The National Australia Bank has been criticised by the banking royal commission for not disclosing fraudulent behaviour by its bankers and third parties to the corporate regulator within the legal deadline.

NAB executive Anthony Waldron was grilled today by senior counsel assisting the commission, Rowena Orr, QC, about the bank’s Introducer Program, which saw professionals, including solicitors, accountants and financial planners, refer customers to the bank for loans in exchange for commissions.

In November 2015, the bank fired five bank staff in the Greater Western Sydney area, including two branch managers, for dishonesty, fraud and conflict of interest involving the Introducer Program.

The contract of two introducers was also terminated.

But NAB did not report the significant breach to the Australian Securities and Investment Commission (ASIC) within the 10-day deadline under the Corporations Act.

Instead, NAB reported the behaviour to ASIC in February 2016.

Commissioner Kenneth Hayne was scathing about the delay when questioning Mr Waldron.

“NAB knew enough to sack five employees for dishonesty and for conflict of interest,” she said.

“It knew enough by November to sack people for those reasons. [Are] you telling me it didn’t know enough to tell ASIC there was a problem?”

Mr Waldron said he could not offer a reason for the delay.

The misconduct involving the Introducer Program included faked customer signatures on loan applications and the use of fake documents, including payslips, as well as unsuitable loans provided to customers.

One of the sacked branch managers was accused of being dishonest about their relationship with an introducer, with the introducer’s address the same as the branch manager’s immediate family address.

The same branch manager was accused by a whistle-blower of misconduct in an April 2015 internal NAB email.

Another sacked employee was accused by a whistle-blower of taking a bribe which she later returned.

NAB internal documents tendered during the commission showed NAB introducers had a target of $2 million a year in loan referrals and $10 million for commercial lending.

Introducers got commissions of about 0.4 per cent of the value of a loan, and between 2013 to 2016, when fraudulent behaviour was identified, NAB had 8,000 introducers.

Nearly 46,000 home loans worth more than $24 billion were referred to NAB by introducers over those three years.

Commissioner Hayne estimated that NAB would have paid out about $100 million in commissions during that time.

Mr Waldron even admitted that some introducers were gym owners who referred loan customers to NAB in breach of the program rules.

“We weren’t as strict as ensuring they came from industries we were comfortable with,” Mr Waldron told Ms Orr in response to a question.

The bank sacked 20 staff in New South Wales and Victoria last year, and disciplined more than 30 others over the Introducer Program.

In a letter to customers released just before the hearing began today, NAB boss Andrew Thorburn said the bank acknowledged it had not done the right thing by customers in the past and that conduct was regrettable and unacceptable.

“It is important to note that since the issue was identified in 2015 via NAB’s whistle-blower program, we have made extensive changes to our Introducer Program, worked closely with ASIC, fully reviewed the cause of the issue including engaging KPMG to carry out an investigation, and commenced a remediation program for customers,” Mr Thorburn said.

The commission heard sensational evidence from an NAB internal email from October 2015, which outlined whistle-blower allegations of a bribery ring at five bank branches in greater western Sydney involving 11 bank staff, including six branch managers.

They were accused of fraud, including making fake payslips and fake identification, including Medicare cards.

“They charge $2,800 bribery for each customer for home loans mainly, but also personal loans,” Ms Orr told the hearing.

Ms Orr read from the October 2015 internal bank email: “The whistle-blower said the money exchanges hands in cash in envelopes, white envelopes, usually over the counter. Money is deposited at CBA so NAB can’t detect the deposits.

“[It’s] happening on a daily or weekly basis and has been happening for a number of years.”

Wow. The next time somebody tells you about Australia’s sound lending standards, send them this. How on earth could Wayne Byers say he knew of no such problems the other day in the senate:

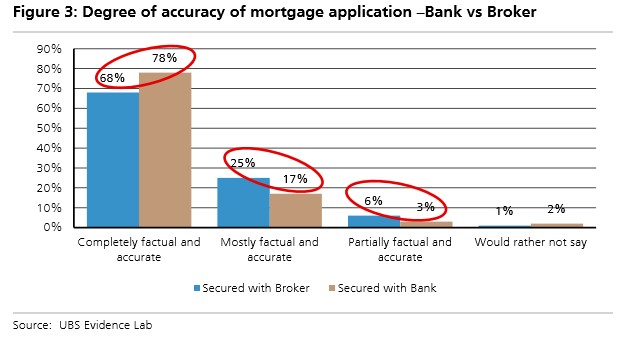

The most significant findings of the survey were (1) Only 72% of respondents stated their application was “completely factual and accurate”. 21% stated they were “mostly factual and accurate”, 5% stated they were “partially factual and accurate” while 2% “would rather not say”; (2) 32% of respondents who secured a mortgage via a broker stated they misrepresented some element of their application, compared to 22% who secured a mortgage via bank distribution; (3) More concerning, 41% of respondents who used a broker in 2016 and misrepresented elements of their application stated they did so based on their broker’s suggestion (vs 13% for bank channel equivalent)…

Of the 344 respondents who stated they misrepresented parts of their application: 14% over-represented household income (18% of those who used brokers and 5% who used bank networks); 13% overstated other assets; 17% under-represented other financial liabilities; 26% under-represented living costs; 11% “other”; 31% “would rather not say”. 12% stated they misrepresented multiple factors.

