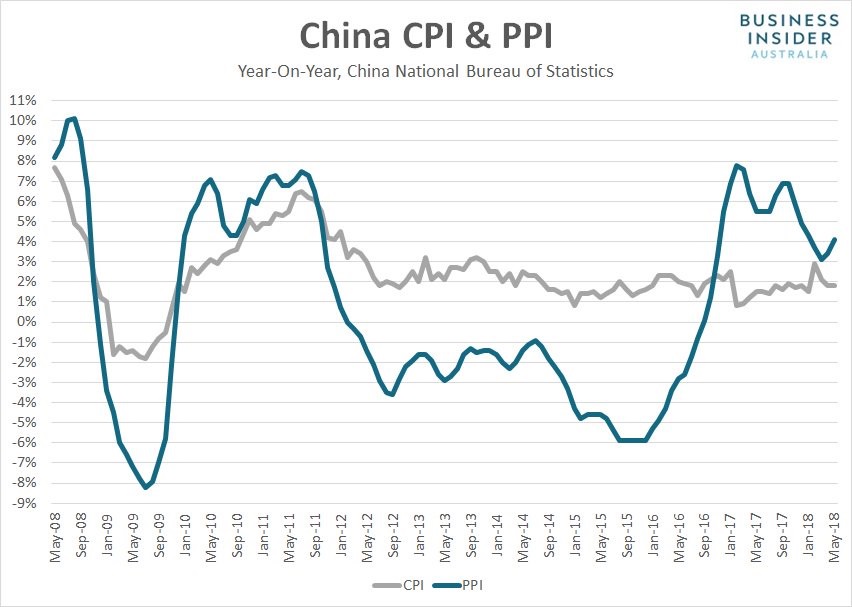

China CPI & PPI

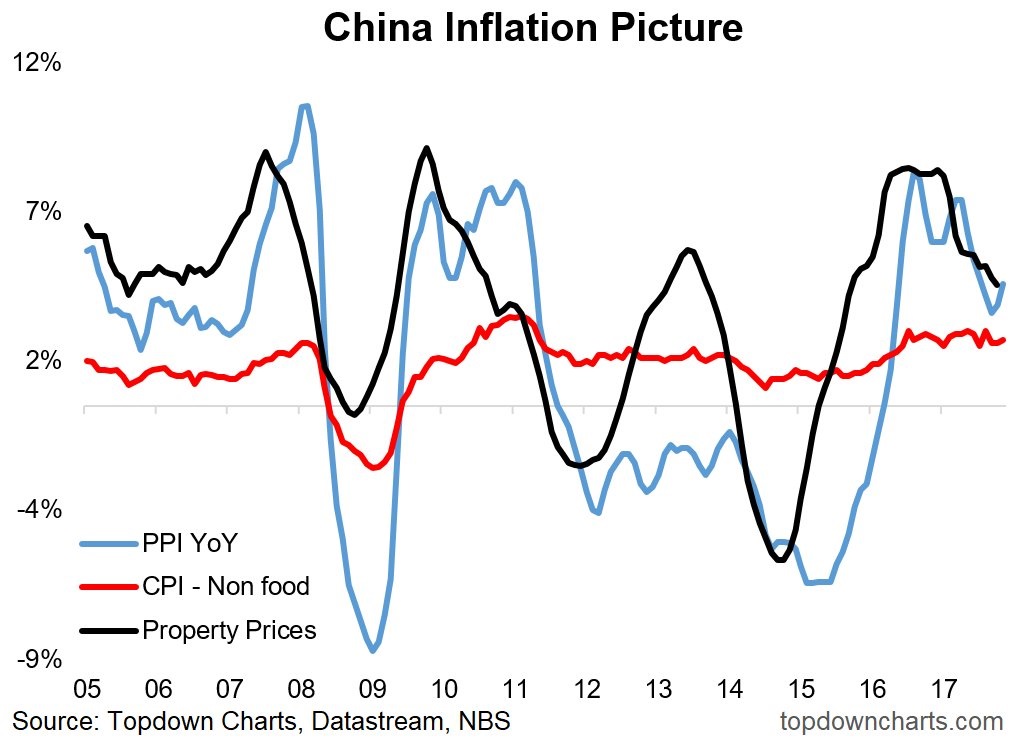

China CPI & PPI & Real Estate

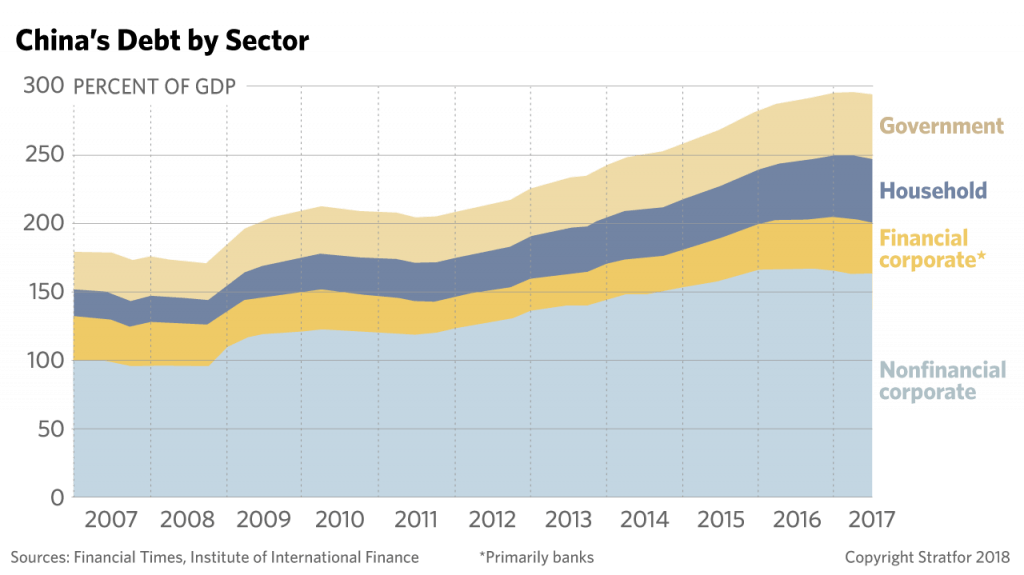

China debt by sector

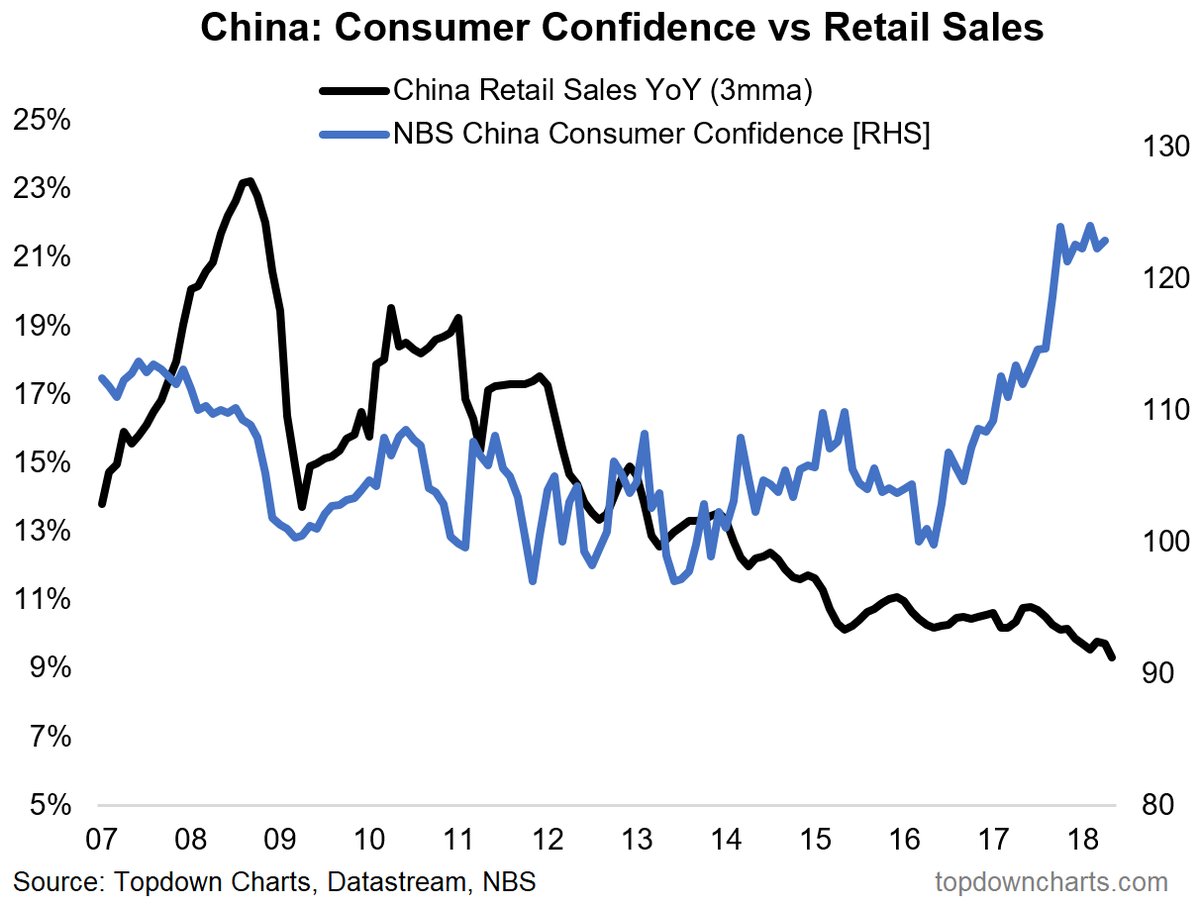

China Consumer Confidence and Retail Sales

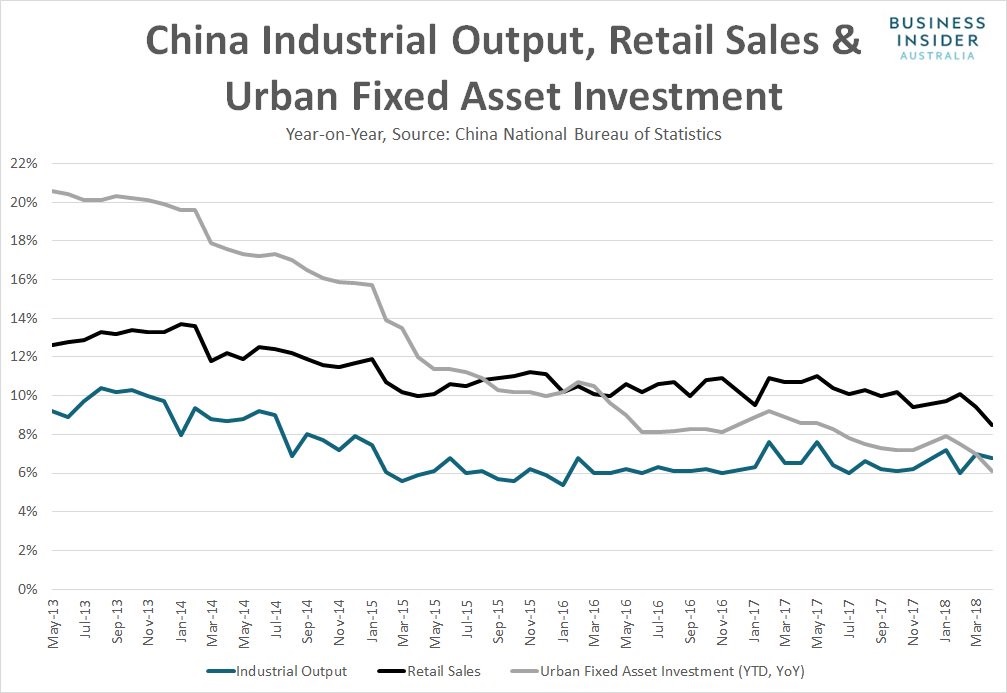

China Industrial Output, Retail Sales & Urban Fixed Asset investment

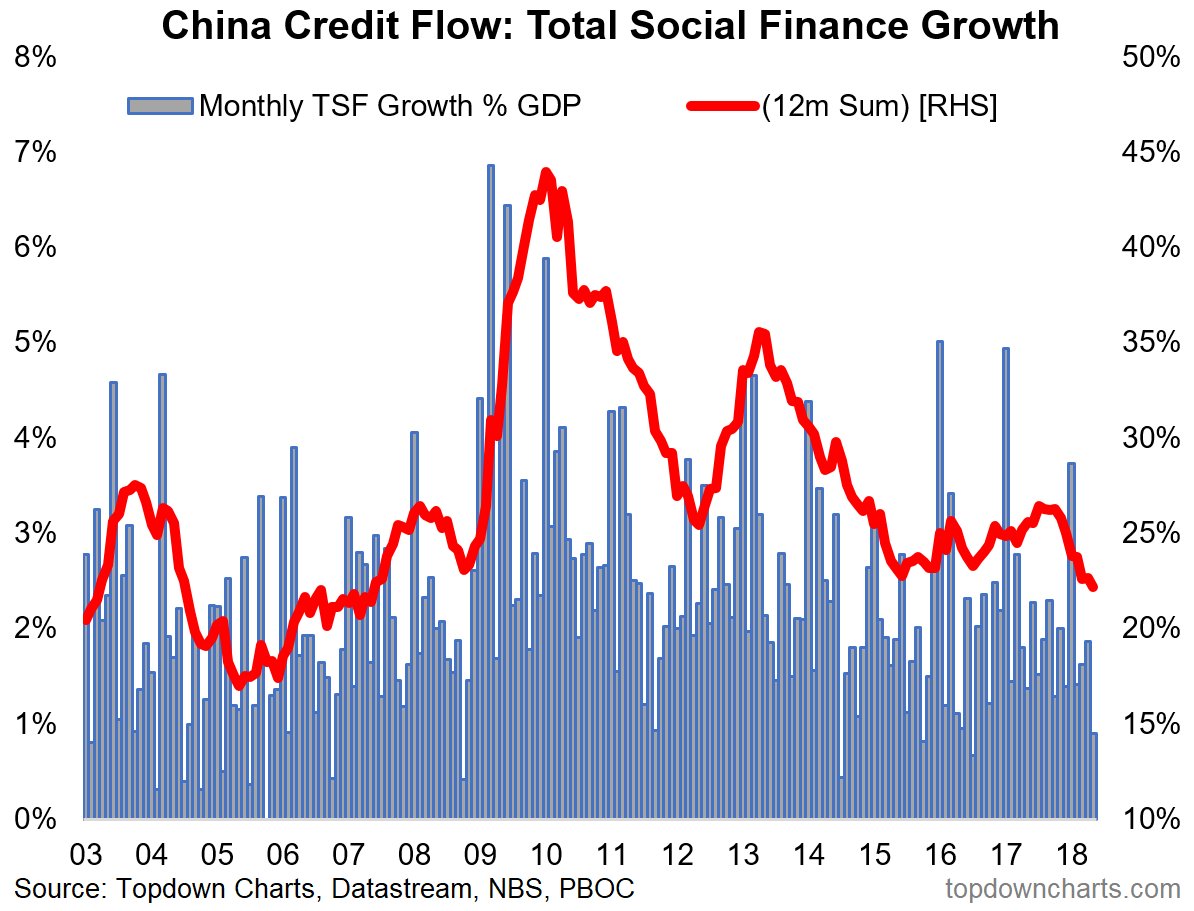

China Credit

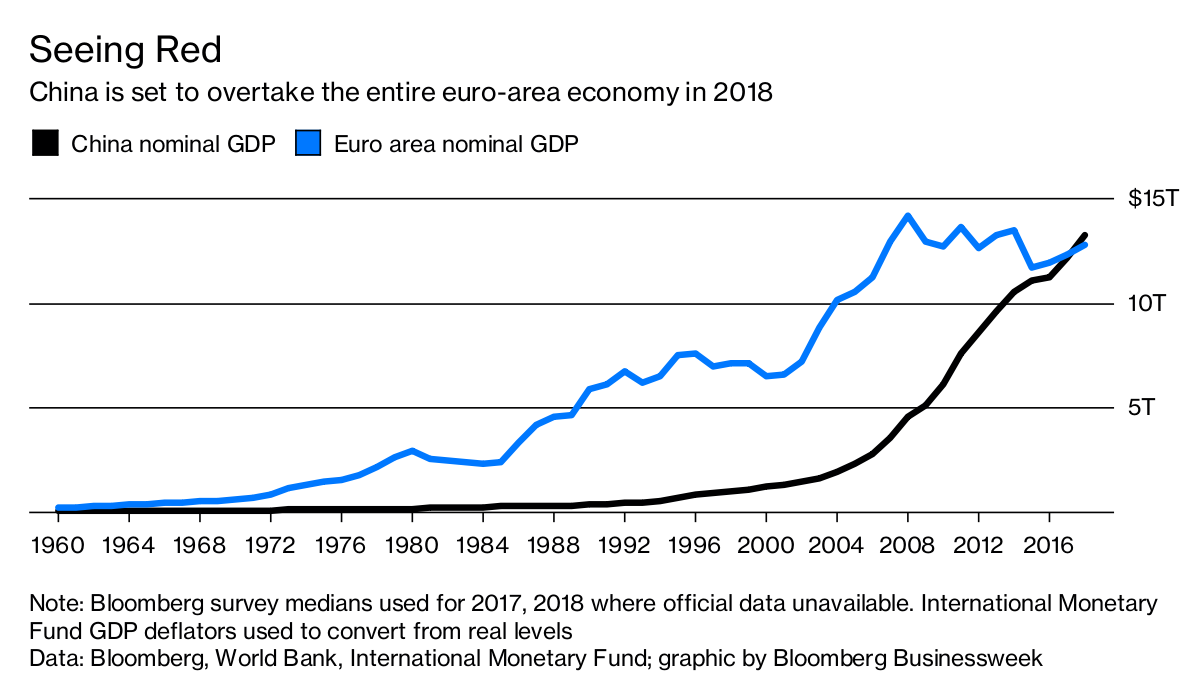

China & Eurozone – Nominal GDP

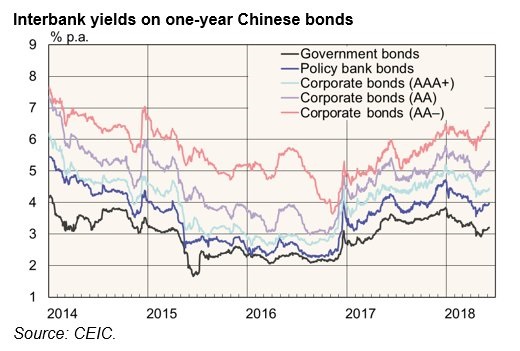

China Bonds – Interbank Yields

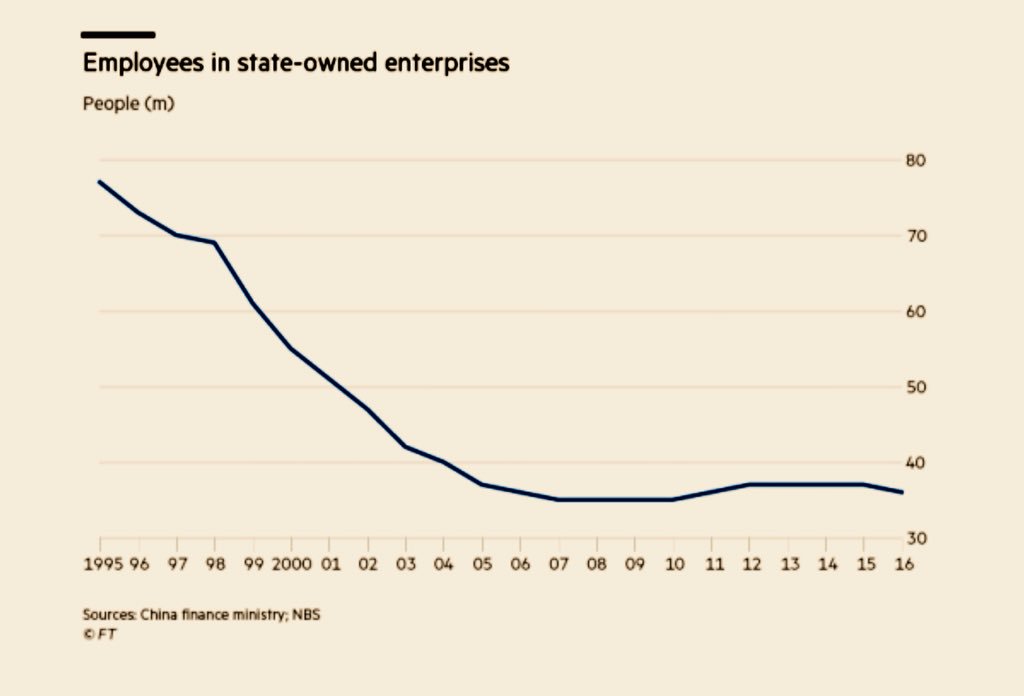

China SOE Employees

Europe

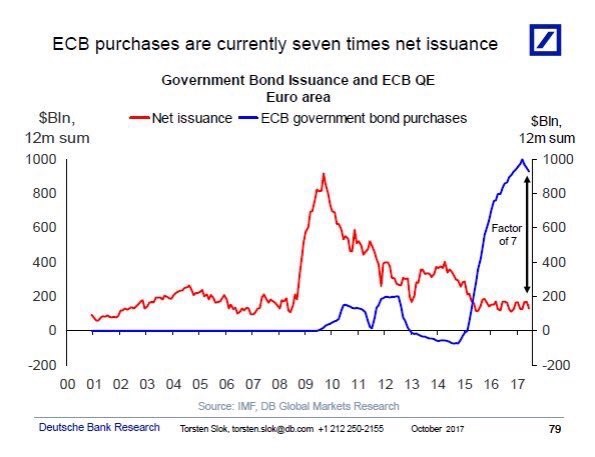

ECB Bond Purchases & National Issuance

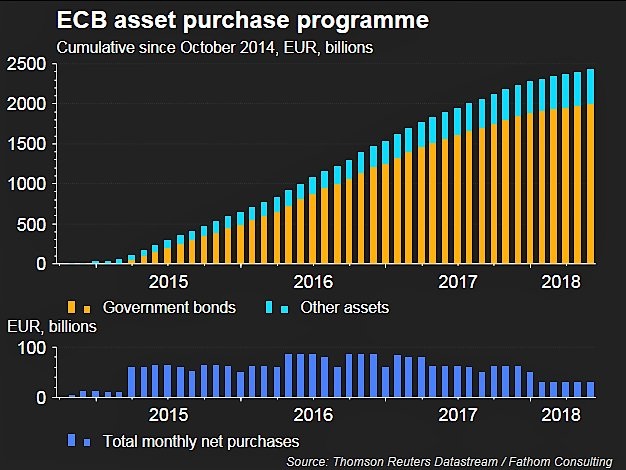

ECB Asset Purchases

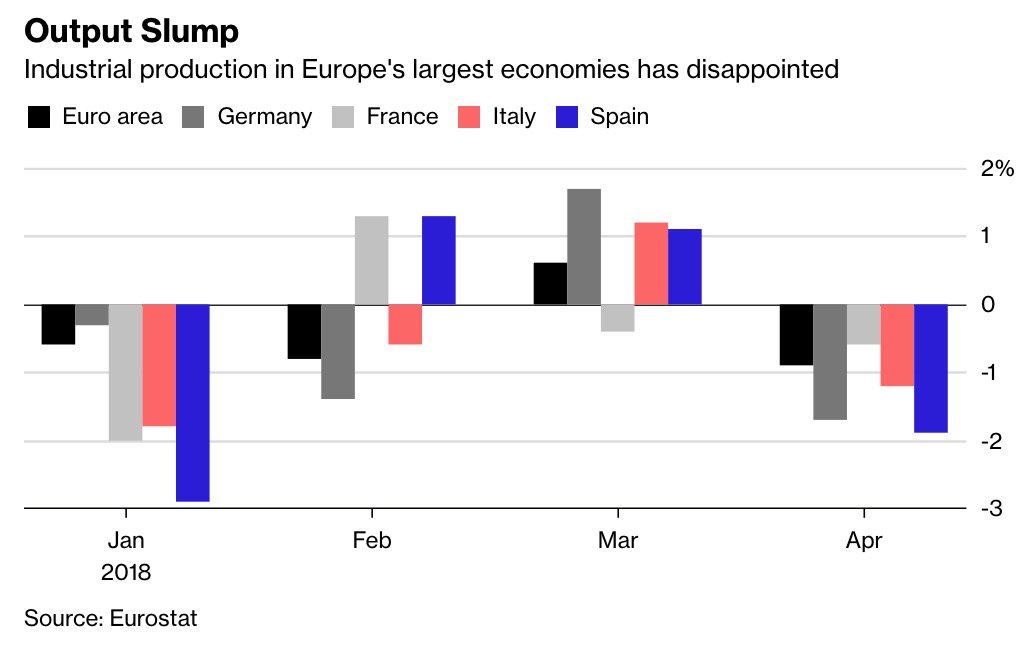

Eurozone Industrial production – Selected nations

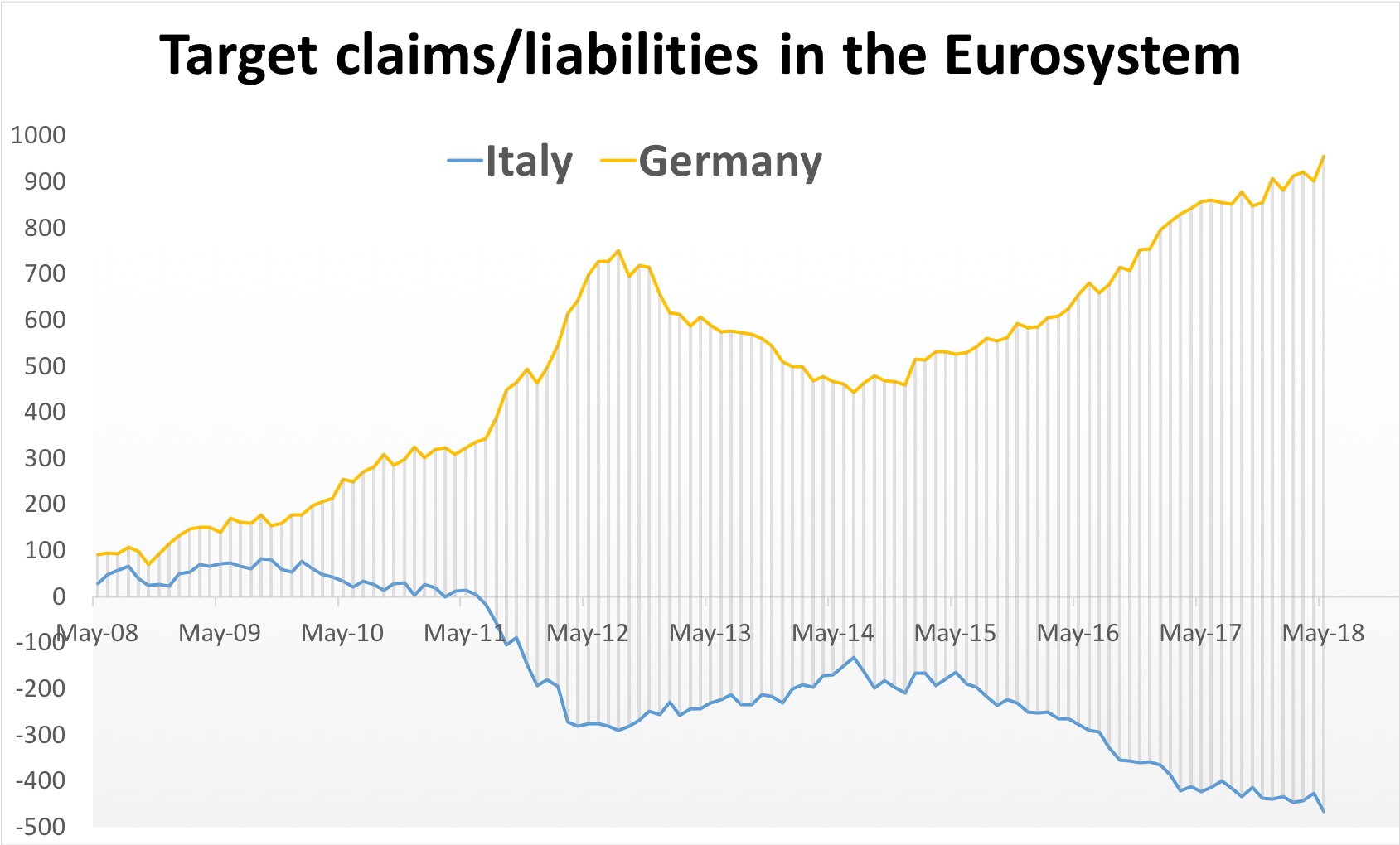

