In his masterpiece, The World in Depression, Charles A. Kindleberger concludes the major cause of the Great Depression was a paralysis of leadership caused by the decline of the UK and the immaturity of the US. Neither was able to provide leadership and put themselves forward as the economy of last resort.

Kindelberger argues that during the 19th century, global growth was balanced by the UK’s decision to keep its economy open. When the home country boomed, capital flooded in to invest, but imports surged and offset the depletion of capital elsewhere. When the home country swooned, capital sought higher returns offshore, boosting growth elsewhere and therefore exports from the UK, softening the downturn. This mechanism prevented recessions from spiraling into depressions.

When the UK’s political and economic weight dramatically declined through the first 30 years of the 20th century so did this mechanism. And to make matters worse, when 1929 arrived the US was not ready to shoulder the burden of global leadership. When trouble came, it closed its trade borders. The globe was leaderless.

This analysis has two important points to make about our current situation. The first is that for the past couple of business cycles, the world has enjoyed a remarkably similar parallel in its macros settings. As the US boomed through the late nineties internet economy then again through its post-millennium housing bubble, capital flooded in, causing some to argue that the widening current account deficit was a result of a surplus of investment opportunities. In retrospect I think that’s been shown to be ‘new age’ thinking and all that was really happening was a credit bubble and over-consumption. Nonetheless, the result was an imports boom, which boosted the peripheral or emerging markets.

Then, as the US weakened, and monetary and fiscal policy was eased, capital flooded outwards to emerging markets, especially China. Since then the US has slowly recovered.

The second point to draw from Kindleberger is that as US economic power declines and China rises, the world finds itself at a similar impasse in political leadership. The US is in a diminished position to be the engine of global demand. Its debt burden has surpassed it, and its class wars have thrown up political regression. Equally clearly, China is not yet of sufficient size, power or sophistication to lead the world into a new economic era through an open economy.

The Kindelberger narrative for the Great Depression puts the onus on the rising power to avert a trade war. After all, the declining power can elect to take the pain for the greater good by ignoring its own demand shortfall but it pays a high price for doing so (and the politics of that are already on show). The choice for the rising power is easier. It needs to rebalance its demand not slow growth completely. Moreover, the surplus country stands to lose most if the tariff war does begin.

Except, in the case of China, that doesn’t quite hold does it? The magnitude and political structure of the place makes it VERY difficult for them to accept slowing growth.

Making this worse is the uncomfortable realisation that unlike during the Great Depression, we are not seeing a transfer of power within a civilisation, which was difficult enough. This time its a power shift to a new civilisation. Not to mention China has just appointed its first emperor in a few decades. Such historic shifts tend to happen through crisis and conflict. Empires hold onto power, rising states seek to seize it. It is only ever clear in hindsight where this process of transfer is up to.

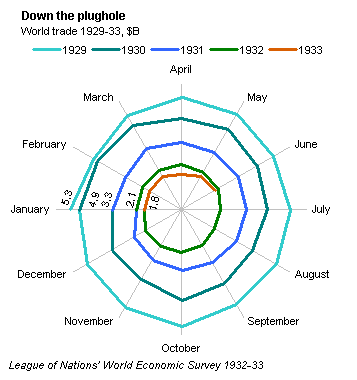

Thankfully, there are also differences to the geopolitics of the 1930s. We are not mid-crisis as the world was when protectionism took hold with Smoot-Hawley in 1930:

That means any impact from tariffs is likely to be more chronic than acute. That said, given we’re late cycle things could get quickly out of control if we are overtaken by another bust. At least in the meantime there is an opportunity to head off a deteriorating trade system.

