Damien Boey at Credit Suisse has taken his bear pill today:

Investor concerns about trade tensions are soothed by Kudlow

Overnight, investors were initially very concerned about trade retaliation measures announced by Chinese officials. However, sentiment turned sharply higher after US President Trump’s new chief economic advisor Kudlow told investors to relax. US equities reversed course from being 1.5% down to 1.2% higher on the day. Within the equity market, it was interesting to see that every major quantitative style lost money, with quality underperforming the least, and value underperforming the most. It was very much a night of beta dominating alpha.

Our initial observation is that trade policy by itself is not driving market dynamics. If it was, Chinese retaliation would have been the dominant driver of (negative) market sentiment. We highlight this because:

1. There are more powerful liquidity undercurrents at work in the market that we should not overlook.

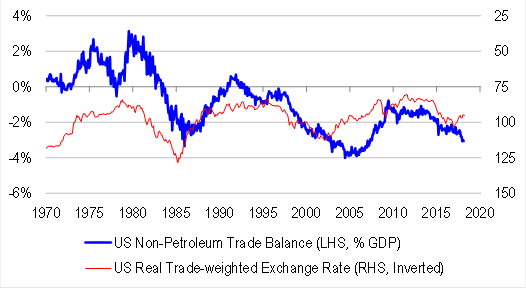

2. Trade policy by itself will not drive the direction of the US current account deficit. There are many other moving parts to the equation.

On the second point, note that it is possible for the US trade deficit to get bigger (rather than smaller) in response to more protectionist measures if:

1. The USD strengthens significantly, eroding the initial shock to export-import relative competitiveness from tariffs. A stronger real USD could make imports look far more competitive relative to exports, widening the US trade deficit at the margin. At the same time, a stronger USD could put pressure on USD-pegged economies, with capital flight causing liquidity management problems, slower domestic demand growth, reduced appetite for imports, and larger trade surpluses.

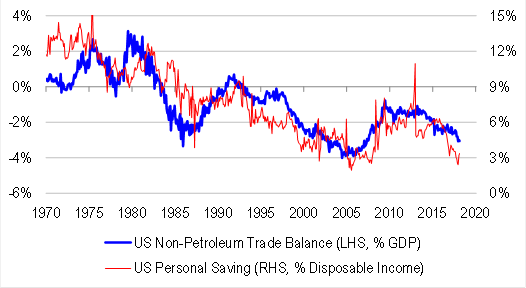

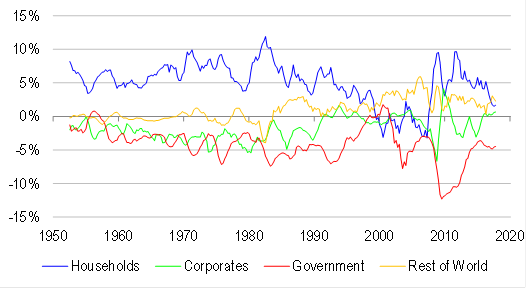

2. The US government pursues large scale fiscal deficits, and the private sector responds in kind. Recall that the US government can create USDs through deficit spending because it has access to an “overdraft-like” facility with the Fed. And by definition of the balance of payments, the trade balance is equal the sum of saving across private and public sectors. If the US fiscal deficit gets larger, and the private sector does not increase its saving, the resulting injection of USDs passes straight over to foreigners, increasing USD liquidity in offshore markets.

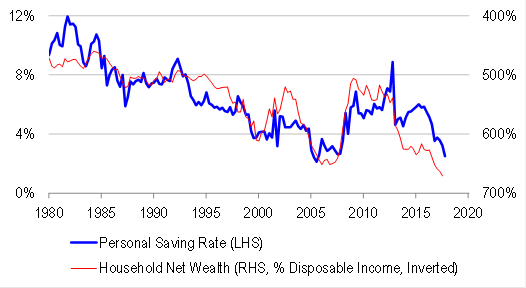

In this context, perhaps investors remain wary of the Trump administration taking with the one hand (protectionism) but giving with the other (fiscal spending). Perhaps they are still trying to figure out the balance between the two forces. And at the risk of being a little circular, asset prices are the key swing variable. The key question is how the US private sector responds to the changes, and the key driver of the US household saving rate is net wealth (a proxy for asset prices).

