EUR sank Friday night and DXY hit new highs:

Hilariously, the market remains spectacularly long EUR meaning much more selling pressure ahead:

AUD was soft against the tearaway USD:

But not as soft as EMs:

AUD CFTC shorts pulled back a touch to -23k:

Gold held on and may have found a friend in Italexit:

Oil was crushed as OPEC freed supply:

And the US rig count jumped 15 to 859:

Base metals held on for no apparent reason:

Big miners did not:

EM stocks were OK:

And junk:

Treasuries were bid bigly:

And bunds:

As Italian debt puked:

Stocks held on:

Markets have put the proverbial gun to Italy’s head, via Reuters:

A new government is expected to take office in Italy next week, a coalition of the anti-establishment 5-Star Movement and far-right League, who have jointly promised a bonanza of tax cuts and spending increases that would burst through the EU’s limits on borrowing by member states.

Slovak Finance Minister Peter Kazimir on Thursday called the policy mix a “suicide mission”. Markets have already responded: yields of the benchmark 10-year Italian bonds have jumped 0.7 percentage point since the start of May to 14-month highs above 2.46 percent.

Morgan Stanley warned this week that sustained yields that high could spark contagion by hitting the profits of banks which hold a big chunk of their assets in government debt. Shares in Italian banks hit 11-month lows on Friday, having fallen almost 14 percent so far this month. Economists say that is only a taste of what could come: the rise in rates would be much steeper if markets believed that Italy was actually prepared to go through with the plans.

“If they do what said they want to do, the reaction of the market will be much more than what we have seen so far,” said Francesco Papadia, a senior fellow at the respected Brussels-based Bruegel think-tank.

…As an EU member, Italy is obliged seek a balanced budget in structural terms and have debt below 60 percent of gross domestic product. Instead, its structural deficit has been rising since 2015 and its debt has been close to 132 percent of GDP since 2014. But most Brussels-watchers do not expect Europe to take political action to enforce its rules.

The European Commission, the guardian of EU laws, has the task of disciplining profligate governments through what is called an excessive deficit procedure that could end in fines.

But it has repeatedly declared that punishment is not the way to deal with budget rule-breaking, and showed leniency to repeat budget offenders like France, Portugal and Spain.

The Commission is also held back by concern that enforcement action would only strengthen eurosceptic sentiment in Italy, the euro zone’s third biggest economy, where many people are already ambivalent about the euro currency.

“In the end, crazy countries are always disciplined by markets. Rules can be broken. But you cannot replace market funding with wishful thinking,” one senior euro zone policy-maker said, expressing a widely-shared view.

League leader Matteo Salvini brushed off market pressure.

“The more they insult us, the more they threaten us, the more they blackmail us, the more desire I have to embark on this challenge,” he said.

But analysts point out that only 36 percent of Italy’s massive 2.4 trillion euro debt is held by foreigners, meaning a fall in asset prices would hit Italians hard.

The rest is held domestically by banks, funds, investment vehicles and individuals, who now benefit from demand created by a European Central Bank bond-buying program.

The ECB scheme is likely to wind down this year and rate hikes are expected in mid 2019. Faced with profligate policies that undermine Italy’s ability to repay debt, foreign investors are likely to sell Italian paper. As yields rise, Italian voters would quickly see the value of their assets shrink.

“In Italy, quite a percentage of bonds is held by families directly. So when people see the statements from their banks on the value of their financial wealth, their savings, they would see the consequences,” Papadia said.

Another factor likely to limit the Italian government’s fiscal plans is the threat of a credit rating downgrade. Italy is now just two notches above junk with a BB from Standard & Poor’s and Fitch, and Baa2 from Moody’s. Fitch has already said the plans outlined in the coalition agreement would add risk to Italy’s fiscal position.

If Italian debt were to fall below investment grade, its banks would find it much more difficult and costly to get daily liquidity from the ECB — a constraint that could have serious consequences for the whole sector and the country.