Germany & Italy – Target Claims/Liabilities

Eurozone Unemployment

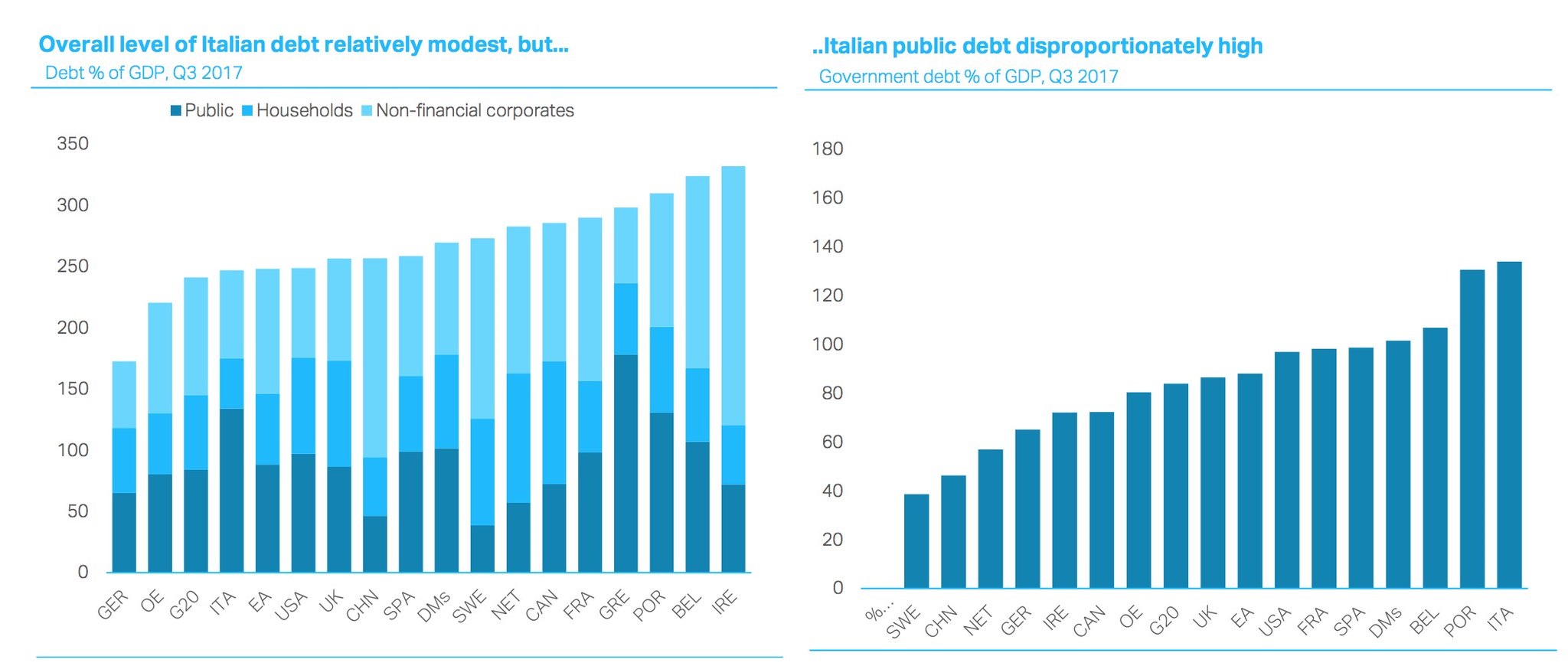

Italy and Eurozone – Total and Public debt

Eurozone – Mobile working age

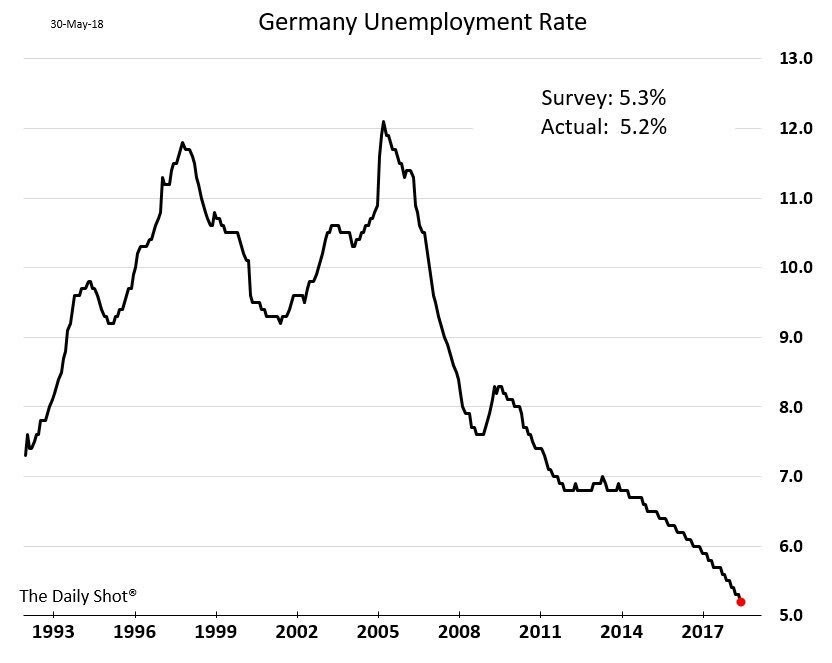

Germany Unemployment

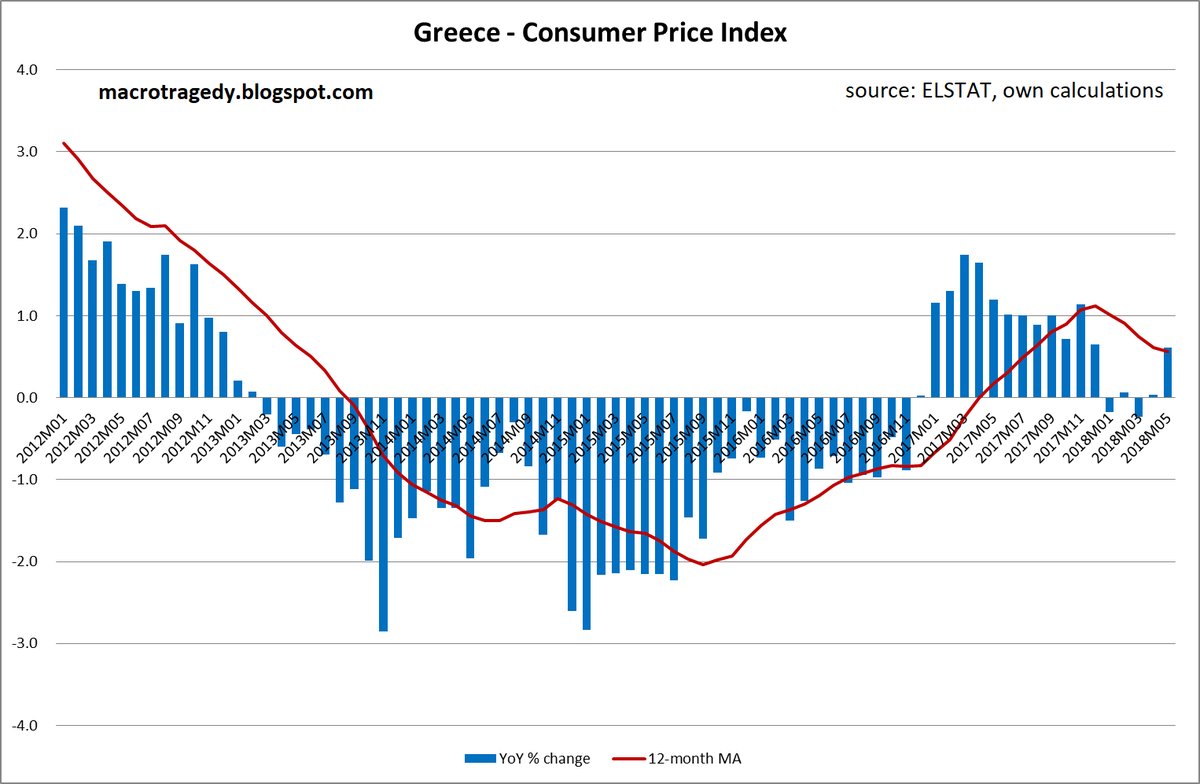

Greece CPI

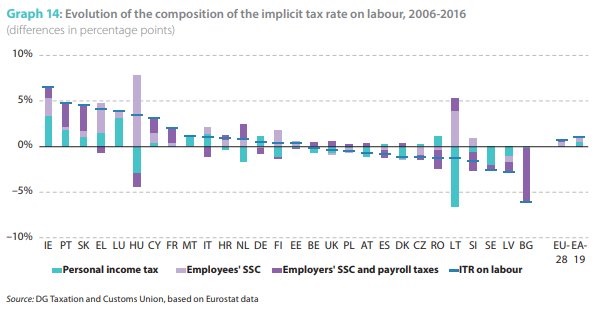

Eurozone – Labour related Taxes

United Kingdom – Manufacturing

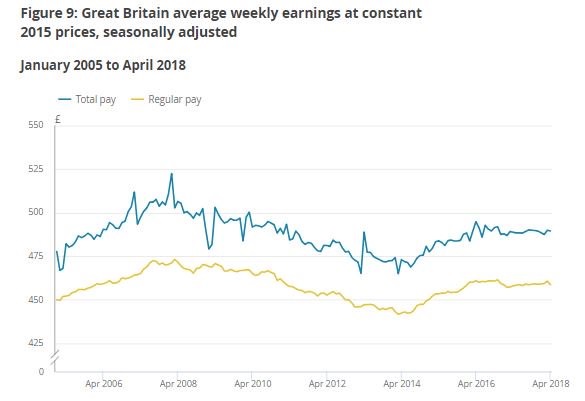

United Kingdom – AWE

Commodities

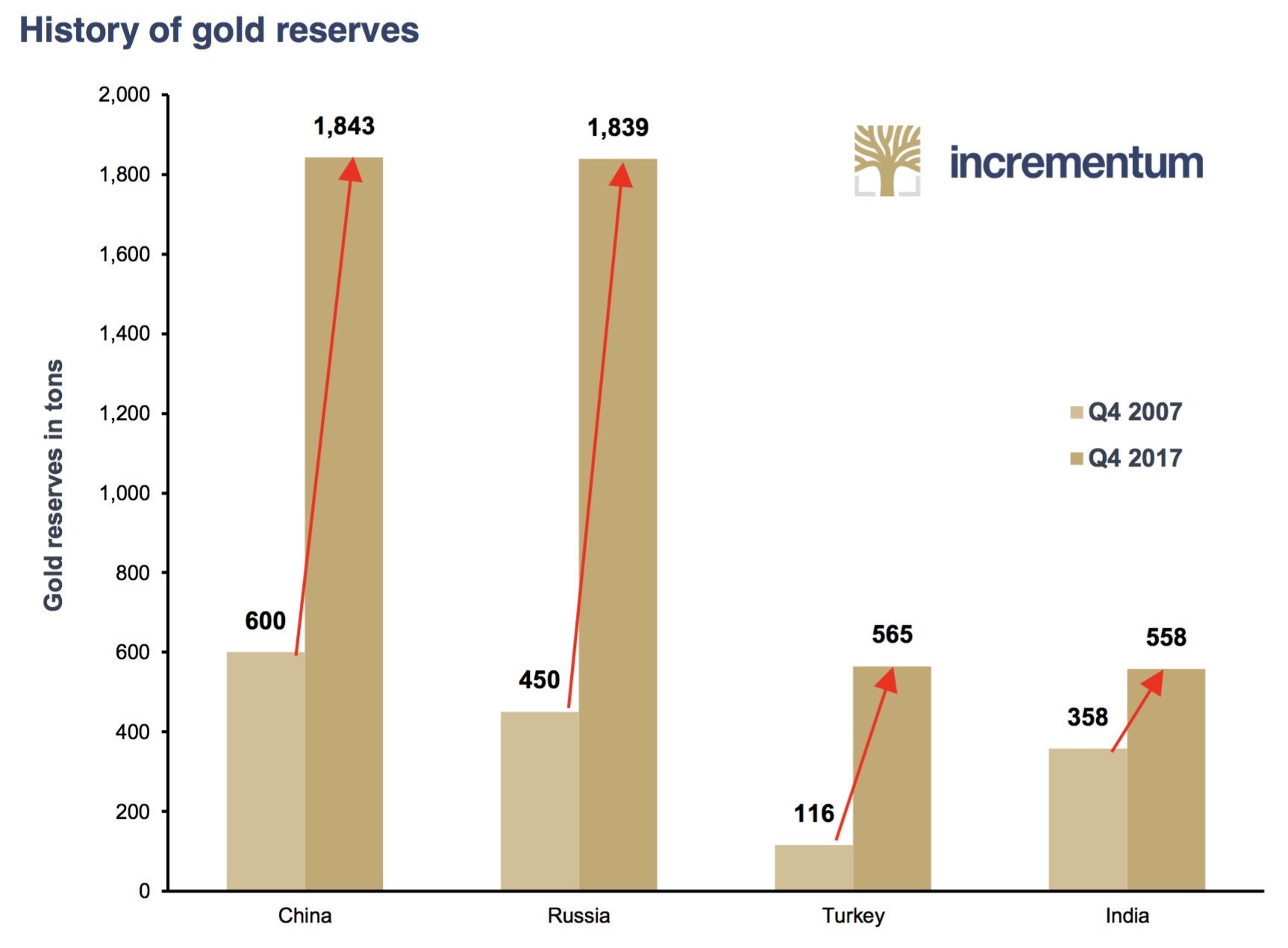

Gold Reserves – Major emerging nations

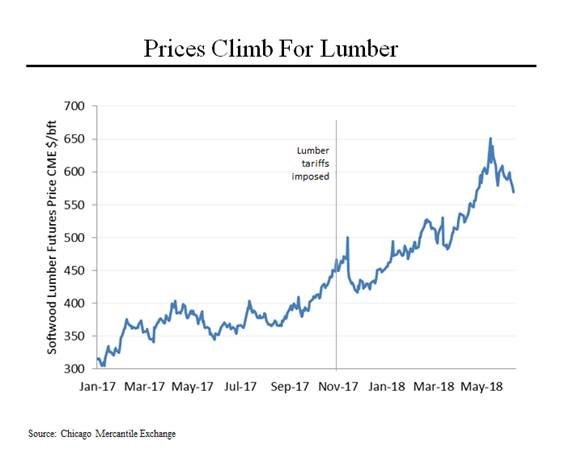

Lumber

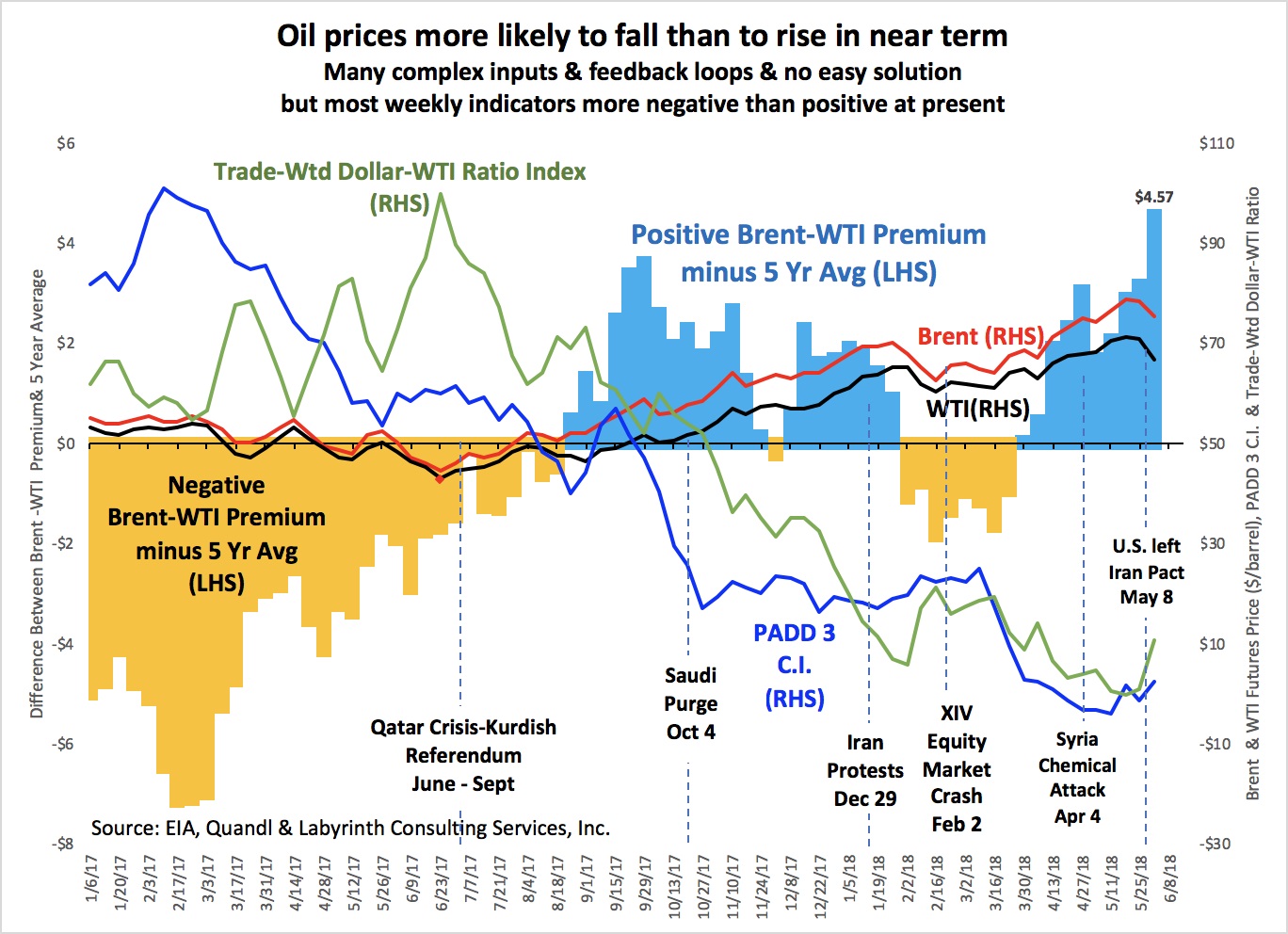

Crude Prices

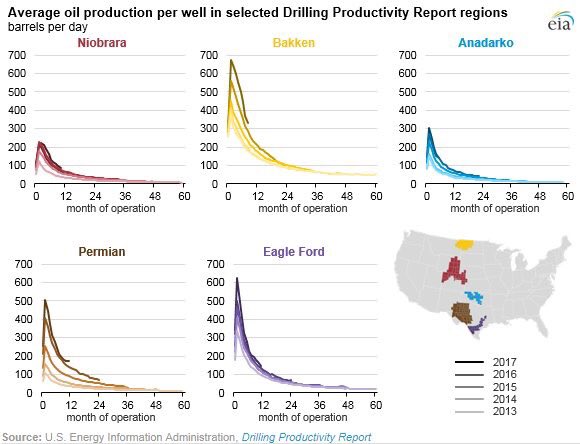

Crude – Selected US Onshore production fields

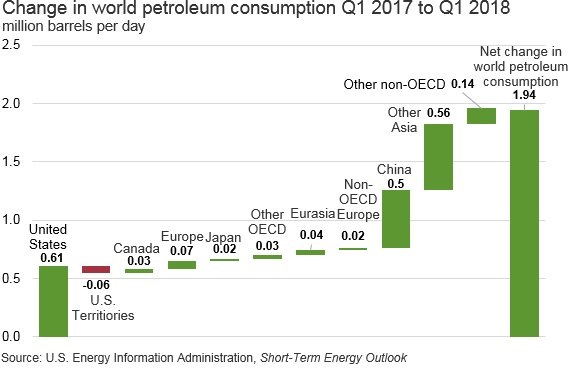

Petroleum consumption

Vanilla

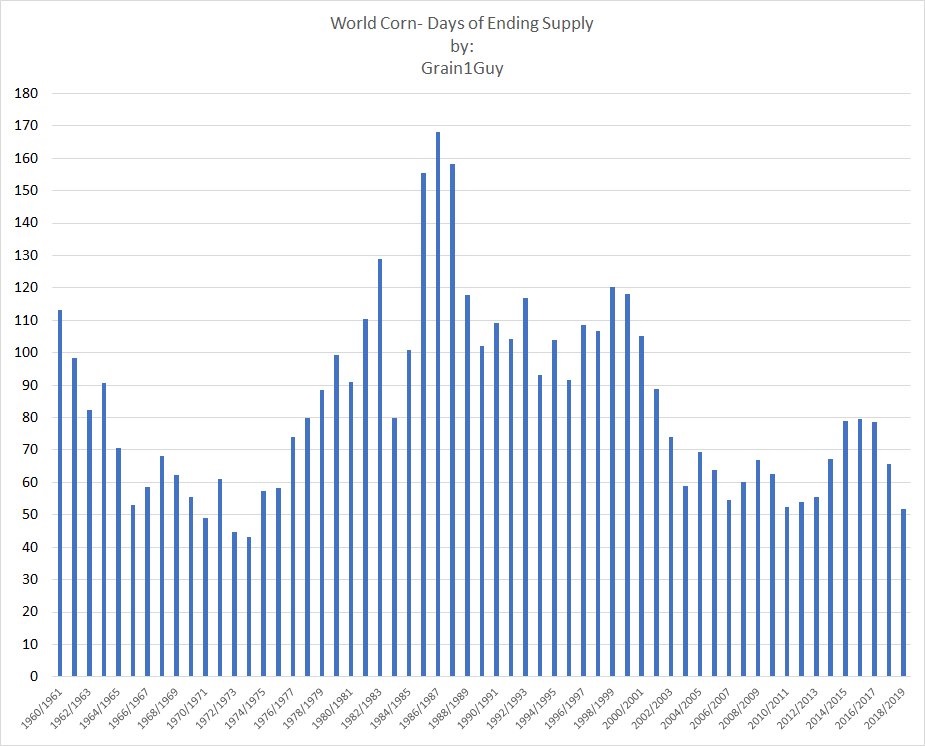

Global Corn – Days supply

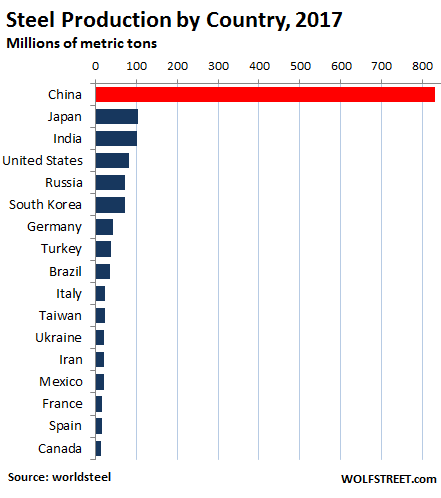

Steel production – Major Nation(s)

