Cross-posted Martin North:

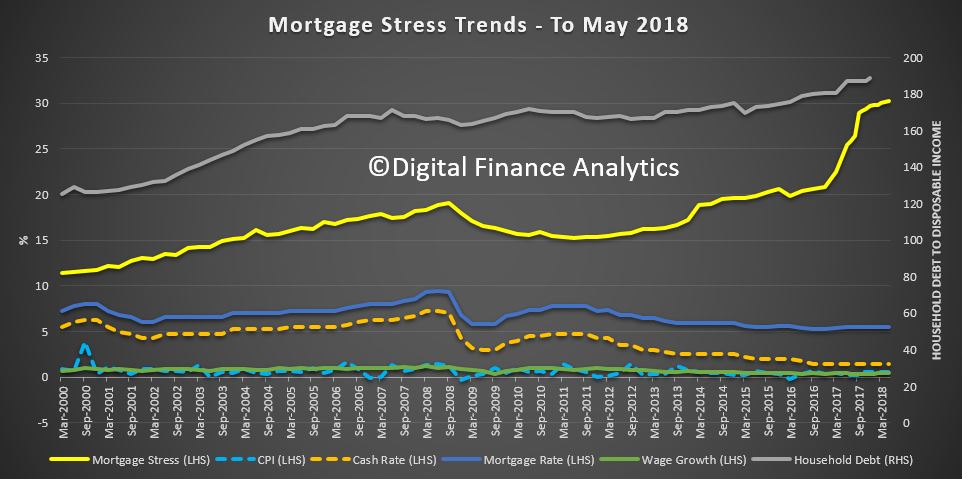

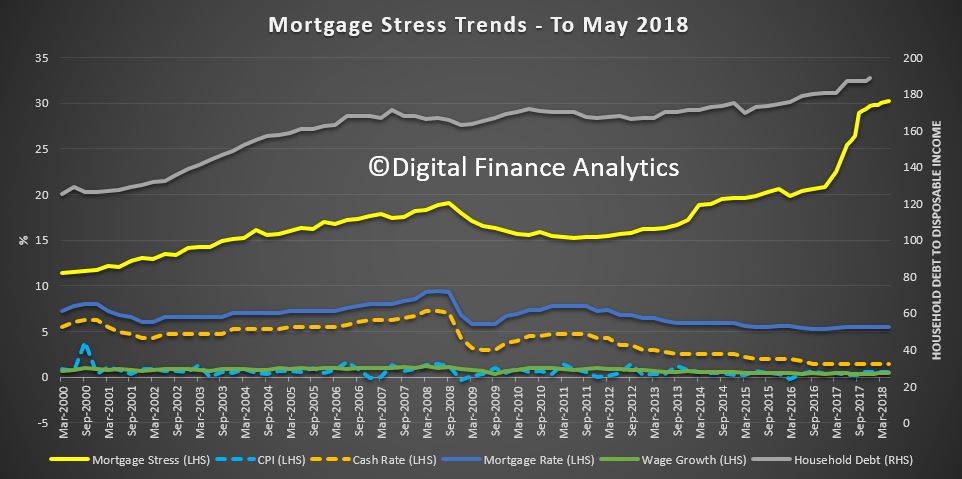

Digital Finance Analytics (DFA) has released the May 2018 mortgage stress and default analysis update. Across Australia, more than 966,000 households are estimated to be now in mortgage stress (last month 963,000). This equates to 30.2% of owner occupied borrowing households. In addition, more than 22,600 of these are in severe stress, up 1,000 from last month. We estimate that more than 56,700 households risk 30-day default in the next 12 months. We expect bank portfolio losses to be around 2.7 basis points, though losses in WA are higher at 5 basis points. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates.

Martin North, Principal of Digital Finance Analytics says “the pressure on households in a low income growth, high cost, highly leveraged environment means that overall, risks in the system continue to rise, and while recent strengthening of lending standards will help protect new borrowers, there are many households currently holding loans which would not now be approved. The recent Royal Commission laid bare some of the industry practices which help to explain why stress is so high. This is a significant sleeping problem and the risks in the system remain higher than many recognise”.