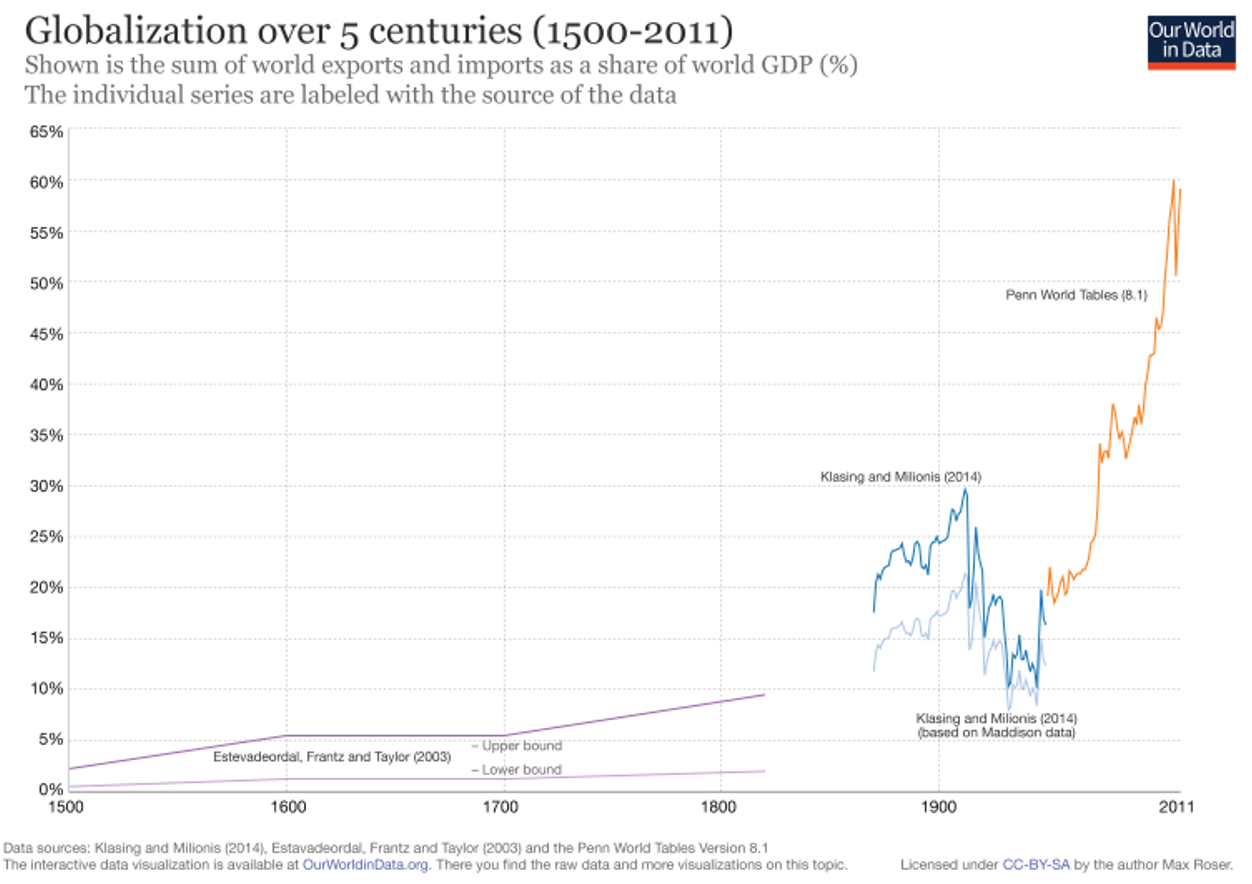

Another difference today is that the normatives and structures of multilateral global trade are much more entrenched than they were in the 1930s and the role of trade immensely more significant:

That bolsters the system significantly against attack versus the 1930s experience, even from its great progenitor.

A third difference is that the US is in a position to provide an immediate and correctional force to its Chinese trade deficit via its oil boom which could capture all Chinese demand growth over the next decade.

Still, the parallels between today and the 1930s are unsettling enough to take seriously.

Join us today for the MBFund webinar: Will Trump trade wars doom the cycle? It is a live broadcast (with Q&A) starting at 12.30AEST in which we will discuss the implications for asset prices.

Register here.