Capital Markets

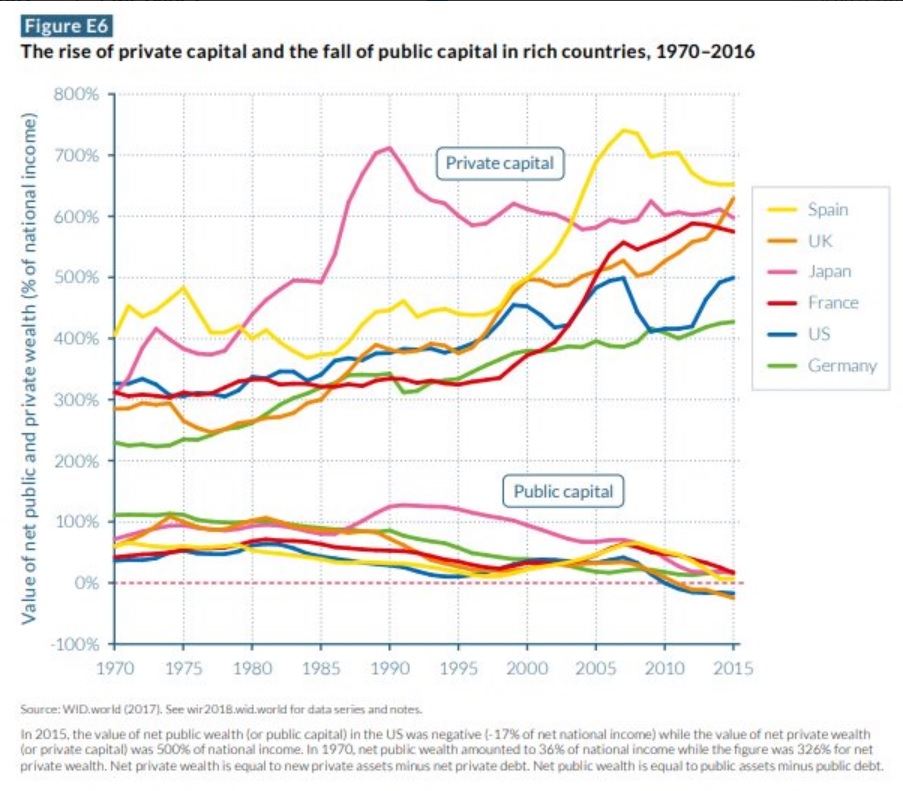

Public & Private Capital – Selected Developed Economies

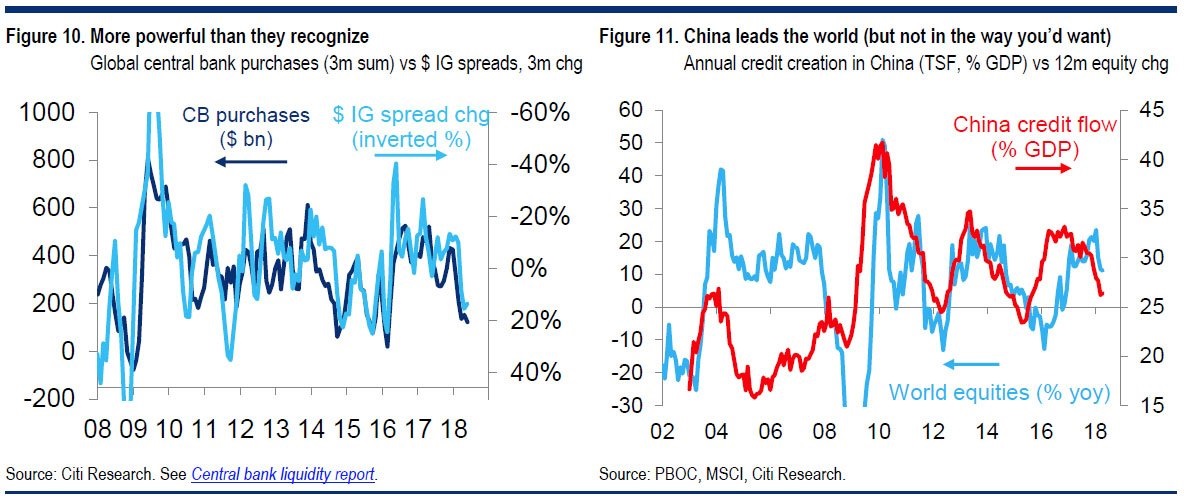

Global Central Banks – Capital Market Impacts

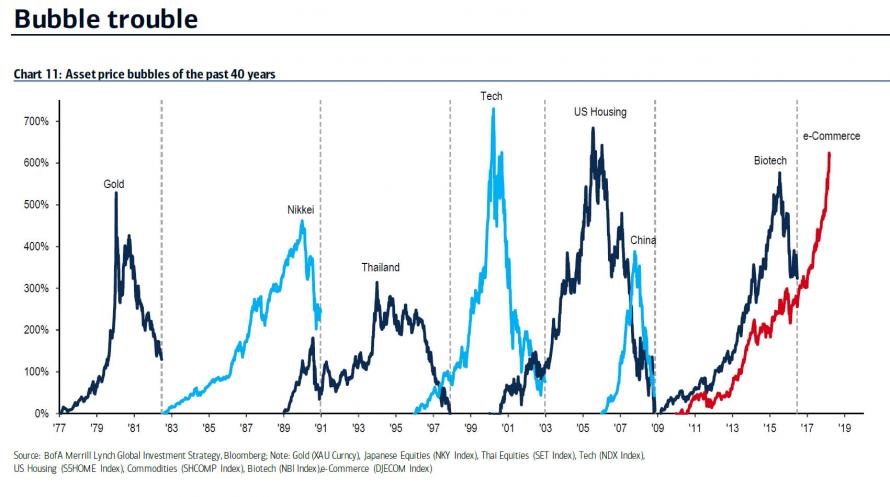

Asset price Bubbles – Selected Historical

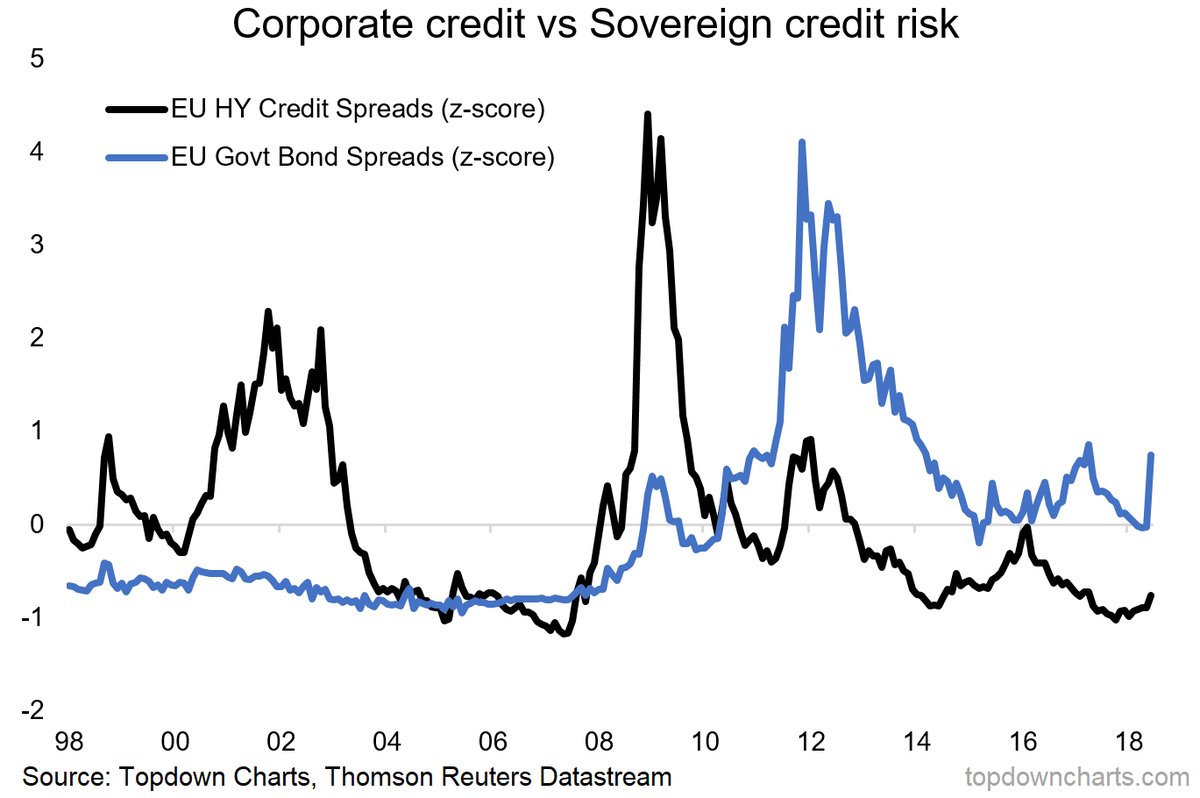

Corporate v Sovereign Risk

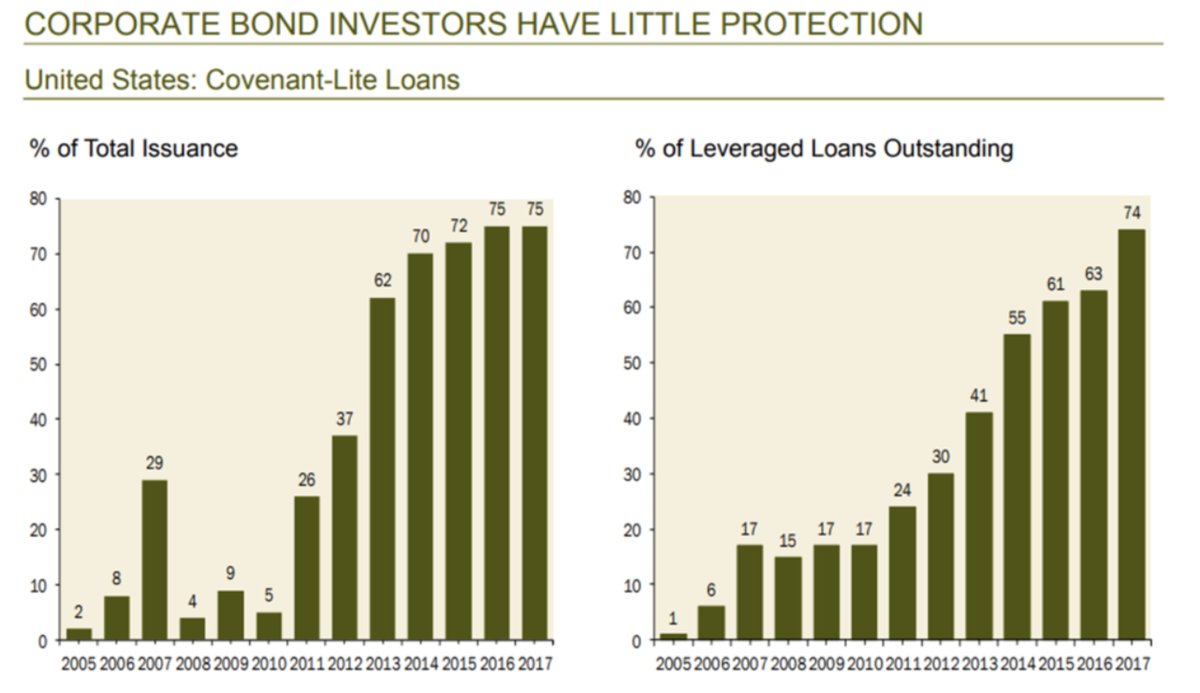

United States – Covenant Lite

Deutsche Bank and Lehman Bros

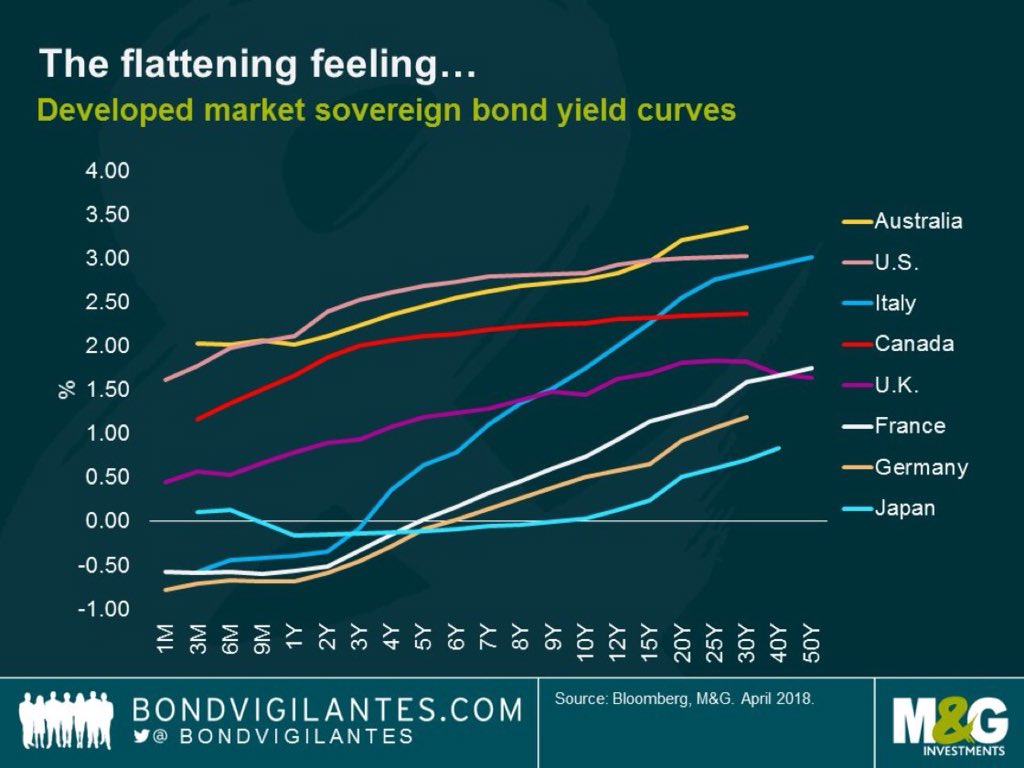

Flattening Yield Curves

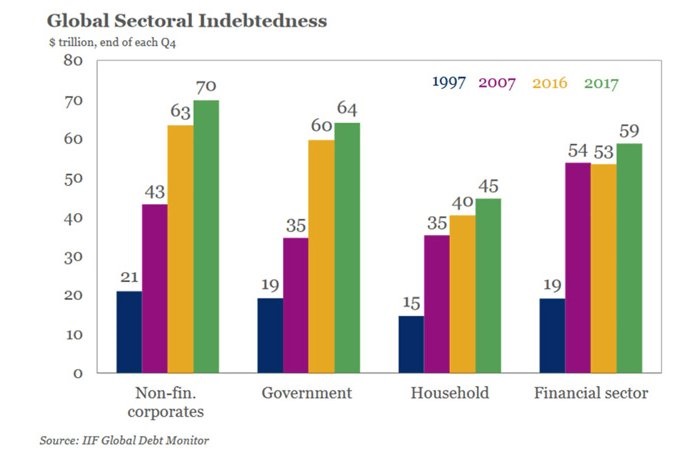

Global Sector Indebtedness

