The ABC’s business editor, Ian Verrender, has written a ripper article today explaining why Australian mortgage rates might soon start to rise:

Official rates may not be going anywhere any time soon… But tremors are roiling through global money markets that will flow directly through to higher domestic rates.

Given the lethargic state of the Australian economy, if the Reserve Bank is going to be forced into action, it’s more likely that its next move will be to lower the official rate, just to counter the impact of higher global rates on an economy that’s mortgaged to the hilt…

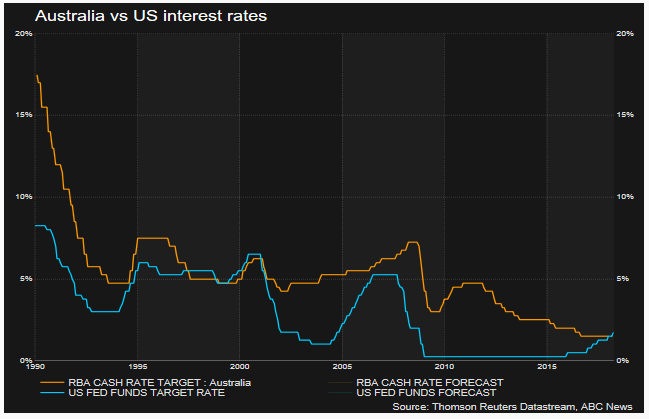

Since the financial crisis, the US Federal Reserve has pumped more than $US3.5 trillion into the US economy — a large portion of which washed around the globe — via a process known in polite circles as Quantitative Easing. But let’s just call it what it is: money printing.

When combined with official rate cuts down to zero, it pushed market rates to their lowest levels in human history, the final sprint in a 30-year run of declining interest rates…

No-one, it seems, has given much thought as to what may happen once the process is reversed. As of October, the Fed began pulling $10 billion each month out of the system… the process already is having an impact, particularly on short-term market rates, which have pushed higher since January…

On the domestic front, the Hayne Royal Commission has begun to cast a pall over the banks, exposing years of reckless management, excessive risk taking and lax lending standards.

That can only mean one thing. Loans will be more difficult to obtain in the future. Potential borrowers are likely to find their bank either unwilling to lend as much as previously, if at all…

How soon before this hits us?

That’s difficult to answer with any precision. But higher rates offshore will ripple through our financial system because our banks have borrowed heavily in wholesale debt markets offshore.

Royal Commission or not, they won’t hesitate to lift mortgage rates if their wholesale funding costs rise…

As a nation, we now have more than $1 trillion in net foreign debt, almost a tenfold lift since 1990. The vast bulk of that is money our banks have borrowed offshore… Our banks have borrowed around $700 billion on offshore markets and watched on in glee as we’ve ploughed that into real estate, pushing prices to the heavens, forcing new entrants to borrow even more…

Those vastly inflated real estate values may have pumped up national wealth. But the downside is that our household debt is at extremely worrying levels. At close to 200 per cent of annual household income, it’s among the world’s highest.

So stretched are household budgets, any kind of interest rate hike would see consumption, by far the biggest driver of our economy, slashed. Add in a spike in bad debts and bank profits would be hammered.

Verrender has touched on all of the key ingredients here, namely:

Rising global funding costs;

The Banking Royal Commission;

The banks’ extreme offshore borrowings to fund non-productive housing lending;

World-beating household debt levels; and

The likelihood that the RBA will cut the official cash rate to offset rising mortgage rates.

Advertisement

The only thing I will add is that the negative press (and possibly outcomes) arising from the Banking Royal Commission could spook offshore lenders to the banks, raising their risk premia and increasing bank funding costs even further.

In any event, the next move in official interest rates is very likely to be down – a view MB has held for several years.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.