Via the AFR comes Phil Lowe:

“I would not like to see a return of 45 per cent of loans being on an interest-only basis,” he said, adding the 30 per cent cap should stay.

However, he said the cap on 10 per cent growth in investor loans was no longer needed, as APRA chairman Wayne Byres told a senate committee last week.

He said APRA need to keep a strong commitment to look at lending standards.

“The measures APRA has taken to reinforce those are permanent and should be”

That’s a lot of pressure to not remove the interest-only caps. Nor should they be removed. Ever.

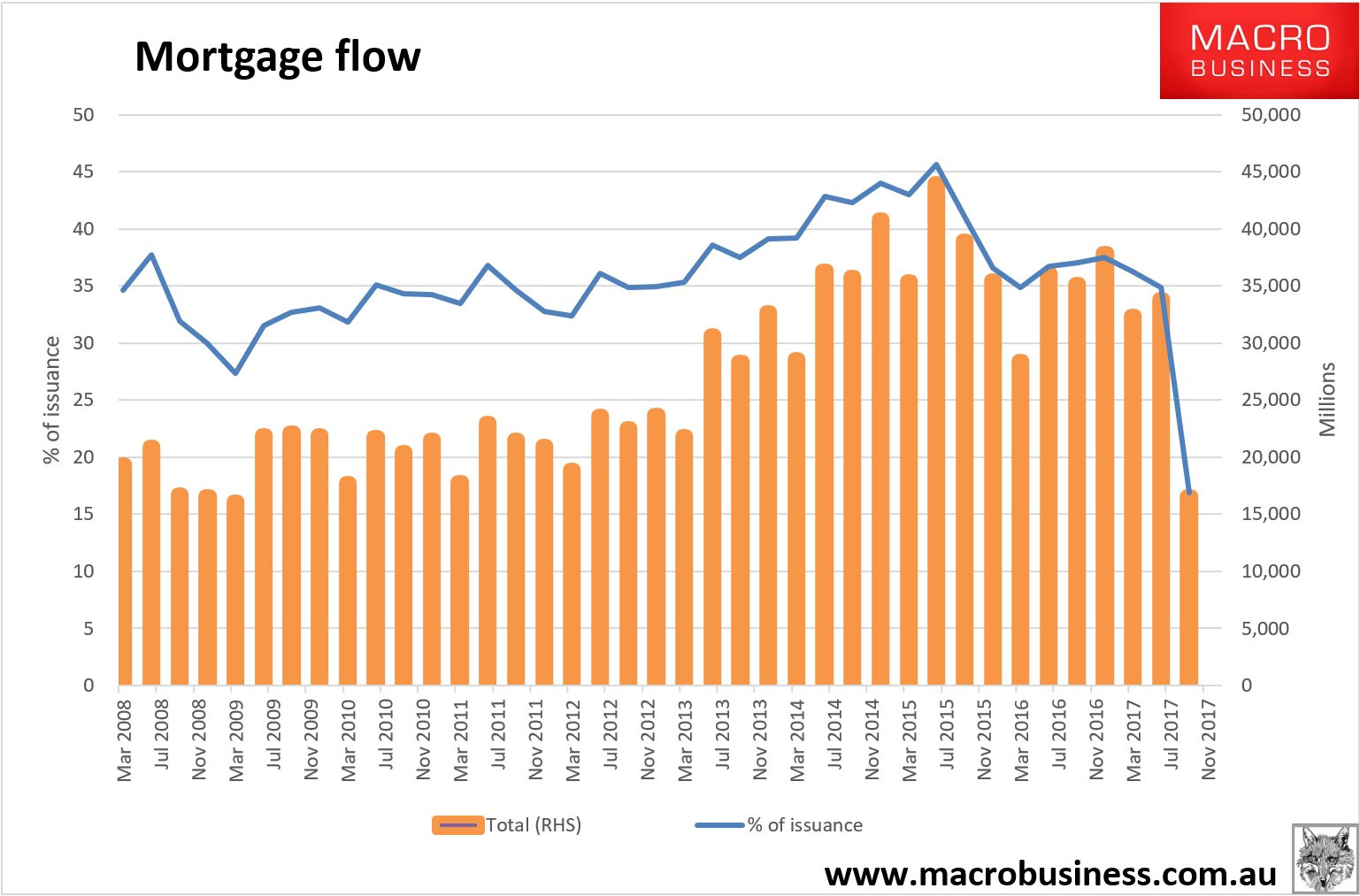

Here is the history of the interest-only bubble:

There is confusion about how much the back book and front book of the banks can absorb the reset. Banks can only issue 30% of new loans as interest-only now. That’s roughly $40bn per quarter which would mean that the reset could absorb the bank’s entire front book IO capacity. So some large portion will have to transpire in the back book.