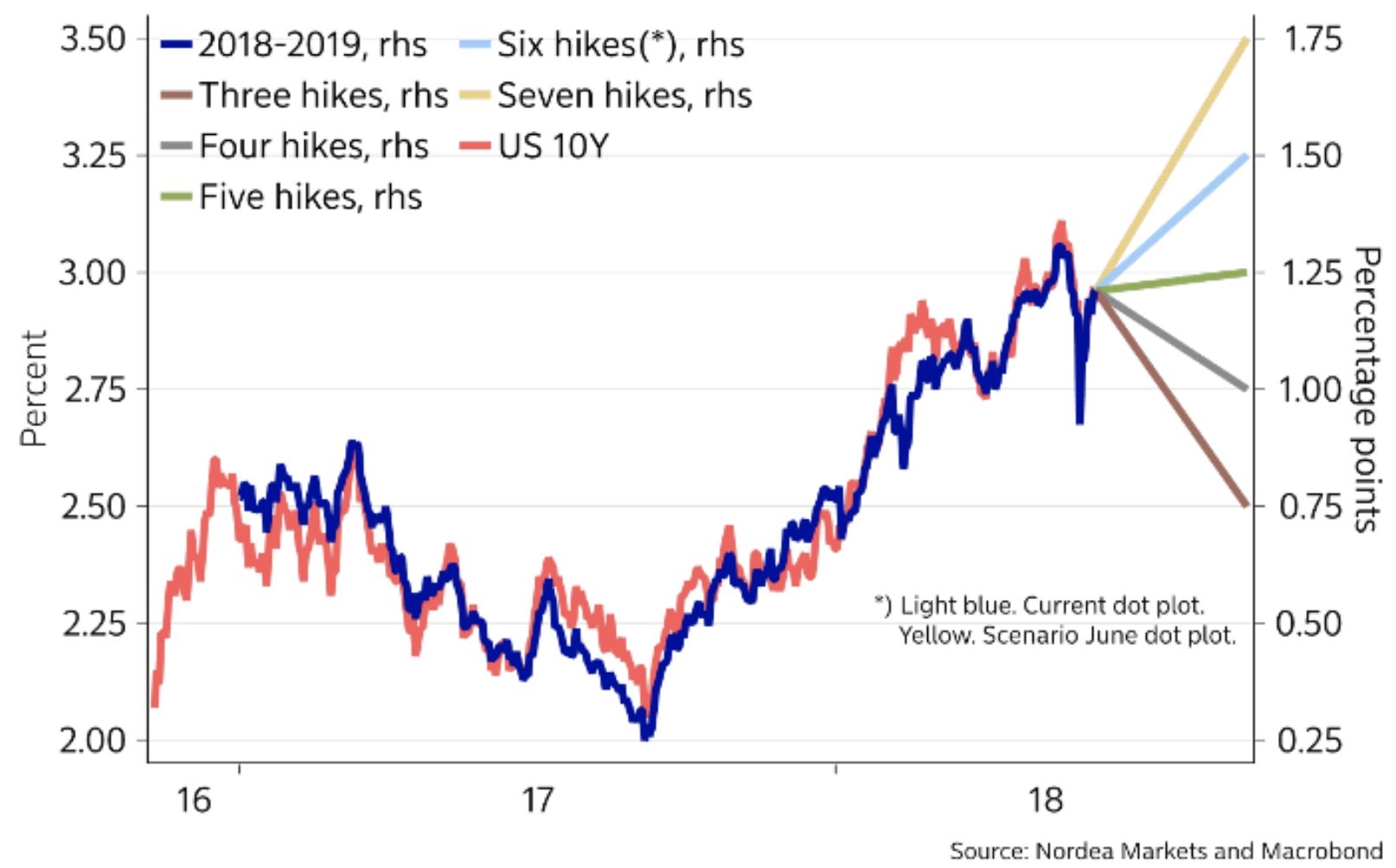

Implied Fed hikes

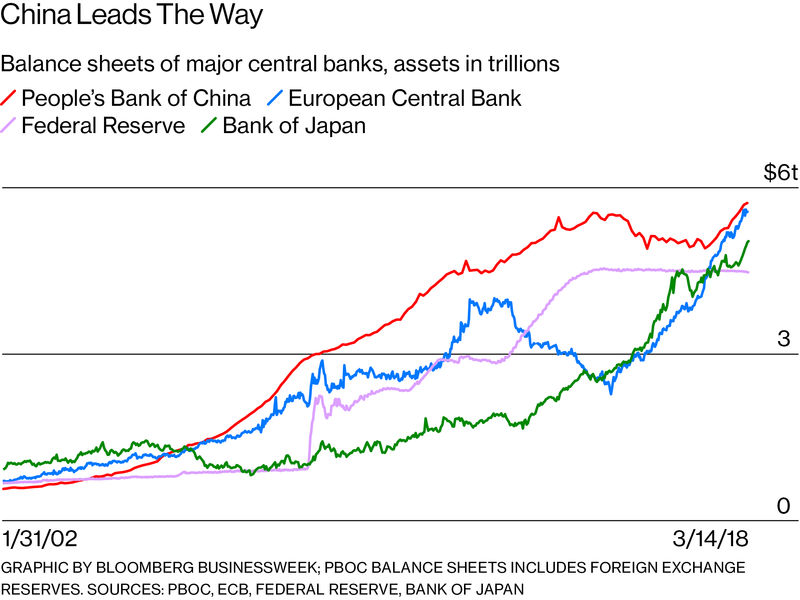

Balance Sheets – Major Central banks

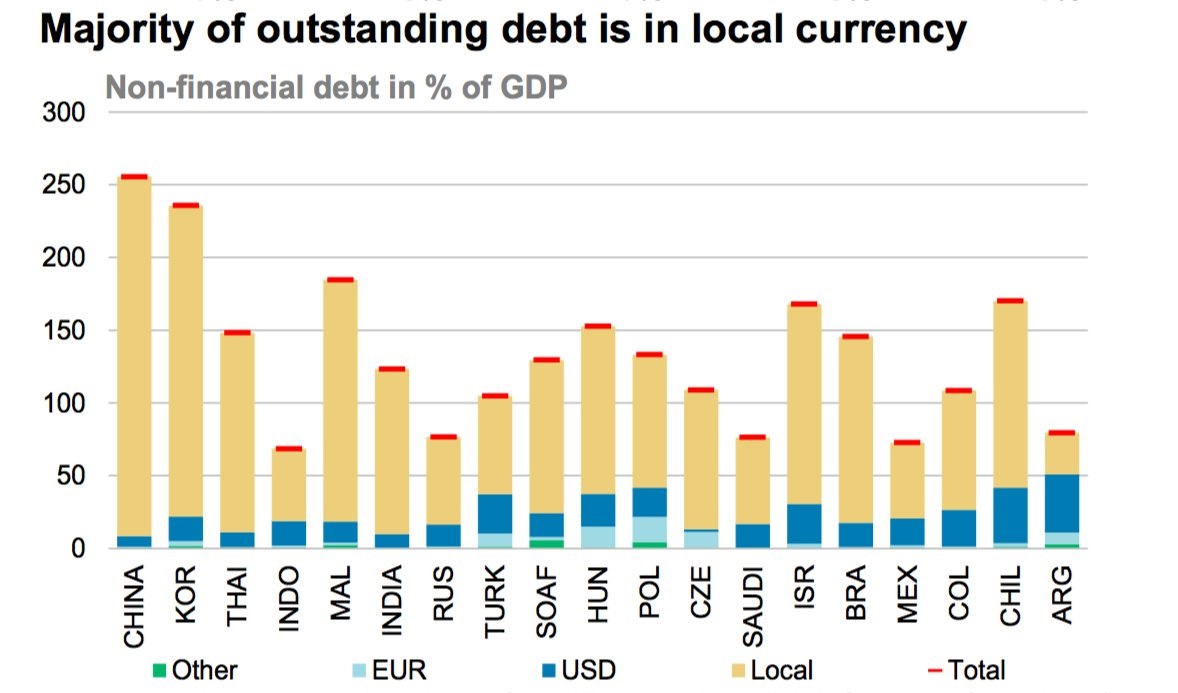

Emerging Market debt & currency

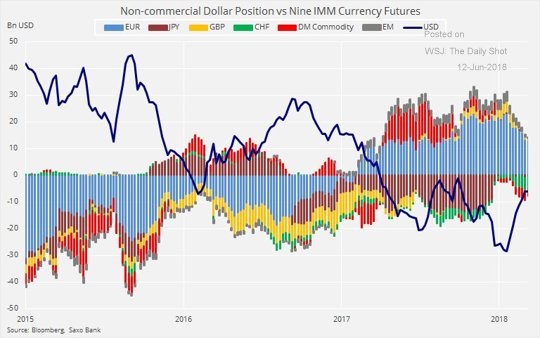

The USD and the rest

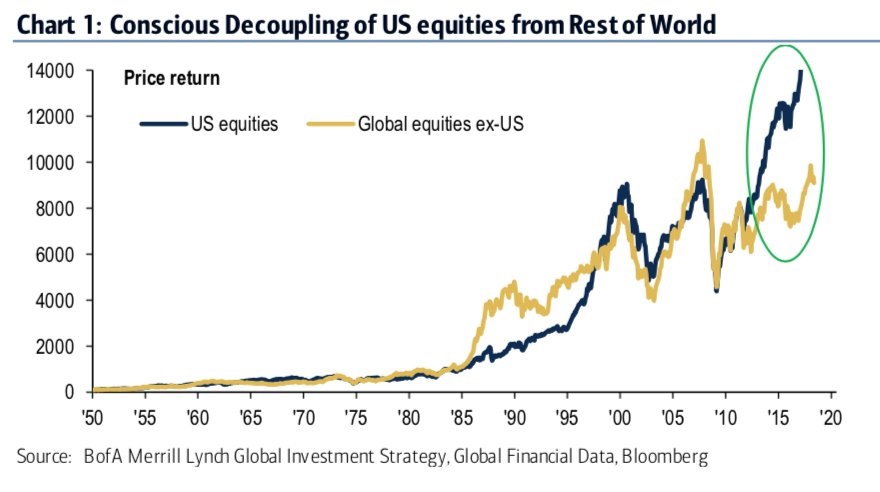

US Equities and the rest

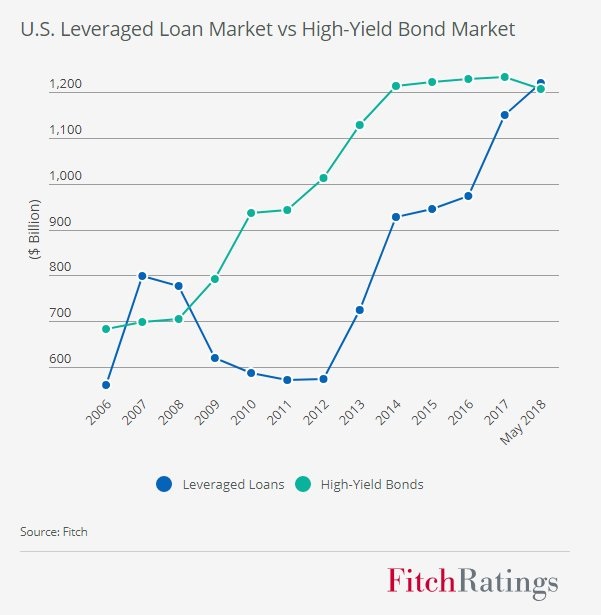

US leveraged loans v High Yield Bonds

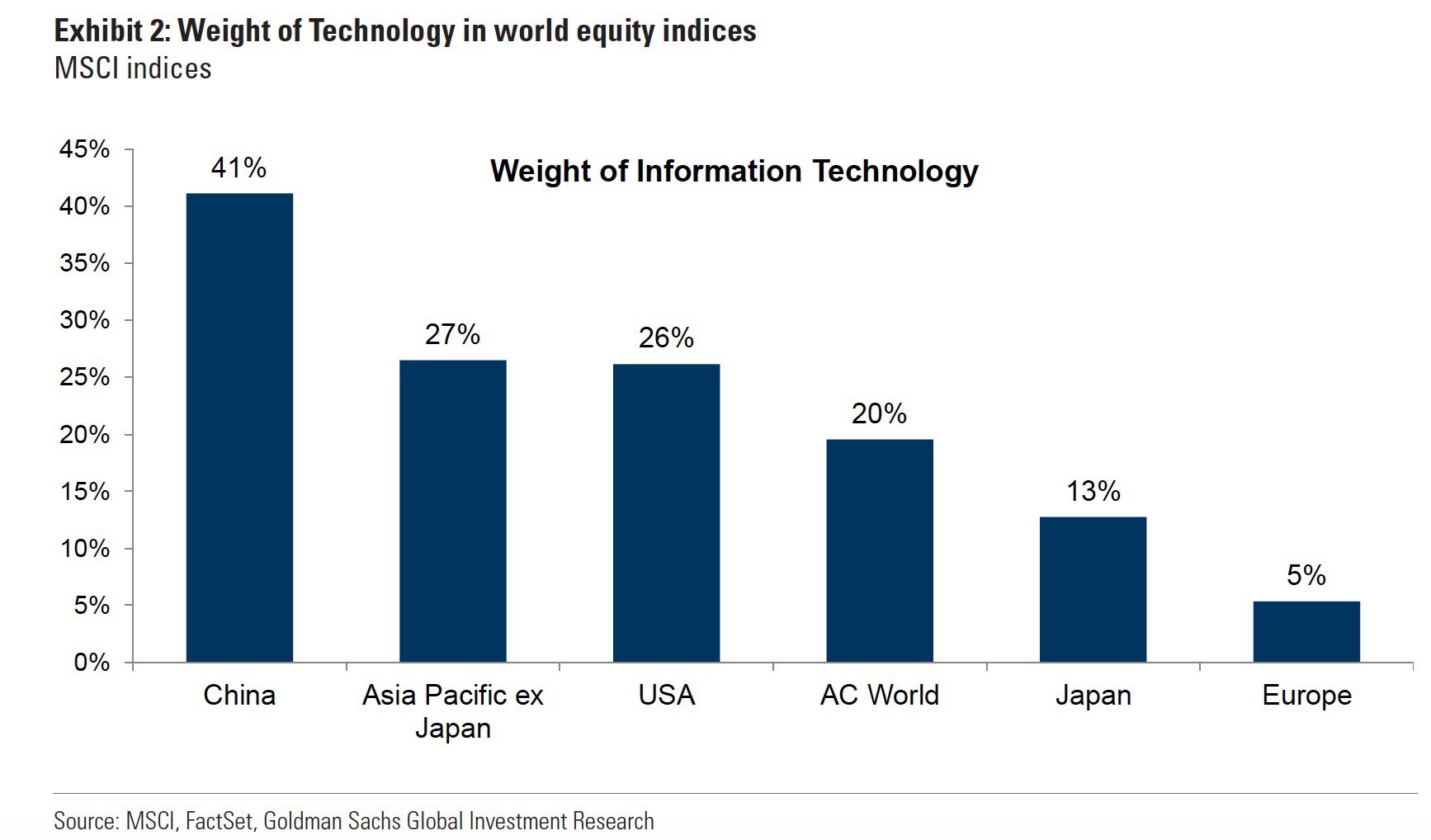

Technology in major global equity indices

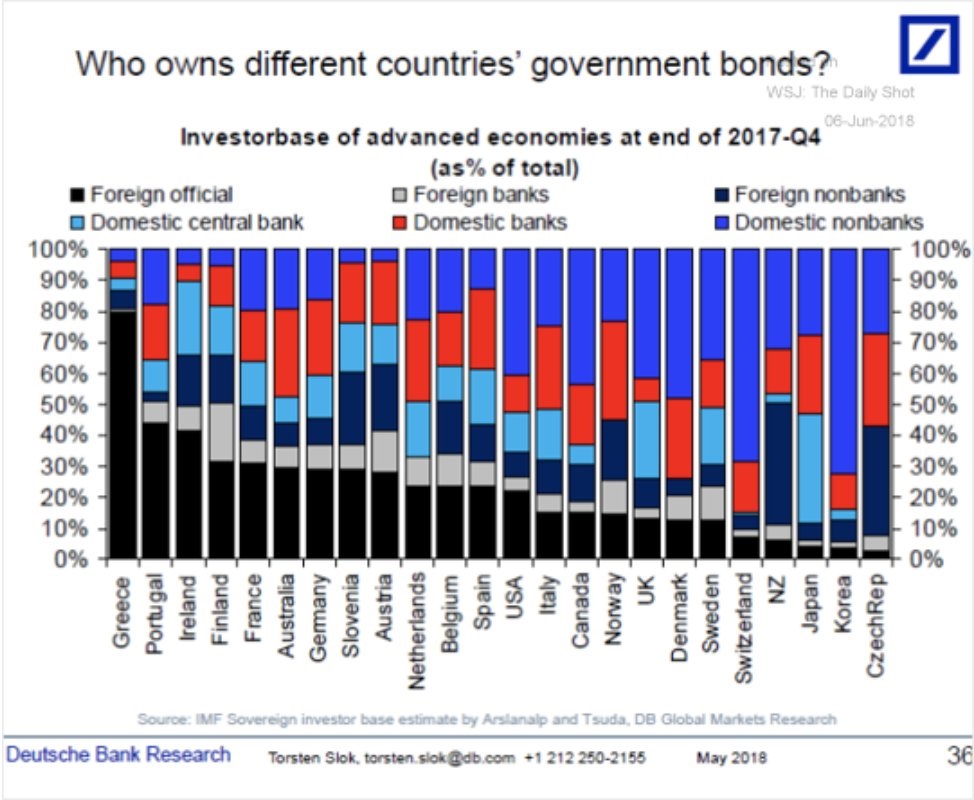

Government Bonds – Who Buys?