Martin North, Principal of Digital Finance Analytics says “the pressure on households in a low income growth, high cost, highly leveraged environment means that overall, risks in the system continue to rise, and while recent strengthening of lending standards will help protect new borrowers, there are many households currently holding loans which would not now be approved. The recent Royal Commission laid bare some of the industry practices which help to explain why stress is so high. This is a significant sleeping problem and the risks in the system remain higher than many recognise”. “We continue to see the number of households rising, and the quantum is now economically significant. Even now, household debt continues to climb to new record levels. Mortgage lending is still growing at two to three times income. This is not sustainable and we are expecting lending growth to continue to moderate in the months ahead as underwriting standards are tightened and home prices fall further”. The latest household debt to income ratio is now at a record 188.6.[1]

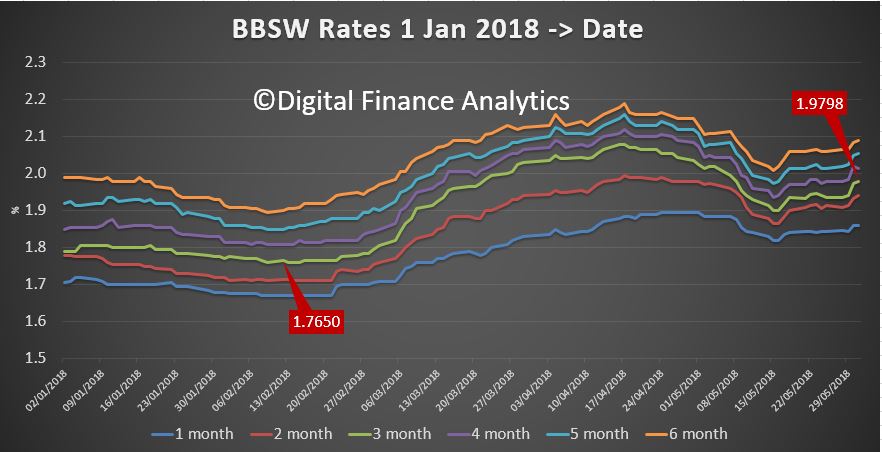

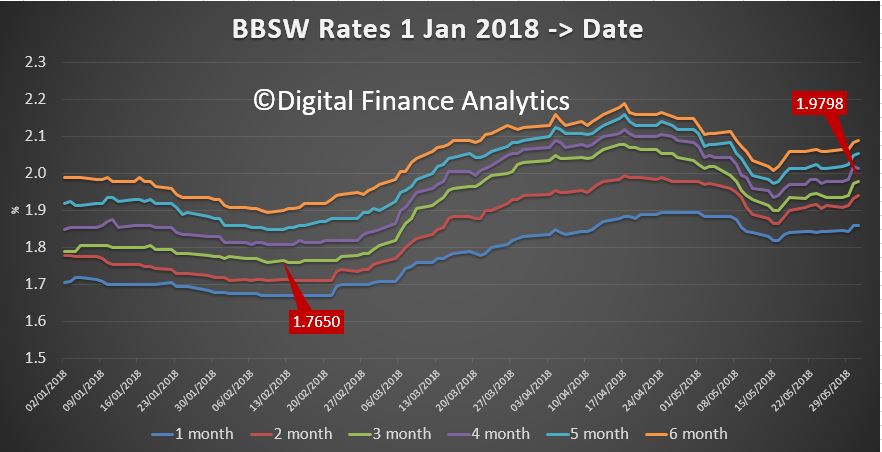

The forces which are lifting mortgage stress levels remain largely the same. In cash flow terms, we see households having to cope with rising living costs – notably child care, school fees and fuel – whilst real incomes continue to fall and underemployment remains high. Households have larger mortgages, thanks to the strong rise in home prices, especially in the main eastern state centres, and now prices are slipping. While mortgage interest rates remain quite low for owner occupied borrowers, those with interest only loans or investment loans have seen significant rises. We expect some upward pressure on real mortgage rates in coming months as international funding pressures mount, a potential for local rate rises and margin pressure on the banks thanks to a higher Bank Bill Swap Rate (BBSW). The potential for a 20-25 basis point hike by the banks is increasing, and this would lift the number of households in mortgage stress higher again.

