Australian dollar free fall has only just begun

DXY was up Friday night as EUR sagged:

AUD versus DM held on:

But slipped versus EM:

Gold is still holding:

WTI broke out despite the rig count climbing again:

Base metals hung on:

Miners caught a bid:

EM stocks were positive but are in real trouble:

Led lower by EM junk which fell again:

As Treasury yields lifted and the curve flattened:

Bunds were bid:

And stocks flew:

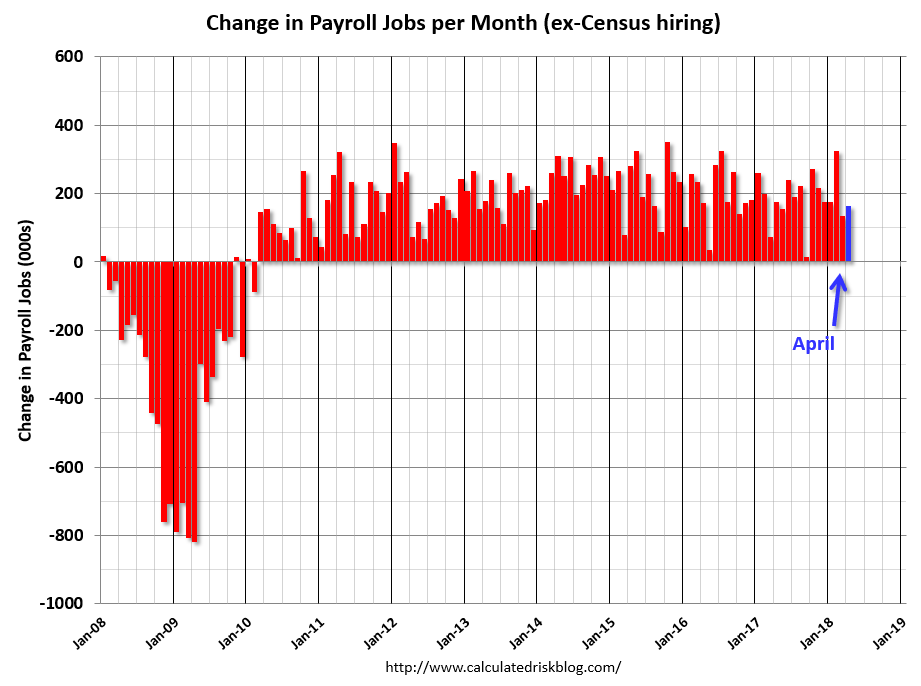

Goldilocks US jobs set everything except EM junk alight, via Calculated Risk:

Total nonfarm payroll employment increased by 164,000 in April, and the unemployment rate edged down to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in professional and business services, manufacturing, health care, and mining.

… The change in total nonfarm payroll employment for February was revised down from +326,000 to +324,000, and the change for March was revised up from +103,000 to +135,000. With these revisions, employment gains in February and March combined were 30,000 more than previously reported.