Global Macro

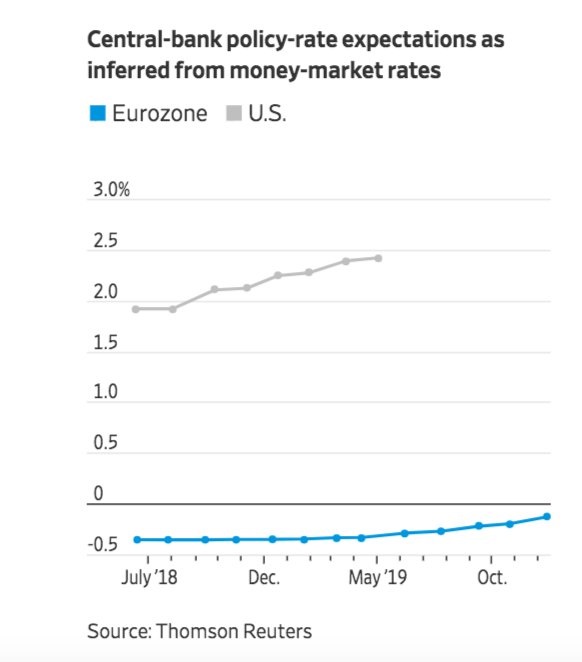

ECB & Fed money market implied moves

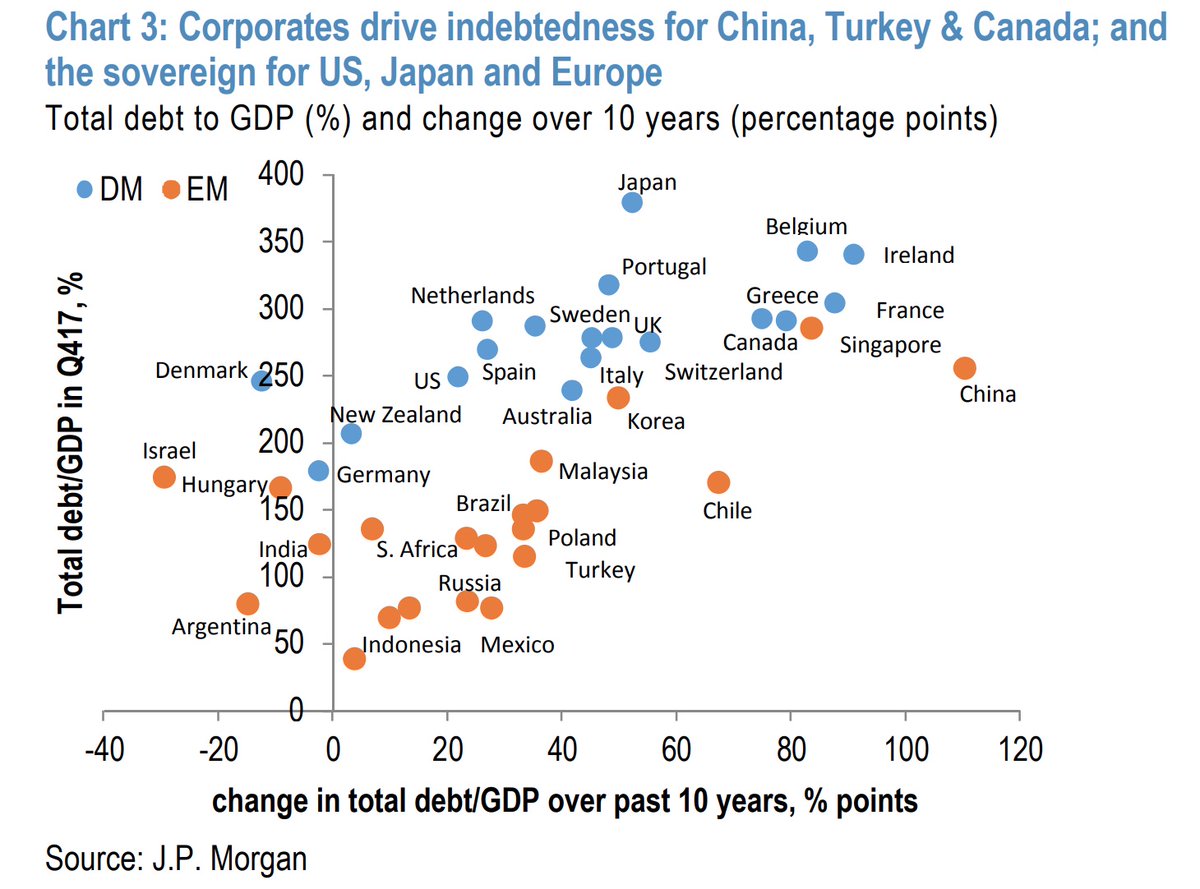

Corporates and Sovereigns as debt drivers

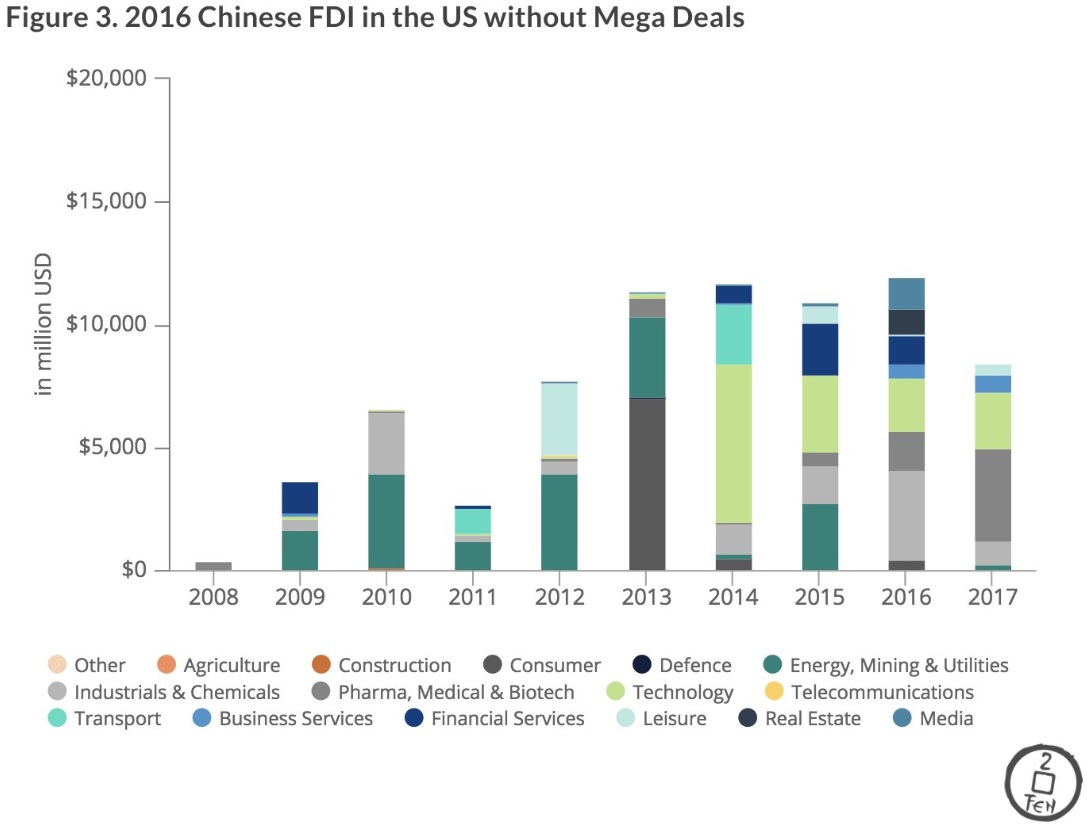

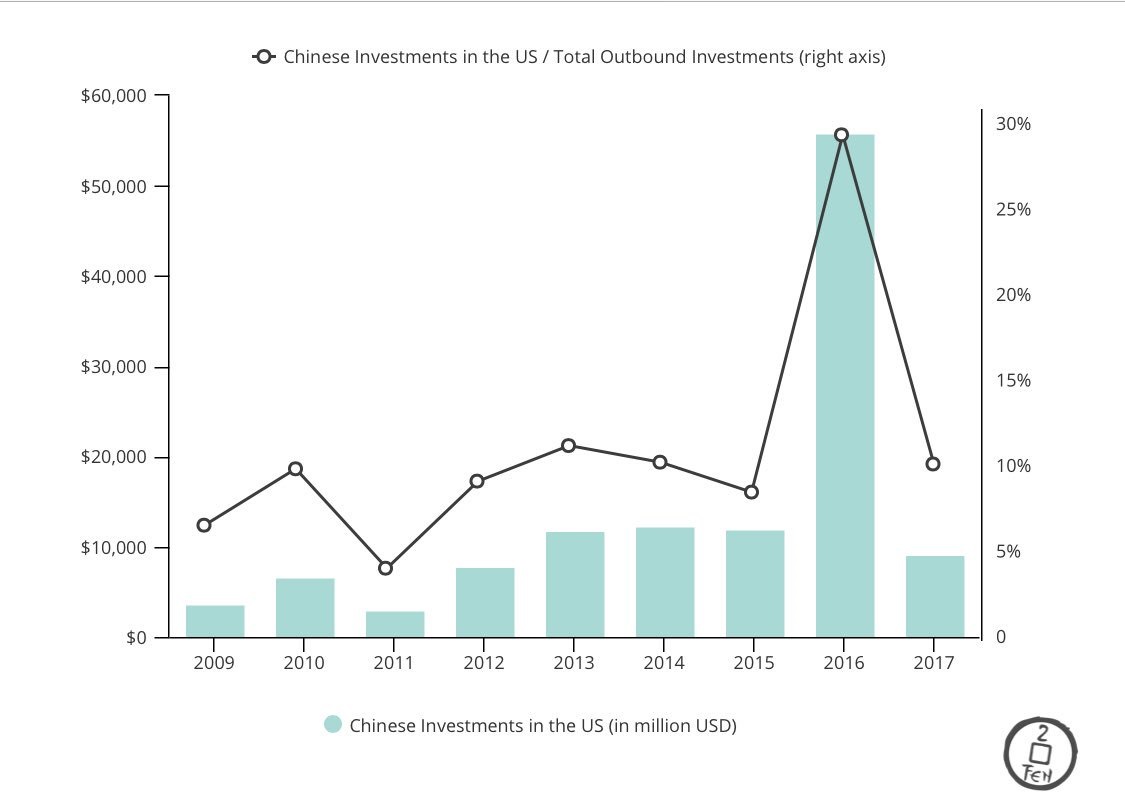

Chinese FDI in the United States

Chinese Investment in the United States as percent of total outbound investment

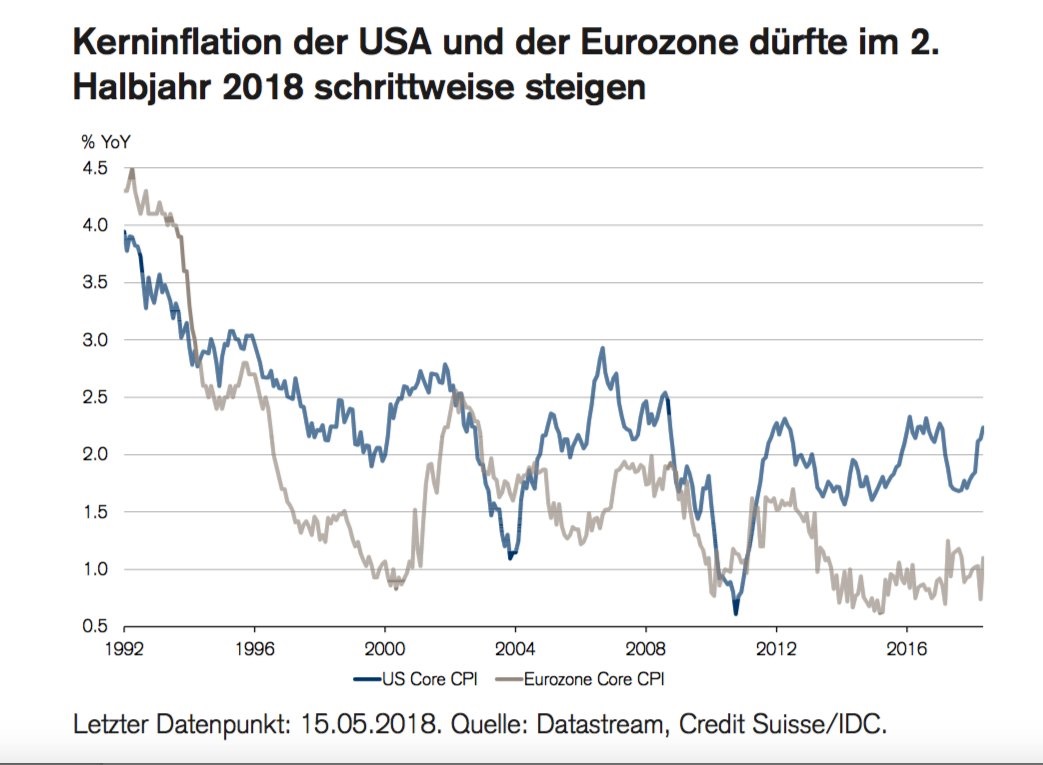

Core CPI – United States and Eurozone

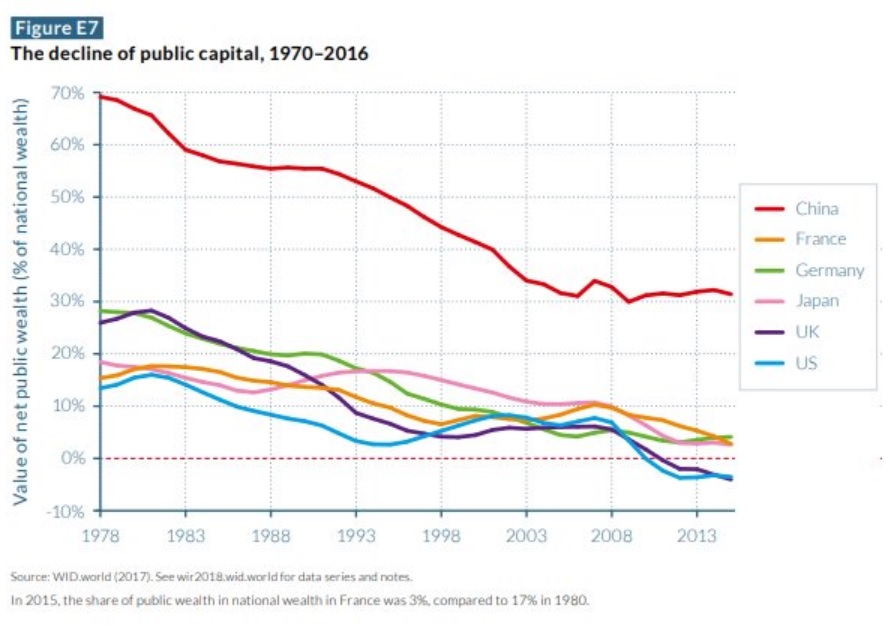

The decline of public capital – selected nations

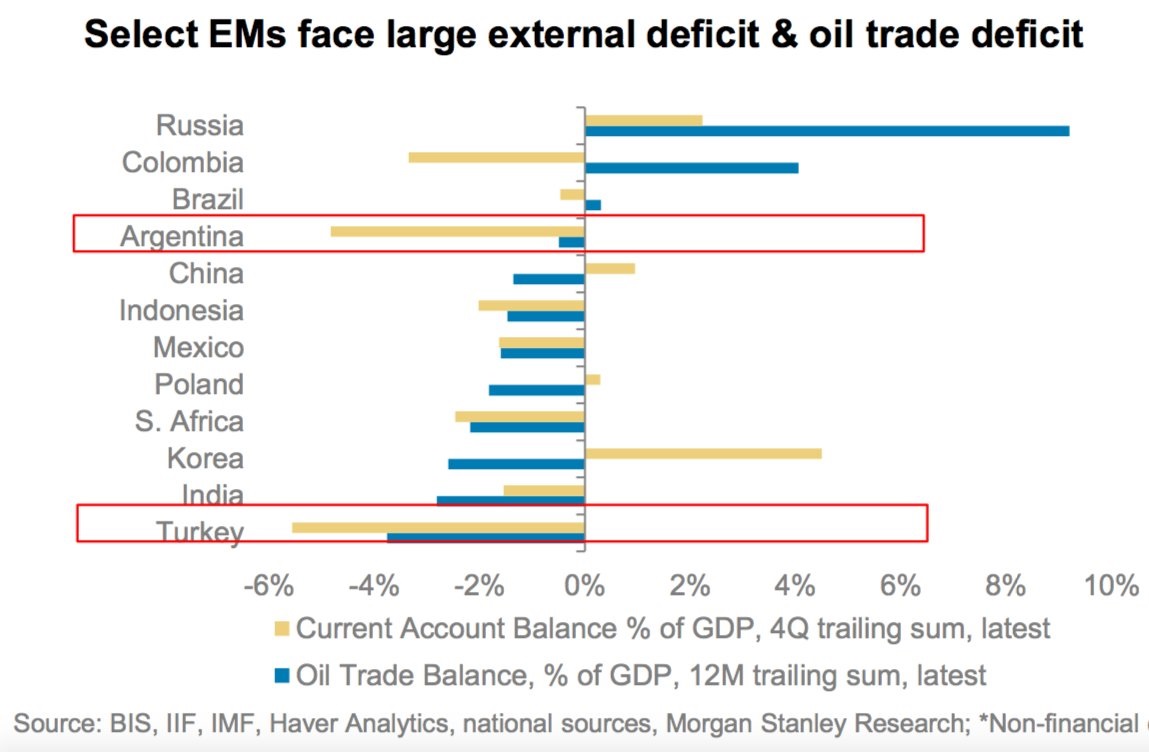

