Suddenly, Straya’s army of property ponzi-borrowers can’t refinance

Here comes the interest-only crunch, via AFR:

Mortgage brokers, who act as intermediaries between lenders and borrowers, claim lenders are “throttling back” amid increased pressure from regulators and fear of exposure by the Hayne royal commission.

“Lenders are making sure they dot every ‘i’ and cross every ‘t’ from borrowers and putting the ruler across every broker application,” said Steve Mickenbecker, group executive for financial services at Canstar, which monitors rates and charges for financial service products.

In addition, many lenders are switching from a ratio of loan to income, which measured their debt as a percentage of disposable income, to the more rigorous loan to debt, which monitors debt from all sources, such as credit cards and school fees.

Martin North, principal of Digital Finance Analytics, an independent consultancy, said the number of troubled households seeking to refinance has increased from about 15 per cent to nearly one-third of refinancing borrowers.

Much of this is interest-only borrowers seeking to roll over their ponzi-finance. Recall the definitions of Hyman Minsky:

Minsky argued that a key mechanism that pushes an economy towards a crisis is the accumulation of debt by the non-government sector. He identified three types of borrowers that contribute to the accumulation of insolvent debt: hedge borrowers, speculative borrowers, and Ponzi borrowers.

The “hedge borrower” can make debt payments (covering interest and principal) from current cash flows from investments. For the “speculative borrower”, the cash flow from investments can service the debt, i.e., cover the interest due, but the borrower must regularly roll over, or re-borrow, the principal. The “Ponzi borrower” borrows based on the belief that the appreciation of the value of the asset will be sufficient to refinance the debt but could not make sufficient payments on interest or principal with the cash flow from investments; only the appreciating asset value can keep the Ponzi borrower afloat.

If the use of Ponzi finance is general enough in the financial system, then the inevitable disillusionment of the Ponzi borrower can cause the system to seize up: when the bubble pops, i.e., when the asset prices stop increasing, the speculative borrower can no longer refinance (roll over) the principal even if able to cover interest payments. As with a line of dominoes, collapse of the speculative borrowers can then bring down even hedge borrowers, who are unable to find loans despite the apparent soundness of the underlying investments.

That’s where we are today.

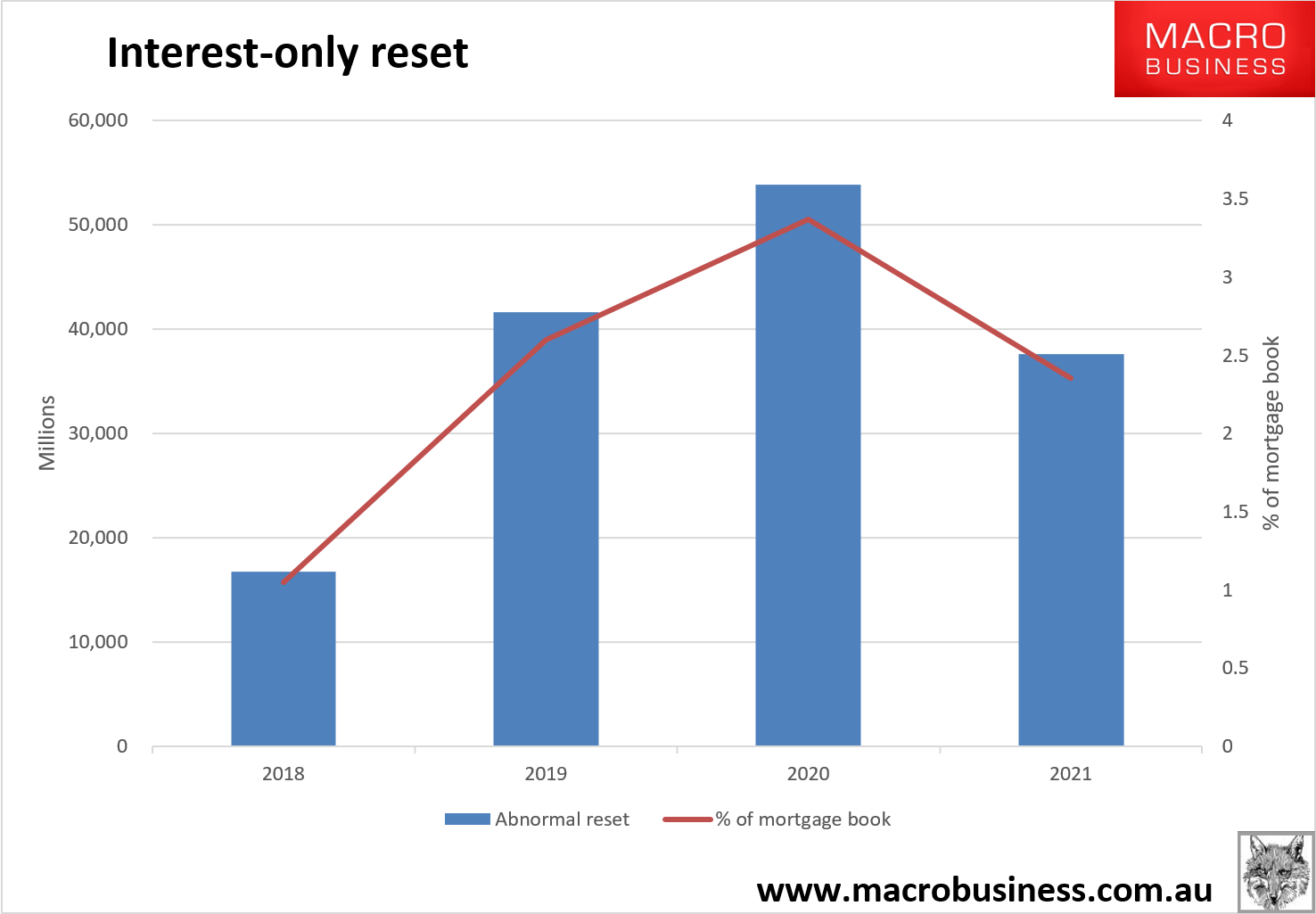

There is confusion about how much the bank’s back book and front book can absorb the rollover. Banks can only issue 30% of new loans as interest-only now. That’s roughly $40bn per quarter which would mean that the reset could absorb the bank’s entire front book IO capacity. So some large portion will have to transpire in the back book. My best guess how much that will be based upon the history of what the banks have managed previously, I’ve guessed they will be able to manage $25bn per quarter in the back book as the great reset builds. That means we’ll see the following total resets to principle and interest:

At the peak, that’s 3-4% of the loan book being shocked by 40% repayment hikes. That’s easily enough ponzi-finance to destabilise the entire system as forced sales push down prices.