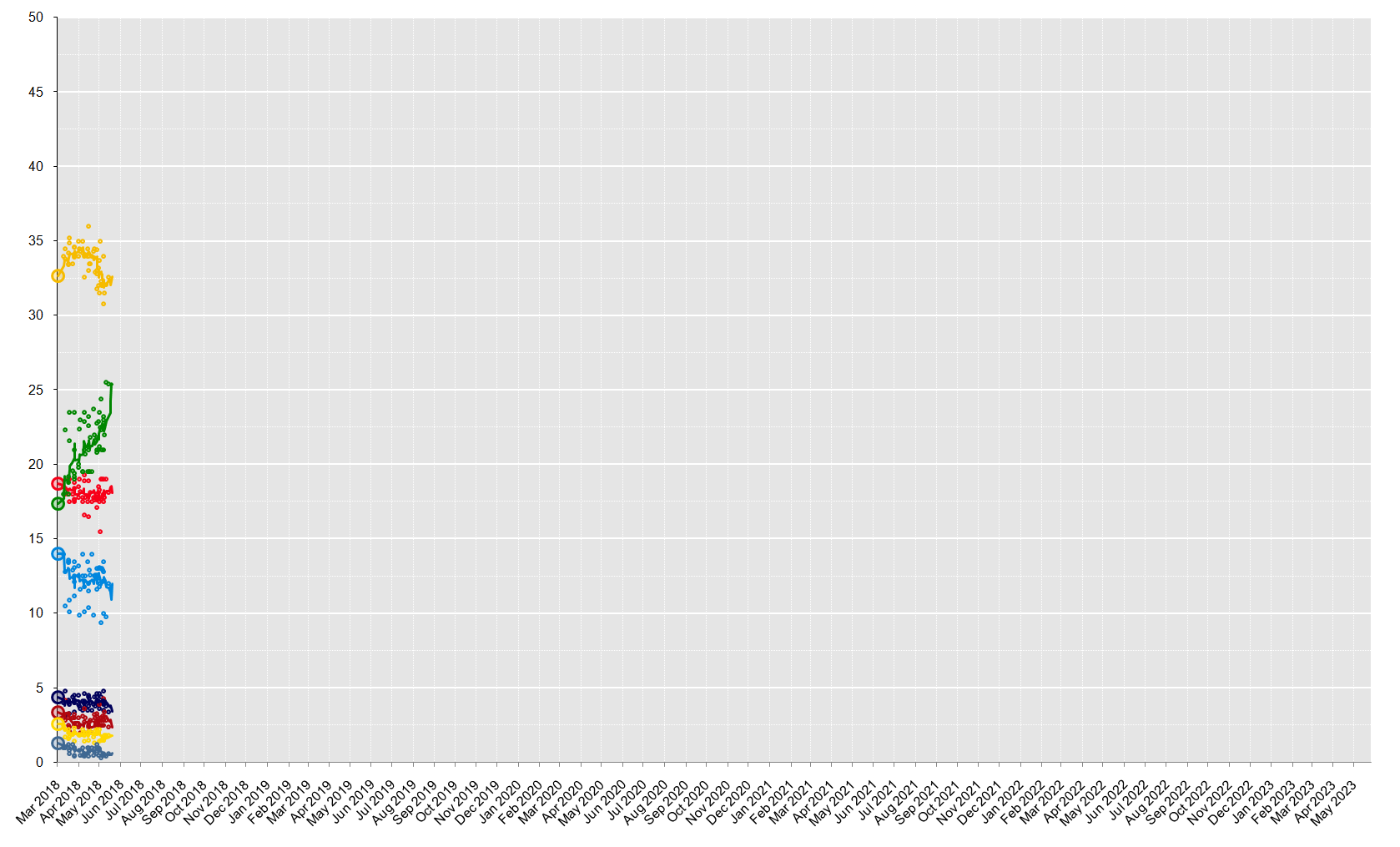

The latest opinion polling looks headed for landslide support behind the populist Coalition (green and yellow):

This will embolden MS5 and the League to push forward its radical fiscal agenda. Markets will sell Italian bonds and try to break the government. It will either fold or issue its mini-BOT to local creditors, also via Reuters:

One of the most radical proposals in the programme of Italy’s anti-establishment coalition is to issue securities to pay off individuals and companies who are owed money by the state as payment for services or as tax rebates.