Selected Emerging markets – external deficits and oil

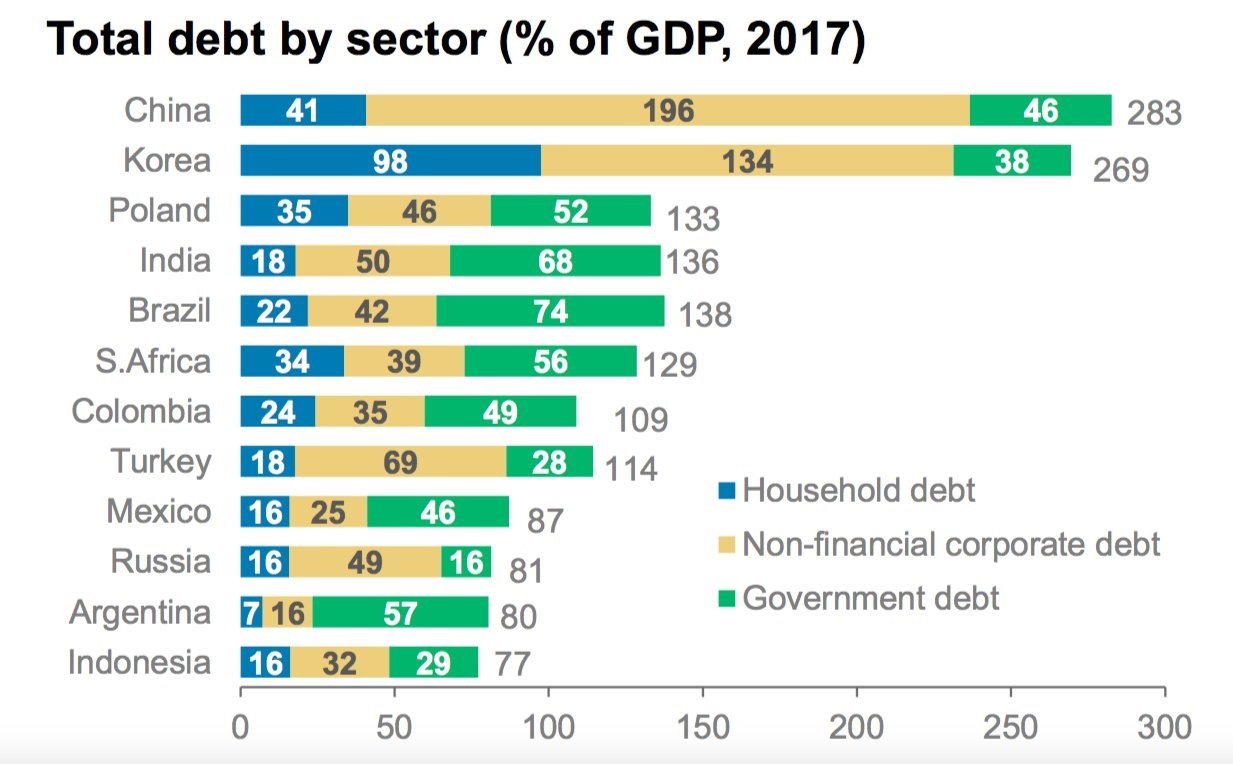

Emerging Markets – debt by sector

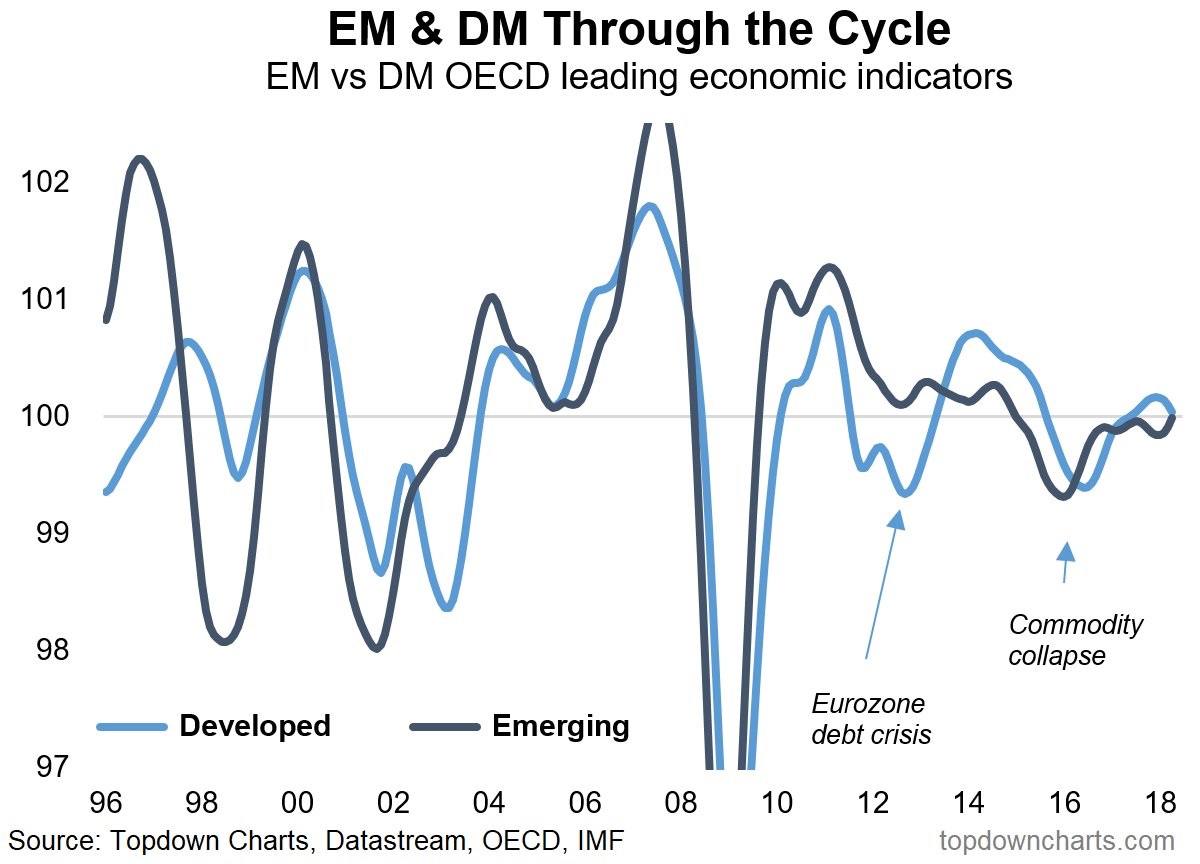

Emerging & Developed Markets

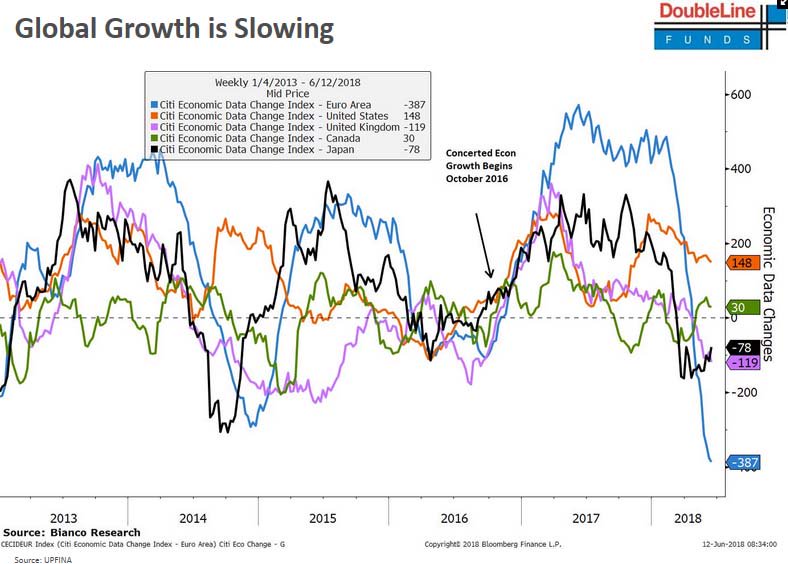

Citi economic data change by region

Intergenerational earnings and mobility – selected developed economies

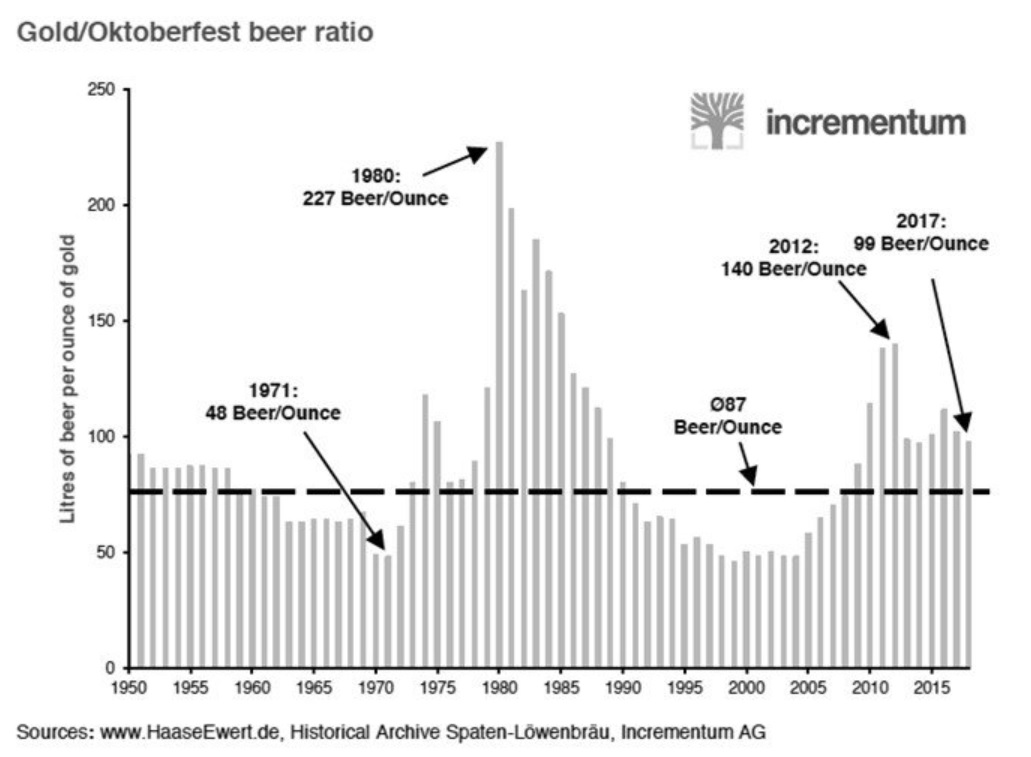

Gold/Oktoberfest beer

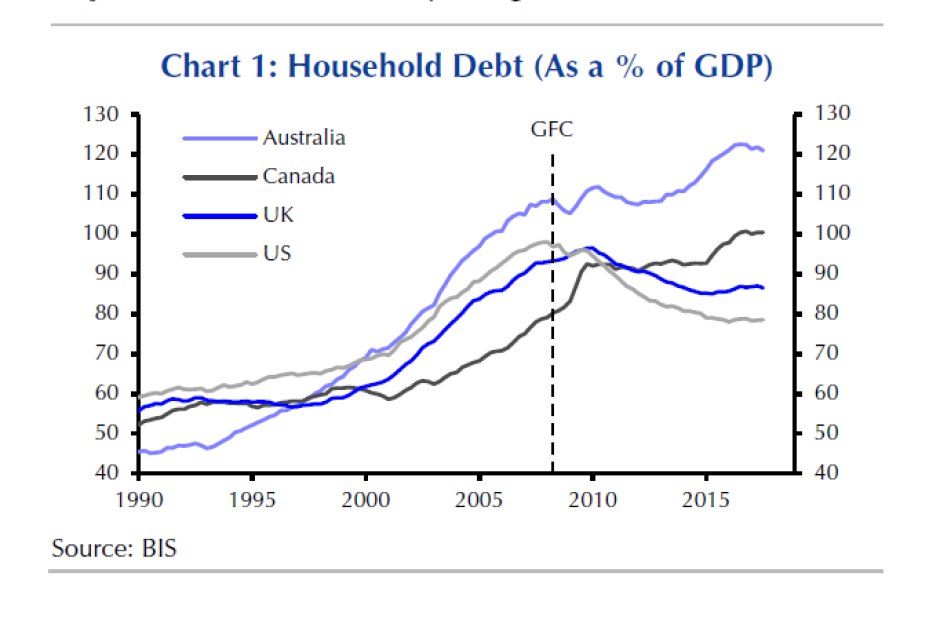

Household debt – the Anglosphere

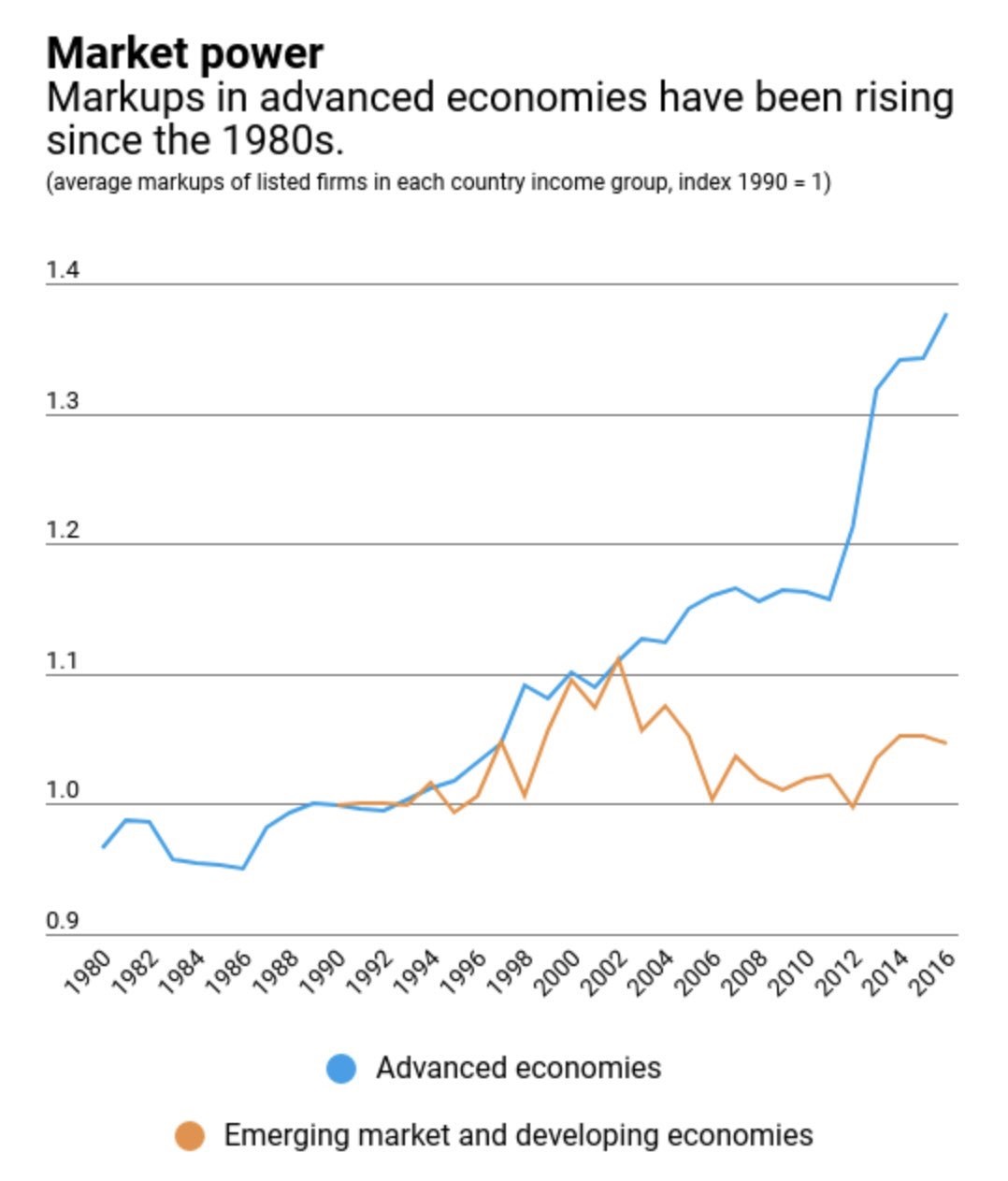

Markup Power – developed and emerging economies (maybe all that talk about competition was………)

