Interbank credit spreads measure the compensation that money market participants require for taking on counterparty credit and liquidity risks. These spreads have widened sharply in recent months. The three-month bank bill spread to overnight indexed swaps (OIS) has increased to 40bps from a cyclical low of 19bps in October 2017. Spreads are now at their widest since 2011–12, the European financial crisis. This means that money market investors are seeing a material tightening of liquidity conditions and are actively repricing risk.

At a high level, we worry about widening spreads because:

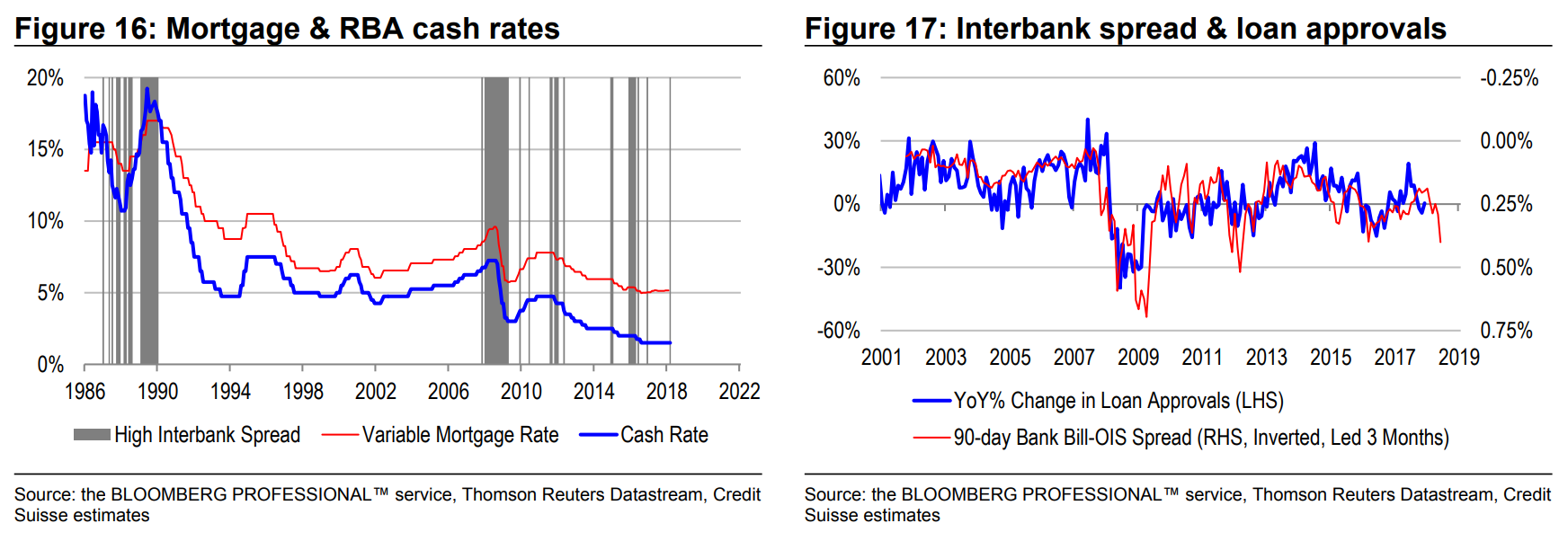

1. If widening is sustained, it usually foreshadows a problem with monetary transmission. RBA rate cuts tend not to get passed on in full.

