It looks like the wheels are well a truly falling off Toronto’s housing market. From the Financial Post:

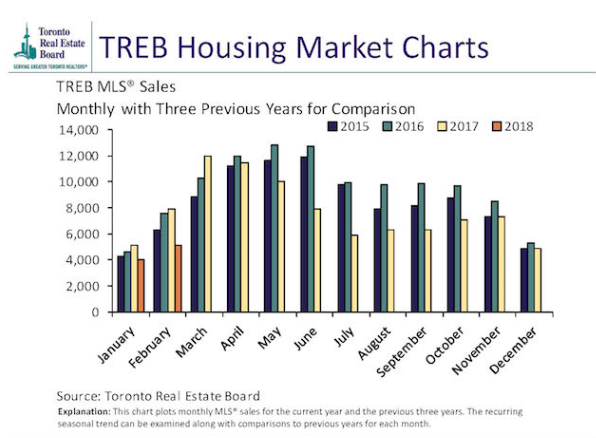

Home sales in the Greater Toronto Area plunged 34.9 per cent in February compared to the same month a year ago as buyers adjusted to new mortgage rules and government policy interventions, the Toronto Real Estate Board (TREB) said.

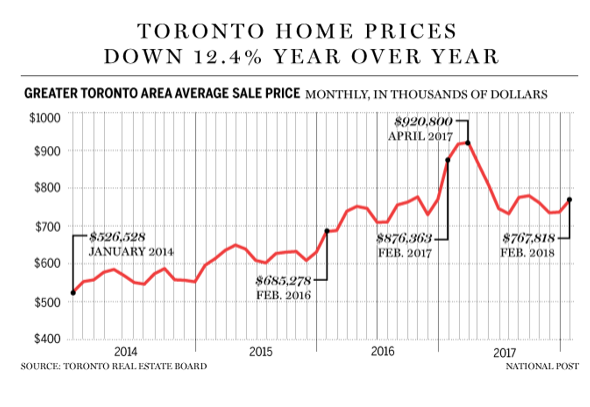

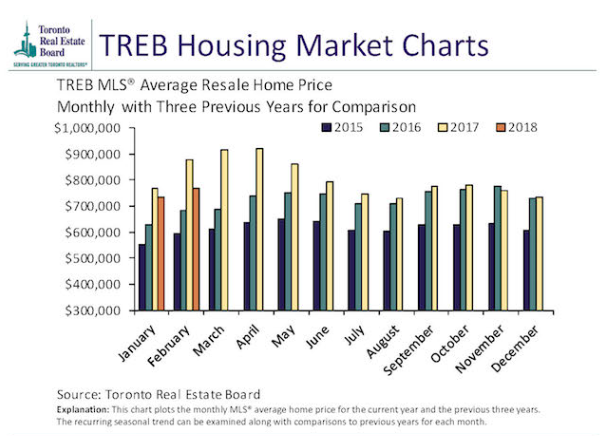

Prices tumbled too, with the average sales price for all housing types falling 12.4 per cent to $767,818.

TREB said the declines had been expected due to market-cooling measures brought in by the Ontario government last April and tougher new mortgage rules introduced in January. The board had also warned that figures would be particularly stark in comparison to the opening months of 2017, when a booming market sent sales and prices skyrocketing. The market slowed considerably in the second half of last year following the implementation of the Ontario measures – which included a 15 per cent foreign buyers’ tax…

Prices for single detached family homes fell 17.2 per cent in the GTA to just over $1 million – weighed down by an 18.6 per cent decline to $1.28 million in the city of Toronto, and a 17.8 per cent drop to $911,065 in the 905 region. The number of single detached houses sold in the GTA fell by 41.2 per cent…

TREB president Tim Syrianos said prospective homebuyers are still coming to terms with the “psychological impact” of the Ontario housing market measures and some have had to re-evaluate their home buying plans due to higher interest rates and new mortgage stress testing guidelines brought in by the Office of the Superintendent of Financial Institutions in January.

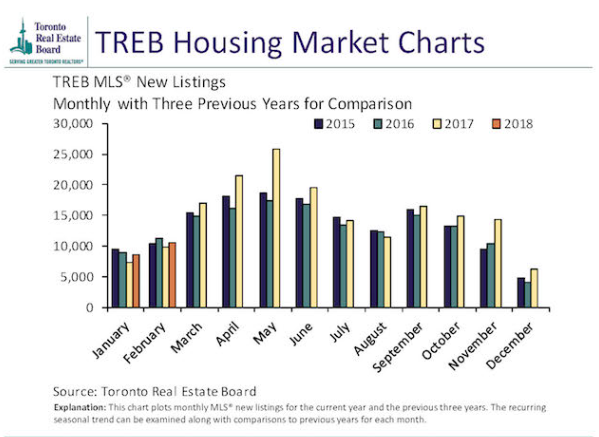

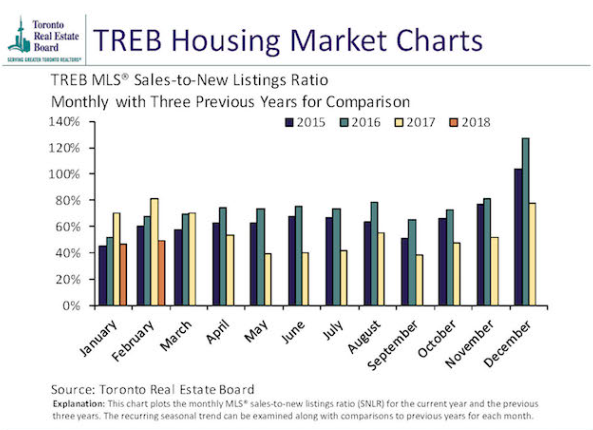

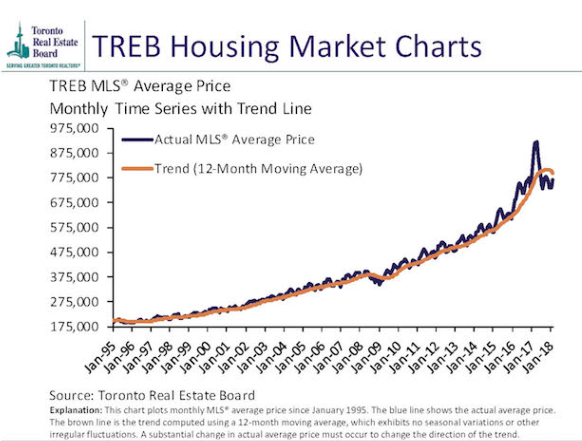

The below charts from TREB provide further context:

Advertisement

New listings strong, sales down, prices down. Those are some bearish indicators right there.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.