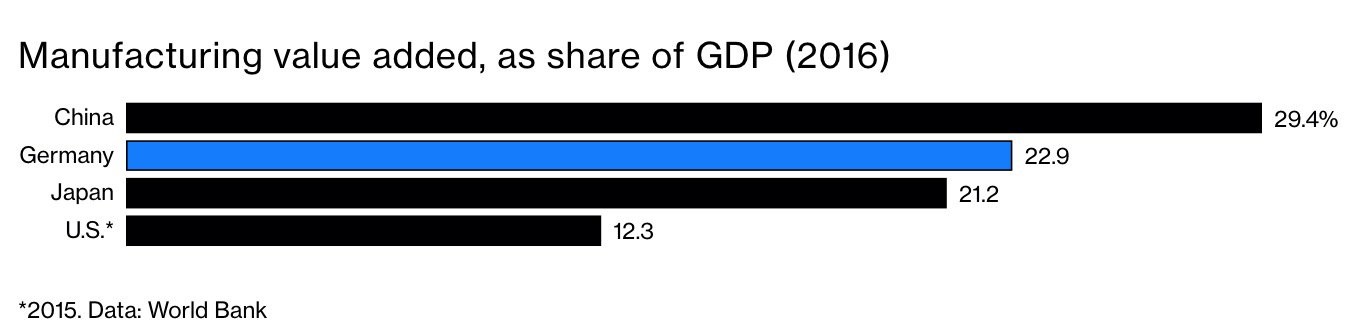

Manufacturing Value Added – major manufacturers

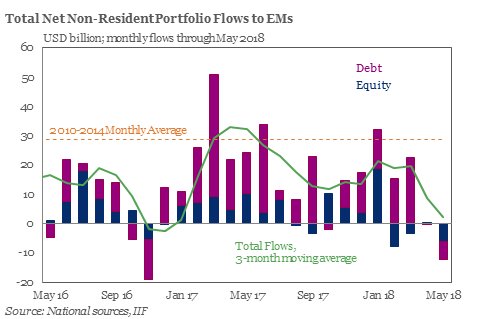

Emerging Markets – Non Resident Portfolio Flows

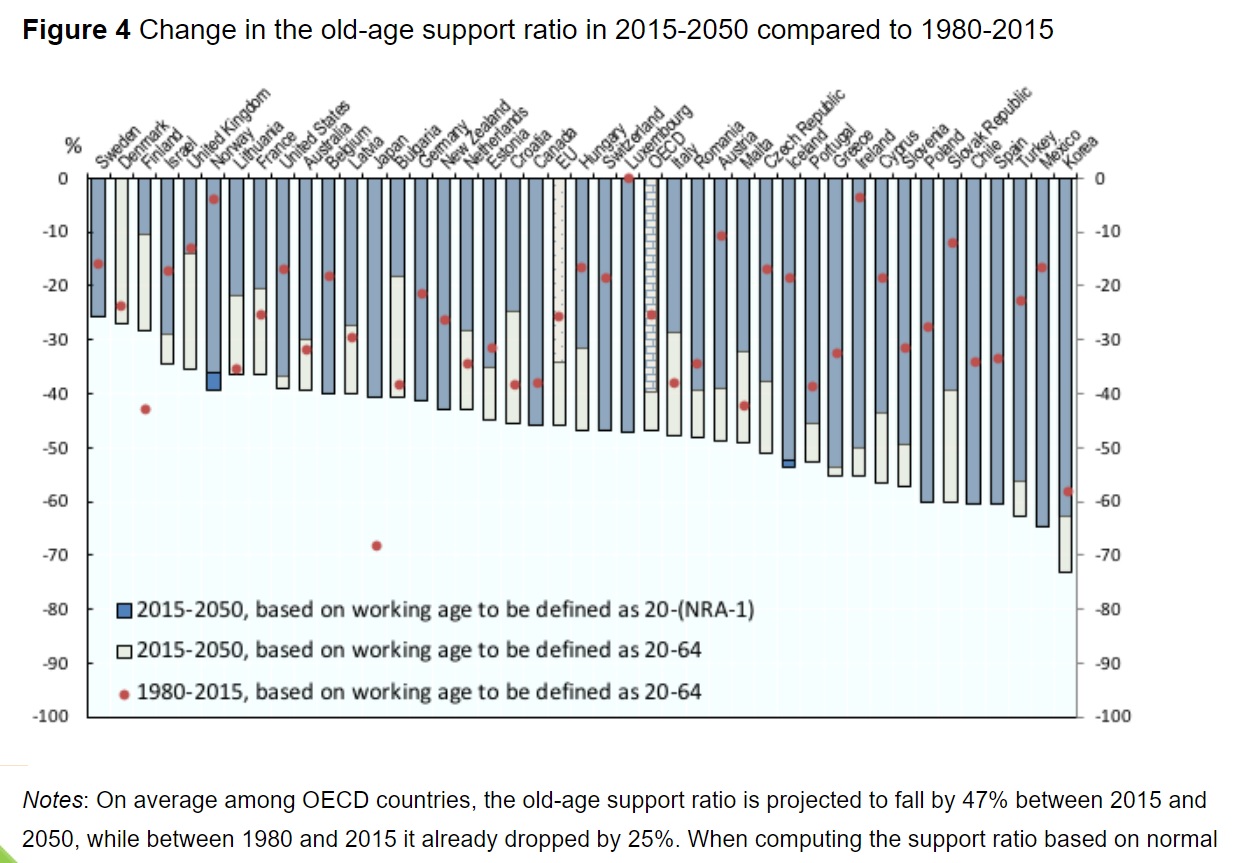

Old Age Support Ration – Selected Nations 1980-2015 and 2015 – 2050

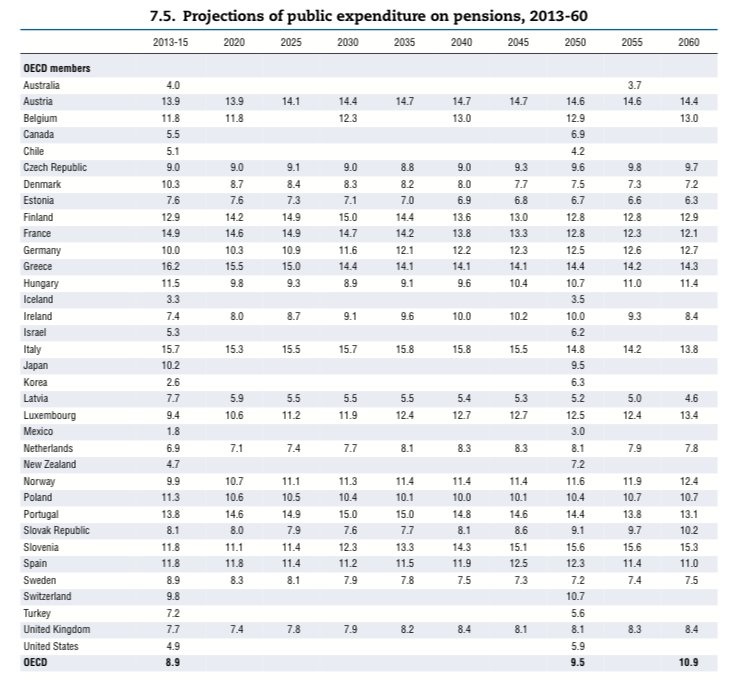

Pension related Expenditures – selected nations 2013-2060

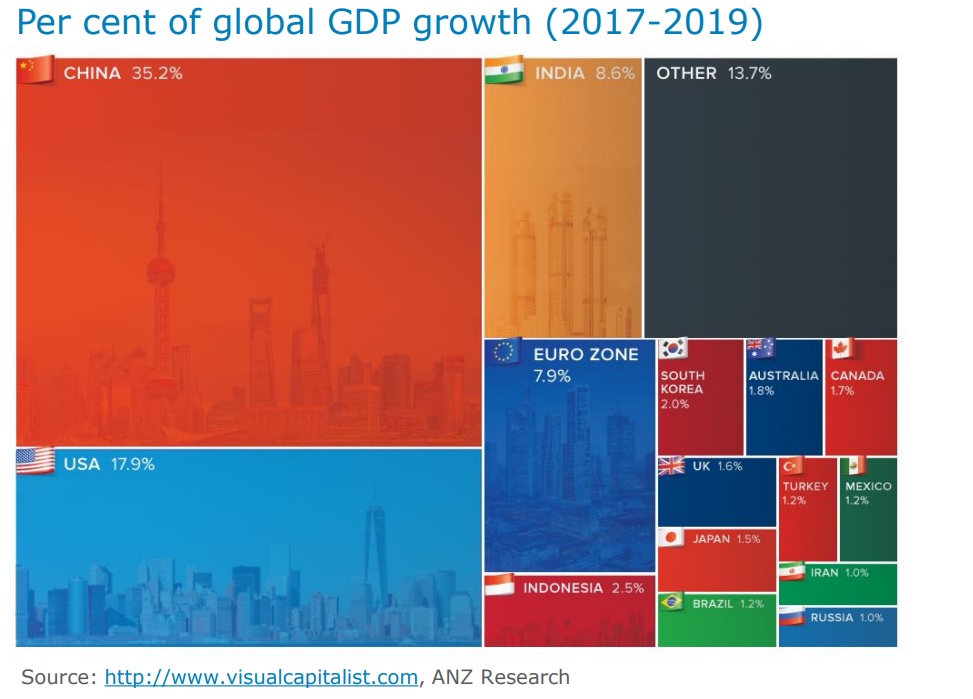

National drivers of global growth – 2017 – 2019

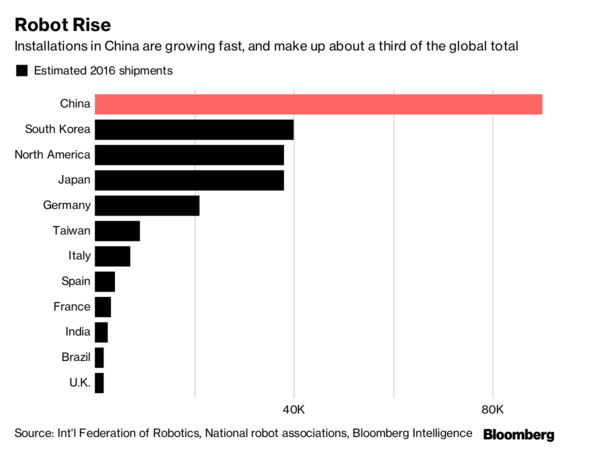

Robot Installations – selected nations

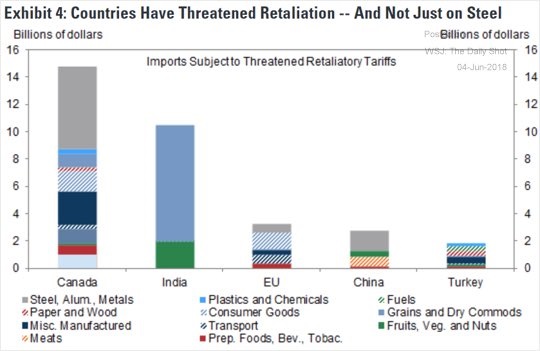

Trump Tariffs – potential responses

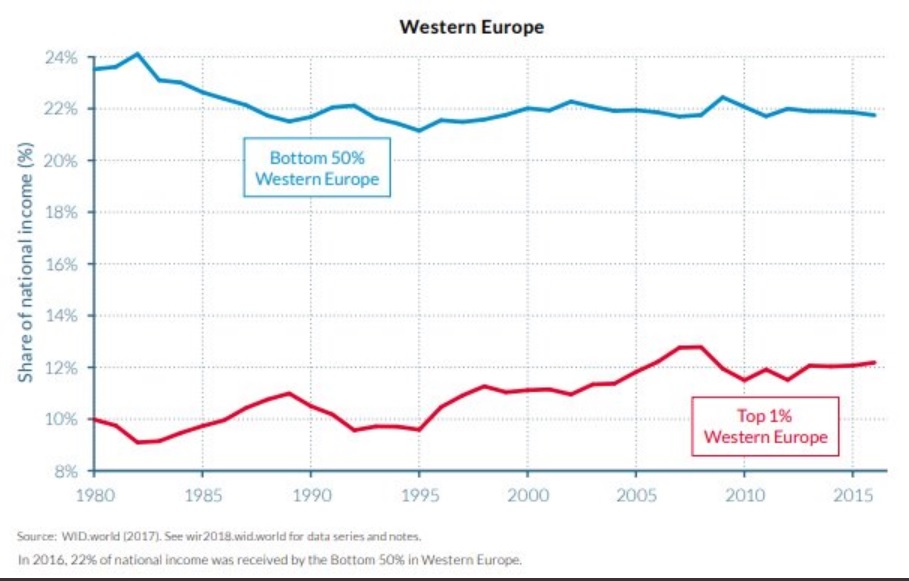