2. It usually foreshadows weakness in loan approvals, with negative repercussions for economic activity.

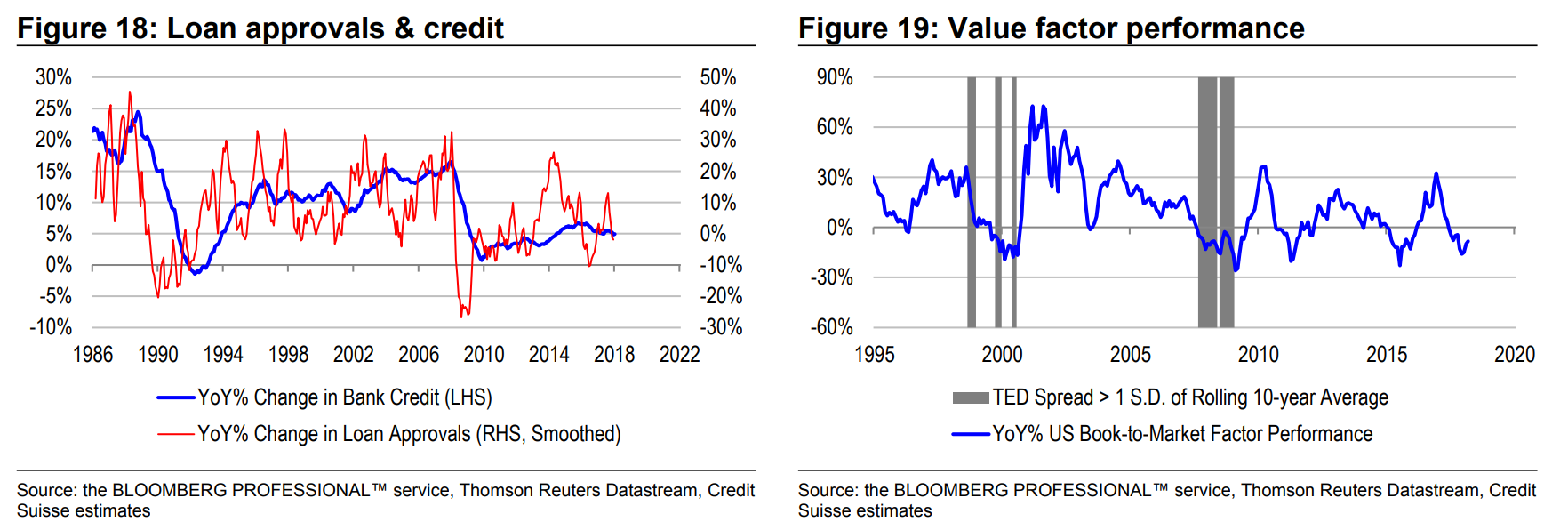

3. It can signal de-leveraging risk, which undermines the efficacy of value factors within the equity market. Note that for value factors to work well, earnings, dividends and book values need to anchor prices, rather than the other way around. But in a deleveraging environment, asset prices tend to drive fundamentals, rendering value factors less useful, or even counterproductive.

