From Bill Evans:

Over the last few months the AUD has been generally weaker starting in early February at around USD0.80 and reaching USD0.765 during March. It is now hovering around USD 0.77.

This is broadly in line with Westpac’s view that AUD will gradually weaken over the course of 2018 and 2019.

We retain our “targets” of USD 0.77 by June; USD 0.74 by December and USD 0.70 by end 2019.

It appears that AUD‘s 2018 peak will prove to be in late January. At that time AUD was valued at USD 0.81 and the Trade Weighted Index was around 65.7. Since then the trade weighted index has fallen to 62.5 (down around 5%) while against the USD the AUD has fallen by 5.2%. This weakness in the AUD has coincided with some stability in the US Dollar with the USD Index (DXY) increasing by a modest 1%.

That stability in the USD over the last few months contrasts with 2017 when the Index fell by around 13.5%; while the AUD lifted from USD 0.72 to USD 0.81 or 12.5%.

Over the same period the Trade Weighted Index was relatively steady rising a modest 2.5% emphasising that most of the AUD’s “strength “ against the USD in 2017 was explained by USD weakness.

That period of excessive USD weakness reflected a solid boost in optimism around the world economy. “Risk on” was the catch cry and the “safe haven” USD was out of favour.

That boost in global optimism can be encapsulated in the movement in manufacturing PMI’s over that period. Recently that positive euphoria around global growth appears to be fading.

Manufacturing PMI’s stood out in 2017 as signalling strong contemporaneous global growth. However, movements in these PMI’s have been less encouraging in 2018. The PMI’s are estimated to have bottomed out around September 2016. The global manufacturing PMI lifted from 50.4 (September 2016) to 54 (December 2017 but has fallen) back to 53.2 (March). Respectively Europe (52.6; 60.6; 56.6); US (51.5; 55.5; 55.7); Japan (50.4; 54; 53.1) ; Korea (47.6; 49.9; 49.1)) and China (50.1; 51.5; 51.0) indicate that only the US PMI appears to be continuing the upswing we saw through 2017.

Trade tensions must be impacting confidence although there remains considerable uncertainty over the extent and timing of President Trump’s trade policies. The 25% and 10% tariffs on steel and aluminium announced at the beginning of March were initially imposed on all countries, but subsequently rolled back to only a few nations, including China , although excluding Europe; Brazil; and Canada (among others). This exemption has been enough to hold the EU back from retaliating to date.

China has quickly become the sole focus of the trade debate with tariffs to be imposed on around $50bn of imports from China. Less than 24 hours after this announcement, China retaliated with planned tariffs on $3bn of US imports across 128 products. Further bi-lateral responses have followed. China can be patient and play “the long game” whereas the US, with mid-term elections rapidly approaching, is likely to “blink” before China needs to step back.

Recent developments in global financial markets also point to less of an appetite for the “risk on” trade. LIBOR and BBSW are rising; credit spreads are widening. Equity markets are falling – US down 9%; Europe down 8%; Japan down 12%; and Australia down 5.2% since late January.

One important explanation is the recent US tax changes which allow US corporates (in particular the cash rich technology companies) to direct funds (mainly US dollars) back to the US from foreign sources (total funds estimated at around $1.5 trillion without paying the onerous 35% tax rate). Foreign banks, including Australia, which had relied on this USD funding, have had to switch demand for funds to local markets, intensifying rate pressures. The “shortage” of USD offshore funds has boosted USD funding costs – LIBOR by around 25 basis points.

Most business borrowers will be affected by this increase in BBSW. One small bank even slightly raised its variable mortgage rate to reflect this 25 basis point increase in short term funding costs. Australian banks have also recently suffered increases in their funding costs in longer maturities with bank 5 year paper lifting by around 15 basis points compared to the risk free rate.

Credit growth has slowed to 3.8% annualised over the three months to February compared with 4.9% growth for 2017. This includes a slowing in housing credit growth from 6.3% in 2017 to 6.0% annualised over the past three months. Business credit stalled over the past three months, with 0.4% annualised growth, in contrast to a 3.2% increase in 2017.

Our core reasons for the further expected falls in the AUD centre around expected interest rate differentials and a downswing in commodity prices. We expect to see the cash rate differential between Australia and the US to widen to 112 basis points (from the current 12.5 basis points) by mid-2019; while the 10 year differential is expected to increase from the current 16 basis points to 40 basis points. These forces are also playing out in commodities. The iron ore price has fallen by around 20% since early February while the coking coal price is down by 15%.

A key issue here relates to the slowing in the growth of the shadow banking system in China (asset growth in the first two months of 2018 is down around 65% on 2017). Non-banks have been key financiers of local government (around 80% of infrastructure investment in China); property developers; and commodity speculators.

These forces can be expected to weigh directly on the AUD and will be most clearly signalled by movements in the TWI – note the 5.0% fall in the TWI since late January. However, if global sentiment recovers and starts to weigh on the USD these forces will be obscured when assessing the AUD in terms of the USD.

With this change in global sentiment signalling a neutral USD we can expect falls in the TWI and AUD/USD to be broadly in line with each other as has been the case since late January.

We see 70 cents by year end on steeper commodity price falls.

FYI, MB has launched a new Australian dollar forecast index which will be updated regularly to keep you abreast of market outlooks. See it here.

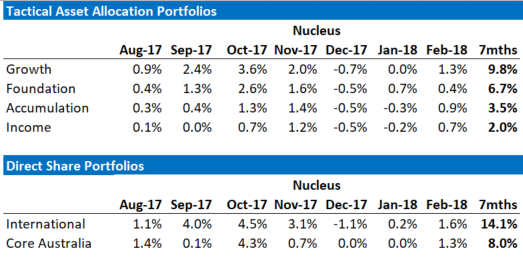

David Llewellyn-Smith is chief strategist at the MB Fund which is currently overweight international equities that will benefit from a weaker AUD so he definitely talking his book. Fund performance is below:

If these themes interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.