From Australian Broker comes a sombre analysis of the interest-only mortgage reset looming for Australia’s housing market:

In January, UNSW professor of economics Richard Holden published a sobering observation of Australia’s relationship with high-LVR and IO loans. In it he reported Australian banks lend an average 25% more than their US counterparts and that these loans are poorly structured and sometimes based on falsified or inaccurate household finances.

A decade ago, US banks learned this lesson the hard way, when five-year adjustable rate mortgages could not be refinanced and the fallout triggered a chain reaction that dragged most of the globe into recession.

In Australia, IO lending has comprised as much as 40% of the loan book at the major banks, and a particularly large share of property investors choose IO…

“Interest-only loans in Australia typically have a five-year horizon and to date have often been refinanced. If this stops then repayments will soar, adding to mortgage stress, delinquencies, and eventually foreclosures,” Holden told Australian Broker…

“It’s our professional and ethical obligation to look after the best interests of our clients and help them plan strategies” Louisa Sanghera, Zippy Loans

A teacher at the University of Chicago when the US housing market crashed, he added, “The high proportion is similar to the high proportion of adjustable rate mortgages in the US circa 2007.”

So how scared should people be? According to Hair, a lot of people “should be very afraid”, although he says dynamic lending policies, a banking sector unwilling to lose market share and strength in non-bank lenders will dampen some impact…

“The bigger concern should always be unemployment that triggers substantial hardship, very quickly across a broad group of people, which has the effect of contagion”…

“Expect to see some very angry investors looking for a lender, broker or adviser to blame, and pay compensation, for the position they find themselves in,” he adds.

Is this Australia’s sub-prime crisis? From those in the industry it’s a unanimous no. However that doesn’t mean to say a significant number of borrowers won’t receive a harsh wake-up call.

There’s still more tightening of lending standards to come amid falling house prices, all of which will run headlong into the fallout from the ongoing macroprudential tightening and interest-only loan reset that will clobber banks for the next four years.

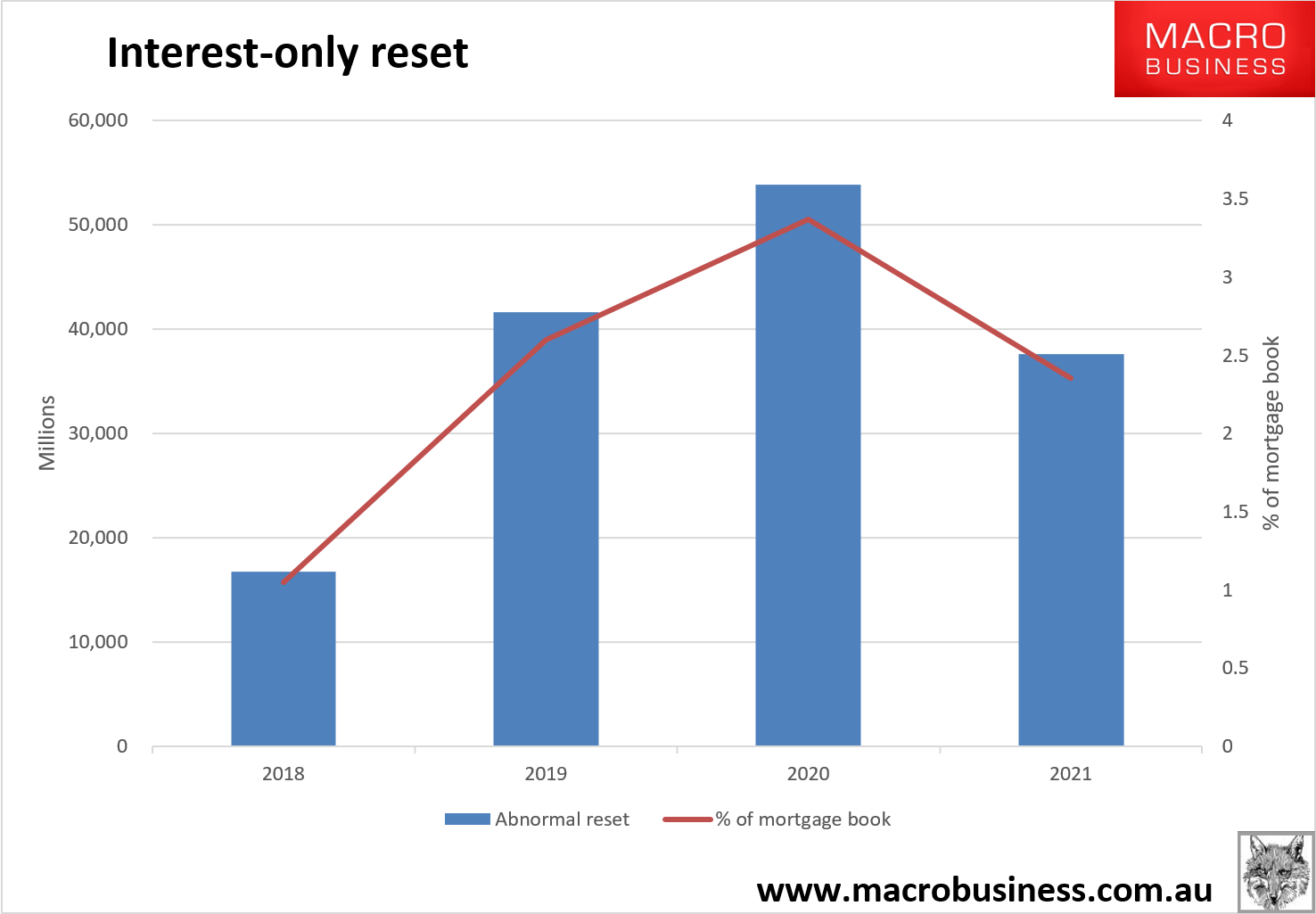

There is still confusion about how much the back book and front book of the banks can absorb the reset. Banks can only issue 30% of new loans as interest-only now. That’s roughly $40 billion per quarter, which would mean that the reset could absorb the banks’ entire front book IO capacity.

Advertisement

Therefore, some large portion will have to transpire in the back book. Our best guess how much that will be is based upon the history of what the banks have managed previously, We’ve guessed they will be able to manage some $25 billion per quarter in the back book as the great reset builds. That means we’ll see the following total resets to principle and interest:

At the peak, that’s 3-4% of the loan book being shocked by 40% repayment hikes. It’s huge.

Advertisement

If that wasn’t enough, negative gearing and SMSF borrowing will be stripped next year when Labor wins the election, adding to the stiff headwinds facing investors.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

.PNG)