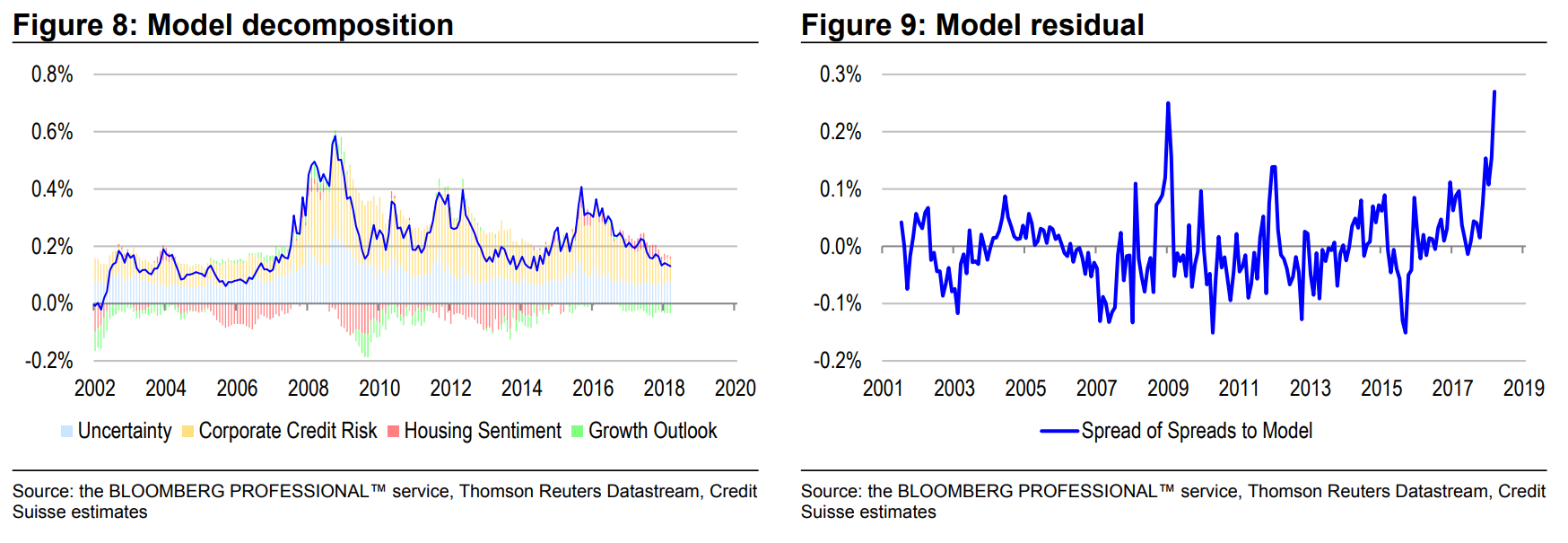

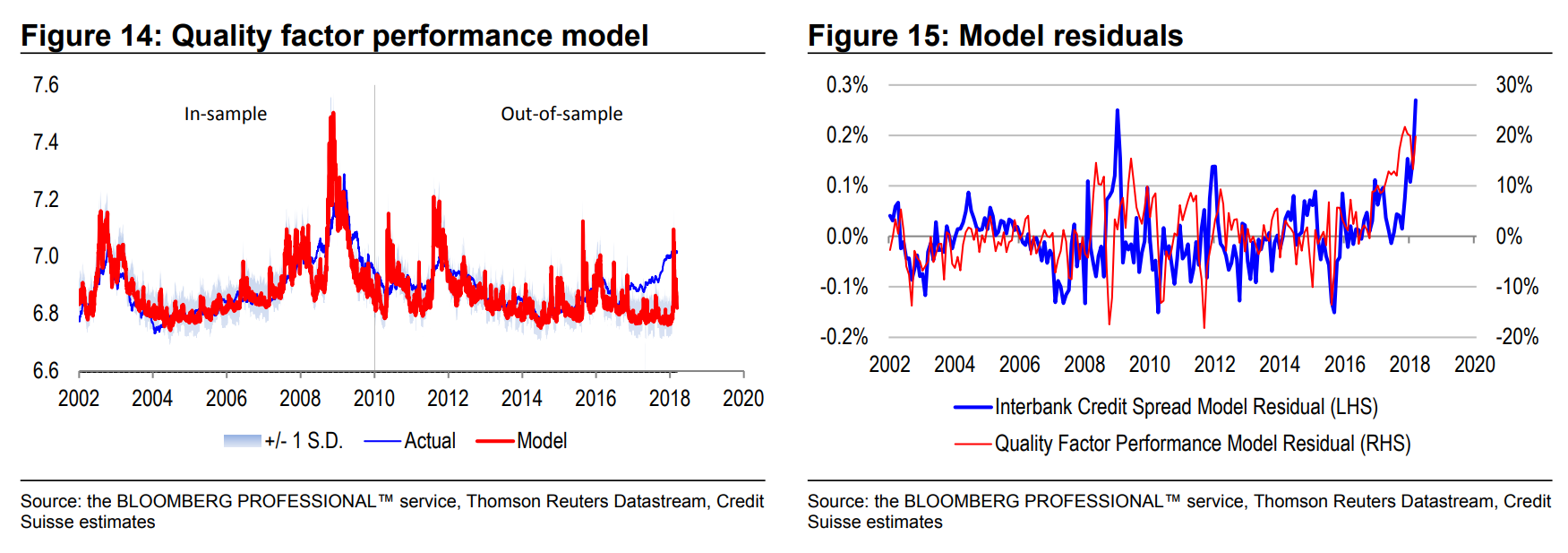

Here, we add another reason to worry: the widening of interbank credit spreads cannot be explained by conventional macro factors, such as corporate credit spreads, volatility, the slope of the yield curve or home-buying sentiment. Indeed, the “spread of spreads” relative to our macro model is now at its widest in recorded history. We are surprised that our model residual is even higher than that during the 2008 financial crisis—yet there is no immediate crisis to speak of.

