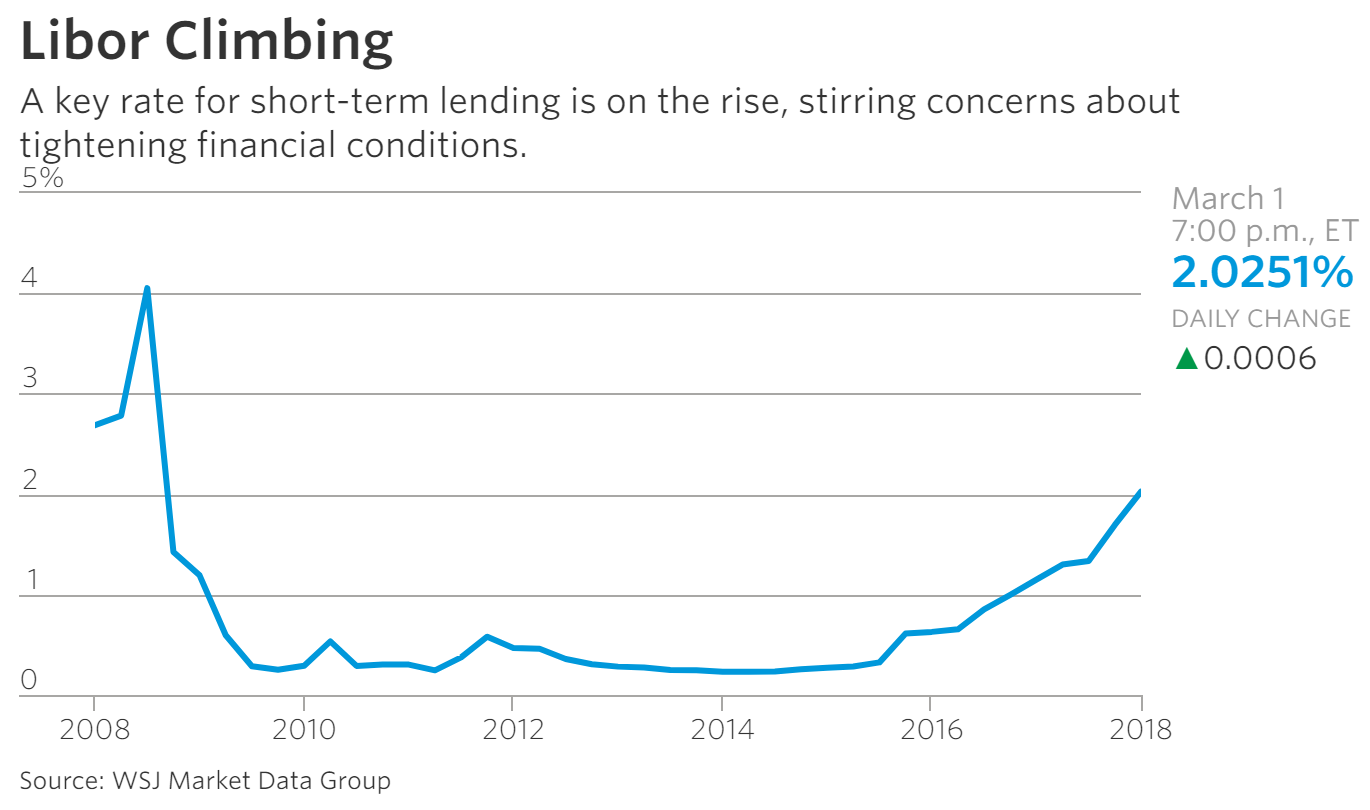

The WSJ has some concern for a steepening climb in Libor interbank lending rates:

Libor has been rising for the last two years as the Federal Reserve has tightened interest rates. But gains have accelerated in recent months, according to RBC Capital Markets strategist Michael Cloherty, because of changes to the U.S. tax code that have encouraged companies to reshuffle bond holdings.