Following are some questions and answers about the so-called “mini-BOTs”, named after Italy’s short-term Treasury bills.

The Treasury would print billions of euros of non-interest-bearing, tradeable securities which could then be used by recipients to pay taxes and buy any services or goods provided by the state, including, for example, petrol at stations run by state-controlled oil company ENI.

According to Claudio Borghi, the economics chief of the far-right League, who is the main proponent of the scheme, the certificates would quickly become accepted more widely and used as a form of money to be “spent anywhere, to buy anything.”

Initially they would be used only domestically and would not be traded on international financial markets.

The programme says “something must be done to resolve the problem of the public administration debts to taxpayers.” It says the solution could be “the securitisation of tax credits, through instruments such as small-denomination state bonds.”

In order that these not be classified as additional public debt, it calls for “a redefinition of statistical indicators at the European level,” and “a reassessment of the definition of public debt.”

The League and its coalition partner, the anti-establishment 5-Star Movement, both have a history of euroscepticism, though their programme contains nothing that calls into question Italy’s membership of the single currency.

Critics see the mini-BOTs as a way of issuing a parallel currency with the aim of allowing Italy’s economy to continue to function if it leaves the euro zone.

Borghi is openly hostile to the euro and says it is only a matter of time before it collapses. Italy’s outgoing economy minister Pier Carlo Padoan last year called mini-BOTs “a plan to circulate a disguised parallel currency”.

Lorenzo Codogno, head of LC Macro Advisors and a former Italian Treasury chief economist, said the scheme would “increase both the budget deficit and the debt.”

“It would signal that Italy wants to issue a parallel currency to prepare a euro exit, which the real objective of the League,” he added.

There’s a feedback loop here. The more the mini-BOT is issued, the more markets will fear the exit and pull back from Italian debt, requiring ever greater quantities of mini-BOT. So and so forth until Italy simply slides out of zone and mini-Bot is renamed Lira 2.0. It then crashes precipitating default on external debt.

Peterson Institute has a good wrap of scenarios:

Earlier PIIE research examined whether rising interest rates might unleash a debt crisis in Italy. The answer was “no,” under two conditions: First, that rising interest rates reflected economic recovery; and second, that the Italian government would be prepared to cooperate with European authorities—the European Union, the European Stability Mechanism (ESM) and the European Central Bank (ECB)—to manage a loss of market confidence.

Ten months later, these conditions no longer hold. Political backlash to slow growth and immigration has produced the least cooperative government imaginable, a coalition between the left-populist Five Star Movement (M5S) and the right-populist Lega. And borrowing costs have started to rise in reaction. Does this mean that a crisis is imminent? If so, how bad would it be?

HOW BAD WOULD A DEBT CRISIS BE?

The second question is easier to answer than the first. A crisis could be horrific, for two reasons. First, none of the powerful stabilization instruments that the euro area has developed over the years could be deployed to rescue Italy. Following crisis-related downgrades, Italy would no longer be eligible for the ECB’s quantitative easing bond-purchasing program. The ECB would stop accepting Italian bonds as collateral. Access to emergency support programs—the ESM, and through it, the Outright Monetary Transactions (OMT) program—would be conditional on fiscal adjustment, the opposite of what Italy’s new government has promised. Unless the government were to change course, it would be forced to exit the euro, even if this is not its current plan.