All of this means that either:

1. We are seeing a temporary spike in spreads which will subsequently unwind as fundamentals re-assert themselves.

2. Alternatively, our model (which incidentally has worked very well in some of the most turbulent macro environments of the past few decades), may be broken.

If the model is broken, it could be the case that the input variables have stopped measuring the risks that actually matter for money market pricing. This would be an especially worrisome development.

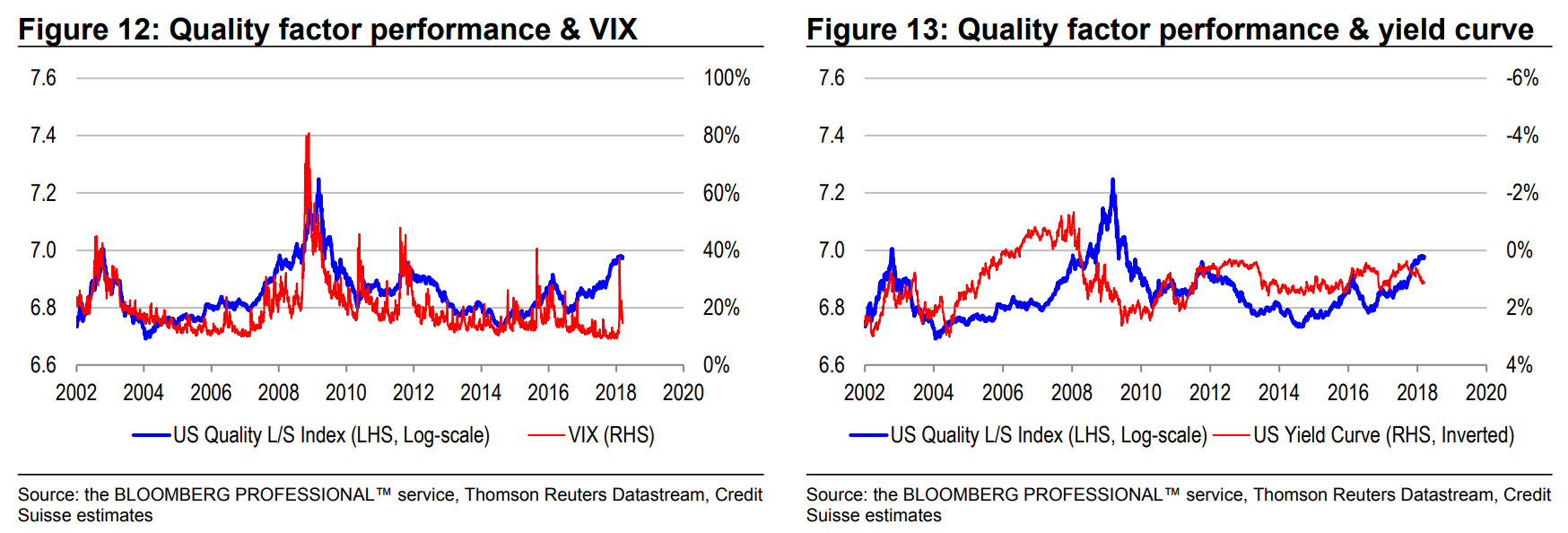

Interestingly, the same divergence can be seen in quality factor performance within the equity market. Quality factors have dramatically outperformed since US President Trump’s election victory in November 2016, despite the positive narrative about growth and very low market volatility. In other words, stock pickers, and not just money market participants, have seemingly “jumped at shadows”. But if this is the case, the phenomenon is exhibiting an uncomfortable permanence and pervasiveness that should at the very least make us reconsider what the risks driving behaviour really are.

Has the money market gone mad?

