The dust is starting to settle a little on the Labor governments recent proposal to stop the refund of unused franking credits and lines are slowly being drawn in the sand in preparation for battle.

An interesting (but unfortunately obvious) emergence has been the ‘inbetweener’ advocation of battlers that are potentially going to be adversely affected having done the right thing and put aside money for potentially their own self-funded retirement.

For those opponents of the changes, an easy path to take is highlighting the worst case examples of where franking credit refunds will have the biggest impact.

How to conjure a loser from changes

One recent example highlighted a single female retiree, aged 75, who had total assets of $600,000 including a share portfolio of $500,000 and therefore was above the asset tested age pension cutout of $556,500 (homeowner).

The proposed changes see a calculated drop of around $11,000 in franking credit income which against the supposed $30,000 annual drawdown, which is substantial. But the question remains, is this a realistic, or contrived scenario?

Upon considering the situation, my financial adviser warning light starts to burn brightly.

Immediately you begin to wonder why a person in their 70’s would have 100% of their liquid wealth tied up in one equity market. Franking credit benefit aside, the volatility this poor lady would be enduring daily would require nerves of steel at 40, leave alone age 75. An easy example of this volatility is the recent drop in the ASX20 over March which would have seen the portfolio fall by around $20,000 for the month!

It’s an interesting choice of an illustration that clearly lends itself to emotive bias over what would exist in the real world. The fact that it gets repeated by experienced financial advisers (who just happen to be in the SMSF sector of which franking credit refund benefits make for a great sales case) is a little more befuddling.

To get a better idea of the impacts, we should start by giving this lady a portfolio that is more realistic and then have a look at the franking credit impacts, as shown below. I have assumed a dividend yield for the Australian component of 5%, and a mix of 45% defensive vs. 55% growth assets (which is at the upper end of investment aggression for what you would typically see in a properly setup portfolio for a person at this age and stage).

| Given Example | More Realistic | ||||

| Weight | Weight | ||||

| Total Balance | $ 500,000 | $ 500,000 | |||

| Cash | 20% | $ 100,000 | |||

| Fixed Interest | 25% | $ 125,000 | |||

| Australian Shares (100% Fr) | 100% | $ 500,000 | 35% | $ 175,000 | |

| International Shares (0% Fr) | 20% | $ 100,000 | |||

| Total | 100% | 100% | |||

| Franking Credit benefit | $ 10,714 | $ 3,750 | |||

Given the above, the impact now drops to $3,750, which whilst not insignificant, is roughly a third of the previously illustrated impact, and highlights that for most cases found ‘in between’ the have and have nots, the impacts of the proposed changes are not as dramatic as initally indicated.

Further thoughts on the proposal

At this point I should make it clear that these changes, recently watered down to exclude current Age Pension recipients, will of course be detrimental to retirees existing cashflow and do exhibit signs of a bit of a ‘new tax’ on self funded retirees. However, as the surge into taxless structures such as SMSF pension accounts continues it is easy to see why some Government revenue tweaking may need to be installed to stem the losses that would otherwise continue unabated.

Considering the MacroBusiness Fund has many SMSF clients, I feel the need to respond in the defense of the SMSF sector. It is obvious that these impacts are deleterious to one of the benefits of choosing an SMSF over other pooled options. Absolutely.

It is important to remember that there are still a number of great reasons to consider one or to remain in one including:

- control and transparency,

- combining family assets in the superannuation system,

- a broader palette of investment options

- and if the changes come into force, the ability to utilise unused franking credits from one member against another in the fund.

Conclusion

Yes, there will be an impact on previous potential returns for those classed as ‘in-betweeners’ and above from the changes, but it important to focus on your portfolio and not be too persuaded by spurious examples. There are other areas of the investment world, particularly overseas, that offer the potential for better capital returns and have the benefit of a falling dollar tailwind. Superannuation still offers the superior solution for most Australians to build retirement wealth.

Ultimately, it is always a risky move to arrange your affairs solely on the basis of saving tax, and once again these recent proposals have shown that legislation can giveth and in turn potentially taketh away.

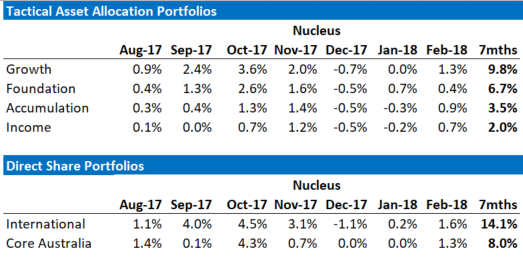

Tim Fuller is operations manager at the MB Fund which is currently overweight international equities that will benefit from a weaker AUD so he definitely talking his book. Fund performance is below:

If these themes interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.