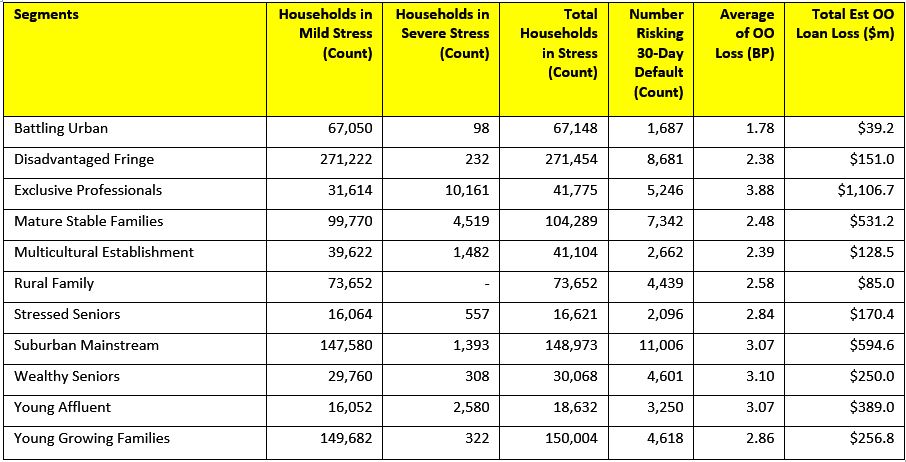

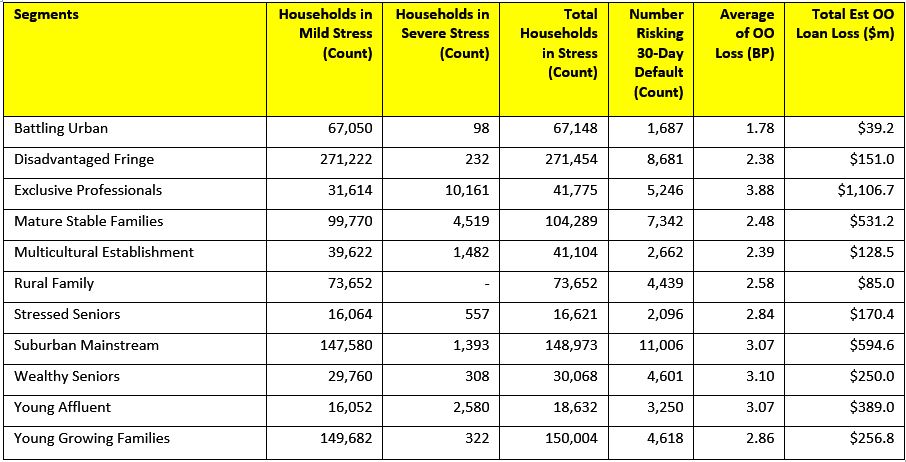

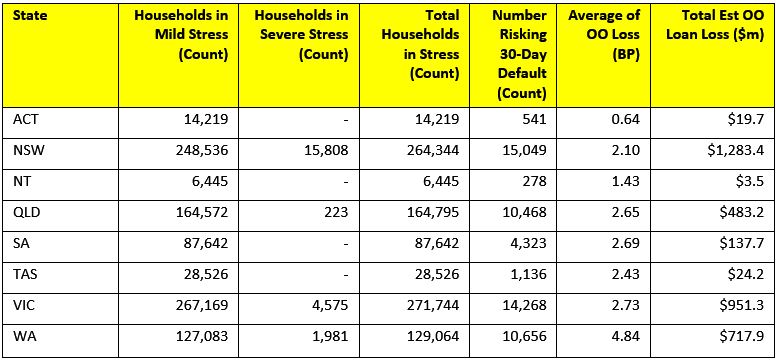

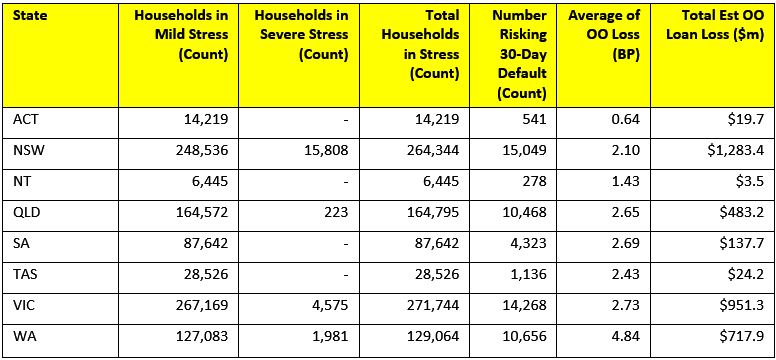

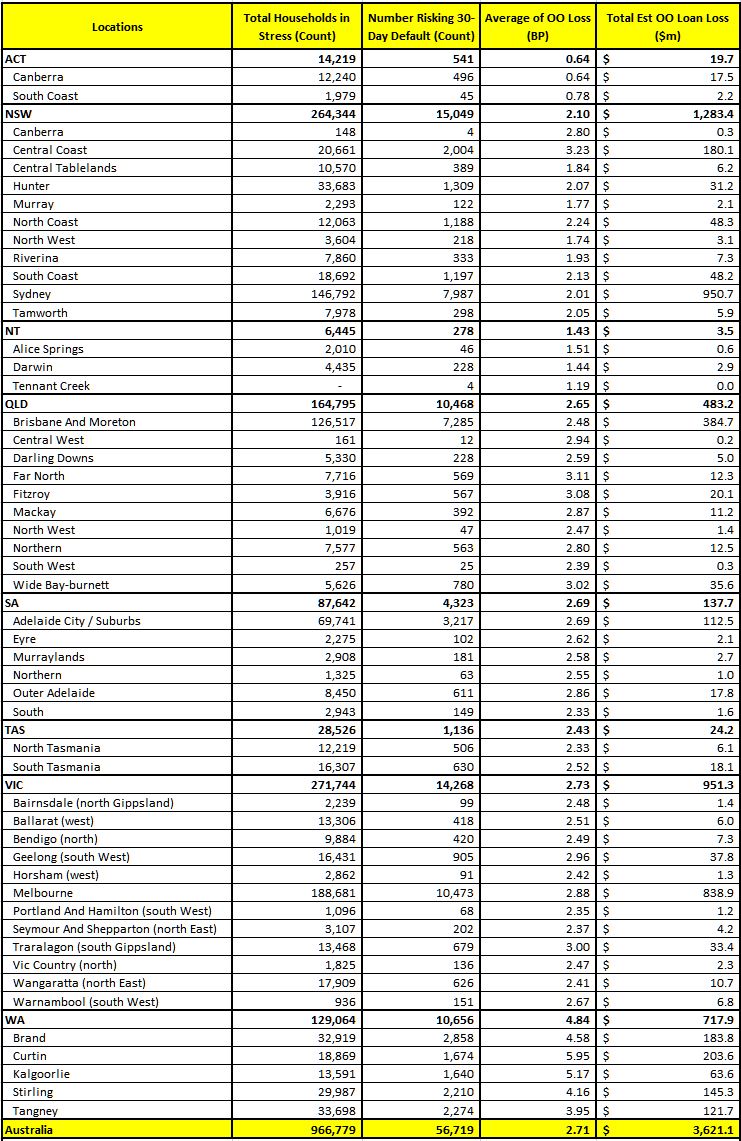

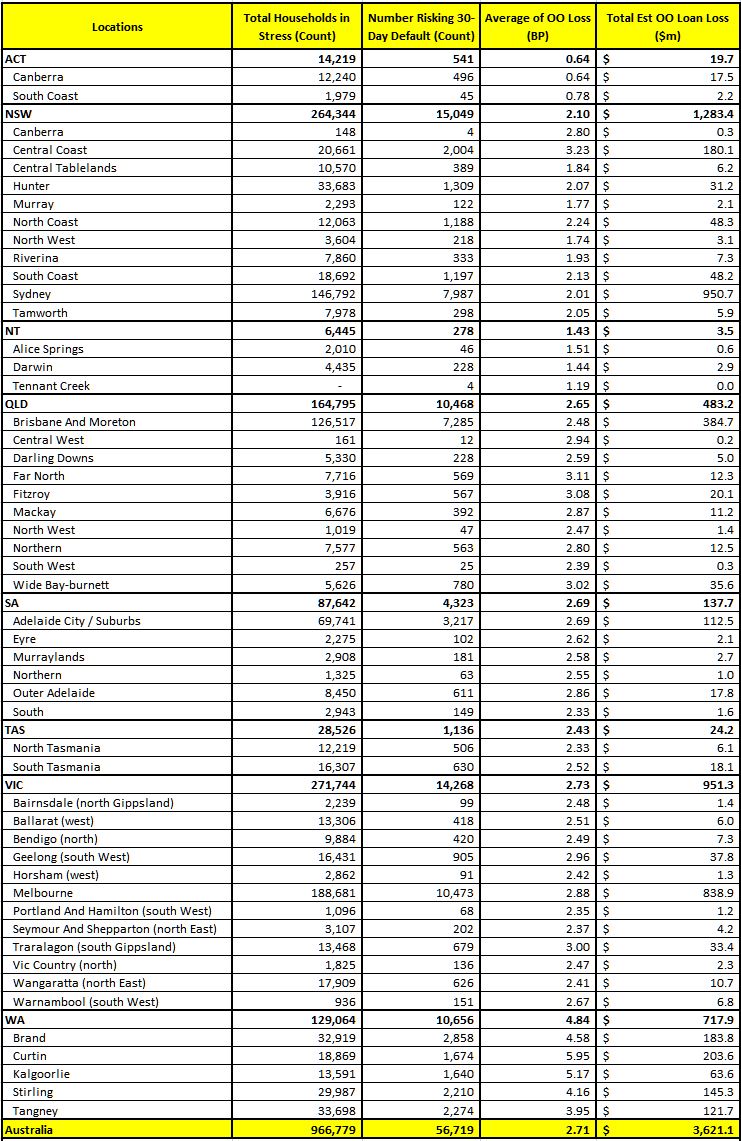

Households are defined as “stressed” when net income (or cash flow) does not cover ongoing costs. They may or may not have access to other available assets, and some have paid ahead, but households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell. Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes. Our Core Market Model also examines the potential of portfolio risk of loss in basis point and value terms. Losses are likely to be higher among more affluent households, contrary to the popular belief that affluent households are well protected. Regional analysis shows that NSW has 264,344 households in stress (262,577 last month), VIC 271,744 (256,353 last month), QLD 164,795 (175,960 last month) and WA has 129,064. The probability of default over the next 12 months rose, with around 10,656 in WA, around 10,468 in QLD, 14,268 in VIC and 15,049 in NSW. A fuller regional breakdown is set out below.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end May 2018. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end May 2018. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Stress by The Numbers.

Stress by The Numbers.

The largest financial losses relating to bank write-offs reside in NSW ($1.3 billion) from Owner Occupied borrowers) and VIC ($951 million) from Owner Occupied Borrowers, which equates to 2.10 and 2.73 basis points respectively. Losses are likely to be highest in WA at 5 basis points, which equates to $718 million from Owner Occupied borrowers.

The largest financial losses relating to bank write-offs reside in NSW ($1.3 billion) from Owner Occupied borrowers) and VIC ($951 million) from Owner Occupied Borrowers, which equates to 2.10 and 2.73 basis points respectively. Losses are likely to be highest in WA at 5 basis points, which equates to $718 million from Owner Occupied borrowers.