We have constructed a model of Australian 90-day interbank credit spreads based on the following macro factors:

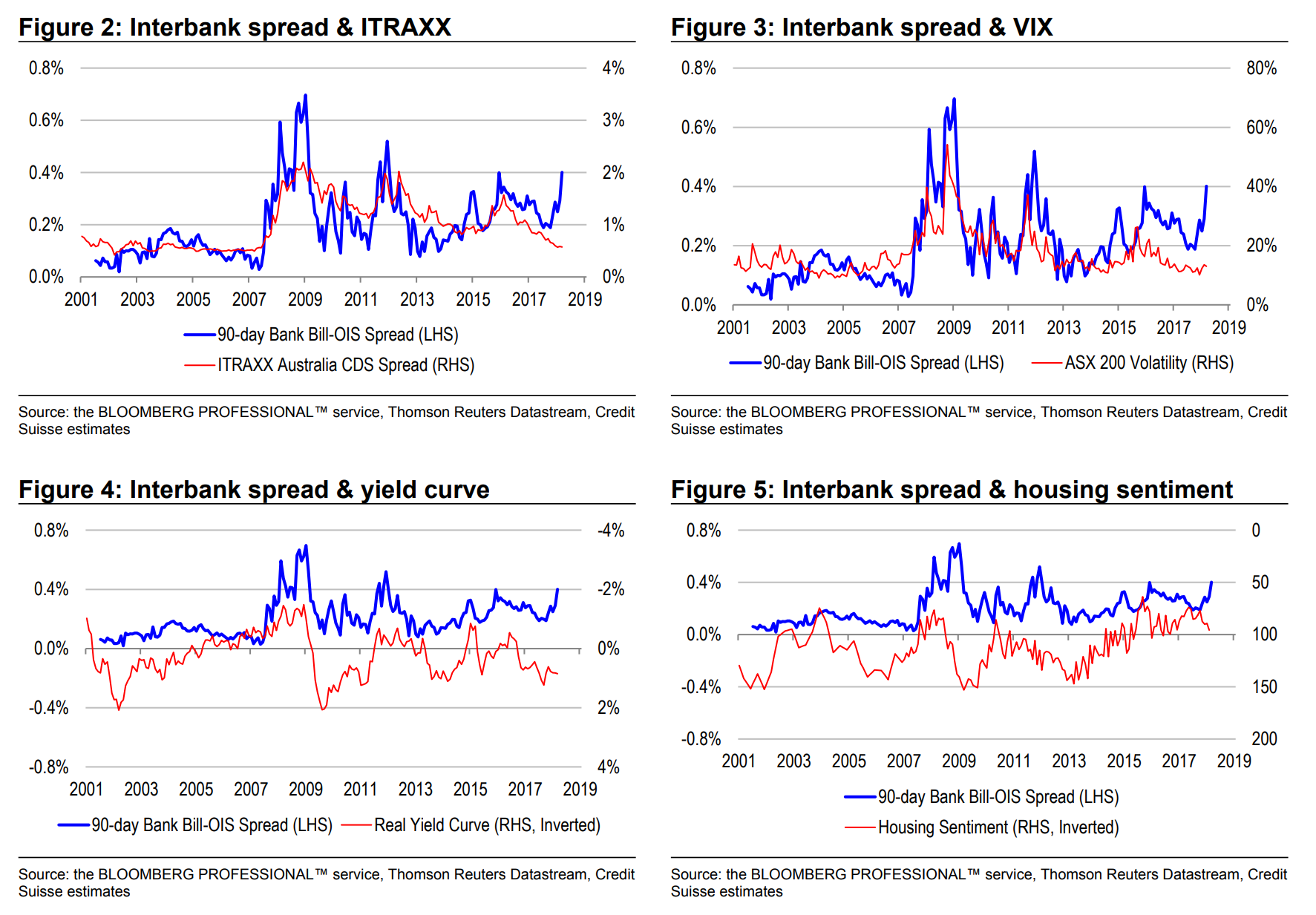

1. Corporate credit spreads: as proxied by a blend of credit default swap (ITRAXX), BBB- and AA-rated spreads.

2. The implied volatility of the ASX 200: A real-time gauge of uncertainty among equity market investors.

3. The slope of the (real) yield curve: A real-time proxy for the growth outlook and the appropriateness of monetary policy settings. We measure the curve as the 10-year inflation-indexed bond yield minus the real cash rate.