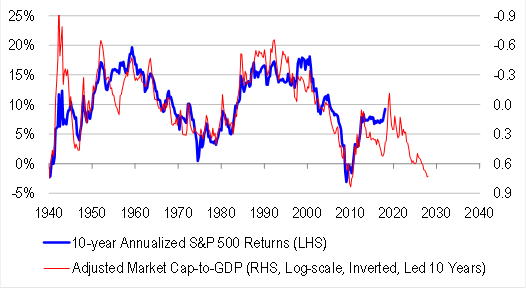

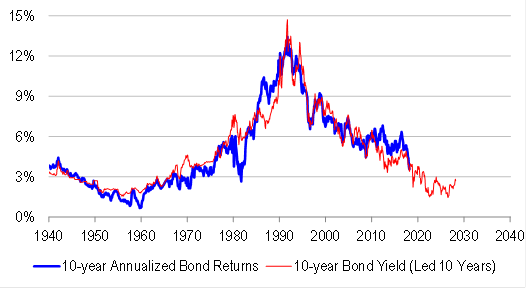

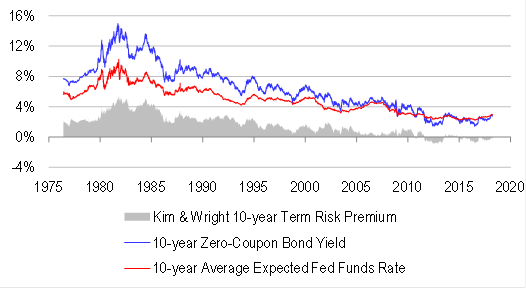

With all of this in mind, our starting point is not so much with the real economy or policy settings. Rather, with asset prices at extreme levels in the US (eg equities yielding less than bonds, which themselves contain a negative term risk premium), the better starting point in our view is to look at asset allocation signals. In a (broadly-defined) tightening environment with stretched asset prices, the predominant risk is that asset prices weaken in the medium-term, causing US household saving to rise. Asset prices could drive the real economy which in turn could drive policy settings. To be sure, strong fiscal stimulus could disrupt the chain of causation in the short-term, by re-focusing investor attention on growth and the real economy as drivers of asset pricing. But unless the US government plans to geometrically (as opposed to linearly) increase debt, and the Fed chooses to stop tightening, this would at best be a short-term disruption.

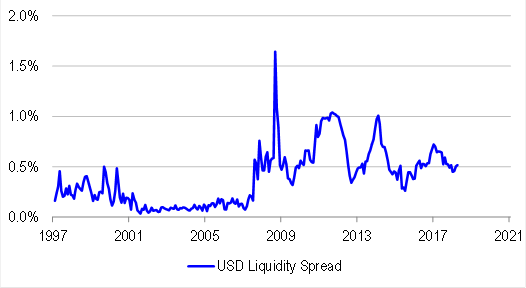

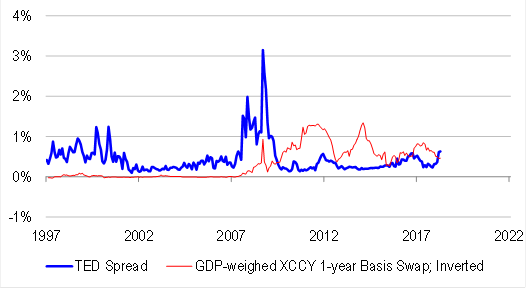

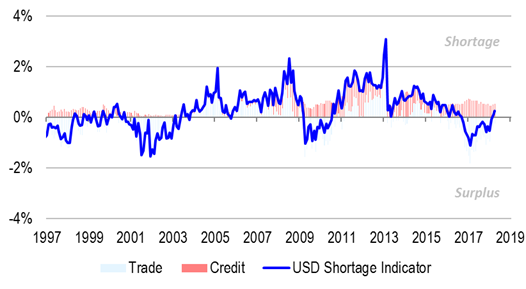

Interestingly, in the background, USD interbank credit spreads continue to drift higher. Cross-currency basis swap spreads are also starting to widen (ie become more negative).

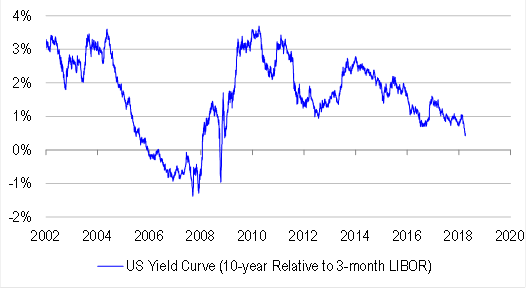

It seems that the money markets are responding to a more general liquidity drain that can only be coming from Fed balance sheet reduction, as gradual as it currently is. Never mind what the Fed does with rates – balance sheet reduction is already making waves in rates markets. Tightening is ongoing, and to some extent independent of the Fed. In turn, this is contributing to flattening of the yield curve (broadly-defined), volatility in equities, and a flight to quality within the equity market.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.