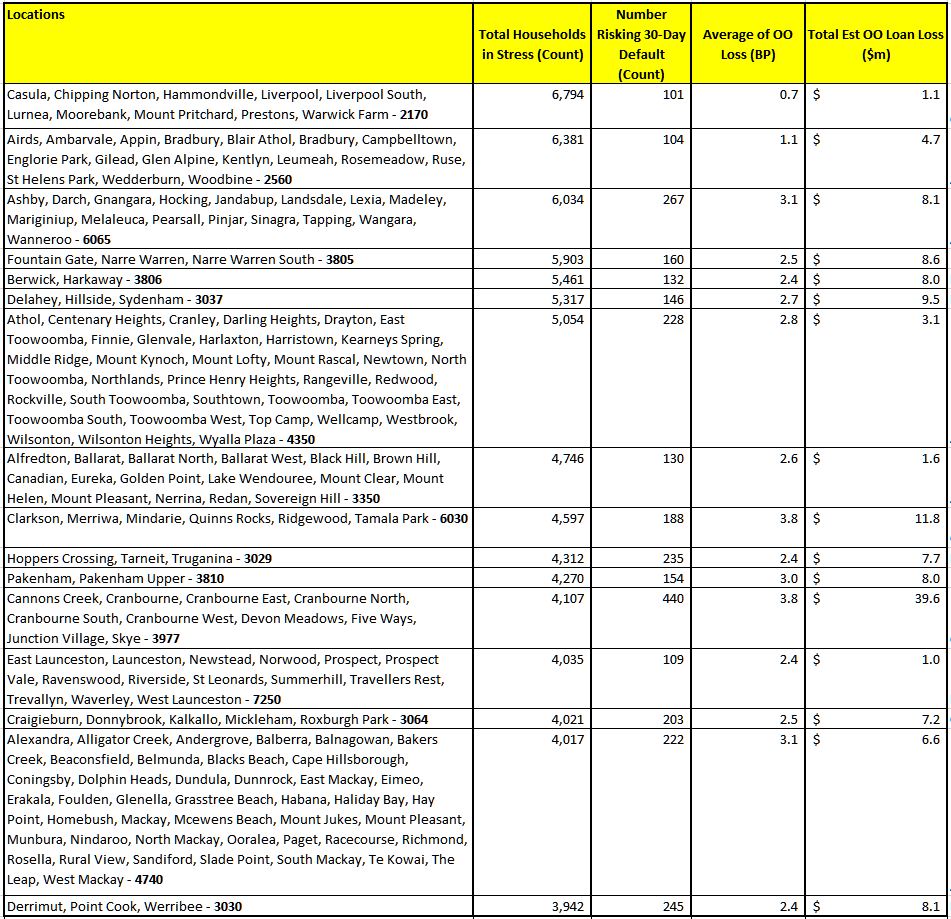

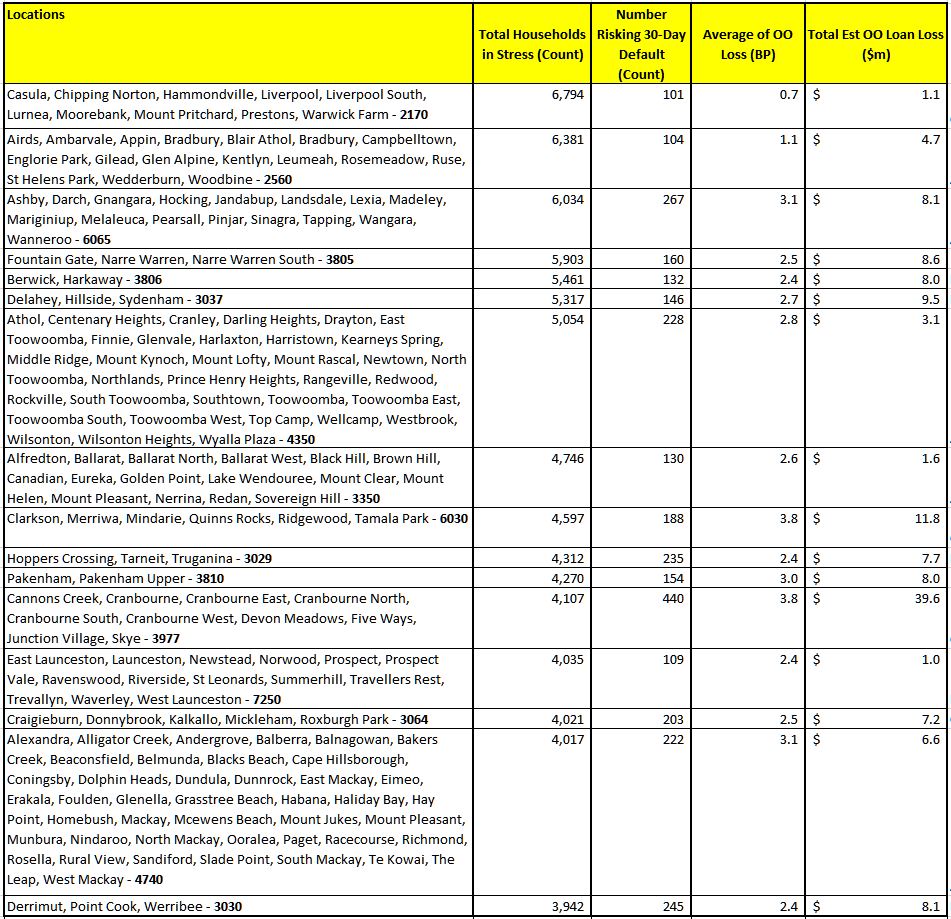

Here are the top 20 postcodes sorted by number of households in mortgage stress.

Here are the top 20 postcodes sorted by number of households in mortgage stress.