4. Home-buying sentiment: Taken from the Westpac consumer survey. Sentiment has historically been a useful leading indicator of housing demand—a key driver of the growth outlook.

Higher (lower) corporate credit spreads and market volatility should lead to wider (narrower) interbank credit spreads. Also, a steeper (flatter) yield curve and stronger (weaker) home-buying sentiment should lead to narrower (wider) interbank credit spreads.

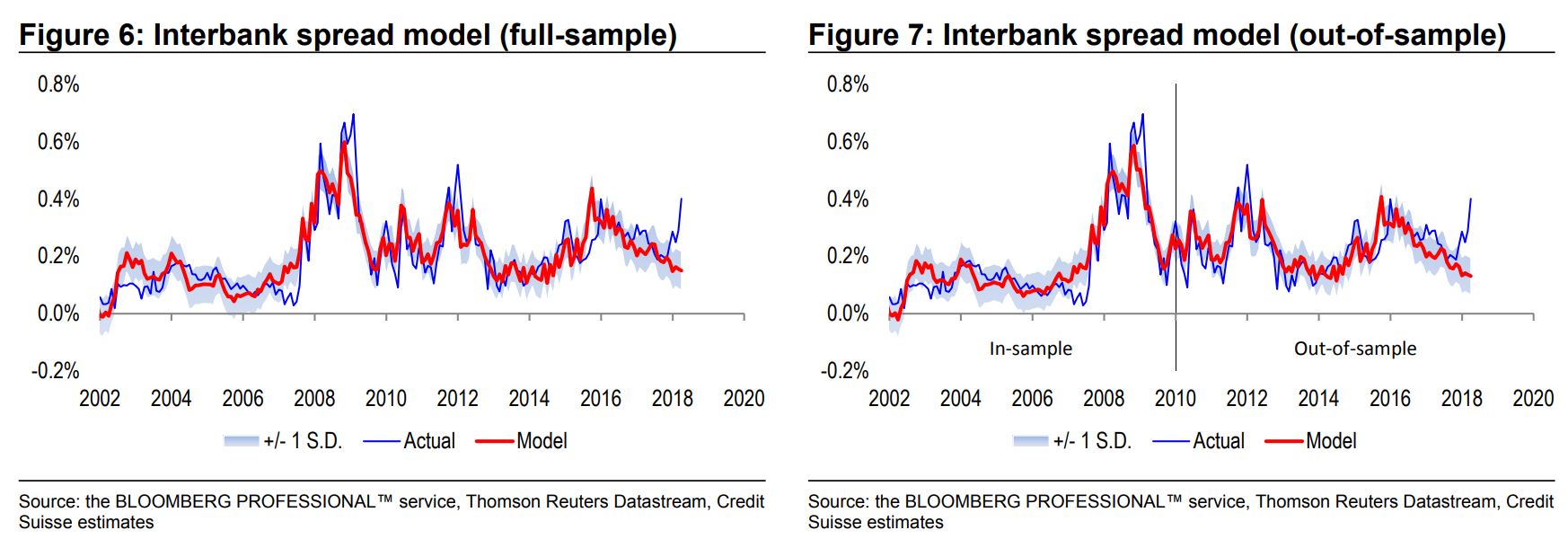

Our model explains roughly 94% of the variation in interbank credit spreads since 2001. Importantly, our model has the following important properties:

1. Statistical significance: Parameters are statistically significant and correctly signed.

2. Cointegration: Through time, spreads tend to converge to a linear combination of our fundamentals.

3. Granger causality: Fundamentals lead spreads, more so than the other way around.

4. Stability: Parameters are quite stable through time, as evidenced by strong out-ofsample forecasting performance since 2010.

Interestingly, all of these features are now being challenged by recent market dynamics. Interbank spreads have widened sharply to 40bps from a cyclical low of 19bps in October 2017. Spreads are now at their widest since 2011–12, the European crisis. But the widening cannot be explained by our set of fundamentals. The spread of spreads relative to our model is now at its widest in recorded history, at more than three standard deviations. While market pricing has moved significantly higher, fundamentals have moved in the opposite direction. Interbank credit spreads have widened—but volatility and corporate credit spreads remain very low. Also, growth outlook factors remain supportive of narrow spreads, with the yield curve steep and home-buying sentiment seemingly bottoming out.