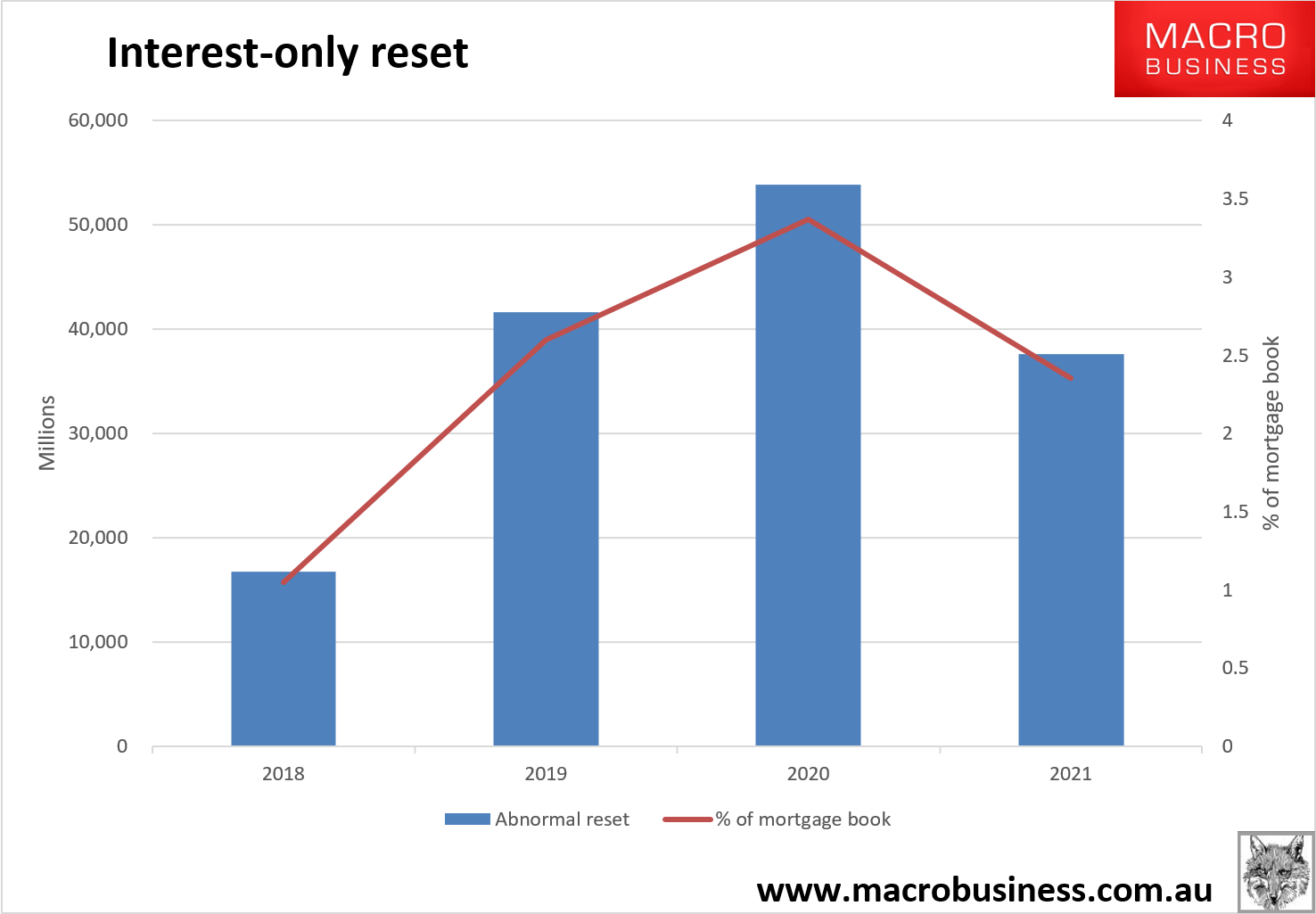

Here’s my best guess how much that will be based upon the history of what the banks have managed previously, I’ve guessed they will be able to manage $25bn per quarter in the back book as the great reset builds. That means we’ll see the following total resets to principle and interest:

My total is more like $150bn of forced resets. That is a lot of tightening ahead. My guess would be overly bearish by a long way and it will still be a lot of tightening.

For perspective, the above is similar in relative scale to the US sub-prime reset experience:

One can’t be sure of these totals but it is certain that the great reset is not going to be easy and property prices are likely to keep falling as forced sales mount. Most worrying of all, the reset piles higher straight into what is clearly shaping globally as the end-of-cycle period.

It’s no wonder that APRA is now loosening. The RBA is next.