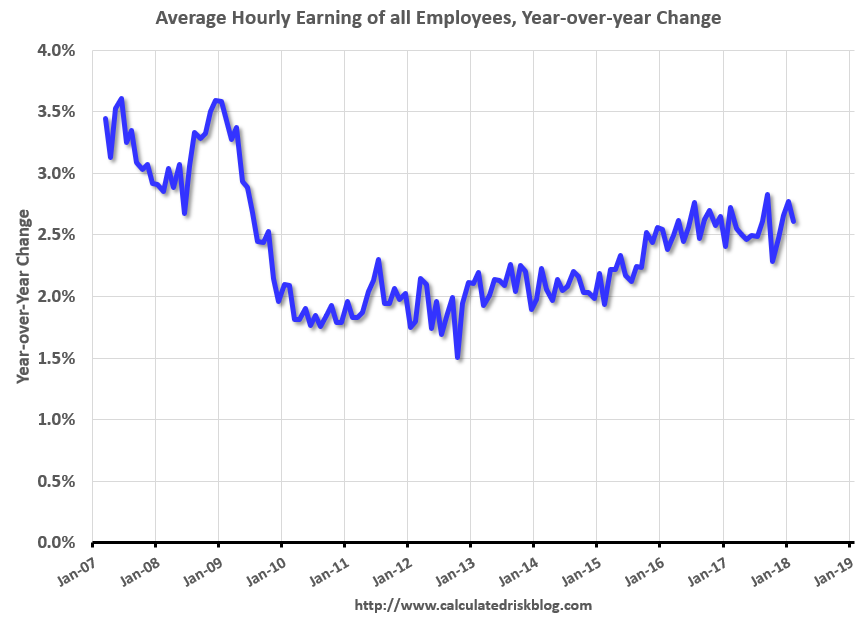

…In April, average hourly earnings for all employees on private nonfarm payrolls rose by 4 cents to $26.84. Over the year, average hourly earnings have increased by 67 cents, or 2.6 percent.

Read more at

Headline was solid:

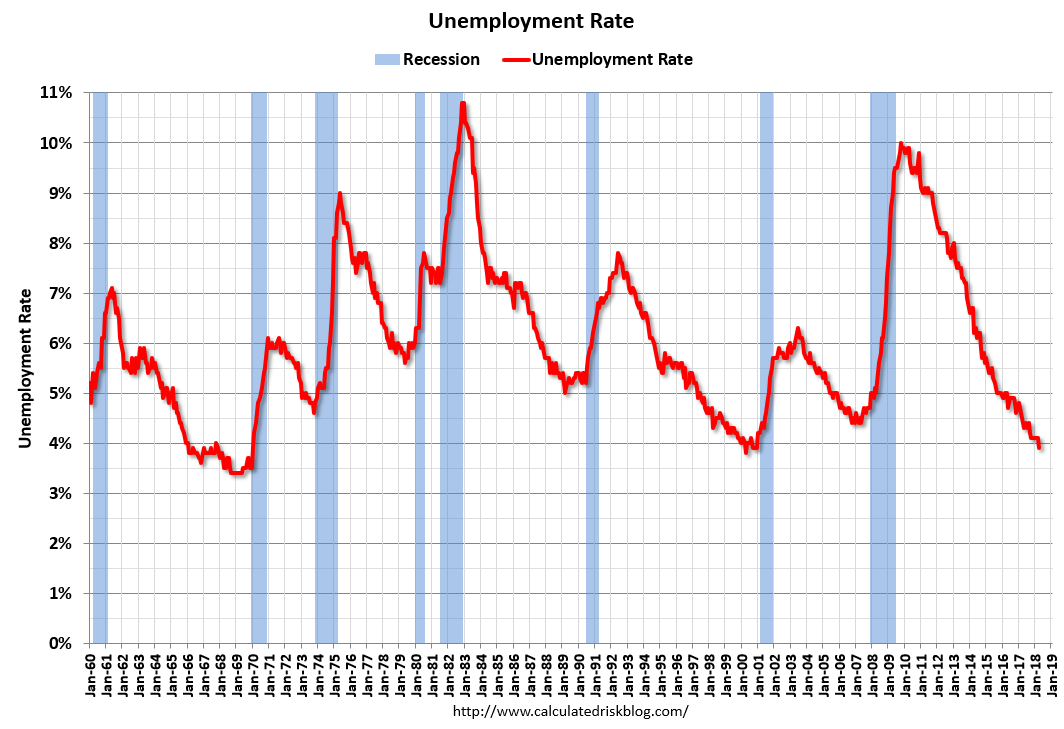

The UE rate plunged below 4%:

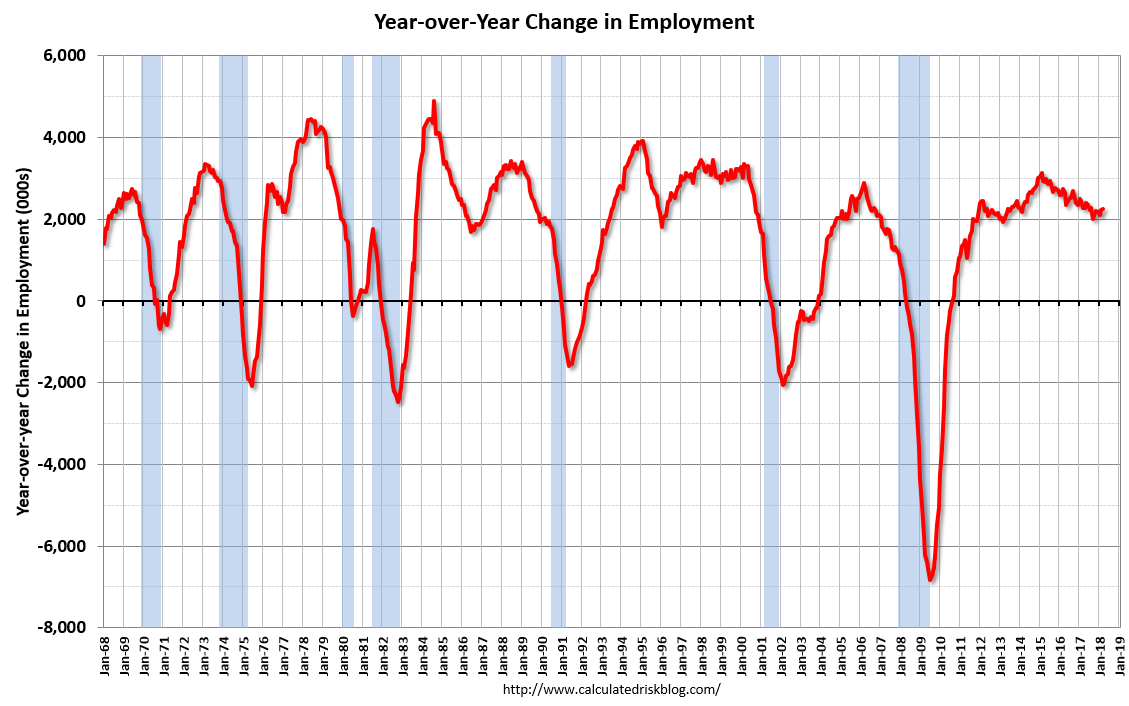

Year on year job growth is climbing again:

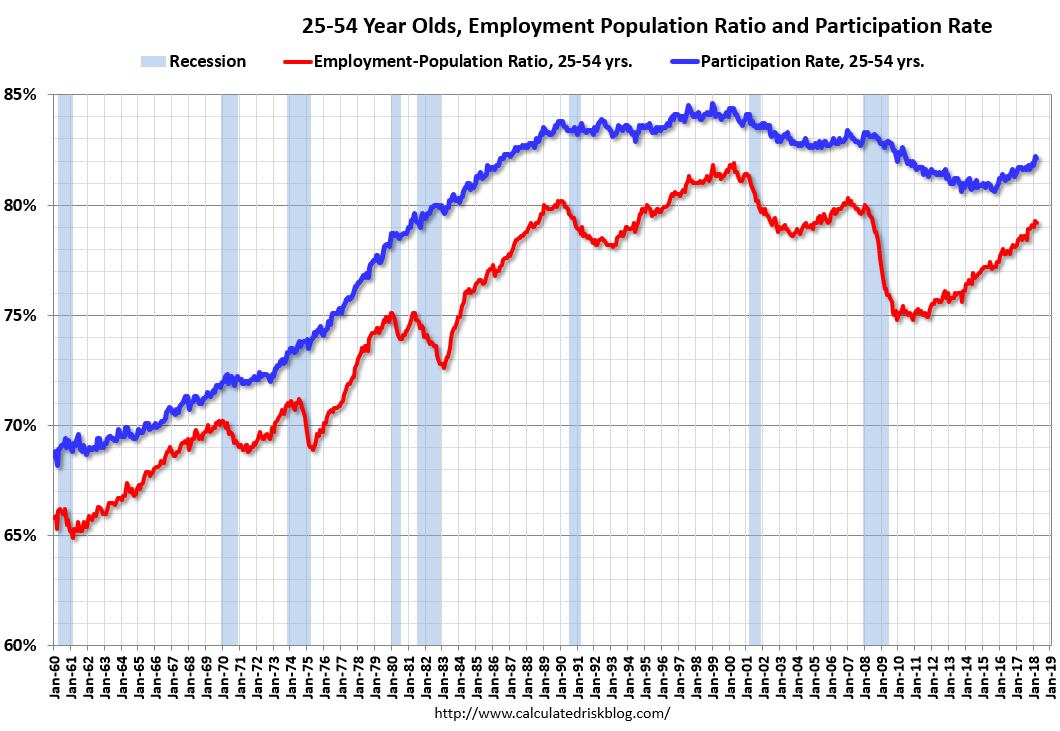

So are analytical measures:

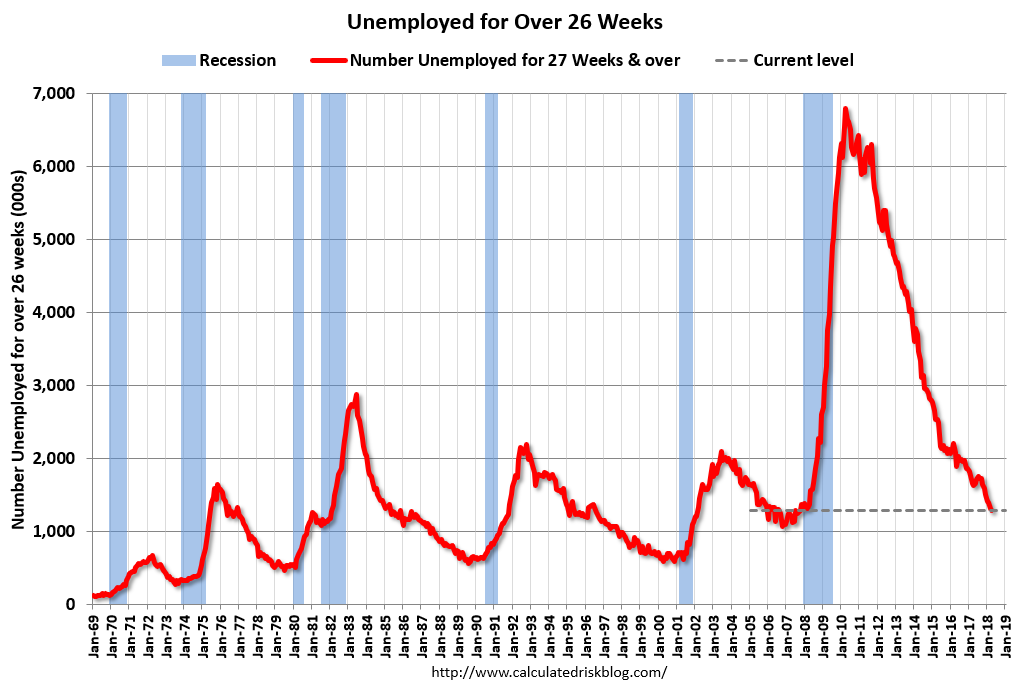

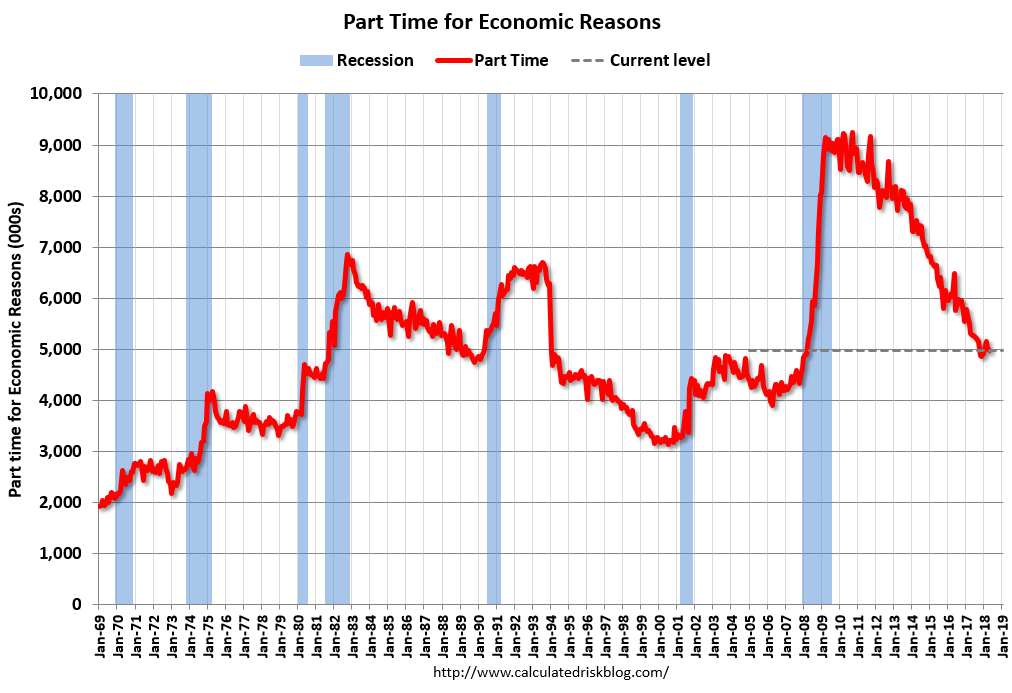

Shadow slack is falling:

But still abundant:

Wages growth is a balmy 2.6%:

Pure Goldilocks.

Which can be compared with Europe where the porridge has gone cold as the composite PMI rolls:

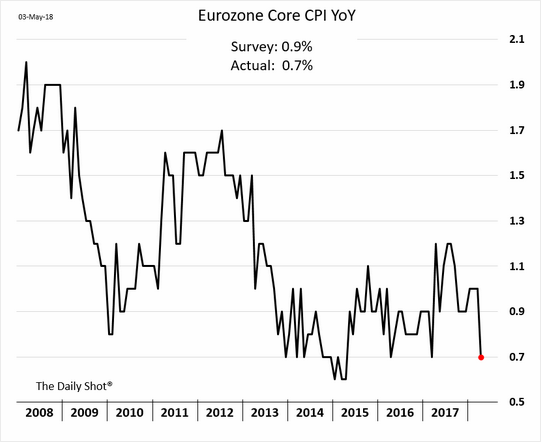

And Core CPI sinks:

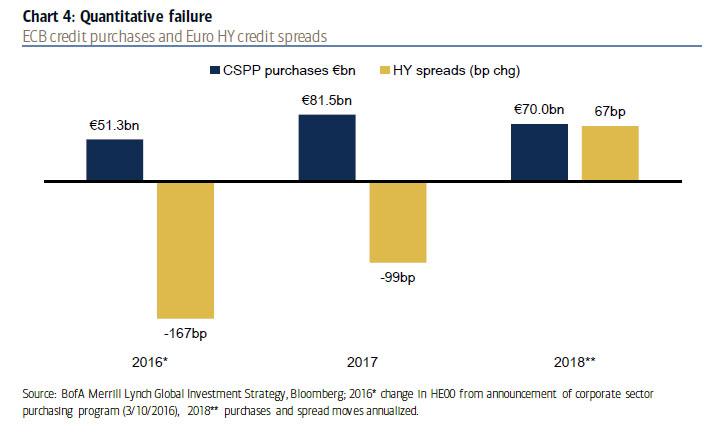

Plus peripheral spreads are blowing out despite the ECB not even reducing QE yet:

Yet the EUR long remains spectacularly, wonderfully long, ensuring puking of positions ahead and a rising DXY:

Which will slam EMs, commodities and AUD lower. And that’s before the H2 China slowing!