And second, there is Italy’s interconnectedness and size. With the ECB using all available tools to limit contagion, the euro might survive Italexit. But an exit would nonetheless put Italy, the euro area economy, and the European Union in deep distress. With credit, investment, and consumer confidence collapsing, Italy would enter a deep recession. Redenominating assets and liabilities of Italian corporates and banking would trigger bankruptcies and legal conflict. The resulting acrimony—both within the country and across Europe—would dwarf what was witnessed during the 2010–12 crisis. If Italy also exits the European Union, a massive trade shock would aggravate the financial crisis and recession in Italy and Europe at large.

THE COALITION’S FISCAL PLANS: RECIPE FOR A DEBT CRISIS

How likely is such a scenario? To answer this question, one needs to take a closer look at the incentives facing the incoming coalition government. To succeed in the next election, the two parties will want to deliver on their major promises. Are the promises featured in the M5S-League contract compatible with a scenario in which Italy (and Europe) do not end up facing a debt crisis? And what might happen if they are not?

M5S and League’s electoral promises are both centered on a more expansionary fiscal stance, although with major differences. M5S promised the introduction of a minimum guaranteed income—which appealed to voters in the economically suffering south. The League party promised a flat tax—which appealed to voters in the economically thriving north. Both parties advocated the repeal of a controversial pension reform introduced in 2011 by the government of former prime minister Mario Monti. The government contract between the two parties features all three promises. Moreover, both parties have committed to repeal an otherwise automatic hike in the value-added tax (VAT) planned in the 2018 budget.

How much would this largesse cost, and how might it be financed? Repealing the VAT hike would require €12.5 billion. As for the other promises, Carlo Cottarelli at the Osservatorio Conti Pubblici Italiani estimates that the League’s flat tax would cost around €50 billion, while M5S’ guaranteed income would cost about €17 billion. Scrapping the Monti government’s pension reform would add a further €8 billion. Counting in some of the minor promises, the total would reach a whopping €109-126 billion (6 to 7 percent of GDP).

The government contract is vague on how these measures would be funded. With respect to M5S’ minimum guaranteed income, it suggests that part of the cost could be covered with resources from the European Social Fund, but whether this would be possible, and to what extent, remains unclear. Both the contract and the original center-right program also mention the intention to eliminate deductions and lower tax expenditures, but provide no detail. At the same time, it is worth recalling that the original center-right program was the expression of a three-party coalition with different views about the appropriate path for public finance. The League’s economic projections included a much larger recourse to deficit financing than the center-right party Forza Italia’s projections did. The League broke away from this coalition to pursue the alliance with M5S. Without the restraining influence of Forza Italia, it may decide to follow through with its initial intentions.

As a result, the makeup of the incoming coalition, and its contract for governing, make it difficult to imagine a course of policy that would not put it on collision course with financial markets and the European Union. The magnitude of the increase in the deficit implied by the combined measures will likely violate all EU and domestic fiscal rules and put debt on an unsustainable trajectory. Furthermore, the possibility that the government may use “mini-BOTs”—tradable government securities for settling arrears, potentially creating a homegrown source of monetary financing inside the currency union—is deeply worrisome. Schemes of this type have been tried, and failed, in emerging-market crises. Markets may see them as the first step towards the reintroduction of a national currency—and they may well be right.

GOVERNMENT NOT LIKELY TO CORRECT COURSE BEFORE A DEBT CRISIS ESCALATES—BUT ITALEXIT ALSO NOT LIKELY

Could one imagine the government program being implemented on a much-reduced scale, one that would avoid violating fiscal rules and risking debt sustainability? Perhaps. But given the lack of identified funding, this seems possible only if one of the coalition parties is prepared to significantly water down, or at least delay, its signature promises. This is what makes the current situation so worrisome. Any trajectory that avoids a collision would seem to require a climb-down by the League, M5S, or both, and this is not likely to happen voluntarily.

As a result, a scenario in which the government corrects course before the situation escalates appears unlikely. A scenario in which Italy loses market access—perhaps triggered by a downgrade—followed by an unsuccessful negotiation attempt with European authorities and Italexit, certainly looks possible. But it remains unlikely, for several reasons.