All of this means that either:

1. We are seeing a temporary spike in spreads which will subsequently unwind as fundamentals re-assert themselves.

2. Alternatively, our model may be broken, perhaps because its input variables have stopped measuring the risks that actually matter for money market pricing, or because the chain of causation has started to reverse. If this is the case, perhaps fundamentals converge to the elevated level of spreads, rather than the other way around.

A global phenomenon?

Money markets tightening everywhere

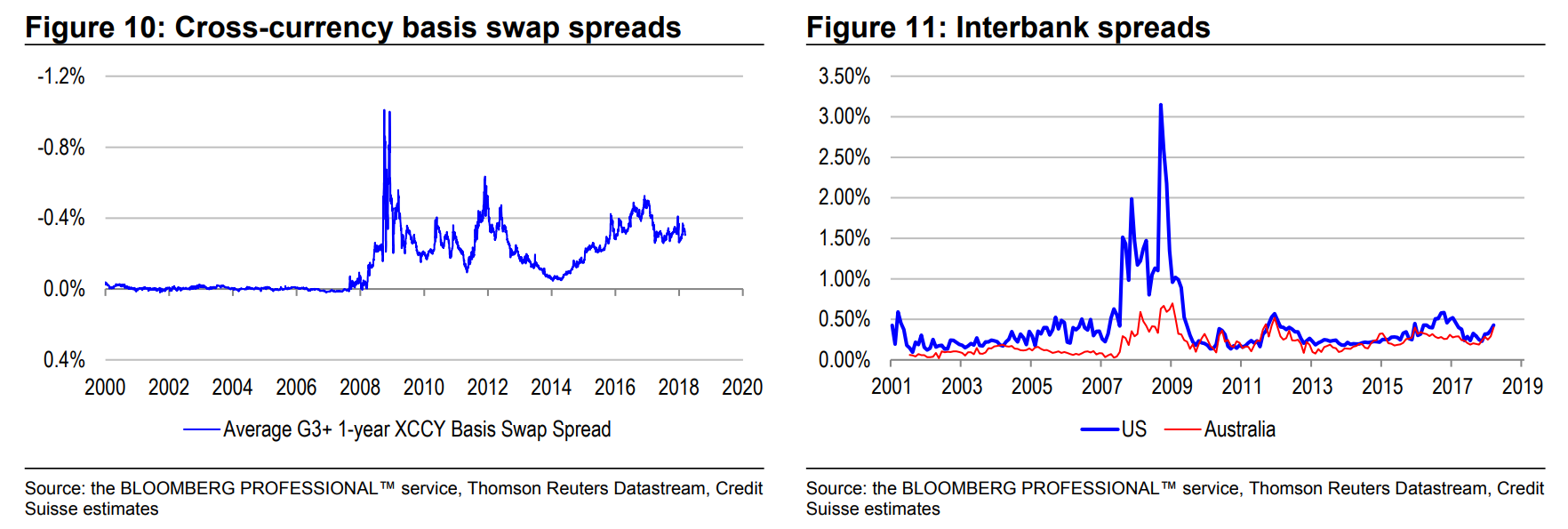

The widening of Australian interbank credit spreads is unusual by historical standards. But it is perhaps not unique by global standards. We note that LIBOR-OIS spreads are widening in most economies, consistent with tightening liquidity conditions globally. The Australian spread is not much wider than its US counterpart, which too has increased in recent months.

Our global money markets expert, Zoltan Pozsar, has explained in recent articles why he believes global money markets should be tightening. His thesis is that:

1. There is a new global reserve requirement, which is superseding the Fed’s. Banks may have excess reserves by the Fed’s standard, after years of quantitative easing. But these reserves are not excessive by Basel III standards. Basel III introduces a liquidity coverage ratio (LCR) which favours banks holding reserves over bonds.