Unfortunately survey results suggest misrepresentation is systemic with findings similar across the 2015 and 2016 Vintages, price to income levels, LVR, owner occupiers and investors. However, there was a correlation between borrowers who misrepresented their application and: those whose expenditure was broadly equal to their income; stated they are under financial stress; or have missed a debt payment…

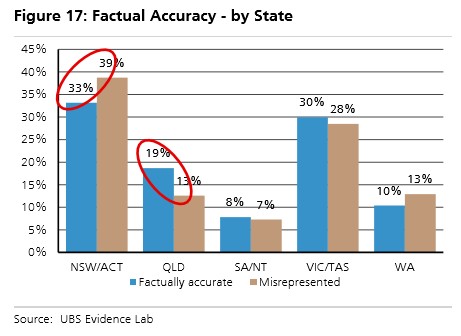

Interestingly customers who come from NSW were more likely to misrepresent their mortgage applications. Notably this continues to be the most buoyant housing market in Australia. Customers from Queensland are more likely to be factually accurate.

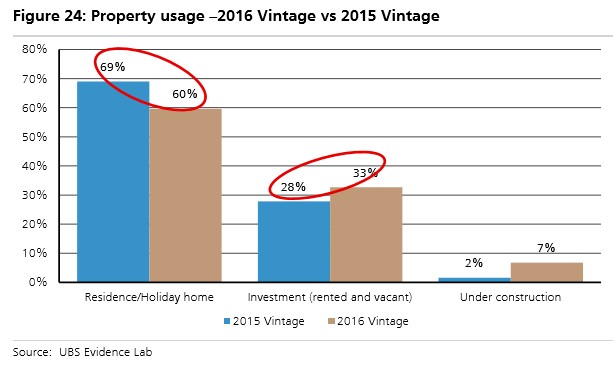

Finally, the use of mortgages for investment purposes accelerated in 2016 contrary to the banks’, RBA and APRA’s data…

We believe this ties in with the ‘areas of less factual accuracy’ section above. This may suggest some customers were not factually accurate when stating the purpose of the loan, especially given the higher interest rate which has now been introduced on Investment Property compared to Owner Occupied mortgages.

What does this mean?

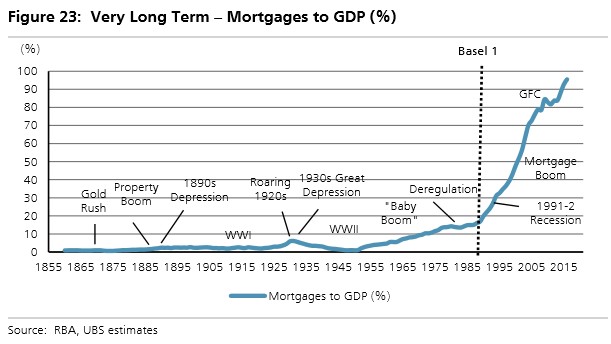

We believe these results are disturbing given: the recent housing market reacceleration; elevated household leverage (186% debt to income); and mortgages accounting for 62% of bank loans.

While banks have tightened underwriting following APRA’s ‘sound lending’ guidance, it does not appear to have prevented applicants ‘stretching the truth’. While low unemployment and rising house prices may help prevent losses near term, more rigorous auditing of applications appears essential, especially via brokers…

We believe it is more important than ever that the banks tighten their mortgage underwriting standards and ensure applications are factually accurate. We continue to see the mortgage broker network as a potential area of weakness in this process.

Even more here. And don’t forget the hedgie sting in Sydney in 2016 which showed that little if anything had changed:

Advertisement

Underwriting standards are poor in banks. The regulators trust the big four banks’ statistics, but we’ve seen that underwriting standards are much worse than advertised.

In our due diligence, we told mortgage brokers and bank managers that we required a 95% loan-to-value mortgage at 10x our gross household income to buy our dream house, and we were consistently told it was not a problem at all. All we needed were two payslips and mortgage insurance. We asked if the bank would call our employer, and both reputable and disreputable brokers said banks rarely verified payslips. Also, “most of the people checking documents are in Indian call centres.” Furthermore, we were told that as long as the payslips had the right Australian Business Number (ABN) and the business checked out, that was enough.

This is not how it has to be. In the UK, for instance, after the credit crunch, banks are far more thorough when verifying income. The bank cross-checks payslips with one’s bank account to see the net amount received corresponds to the gross amount paid. A lengthy affordability questionnaire must be filled out to make sure that pay is sufficient to cover mortgage payments, that are also stress-tested for higher rates. Bonuses, once nonchalantly taken as regular income, are much more strictly dealt with. No-deposit and minimal-deposit loans are much rarer and harder to obtain. Similarly, the US has tightened lending standards since the financial crisis.

But in Australia, more alarmingly, we were informed from various sources that disreputable brokers had software to make authentic looking tax returns for clients who needed mortgages. We were encouraged to lie about our incomes by multiple brokers in order to get dodgy loans past bank loan officers.

It should come as no surprise that lending standards have fallen as third-party origination of mortgages has risen. This was typical of standards in the US in 2005-07. Today, almost half of new housing loans are originated by third parties.

But our biggest surprise came when we visited a building society (a thrift). The bank manager told us her lending standards were conservative compared to the big banks. She would check our income more thoroughly. She then encouraged us to take a 95% loan to value ratio at 10x our gross income because, “It isn’t worth saving another 5% when house prices will rise more than 5%. By the time you save the 5%, prices will rise exponentially.” Those were her words, not ours.

Needless to say, John Hempton of Bronte Capital and your dumbfounded analyst from Variant Perception wandered around Sydney in shock and amusement after every meeting.

When the Dumb Bubble implodes it will be epochal stuff.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.