Australian dollar rout pauses as global stocks roar

DXY was up again last night but well off the highs. It’s mirror image EUR was the reverse:

AUD finally caught a little bid against DMs:

It was mixed against EMs:

Gold held on again:

Oil is unhinged:

Base metals were stable:

Big miners surged despite the falling dirt/rising oil paradigm crushing their margins:

EM stocks tacked on a few pips:

But nothing can save EM junk and that’s your leading indicator for all things EM:

Treasury yields broke higher:

Not so bunds:

Stocks boomed:

Nomura wraps it nicely:

‘CYCLICAL MELT-UP’ THESIS IN REAL-TIME

- Peak “Cyclical Melt-Up” as my thesis continues to play-out in “real time” overnight: Crude +2.9% / new 3.5 yr highs, UST 10Y Nominal Yields back through 3.00+, 5Y “Real Yields” at new nine-year highs and Spooz at two-week highs

- “Hawkish” Iran deal decertification “event” perceived as the bullish catalyst needed for next leg of Crude rally, as upwards of 200-300k b/d of Iranian production potentially curtailed in an already “tight market” last night’s API inventory draw “beat” as additional ‘bullish’ confirmation into EIA later today

- I’ll say it again: Crude is “the straw that stirs the drink” ->Higher Crude = Higher “Inflation Expectations” = Long Equities “Cyclical Growth”(Energy / Financials / Materials) / Commods / TIPS, Short Fixed-Income / Defensives in this TACTICAL “melt-up” phase

- SPX factor model (per Quant-Insight) confirms this, showing that “inflation proxies” (Iron Ore, Copper, CRB Rind) and “inflation expectations” (both 5Y and 10Y zero coupon inflation swaps) are larger price drivers for U.S. stocks than global GDP growth, 1 year fwd earnings and VIX in the current SPX macro regime

- Additional potential catalyst for inflation? Chinese / PBoC liquidity-boost following the recent monpol “easing” (RRR cut) and fiscal stim (small biz tax cuts), with 7d repo rate making new 1 year lows (high interbank liquidity) and 1s10s Curve steepening to multi-year highs as a “tell” for higher Commodities

- And as a reminder, it’s not just inflation implications (PPI / CPI tomorrow) impacting Rates:

- Today sees a $25B 10Y auction which Darren Shames notes could print the first 3% coupon in nearly seven years

- Heavy seasonal U.S. IG calendar continues with $22B printed already WTD

- U.S. Dollar weakness overnight (predominantly vs G10 as EM still a mixed-bag) should also (near-term) help “hold” Commod gains

- However, the positive “tactical” U.S. Dollar “momentum” backed by 1) ongoing widening in Rates Differentials, 2) multi-year highs in U.S. “Real Yields” and 3) more disappointing global growth data overnight:

- EM data shows Philippine exports print their largest annual decline in 20 months

- Euro (~58% of DXY weighting) earlier new five-month lows overnight after French IP and Manu data weakness (currency has

- In turn, the legacy “long EURUSD” widely held by systematic trend-following CTAs since last year becomes further endangered for “capitulation risk” with likely “sell trigger” at 1.179

- EMFX and equities selloff moderates a touch after the Argentina / IMF credit line news y’day, although sovereign bonds still messy on foreign outflow concerns

- However, ‘Crude’-centric EMs offer some “relative” attraction (Russia, Mexico, Brazil) along with idiosyncratic ‘havens’ (South Korea) on geopol thawing

- USDCNH 6.43 level is another popular “short USD” trade to watch, as Nomura Quant Strategies Tokyo notes it as a potential “capitulation point” from CTAs in trade since late last year, ESPECIALLY as the PBoC cuts the daily reference rate for the Yuan for the 19th consecutive day and to the lowest level since Jan 24th.

I remain of the view that the next shoe to drop is softening Chinese growth which will hit the commodity trade across H2 and drive the AUD to new lows. That ought to ease the inflationary pressures everywhere outside of an overheating US. This is the MB “reverse decoupling” thesis that sees both a falling AUD and rising global stocks into a final global blow-off that has the US Fed tightening virtually by itself. The potential boom returns for Aussie investors allocated offshore in this scenario is what has kept the MB Fund long international equities (with a big cash hedge) throughout Q1 volatility.

Needless to say, we’re some way into it already and the fund is tearing the roof off.

—————————————

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

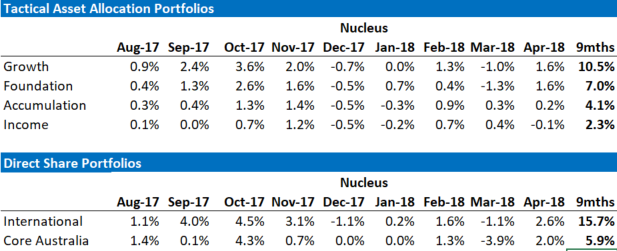

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.