First, the government may eventually blink. A full-fledged crisis would hurt Italy at least as much as the rest of Europe. The Italian financial system is still fragile, and many banks are heavily exposed to government bonds. Two-thirds of Italian sovereign bonds are owned by residents. Hence, an across-the-board debt crisis is not a tool that an Italian government—even one that wishes to defy its international partners—can easily use to lower its debt at the expense of foreigners. A crisis leading to an Italian default would hurt mostly Italians, and so would its knock-on effects. It is hard to see how parties triggering such a crisis would not be punished in the next election.

Second, most of the policies that could bring Italy to the brink of crisis will be manifested in the revision of the 2018 or 2019 budget. These budgets need to be approved by both chambers of Parliament. The governing coalition’s majority in the upper one—the Senate—is slim: 6 votes. In the course of a sharp increase in borrowing costs triggered by an irresponsible budget (or its anticipation), that majority may well erode quickly.

Third, Article 81 of the Italian constitution introduces a balanced budget principle, and Article 97 states that general government entities, in accordance with EU law, shall ensure balanced budgets and the sustainability of public debt. A budget that too bluntly contravenes these rules could be deemed unconstitutional by the president of the Republic, who could refuse to sign it. This would clearly not be without costs—as it would start an institutional crisis and a phase of uncertainty—but it is possible.

As a result, one can imagine several scenarios in which escalating crisis conditions —rising borrowing costs, accelerating outflows—eventually induce a correction. Under heavy pressure from businesses and Italians who wish to remain in the euro (perhaps a slim majority, but a majority nonetheless, according to Eurobarometer), the Italian political system will at some point pull the emergency escape trigger. This could come in several forms. In the face of a crisis, the coalition may decide to postpone or heavily water down its signature fiscal plans. Or it may press ahead and trigger a confrontation with the president or lose its majority in the Senate. Or it may collapse because one of the two coalition partners does not want to join the other in jumping off the cliff.

Because one of the scenarios in this class is likely to come to pass, Italy’s membership in the euro area may live to see another day. A European catastrophe may be avoided. But the costs of doing so could still be high, both for the political and social cohesion in Italy and for the future of Europe.

The one thing that this analysis does not describe is what happens after Italy exits. The new lira craters and, although that results in external default, it also effects radical repair to Italian competitiveness. Not everybody loses. Indeed there are lot’s of winners. After a few years the economy can grow more swiftly and sustainably than within the zone. The Coalition might want to punt on that.

Now, this morning, the crisis has deepened, via Bloomberg:

Italy’s premier-designate Giuseppe Conte has given up on forming a populist government, raising the prospect of early elections after President Sergio Mattarella clashed with party leaders over the candidacy of a euroskeptic economist as finance minister.

Conte, 53, a law professor with no political experience, told reporters after meeting the head of state Sunday evening that he had handed back his mandate for forming “the government of change.” He added: “I can assure you that I did my utmost to try to fulfill this task.”

Mattarella, whose task it is to name the premier and ministers, earlier rejected the candidacy of economist Paolo Savona, 81, who has repeatedly urged the Italian government to plan for a euro-exit, and who has criticized what he says is German dominance over Europe.

Five Star leaders are discussing a possible attempt to seek Mattarella’s impeachment, invoking a constitutional clause which says the president is not responsible for actions carried out as part of his office, except for high treason or for violating the constitution, newswire Ansa said. Mattarella’s office declined to comment on the report.

As noted above, the Coalition parties are dominating polling. Another election will hand them an even stronger hand.

I am not going to pretend to know the outcome here. What can be observed is that:

- Italy is entering crisis and it’s going to take quite a while to sort it out;

- it is large enough to suck in the entire Eurozone and re-pose fundamental questions about the viability of EUR;

- yet markets are hilariously long EUR and ECB tightening;

- the USD is going keep rising and push the contagion into emerging markets;

- wholesale funding costs worldwide will begin to rise so here comes another blow to Aussie banks, and

- the AUD is going to keep falling.