It’s over and the MB Fund won. The “bond kings” Jeff Gundlach and Bill Gross have been vanquished. How did the MB fund do it?

First, recall that Jeff Gundlach has been for the past six months telling everyone to buy emerging markets and commodities. Second, Bill Gross has been telling everyone to bet on a narrowing yield spread between US and European debt. We’ve been challenging these views throughout.

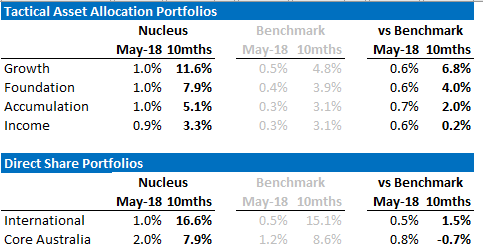

After last night’s dovish ECB meet, both bond king trades are now disastrous as the US dollar and US yield spreads fly. Conversely, MB Fund positioning is caning it with the international stock fund up 20%, tactical growth up over 13% in ten and half months. And this with heavy hedging to protect any downside.

How did we do it? There are lots of reasons but four stick out, coming under the banner of macro principle meets market narrative and investment process:

- First, it was obvious that Europe would slow this year for one main reason. The EUR had already rallied enough to deliver a 25% real exchange rate shock in just one year. After the debt crisis, the Eurozone is a Teutonic externally driven economy. It can’t take that kind of shock. There was also the Italian election to worry about which was always going to be problematic at some point and likely to weigh on growth.

- Second, as markets turned irrationally bullish over European prospects based upon the “global synchronised growth” narrative and a renewed hope for inflation, our underlying model told us that secular stagnation is fully intact. This meant that those traders that were worrying about inflation and therefore external imbalances, such as those that fled the USD and embraced EUR, we’re betting on a passing fad. Markets were always going to return to the search for growth soon enough.

- Third, we knew that Chinese growth was going to slow. The leading indicator of credit is very clear. If you add a strong USD then wider emerging markets are going to slow too as capital outflow tightens credit. This has started to play out now and will get much worse ahead.

- Fourth, these views were constantly challenged and debated in real time on the blog as data and new arguments flowed in.

Am I blowing the MB Fund trumpet? Yes. But worry not that this is arrogance. Investment is hard and we know we’ll win some and lose some. I’m only claiming round one in an endless boxing match.

My main point is that the investment process that has evolved at MB is keeping our thinking on the cutting edge to the benefit of all of our asset allocation decisions and, moreover, it can compete with and beat the world’s best.

David Llewellyn-Smith is the chief strategist at the MB Fund which is overweight US equities. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

If these themes interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.