2. The Fed funds system has been replumbed in the era of rate hikes with an expanded balance sheet. The Fed has needed to use a reverse repo facility to control rates without first draining excess liquidity from the interbank market.

3. Fed balance sheet reduction is likely to drain hard USDs from the system—and not just reserves. As the Fed shrinks its balance sheet and drains reserves from the system, in an environment where banks are incentivised to hold on to them, more money is likely to switch from deposits to government money-market funds. This is because banks are unlikely to pass on rate hikes in full to end savers, while government funds can offer full value because they place their proceeds directly with the Fed via its reverse repo facility. The system is likely to see a rebalancing between deposits and reverse repos. But this is not a zero-sum game, because the Fed is not a money dealer in normal times—cash held in reverse repo does not see the light of day again unless there is an emergency. So functionally, the system experiences a reduction in deposits.

4. The tax regime has shifted from global to territorial. Republican tax reform encourages multinational corporates to repatriate USDs held in offshore markets.

The cumulative effect of these changes is that USD liquidity in offshore markets is likely to shrink. And given that there are more USDs held outside of the US than within, this potentially has dramatic implications for the cost and availability of USD funding abroad in so-called eurodollar markets.

Interestingly, there is very limited evidence of USD liquidity tightening in cross-currency basis swap spreads. These spreads are wide by historical standards—but have not widened much in recent months. But perhaps the tightening is manifesting instead in LIBOR-OIS spreads.

It is also interesting that current and prospective Fed balance sheet reduction has not triggered a sustained increase in equity market volatility, nor corporate credit spreads. And given that pricing of volatility and corporate credit is more global than not, Australian market volatility and corporate credit spreads have not experienced a sustained uplift. Yet money market conditions are clearly tightening. In other words, different markets are reacting differently to central bank tightening efforts and the disconnect is becoming quite noticeable.

One possibility is that ongoing strong global growth, mixed in with very gradual central bank balance sheet reduction, is continuing to keep volatility and corporate credit spreads in check, even as liquidity conditions change. Another possibility is that perhaps the chain of causation is changing. Rather than market pricing driving interbank liquidity, perhaps we should be examining the possibility that changing liquidity conditions will eventually feed into market pricing. And perhaps the first warning sign is in the health of companies or economies dependent on USD funding.

Money market investors are not alone in ‘jumping at shadows’

Another disconnect worth monitoring is between equity market participants. A critical mass of investors still favours volatility suppression. But a critical mass of investors still also favours quality investing. Historically, quality factor performance has been highly positively correlated with equity market volatility. But since November 2016, quality stocks have significantly outperformed, despite generally low volatility. The decoupling is quite stark. It is almost as if stock pickers do not believe that a low volatility environment can be sustained as central banks tighten.

Interestingly, model residuals from our quality factor model are almost 30% correlated with residuals from our interbank credit spread model. In other words, money market investors are not alone in “jumping at shadows”. There are enough equity market investors to join them. The common ground is that neither group believes currently low market volatility readings.

Investment implications

If wide interbank credit spreads are sustained, we should expect to see:

1. Impaired monetary transmission. Historically, banks have not passed on RBA rate cuts in full when spreads are elevated.

2. Slower loan growth. Interbank credit spreads are a powerful and inverse leading indicator of bank net loan approvals, which in turn lead the stock of credit. Currently wide spreads are consistent with a sharp decline in loan approvals and slower credit growth.

In other words, there could be a tightening of financial conditions that is not a sign of good growth. This undermines the case for buying cheap cyclicals within the equity market. Indeed, value has tended to underperform as a style whenever interbank spreads have been wide. This is because wide spreads usually foreshadow de-leveraging risks, causing asset prices to drive fundamentals, rather than the other way around.

The key question is whether or not the widening of spreads will be sustained. Ordinarily, we would suggest not, as mean reversion should hold and spreads should revert to levels more consistent with a low-volatility environment. But money market participants are seeing tighter liquidity conditions globally with the fundamental story pointing to even more tightening to come. Also, stock pickers have been disregarding low volatility levels for some time by chasing quality (over value) stocks. We are extracting enough signals from the market to make us think that this time could indeed be different.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.