An estimated 18 per cent of mortgage customers have a debt-to-income (DTI) ratio that is above six times, an analysis of 1836 mortgagors shows, which is unacceptable when seen through the lens of new lending rules.

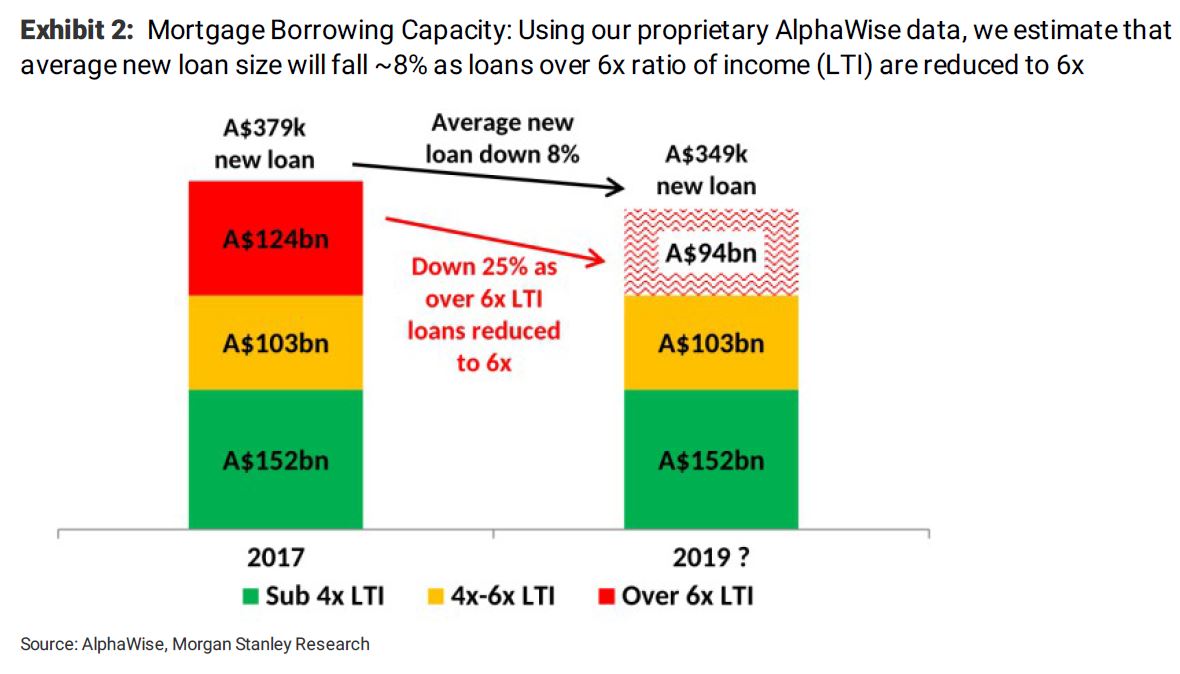

A correction of the “very high” debt-to-income segment of the mortgage market could pull average new loan sizes noticeably lower.

Morgan Stanley’s analysis estimates the median loan-to-income ratio is 3½ times, about 40 per cent of mortgage holders have a loan-to-income ratio of over four times, and 18 per cent are in the “very high” category of over six times.

The analysts have halved their housing loan growth forecast to 2 per cent for fiscal 2019 and 2020, and see “risks to the downside”.

We’ve never seen that level of mortgage credit growth in Australia. The lowest it has ever been is 4.4% in mid-2013. Levels of mortgage credit growth at 2% or below will be associated with 5-10% per annum house price falls. As UBS says:

Debt-To-Income limits – a new macroprudential tightening tool – is set to come

In April APRA instructed lenders to renew their focus on embedding sound residential mortgage lending practices. One of the key elements of this was a need for the banks to develop internal risk appetite limits on the proportion of new lending at “very high DTI levels” >6x, and policy limits on maximum DTI. This is consistent with international trends restricting consumer leverage in a low interest rate environment.

Strict limits on ‘very high’ DTI (>6x) lending are likely to be adopted

We believe APRA may be comfortable with limits on ‘very high’ DTI lending (>6x) being set at a low ~5-10% of flow. However, a number of difficulties remain: (1) The definition of income and debt: (a) does debt include car leases, undrawn credit cards, student debt etc; (b) Treatment of SMEs where a mortgage is used for security; (c) treatment of SME income as personal vs business; (d) trusts; (2) Until Comprehensive Credit Reporting is fully adopted – proposed to become mandatory for the Majors from 1 July 2018 and fully adopted from 1 July 2019 – the banks may not have a complete view of their customers’ financial position preventing an accurate estimate of the DTI.

HILDA data suggests (at least) 1/3 of the debt held by households with >6x DTI

RBA analysis of the HILDA data from 2014 showed that while only 5% of Australian households (by number) have DTI >6x, these households hold (at least) 1/3 of the outstanding debt. However, given HILDA is based on the outstanding debt rather than flow, new borrowing in recent years would likely have been even more concentrated.

Combining Responsible Lending with DTI limits would further constrain credit

With the Royal Commission placing pressure on the banks to take reasonable steps to verify customer’s financial positions (e.g. review transaction accounts & credit cards to verify expenses) borrowing capacities are being reduced (up to 30-40%) and credit conditions are still tightening sharply. The adoption on DTI limits provides a further restriction and may become a binding constraint for customers who have very low assumed living expenses or purchased multiple investment properties. Finally the sustainability of Sydney house prices at >9x median income and Melbourne at ~8x median income become problematic when borrowing limits are restricted to 6x income.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.