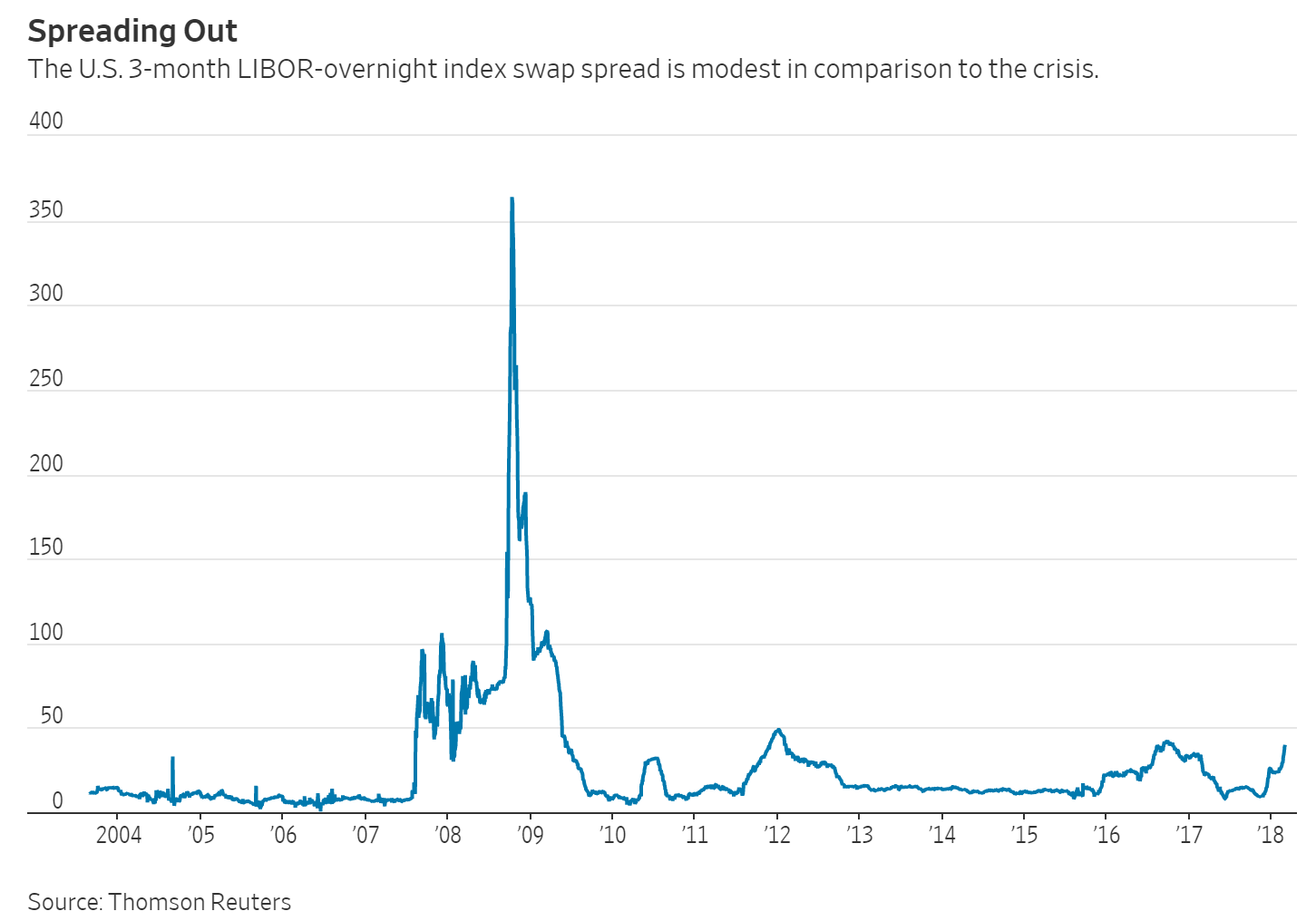

One recent source of worry among strategists and investors has been the growing gap between Libor, which is set amongst banks, and the overnight index swap rate, which is determined by central bank rates. That spread has widened sharply recently and this week was at its highest level since 2009.

