Housing finance approvals data came in well below expectations in March. Owner-occupier loans fell by 1.9% over the month, while investor loans fell by 9%.

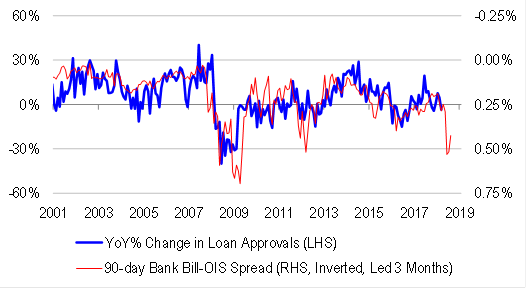

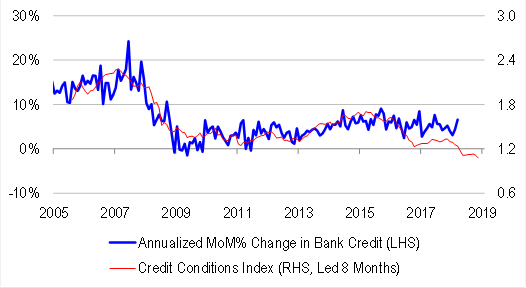

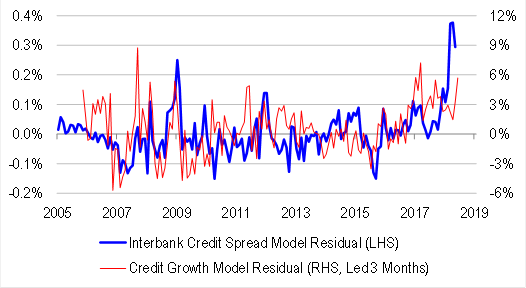

We do not yet have detailed data on business and personal loan approvals. But if we assume that these were flat over the month, total loan approvals would have started to fall in the year-to-March. This is broadly consistent with the tightening of credit conditions we have seen, in part due to macro-prudential regulation, but in part due to market developments. As highlighted in recent articles, we have seen an unusual degree of money market tightening of late, because interbank credit spreads have widened much further than fundamentals (credit default swap spreads, yield curve, stock market volatility and housing sentiment) can explain.

If historical relationships are anything to go by, we should expect to see more weakness in loan approvals in the near-term. Indeed, in the aftermath of the Bank Royal Commission, lending standards are likely to have tightened further.

If loan approvals continue falling, all other things being equal, credit growth should slow further. But all other things are not equal. Credit growth equals loan approvals net of re-financing and re-draws and re-payments. It is possible that net re-repayment activity could weaken, in keeping with recent trends, if households draw down on their pre-payment buffers. This would be a sign of rising mortgage stress, even if bad debts are not an immediate problem.

Investment implications

Our concern is that regardless of which way credit growth goes, there are problems to be reckoned with:

1. If credit growth slows, more work needs to be done by policy makers to stimulate money and credit creation. Otherwise, hard landing risks start to rise.

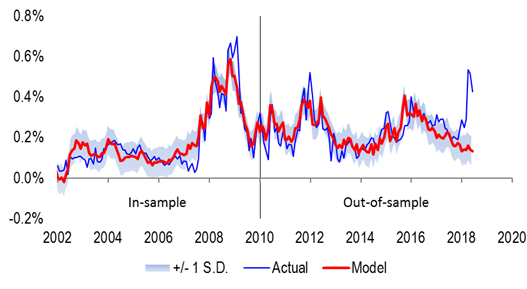

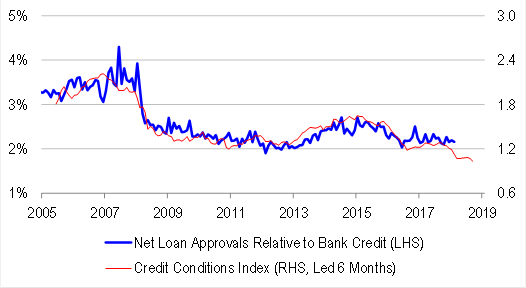

2. On the other hand, if credit growth remains robust, or even picks up further, it is largely a symptom of falling net repayment activity and increasing mortgage stress. We would expect investors to respond to this negatively, and bank funding costs could well rise, or at least, remain elevated. Indeed, historically, the excess of credit growth relative to our credit conditions index (a proxy for bank lending standards), has been a good leading indicator of interbank credit spreads. In recent times, credit growth has been running materially ahead of the credit conditions index, because banks have been able to relax un-reported lending standards. This has led to concerns about excessive debt build up and credit risk, which are now starting to filter through into bank funding costs.

Our suspicion is that in the wake of the Bank Royal Commission, lending standards are starting to tighten to where they should have been a few years ago, shortly after macro-prudential regulation was introduced. Therefore, loan approvals are likely to fall further, negatively impacting credit growth. However, we do not know which way net repayment activity is likely to go.

We think that the data and market developments support the view that de-leveraging risks are material. And in de-leveraging episodes, naïve value investing tends not to work, because asset prices drive earnings, dividends and book values, rather than the other way around. Our preferred way of picking stocks is to use quality.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.