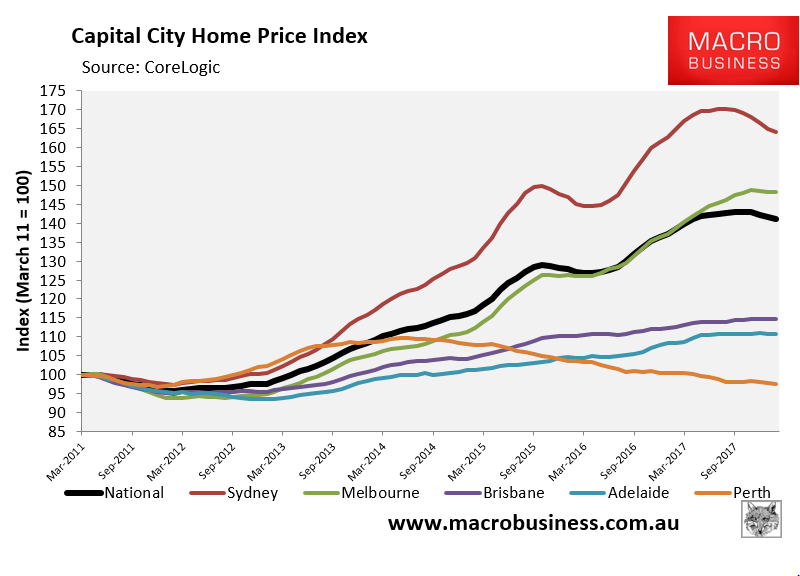

The trend lower in house prices has softened in recent weeks:

Leading indicators don’t suggest any kind of rebound in the offing but one wonders if the following is why we’ve seen a slowing melt, via the AFR:

A record $5 billion worth of mortgages sold in the December quarter of 2017 fell outside APRA’s minimum loan serviceability buffers, as major lenders fight for market share and bigger profits in tougher real estate markets.

That’s a more than a three-fold increase in the number of loans that are in breach of the standard since the Australian Prudential Regulation Authority wrote to them last March insisting on tighter standards, according to analysis of the regulator’s latest data.

Concerned regulators are expected to ask lenders why they have failed to meet its minimum expectations for prudent borrowing and adjust their criteria to reflect a changing lending environment.

The source appears to be Rate City which is not exactly authoritative. The story itself is from the usual realty cheerleaders so should also be taken with a grain of salt. Nonetheless, here’s the relevant material from the royal commission:

Ms Orr is now asking NAB’s Mr Gilfillan about the role of HEM is approving loan applications — HEM is the Household Expenditure Measure, created by the Melbourne Institute.Its a guesstimate of living expenses set at a modest level, not the kind of living expenses many middle and higher income households actually have.Like many other banks, Mr Gilfillan said NAB uses the HEM as a floor for living expenses. If a customer declares that their living expenses are below the HEM, then the banker looking at the loan should make further enquiries of the customer.At one point in time, from Mr Gilfillan’s evidence, it appears that a senior banker could approve a “serviceability waiver” where living expenses were set slightly below the HEM.It now appears that the HEM is an absolute floor on living expenses that can’t be lowered, but Mr Gilfillan’s evidence wasn’t crystal clear on this.Even with the HEM as an absolute floor, Mr Gilfillan admitted concern that a large number of loan applications, especially those coming through mortgage brokers, were declaring living expenses at or within 0.5 per cent of the HEM.That allows such loan applications to bypass any serviceability controls by not triggering the below-HEM red flag.To sum it up, basically a broker in the know (or even “the nice Mr Google” as Kenneth Hayne put it) can tell you the minimum amount of expenses you should declare to the bank to get the maximum loan size.

I recall that during the nationalisation of Citibank following in GFC it was branded a “rogue bank” by regulators after being at the centre of sequential financial crises. But what do you do if all four of your major banks are rogues as is being suggested by the royal commission? It has not come soon enough to apply the blowtorch to the perennially useless APRA.

Act now on enforcing the minimum loan serviceability buffers.

Not another letter.

Enforcement.