Top 1% and Bottom 50% – Western Europe

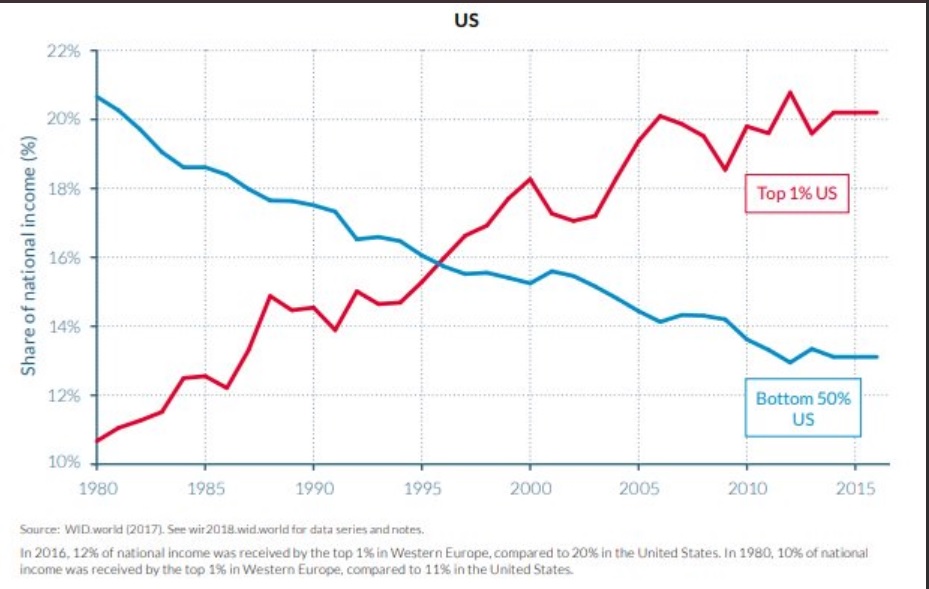

Top 1% and Bottom 50% – United States

…and furthermore…

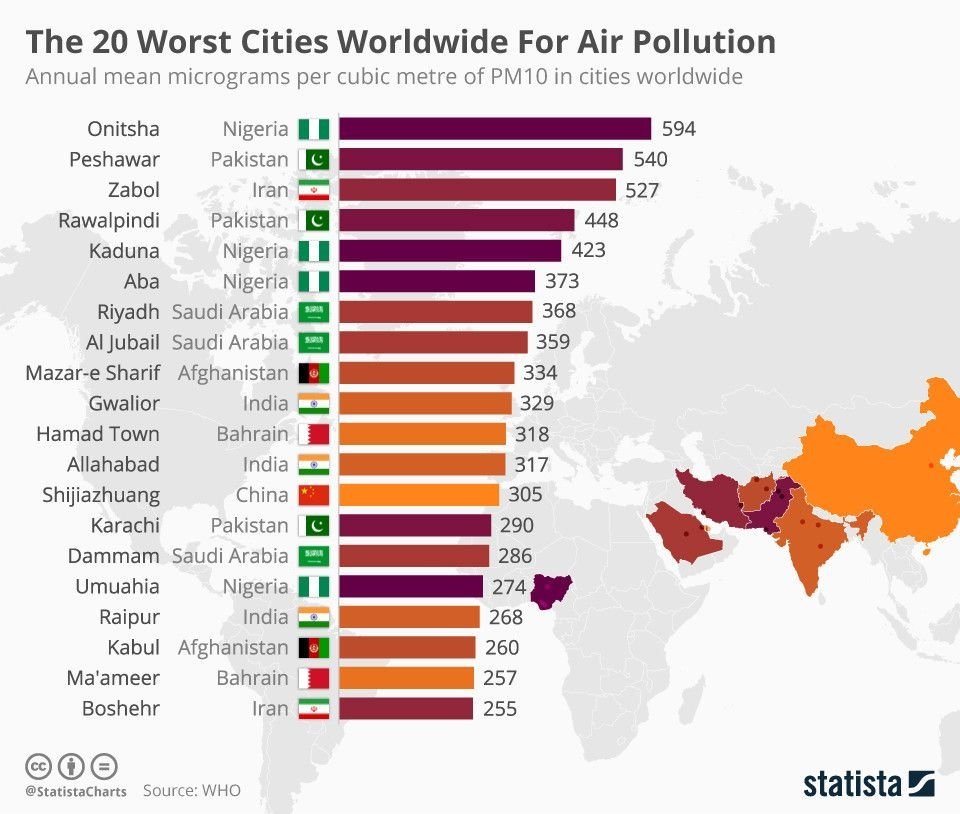

Air Pollution – the worst

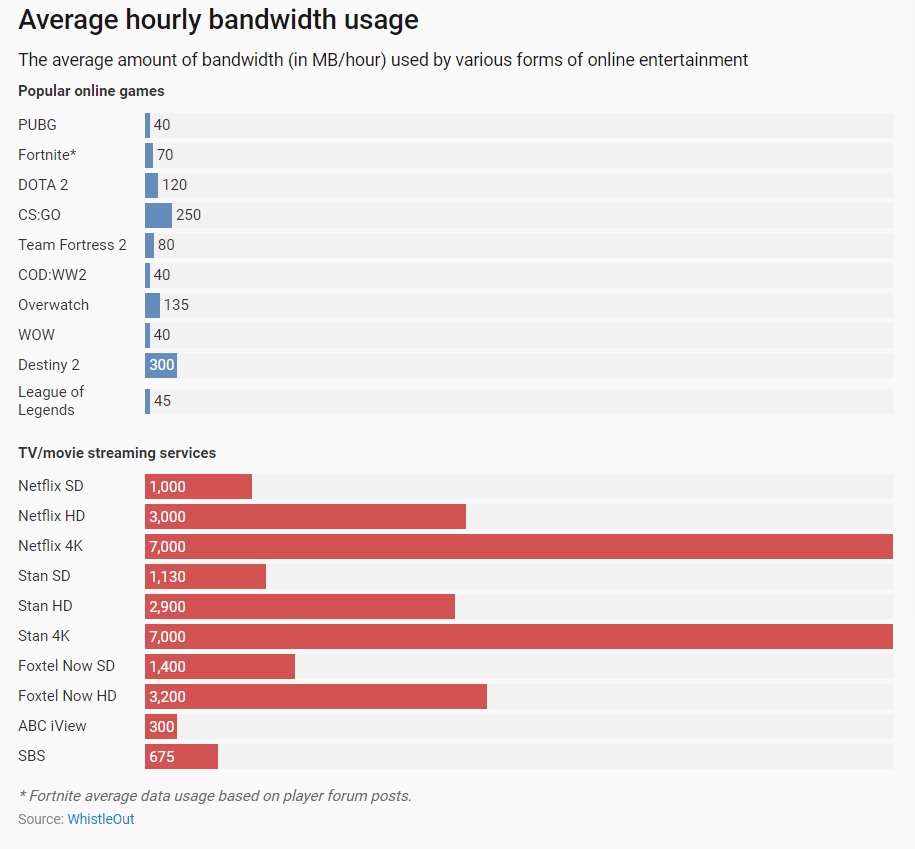

Bandwidth usage – selected games and activities

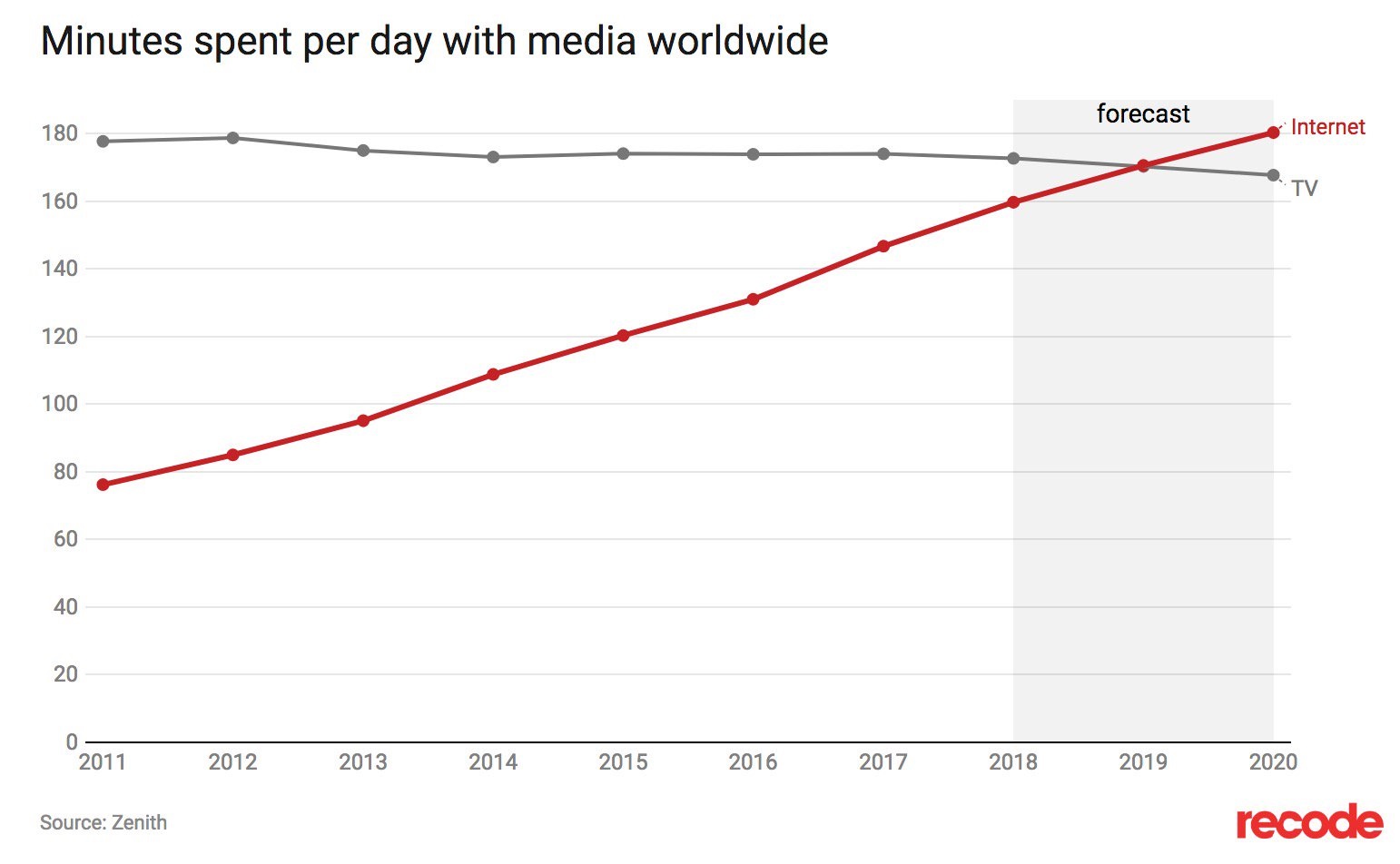

Minutes per day – TV and internet

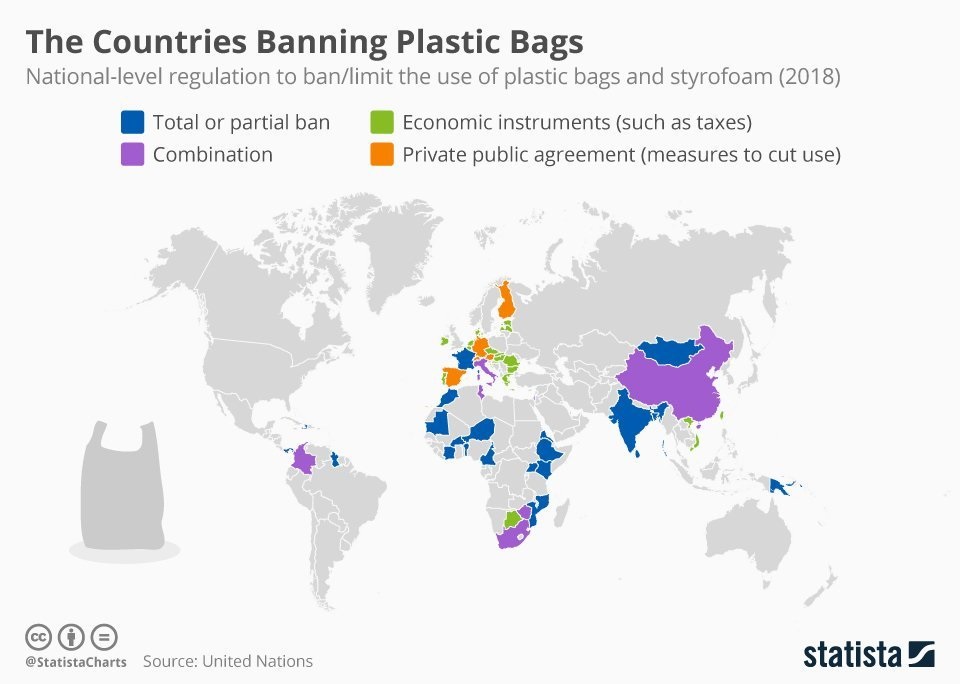

Plastic Bags being Banned

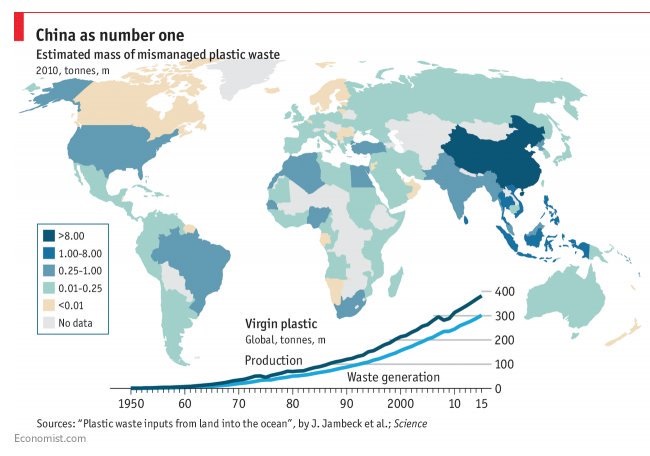

Plastic Waste – estimated blame apportionment

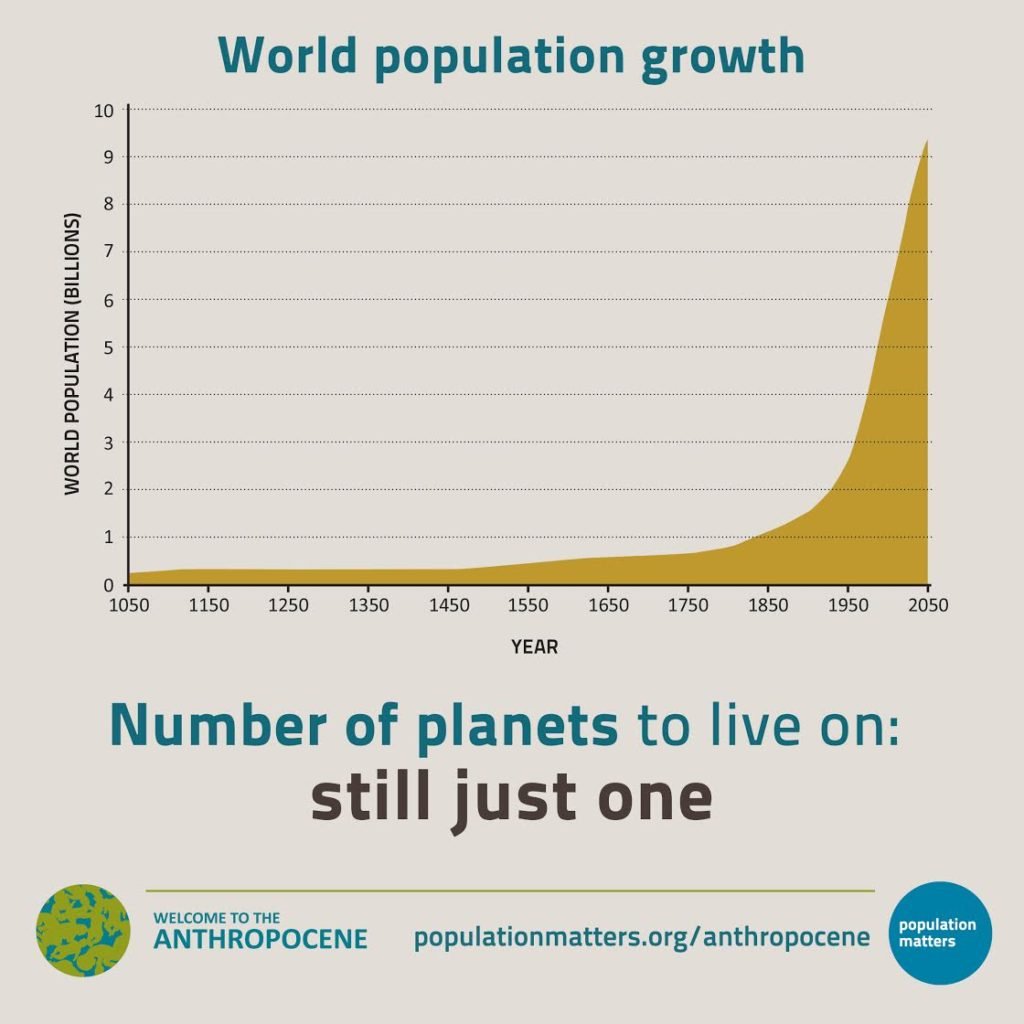

Global Population Growth

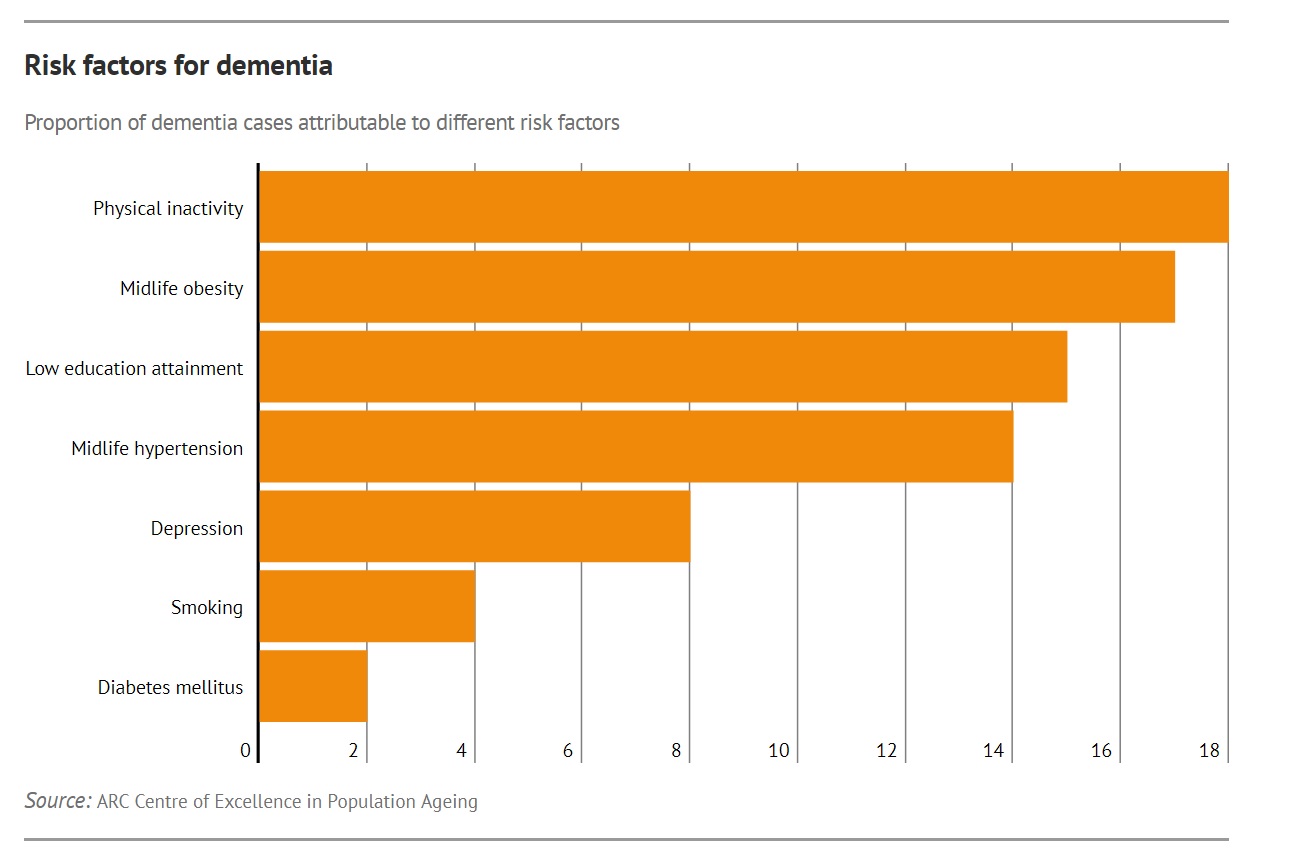

Dementia Risk Factors