I can now see the AUD falling non-stop right through the end of the business cycle as US growth, inflation and rate hikes overtake “global synchronised growth” and DXY just keeps rising. As EMs steadily fall apart owing to capital outflow we’ll sooner or later reach a crisis and DXY will spike on safe haven flows as the global business cycle ends. Russell Napier is thinking along the same lines:

We know what the Federal Reserve plans to sell this calendar year, $228 billion. We know what the rise in global foreign reserves is, and about 64% of that will flow into the United States’ assets. Slightly less of that will flow into Treasuries. $228 billion, at the current rate at which foreign reserves are accumulating, we are not going to see foreign central bankers offsetting the sales from the Fed.

So that’s a net sell. We don’t know what that net sale will be, but it’s a net sale from central bankers at a time when the Congressional Budget Office forecasts a roughly $1 trillion fiscal deficit. This is the first time in my investment career that savers will have to fund the whole lot. And it’s perfectly normal that real rates of interest have to go higher to attract those savings.

$1 trillion is still a large amount of money. It can come from anywhere in the world. It can come from outside the United States. It can come from inside the United States. But it’s a liquidation of other assets or a rise in the savings rate, which is necessary to fund this. Either of these things is positive for the dollar.

…So the strong dollar, if it continues and if it comes to pass, really could force China into a corner. That, combined with the trade tariff policies of the president, may be leading us to a more flexible exchange rate. Or at least what will be billed as a more flexible exchange rate but, for all intents and purposes, is likely to be a weaker Chinese exchange rate. So I was just going to read you the list of those emerging market economies where the debt-to- GDP ratio has been going so strongly that actually the BIS suggests there is a risk of a systemic banking crisis. China is top of the list; you’re absolutely right to point to China.

I think there is definitely a role already being played by higher US rates. So if the dollar goes higher as well, it’s definitely playing a role in creating vulnerabilities. We’ve seen a couple of large Chinese companies unable to pay their US dollar credit. As I’ve mentioned, there’s a lot of Turkish companies that really can’t pay it. And that is already something to do with the rise in US yields. They’ve gone from incredibly low levels to low levels. But it’s enough at the margin when global debt to GDP is to shine the light on particularly vulnerable economies and particularly vulnerable companies.

So all I would add – let’s say I’m wrong on US rates and these yields continue to rise, I think that’s particularly bearish for those outside of America who borrowed dollars, people we’ve already focused on. I think United States growth may be good. United States inflation may be rising.

I wouldn’t specifically see any particularly bad credit issues in America. I don’t see it being anything like we’ve seen in the past. But outside of America, I think there would be an awful lot of pain going on as interest rates go higher and higher and higher. Remembering that, roughly, the European banks – I should say non-US global banks – have got a loan book in dollars of about 4.5 trillion.

That’s a big loan book for people who don’t really take US dollar deposits. And the implications of higher US rates and a higher dollar mean that the pain may not be so America specific, but it could be very emerging market specific.

Leading to an AUD in the bottom half of the 50s or lower.

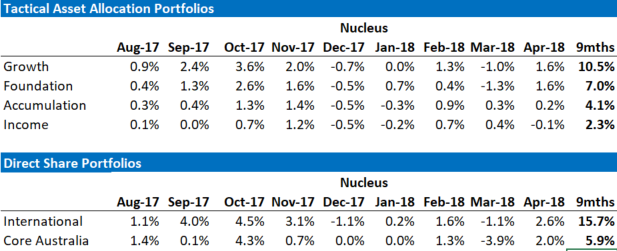

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.