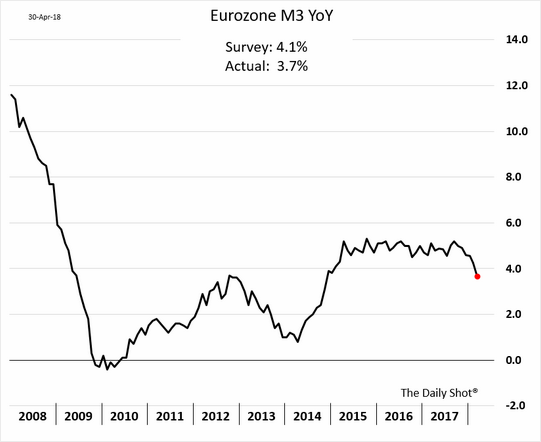

As we bid adieu to an all too brief European boomlet:

Advertisement

AUD was monkey-hammered to a two year low as 75 cents broke:

It was mixed against EMs:

Advertisement

Gold was hit but is hanging on!

Oil gave in:

Base metals can’t take the runaway USD:

Advertisement

Neither can big miners:

Nor EM stocks:

EM junk is screaming get out of the periphery:

Advertisement

As Treasury yields pile it on and keep on flattening over the curve:

While bunds are bought:

Advertisement

Stocks were flat:

Nomura says it all:

DOLLAR BREAKS-OUT, AS RECOUPLING WITH RATE DIFFS BLEEDING LEGACY MACRO POSITIONING

Heard this one before? DXY through 200DMA overnight is escalating the “performance bleed” from consensual macro positioning with implicit “short USD” components

With the “synchronized global growth” narrative now being capitulated against, the Dollar has recoupled with rates differentials, as US is again viewed as the world’s leading growth-story

In conjunction with R.O.W.’s “slower growth” trend, we have seen the “hawkish central bank pivot” thesis break-down as well—BoC, BoE, BoJ are collectively “regressing” with increasingly “dovish” rhetoric, while PBoC takes outright “easing”- / stimulus- actions

Nomura Quant Strategies CTA model showing the “Dollar reversal” phenomenon in “real-time,” as WoW we see “short USD” positioning expressions beginning to reverse / pivot in not just FX but Equities and Commodities as well

EM equities longs then in a dangerous position, as TFF data shows the Asset Manager “net long” position @ +2.5 z-scores, while Leveraged funds too remain high @ +0.8 z-scores

Despite Dollar’s move, “long Crude” trade continues to hold via geopol w/ Iran decertification looking certain…yet is largely “priced-in” as a “known unknown”

Crude holding higher is critical for the larger “bearish rates” / “re-inflation” themes

Goodbye global synchronised growth and EUR long. Hello US leadership and crumbling AUD.

Advertisement

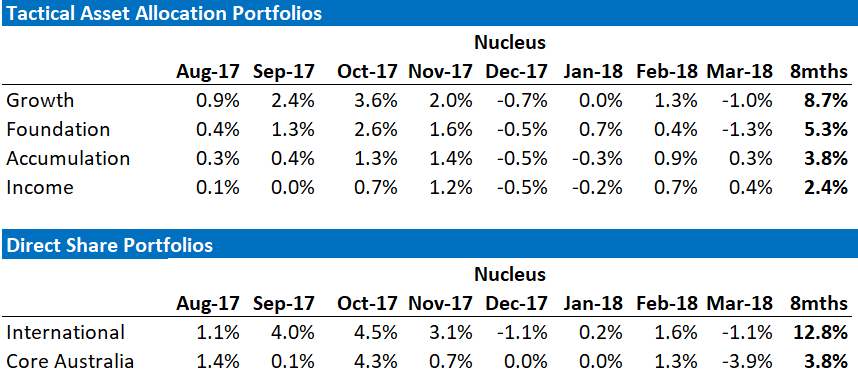

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively to international stocks but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

Advertisement

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.