AUD was soft, flirting with new lows before rebounding:

It was mixed against EM:

Gold is hanging in on geopolitics around Iran:

Advertisement

Oil broke to new highs on same:

That is holding base metals up for now:

And big miners:

Advertisement

But EM stocks are breaking:

As EM junk swan dives:

Treasuries were stable:

Advertisement

Bunds too:

Stocks rose:

Data was slim in the US and mostly weak in the Eurozone, made worse by the renewed prospects of an Italian election driven by the EUR-skeptic Five Star Party.

Advertisement

As the US dollar bull keeps running thanks to the dying EUR, the cycle more and more resembles some kind of rerun of the global macro dynamics that caused the great emerging markets (EM) panic of 2015 and a -25% crash in the Australian dollar. Especially so since China is going to slow in H2 this year. Recall that the 2015 panic was caused by:

a rising USD triggering EM capital outflow and rising interest rates;

a slowing China and falling CNY triggering an EM export crunch, and

tumbling commodity prices especially oil.

At this stage there are two key differences to 2015 that is preventing accelerating EM outflows from turning into an outright crisis. The first is played out in a Capital Economics note on the Chinese capital account today:

Advertisement

• China’s foreign exchange reserves continue to point to very little PBOC action in the FX markets, with muted capital outflows opening the door to renewed efforts to liberalise the capital account.

• The value of the reserves amounted to $3,125bn at the end of April, down $18bn from a month earlier (the Bloomberg median was $3,131bn and our forecast was $3,130bn). We won’t know for certain how much of this change reflects official intervention until the People’s Bank (PBOC) publishes its balance sheet data later this month. But, for what it’s worth, our model suggests that the decline is mostly due to valuation effects and that the PBOC probably largely refrained from intervention. (See Chart 1.)

• Given that the current account is almost certain to have returned to a healthy surplus in April, following a seasonal deficit in March, this would imply a sharp reversal in capital flows from net inflows to net outflows. (See Charts 2 & 3.) This is nothing to worry about, however. Such volatility in net cross-border flows is not uncommon at this time of year and net outflows look to have remained well within regulators’ comfort zone.

• Indeed, regulators have recently taken steps to loosen capital controls, including issuing new quotas on outbound portfolio investment via the QDII and RQDII schemes for the first time in two years late last month. PBOC governor Yi Gang has also pledged to further open up the capital account in the coming quarters and highlighted the fact that the central bank has largely remained on the side-lines of the FX market during the past year.

• These two trends seem likely to persist given our view that the US dollar won’t stage a major comeback anytime soon and that the renminbi will continue to appreciate against the dollar over the medium-term. (See Chart 4.) However, should outflows out of China jump and the renminbi come under pressure again, perhaps due to a sharp dollar rally or an abrupt domestic slowdown, it seems likely that the PBOC would resume large scale FX intervention and revert to tighter capital controls.

China is playing with serious fire here. As the USD rises, it is clear that EM outflows are accelerating fast. That will come to China as well, as we’ve already seen in the Hong Kong dollar crunch. Indeed, CNY has weakened sharply in recent days:

Advertisement

I expect China will be unable to liberalise the capital account, not least given a falling CNY will pour jet fuel all over the Trump trade war fire, but if it does so then look out AUD (and watch for support to Aussie realty).

The second key difference to the 2015 EM panic is oil. It is being supported by OPEC action and geopolitical tensions. While its price remains high then the external accounts of EM producers of oil (and dirt more widely) can be seen as somewhat protected and capital outflows be commensurately more contained.

Nonetheless, the rerun of 2015 dynamics is strong enough that AUD weakness is baked in.

Advertisement

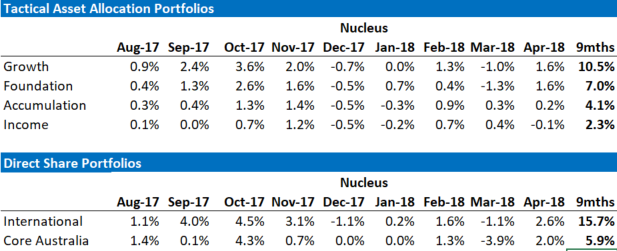

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

Advertisement

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.