Back then, the sudden widening in the Libor-OIS spread signaled mounting stress within the financial system as a liquidity crunch made it more expensive for banks to lend to each other.

The US can doubtless handle the sixfold rise in Libor costs over the last two years since it is a reflection of economic recovery itself. America needs tighter money: the economy is on the cusp of over-heating, with a double blast of irresponsible fiscal stimulus coming from the Trump tax cuts and Republican pork barrel spending.

Whether the rest of the world can handle it is less clear. The Libor spike is transmitted almost instantly through global finance. The Bank for International Settlements says any rise in short-term borrowing costs on dollar markets resets rates on $5 trillion (£3.6 trillion) of dollar banks loans.

Advertisement

It tightens the whole credit structure in Asia and emerging markets regardless of what currency it is in. The Libor-OIS spread measures the extra cost that banks charge each other for short-term “unsecured” dollar loans on the London interbank market. It basically takes the pulse of the lending markets.

Patrick Perret-Green from the hedge fund AdMacro says US companies are starting to repatriate their vast cash holdings abroad to comply with president Trump’s tax changes. This is being drained from the pool of available lending. “It is reducing offshore liquidity. US entities have little incentive to lend that money back out internationally because of risk weightings and capital charges,” he said.

US corporations have some $2.5 trillion in liquid assets offshore, led by the tech giants Apple with $257bn, Alphabet (Google) with $126bn, and Microsoft with $84bn. Much of the money is already in US dollar assets so there is no currency exchange when it returns to the US. The problem is that it vanishes from the dollar-based funding markets in the City or hubs such as Singapore. It rations credit for Asia, Latin America, Russia, and the Middle East.

Borrowers can suddenly find it harder to roll over three-month dollar loans. This is what happened in 2007 and 2008 when offshore markets seized up and threatened to bring down the European banking system.

The scale is epic. BIS data show that offshore dollar credit has ballooned from $2 trillion to $11.6 trillion in fifteen years, turbo-charged by leakage from the Fed’s QE. The BIS has identified a further $13 to $14 trillion in disguised lending through derivatives contracts that are “functionally equivalent”.

Dollar liabilities on this scale are unprecedented and leave the world financial system more vulnerable than ever before to rising US rates.This is the sharp edge of a bigger problem: the $70 trillion edifice of global bonds is built on the assumption of a deflationary global liquidity trap lasting deep into the 21st century. Almost $10 trillion is still trading at negative yields. The structure cannot withstand a sudden shift to a reflation psychology. This week’s Libor spike was driven by the hawkish debut of Fed chairman, Jay Powell, keen to show that he is no White House poodle – no Trumpian “Arthur Burns” – by bravely flagging four interest rate rises this year.

Michael Hartness from Bank of America says the ‘Powell Put’ is set at a lower strike price than the old “Fed Puts” of the Bernanke and Yellen eras, meaning that Mr Powell will not come to the rescue of asset markets until they have suffered.

A vast shift in the balance of the global bond supply and demand is under way

…The buyer of last resort for this debt is currently adding to supply instead. The Fed will be selling down its $4.4 trillion stockpile of bonds at a pace of $50bn a month by the end of the year (though Citigroup warns that the Fed will be forced to carry out a volte-face and resume QE by 2020). In parallel, the European Central Bank will have tapered its asset purchases to zero by September.

A vast shift in the balance of the global bond supply and demand is underway. It is this that lies behind the wild ructions across global bourses this year. My own view is that rising US rates will hit just as the China and Europe come off the boil later this year, creating an unpredictable “scissor” action through currency and credit markets.

As I said this morning, the question for investors is does this become self-correcting as the ructions drive a bid back into the US long bond delivering one more period of Goldilocks growth for the US economy and stocks before the Fed finally undoes the cycle? Or, have the Fed and China it undone it already?

The jury is out on that question. What is perhaps more unsettling is that when the next accident does come, it appears contagion into global interbank market is now the norm not exception.

Not good for Australia’s externally-funded housing ponzi.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.